|

시장보고서

상품코드

1630184

내화학성 코팅 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Chemical Resistant Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

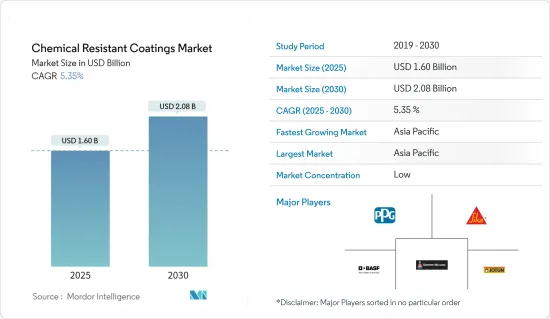

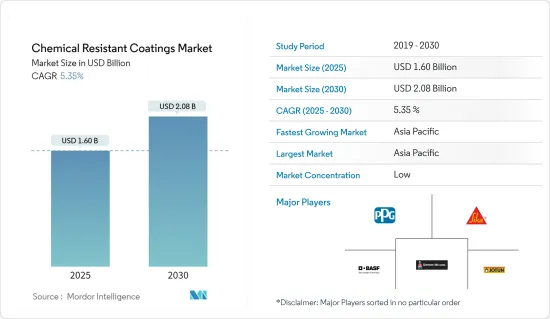

내화학성 코팅 시장 규모는 2025년에 16억 달러로 추정되며, 예측 기간(2025-2030년) 동안 5.35%의 CAGR로 2030년에는 20억 8,000만 달러에 달할 것으로 예상됩니다.

COVID-19로 인해 내화학성 코팅 시장은 부정적인 영향을 받고 있으며, 2020년 상반기에는 봉쇄 조치와 여행 제한으로 인해 대부분의 산업이 상반기 동안 중단되었습니다. 석유 및 가스 수요는 전 세계 각국 정부의 규제로 인해 크게 감소했습니다. 그러나 하반기에는 대부분의 산업이 최소한의 생산능력으로 운영되고 있으며, 여행 제한 해제와 가동 중단 완화는 조사 대상 시장에 밝은 신호입니다.

주요 하이라이트

- 단기적으로는 아시아태평양의 인프라 구축과 산업화 활동의 확대, 아시아태평양 및 북미의 석유 및 가스 활동의 확대가 시장 성장의 주요 요인입니다.

- 반면, 복잡한 제조 공정과 높은 투자비용은 시장 성장에 걸림돌이 될 것으로 예상됩니다.

- 리그닌 기반 폴리우레탄의 개발은 시장에 성장 기회를 제공할 것으로 예상됩니다.

- 예측 기간 동안 아시아태평양이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

내화학성 코팅 시장 동향

석유와 가스 부문이 시장을 독점

- 석유 및 가스 부문은 내화학성 코팅 시장의 주요 최종사용자 중 하나입니다. 이 부문은 사업 운영에 고온 환경이 수반되기 때문에 본질적으로 내화학성이 요구됩니다. 또한, 고온 외에도 코팅은 금속 및 철골 구조물이 습하고 습한 기후 조건에 노출되기 때문에 부식 및 화학제품으로부터 보호하기 위해 코팅이 사용됩니다.

- 해양 석유 및 가스 생산은 가장 가혹한 조건 중 하나입니다. 따라서, 그곳에서 사용되는 코팅 시스템도 비슷한 조건을 충족시켜야 합니다.

- 해양에서는 침투하는 자외선에 장시간 노출되고 거친 바닷물과 지속적으로 접촉하기 때문에 내화학성 코팅의 필요성이 증가하고 있습니다.

- 미국은 지난 6 년 연속 세계 최고의 원유 생산국 지위를 유지하고 있으며, 2023년에는 1,290 만 배럴/일(b/d)의 기록적인 평균 원유 생산량을 달성하여 2019년에 세운 이전 기록을 넘어 섰으며, 2023년 12월 미국의월 평균 원유 생산량은 1,300 만 배럴/일(b/d)을 돌파했습니다. 330만 배럴/일(b/d)을 돌파하여 월간 최고치를 기록했습니다.

