|

시장보고서

상품코드

1851613

스프레이 폴리우레탄 폼 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Spray Polyurethane Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

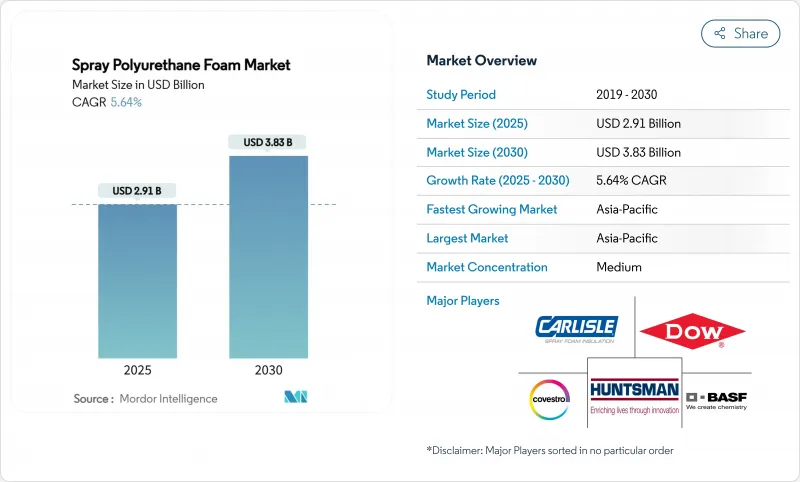

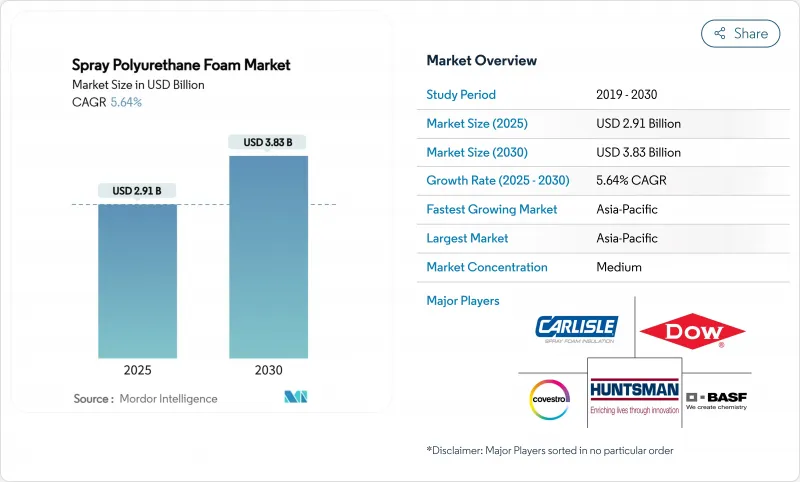

스프레이 폴리우레탄 폼 시장 규모는 2025년에 29억 1,000만 달러로 추정되고, 2030년에는 38억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 5.64%를 나타낼 전망입니다.

이 확대는 건축 에너지 규제가 강화되고, 낮은 GWP 규제가 시행되고, 콜드체인 투자가 가속화되고, 보다 고가치의 단열재 수요가 촉진됨으로써 일어납니다. 제조업체는 2025년 1월 1일에 시작된 EPA 기술 전환 제한 규칙 epa.gov를 준수하기 위해 고 GWP HFC를 하이드로플루오로올레핀 및 기타 차세대 발포제로 전환하고 있습니다. 설치업체 간의 통합, 리노베이션 활동 활성화, ESG에 연동된 자금 조달은 주택, 상업 및 산업 프로젝트의 전반적인 기세를 더욱 강화하는 반면, CO2 기반 폴리올의 혁신은 공급업체에게 장기적인 지속가능성을 높여줍니다.

세계의 스프레이 폴리우레탄 폼 시장 동향과 인사이트

엄격한 건축 에너지 규범과 리노베이션 의무화

2024년 국제 에너지 절약 기준에서는 폐쇄형 셀 스프레이 폼이 권장되는 에어 배리어 솔루션으로 자리매김되었으며, 건축가는 더 높은 R 값과 습기 방지 대책을 지정하도록 강제됩니다. 캘리포니아의 2023년 기준과 플로리다의 2026년 기준 갱신은 모두 리노베이션 허가를 간소화하고 철거 비용을 낮추고 특히 저경사 상업용 지붕 수요를 가속화하고 있습니다. 이러한 규칙 변경은 리노베이션 가능한 기반을 확대하고, 하이브리드 단열재 조립을 장려하며, 계약자를 2성분 시스템에 유리한 트레이닝과 설비 투자의 강화로 향하게 합니다.