- 텍사스 서부와 뉴멕시코 동부에 걸쳐 있는 Permian Basin은 최근 미국 전체 원유 및 천연가스 생산량 급증에 있어 매우 중요한 역할을 하고 있습니다. 미국은 현재 하루 약 1,350만 배럴의 원유를 생산하고 있습니다. 엑손모빌은 텍사스 및 뉴멕시코의 파미안 유역에서 생산량을 늘리기 위해 셰일 대기업인 파이오니어 내추럴 리소스(Pioneer Natural Resources)를 약 600억 달러에 인수할 계획이며, 셰브론(Chevron)은 Hess를 530억 달러에 인수할 계획입니다. Hess를 530억 달러에 인수할 계획입니다.

- 인도에서는 2024년 1월 Oil and Natural Gas Corporation(ONGC)이 벵골만 연안의 크리슈나 고다발리 분지에 위치한 심해 광구에서 석유 생산을 시작했습니다. 이 광구의 나머지 유전과 가스전은 2024년 중반까지 가동될 예정이며, 최대 생산량은 하루 4만 5,000배럴의 석유와 1,000만 입방미터의 가스를 생산할 것으로 예상됩니다.

- 전 세계 확인된 석유 매장량의 약 17%를 보유한 사우디아라비아는 세계 2위의 확인된 석유 매장량을 자랑하며, 가장 중요한 석유 순수출국입니다. 석유 수출로 얻은 수익은 인프라 현대화, 일자리 창출, 사회지표 개선에 사용되어 왔습니다. 주요 종합 에너지 및 화학 기업인 사우디 아람코는 업스트림, 미드스티림, 다운스트림 부문에서 폭넓게 사업을 전개하고 있습니다.

- 2023년 3월, Aramco는 2023년 자본 지출 목표를 450억-550억 달러로 발표했습니다. 이 계획은 2027년까지 석유 생산량을 하루 1,300만 배럴까지 늘리는 것을 목표로 했습니다. 그러나 2024년 1월 사우디 에너지부의 명령으로 인한 혼란으로 Aramco는 원유 생산능력을 하루 1,200만 배럴에서 1,300만 배럴로 늘리려던 계획을 중단했습니다.

- 따라서 석유 및 가스 부문의 성장은 예측 기간 동안 조사 대상 시장의 수요를 증가시킬 것으로 예상됩니다.

아시아태평양 시장을 장악하고 있는 중국

- 아시아태평양에서 중국은 GDP 기준 최대 경제대국입니다. 중국은 주택 및 인프라 프로젝트에 대한 막대한 투자로 아시아태평양의 건설 상황을 지배하고 있습니다.

- 중국 국가통계국 데이터에 따르면 2023년 건설 부문의 GDP 기여율은 약 6.8%였습니다.

- 2024년 1월 주택도시농촌개발부가 발표한 바에 따르면 2023년 중국은 도시 노후 주택 5만 3,700채의 개보수 프로젝트를 실시해 897만 가구에 혜택을 제공했습니다. 이 개조 프로젝트는 1년 동안 2,400억 위안(약 337억 8,000만 달러)에 달하는 막대한 투자를 유치했습니다.

- 최근 몇 년 동안 대형 건설업체(유럽연합)의 중국 진출은 이 산업의 성장을 더욱 촉진하고 있습니다. 또한 중국은 2030년까지 약 13조 달러를 건축에 투자할 것으로 예상됩니다.

- 국가에너지국에 따르면, 2023년 중국의 원유 및 천연가스 총 생산량은 석유 환산 기준 3억 9,000만 톤을 넘어 사상 최대치를 기록할 것으로 예상했습니다. 원유 생산량은 2억 800만 톤을 넘어 2022년 대비 300만 톤 이상 증가할 것으로 예상했습니다. 또한 중국의 천연가스 생산량은 지난 7년간 매년 100억 입방미터씩 꾸준히 증가하여 지난해에는 2,300억 입방미터에 달했습니다.

- 중국 국영석유회사(NOC)는 2021-2025년까지 5년간 시추 및 유정 서비스에 1,200억 달러 이상을 투자할 것으로 예상됩니다. 중국의 석유 및 가스 수요 증가로 인해 향후 몇 년 동안 높은 수준의 시추 활동이 확인될 것으로 예상됩니다.

- 위의 요인으로 인해 아시아태평양의 내화학성 코팅에 대한 수요는 예측 기간 동안 크게 증가할 것으로 예상됩니다.

내화학성 코팅 산업 개요

내화학성 코팅 시장은 세분화되어 있으며, 주요 다국적 기업들이 진출해 있습니다. PPG Industries Inc., Sika AG, The Sherwin-Williams Company, BASF SE, Jotun 등이 주요 진입 기업입니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 아시아태평양과 북미의 석유 및 가스 활동 확대

- 아시아태평양의 인프라 정비와 산업화 진전

- 성장 억제요인

- 복잡한 생산 공정과 높은 투자 비용

- 기타 성장 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

- 수지

- 에폭시 수지

- 폴리에스테르

- 불소수지

- 폴리우레탄

- 기타

- 기술

- 100% 고체

- 용제형

- 분말

- 수성

- 최종 이용 산업

- 화학

- 석유 및 가스

- 해양

- 건설 인프라

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 카타르

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 시장 점유율(%)/순위 분석

- 주요 기업의 전략

- 기업 개요

- BASF SE

- Akzonobel NV

- Daikin Industries Ltd

- Hempel AS

- Jotun

- Kansai Paint Co. Ltd

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

- VersaFlex Incorporated

제7장 시장 기회와 향후 동향

- 리그닌계 폴리우레탄 개발

- 기타 기회

The Chemical Resistant Coatings Market size is estimated at USD 1.60 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 5.35% during the forecast period (2025-2030).

Due to COVID-19, the chemical resistant coatings market has been negatively impacted. Due to the imposed lockdowns in the first half of 2020, and travel restrictions, the industries were shut for the most part of the first half of the year. The Oil and gas demand has fallen drastically due to the restrictions imposed by the governments across the globe. However, in the second half of the year most of the industries were working at a minimum capacity, and the lifting of travel restrictions and relaxation of the lockdowns are a positive sign for the market studied.

Key Highlights

- Over the Short term, the major factor driving the growth of the market studied include growing infrastructure and industrialization activities in Asia-Pacific region and expansion in oil and gas activities in Asia-pacific and North America region.

- On the flipside, complex production process and high investment cost are expected to hinder the growth of the market studied.

- The development of lignin-based polyurethanes is expected to give the market a chance to grow.

- Asia-Pacific is expected to hold the most considerable market share over the forecast period.

Chemical Resistant Coatings Market Trends

Oil and Gas Segment to Dominate the Market

- Oil and gas sector is one of the major end-users for the chemical resistant coatings market. The sector essentially requires chemical resistance, owing to a high temperature environment in its business operations. In addition, apart from high-temperature, the coating is used to prevent metal and steel structures from corrosion and chemicals, as they are exposed to moist and damp climatic conditions.

- Offshore oil and gas production has some of the most demanding conditions. Therefore, coating systems used in it are to be equipped likewise.

- Offshore, prolonged exposure to penetrating UV rays and constant contact with rough seawater increases the need for chemical-resistant coatings.

- The United States has maintained its position as the leading crude oil producer globally for the past six consecutive years. In 2023, the country achieved a record-breaking average crude oil production of 12.9 million barrels per day (b/d), surpassing the previous record set in 2019. In December 2023, the average monthly crude oil production in the United States reached a monthly record high, surpassing 13.3 million barrels per day (b/d).

- The Permian Basin, spanning western Texas and eastern New Mexico, has played a pivotal role in driving the surge in total crude oil and natural gas production across the United States in recent years. The United States is currently producing an unprecedented volume of oil, reaching approximately 13.5 million barrels per day. In addition, major energy corporations are consolidating their operations to boost production from the Permian Basin in Texas and New Mexico. ExxonMobil intends to acquire the shale giant Pioneer Natural Resources for nearly USD 60 billion, while Chevron is planning to purchase Hess for USD 53 billion.