온실가스 배출에 대한 우려 증가

기업의 넷 제로 목표는 건물 소유자의 비용 목표와 융합하며, EPA의 에너지 스타 프로그램에 따르면 냉난방 에너지를 최대 10% 절감하는 스프레이 폼의 능력이 강조되고 있습니다. Installed Building Products는 생산량을 크게 증가시키면서 2020년 이후 스프레이 폼 사용으로 인한 CO2 배출량을 55% 줄였다고 보고하여 이 기술이 배출량에서 성장을 분리한다는 것을 보여줍니다. 존스 맨빌과 같은 제조업체는 에너지 절약 제품의 생산량이 증가하더라도 절대 배출량은 2자리 감소를 기록하고 지속가능성과 수익성의 무결성을 강조했습니다.

유리 섬유와 셀룰로오스의 경쟁

비용에 중점을 둔 주택 건설업자는 수년간의 시산업체 네트워크와 낮은 설비 요구사항을 뒷받침해 왔으며 여전히 유리 섬유 방망이를 기본으로 하고 있습니다. Home Innovation Research Labs의 데이터에 따르면, 집주택이 성장하고 재료비가 절감됨에 따라 스프레이 폼의 점유율은 11%에서 8% 후퇴하여 가격에 대한 민감성이 돋보였습니다. 유리 섬유 제조업체는 고밀도 제품을 제공함으로써 성능 차이를 줄이고 셀룰로오스는 재활용 컨텐츠의 브랜드 힘을 활용하여 환경 의식이 높은 소비자에게 호소하고 있습니다. 따라서 스프레이 폼 공급업체는 수명 주기의 에너지 절약에 대한 가치 메시징을 보다 선명하게 하여 선행 투자 금액 증가를 극복해야 합니다.

부문 분석

2024년 시장 세분화에서 2액형 고압 시스템은 37.62%의 점유율을 차지하며, 이는 일관된 현장 혼합, 우수한 R-값 및 상업 건축에서 법규제의 수용을 반영했습니다. BASF가 쇼에에 신설한 이소시아네이트와 TPU의 라인은 현지에서공급 체제를 강화하고, 아시아태평양에서 이 부문의 우위성을 강화하고 있습니다. 반경질 스프레이 폼은 인프라 프로젝트가 진동과 온도 변화에 대한 유연성을 필요로 하기 때문에 CAGR 7.19%를 나타낼 전망입니다. 일액캔은 소규모 프로젝트의 편의성에 대응하고, 저압 키트는 발열을 억제하는 것이 중요한 섬세한 기재에 대응합니다.

통합 브랜드의 추진은 경쟁 전략을 보여준다 : Holcim의 Enverge(R) 라벨은 Gaco(TM)와 SES(TM) 포트폴리오를 통합하여 시산업체에게 지붕, 벽 및 특수 형태의 단일 사양 경로를 제공합니다. 제품의 다양화에 의해 태양광 발전 대응의 지붕이나 교량의 덱을 대상으로 한 반경질 혁신, 내화성 규제를 대상으로 한 분기 주입 시스템 등, 크로스셀링의 기회가 넓어지고 있습니다. 광범위한 카탈로그 및 지역 기술 센터를 유지하는 공급업체는 사양의 승리를 잡기위한 최상의 위치를 유지합니다.

스프레이 폴리우레탄 폼 시장 보고서는 제품 유형(2액 고압 스프레이 폼, 2액 저압 스프레이 폼, 기타), 용도(단열, 방수, 석면 밀봉, 실란트, 기타 용도), 최종 이용 산업(주택, 상업 빌딩, 산업, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분

지역 분석

아시아태평양은 2024년 스프레이 폴리우레탄 폼 시장 점유율의 48.19%를 차지했으며, 급속한 도시화, 공장 확장, 에너지 코드 채용으로 CAGR 7.66%를 나타낼 것으로 예측됩니다. 한편 인도의 HVAC 부문은 2030년까지 연평균 복합 성장률(CAGR) 15.8%로 300억 달러에 달하고, 건물 외벽 업그레이드 수요가 높아집니다. 일본과 한국은 지진지대에서 엄격한 외벽 요건을 부과하고 있으며, 스프레이 폼과 같은 경량이고 밀착성이 높은 단열재가 지지되고 있습니다. ASEAN 국가들은 수산물과 백신 보관을 위한 콜드체인 능력을 확대하고 지역 수요를 끌어올립니다. BASF의 여러 해에 걸쳐 195억 달러의 아시아태평양 투자 계획은 이 지역의 흡수 능력에 대한 공급업체의 자신감을 보여줍니다.