- in Indua, in January 2024, the state-run Oil and Natural Gas Corporation (ONGC) initiated oil production from its deep-water block in the Krishna-Godavari basin off the coast of the Bay of Bengal. The block's remaining oil and gas fields are anticipated to commence operations by mid-2024, with peak production estimated at 45,000 barrels of oil per day and over 10 million metric standard cubic meters per day of gas.

- With approximately 17% of the world's proven petroleum reserves, Saudi Arabia ranks among the most significant net petroleum exporters, boasting the second-largest proven oil reserves globally. Proceeds generated from oil exports have been used to modernize infrastructure, create employment, and improve social indicators. Saudi Aramco, a leading integrated energy and chemicals company, operates extensively across upstream, midstream, and downstream segments.

- In March 2023, Aramco unveiled a capital expenditure goal of USD 45-USD 55 billion for FY 2023, representing its most significant capital spending plan. This initiative aimed to support an increase in oil production to 13 million barrels per day by 2027. However, the disruption caused by the Saudi Ministry of Energy's order in January 2024 prompted Aramco to halt its plans to elevate crude production capacity from 12 million to 13 million barrels daily

- Therefore, the growing oil and gas sector is expected to boost the demand for the market studied, during the forecast period.

China to Dominate the Asia-Pacific Market

- In Asia-Pacific, China is the largest economy, in terms of GDP. China is the dominant force in the Asia-Pacific construction landscape, fueled by substantial investments in residential and infrastructure projects.

- Data from China's National Bureau of Statistics highlights that in 2023, the construction sector contributed approximately 6.8% to the nation's GDP.

- In 2023, China undertook renovation projects for 53,700 aging residential communities in urban areas, benefiting 8.97 million households, as the Ministry of Housing and Urban-Rural Development reported in January 2024. These renovation endeavors attracted hefty investments of nearly CNY 240 billion (around USD 33.78 billion) for the year.

- In the recent years, the entry of major construction players (from the European Union) in China has further fueled the growth of this industry. Moreover, China is expected to spend nearly USD 13 trillion on building by 2030.

- According to the National Energy Administration, China's combined crude oil and natural gas production in 2023 was forecasted to exceed 390 million tons of oil equivalent, reaching a new historical high. Crude oil output exceeded 208 million tons, indicating a growth of over 3 million tons compared to 2022. Additionally, China's natural gas production steadily increased by 10 billion cubic meters annually for the past seven years, reaching 230 billion cubic meters in the preceding year.

- China's national oil companies (NOCs) are expected to splurge more than USD 120 billion on drilling and well services in the five years between 2021 and 2025. Due to China's growing demand for oil and gas, the country is expected to witness a high level of drilling activity in years to come.

- Owing to above-mentioned factors, the demand for chemical resistant coatings in Asia-Pacific is expected to increase significantly over the forecast period.

Chemical Resistant Coatings Industry Overview

The chemical resistant coatings market is fragmented, with the presence of majorly multi-national players. Some of the major players include PPG Industries Inc., Sika AG, The Sherwin-Williams Company, BASF SE, and Jotun, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Expansion of Oil and Gas Activities in APAC and North America

- 4.1.2 Growing Infrastructure and Industrialization in the Asia-Pacific Region

- 4.2 Restraints

- 4.2.1 Complex Production Process and High Investment Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin

- 5.1.1 Epoxy

- 5.1.2 Polyester

- 5.1.3 Fluoropolymers

- 5.1.4 Polyurethane

- 5.1.5 Other Resins

- 5.2 Technology

- 5.2.1 100% Solids

- 5.2.2 Solvent Borne

- 5.2.3 Powder

- 5.2.4 Water-borne

- 5.3 End-user Industry

- 5.3.1 Chemical

- 5.3.2 Oil and Gas

- 5.3.3 Marine

- 5.3.4 Construction and Infrastructural

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Qatar

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Akzonobel NV

- 6.4.3 Daikin Industries Ltd

- 6.4.4 Hempel AS

- 6.4.5 Jotun

- 6.4.6 Kansai Paint Co. Ltd

- 6.4.7 PPG Industries Inc.

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 The Sherwin-Williams Company

- 6.4.11 VersaFlex Incorporated

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Lignin-based Polyurethanes

- 7.2 Other Opportunities