북미는 성숙하면서도 안정적인 시장으로 연방 정부의 HFC 단계적 폐지가 컴플라이언스를 조화시켜 사양의 복잡성을 낮게 억제하고 있습니다. 캐나다의 추운 기후는 후층 다락방 스프레이 폼의 사용을 유지하는 반면, 멕시코는 니어 쇼어링의 기세와 자동차 제조업의 성장으로 세계 4위의 폴리우레탄 소비국으로 부상하고 있습니다. 건설업자 간의 통합은 미국과 캐나다 전역에서 미국과 미국의 건설업체가 외벽 솔루션을 표준화할 수 있게 해주며 탑 빌드의 네트워크 확장으로 강화됩니다.

유럽의 넷 제로 지령과 리노베이션의 물결은 거시 경제가 침체하고 있음에도 불구하고 수요를 자극합니다. 디이소시아네이트 훈련 규칙은 마찰을 초래하지만, 궁극적으로 견고한 EHS 프로그램을 가진 자본력있는 제조업체에게 유리합니다. 코베스트로의 DreamResource 프로젝트는 CO2를 원료로 20% 함유하는 경질 폼을 도입하여 순환 화학에서 유럽의 리더십을 보여줍니다. 리에주 대학은 70-90%의 바이오 베이스 원료를 사용한 이소시아네이트 프리폼을 개발하여 지역 산학 연계를 강조하고 있습니다. 브라질, 사우디아라비아, 아랍에미리트(UAE)에서는 상업용 대형 프로젝트에 빠르게 스프레이 폼을 채택하여 미래 수량 증가를 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 건축 에너지 규제와 개수 의무

- 온실가스 배출에 대한 우려 증가

- 콜드체인과 냉장 물류의 성장

- SPF 업그레이드를 위한 ESG 연동 그린본드 파이낸스

- 솔라 대응 지붕용 하이 리프트 폼 수요

- 시장 성장 억제요인

- 유리 섬유와 셀룰로오스의 경쟁

- 디이소시아네이트에 관한 규제와 제한

- HFO 블로잉제공급 변동

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 2액형 고압 스프레이 폼

- 2액형 저압 스프레이 폼

- 1액형 폼(OCF)

- 반경질 스프레이 폼

- 용도별

- 단열

- 방수

- 석면 캡슐화

- 실란트

- 기타 용도(콘크리트 리프팅/공극 충전 등)

- 최종 이용 산업별

- 주택용 건물

- 상업용 건물

- 산업 및 인프라

- 농업 및 특수 분야

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- BASF

- Accella Polyurethane Systems

- Carlisle Spray Foam Insulation

- Covestro AG

- Dow

- FOAM-LOK(Firestone)

- GACO

- Huntsman Corporation LLC

- ISOTHANE LTD

- Johns Manville

- NCFI Polyurethanes

- Rhino Linings

- SOPREMA Canada.

- SWD Urethane

제7장 시장 기회와 향후 전망

KTH 25.11.13The Spray Polyurethane Foam Market size is estimated at USD 2.91 billion in 2025, and is expected to reach USD 3.83 billion by 2030, at a CAGR of 5.64% during the forecast period (2025-2030).

This expansion occurs as building-energy codes tighten, low-GWP regulations take effect, and cold-chain investment accelerates, driving higher-value insulation demand. Manufacturers are swapping high-GWP HFCs for hydrofluoroolefin and other next-generation blowing agents to comply with the EPA's Technology Transitions Restrictions rule that began on 1 January 2025 epa.gov. Consolidation among installers, growing retrofit activity, and ESG-linked financing further reinforce momentum across residential, commercial, and industrial projects, while innovation in CO2-based polyols positions suppliers for long-term sustainability gains.

Global Spray Polyurethane Foam Market Trends and Insights

Strict Building-Energy Codes and Retrofit Mandates

The 2024 International Energy Conservation Code elevates closed-cell spray foam as a preferred air-barrier solution, compelling architects to specify higher R-values and moisture control measures. California's 2023 standards and Florida's 2026 code update both streamline retrofit approvals, lowering removal costs and accelerating demand, particularly for low-slope commercial roofs These rule changes widen the retrofit addressable base, encourage hybrid insulation assemblies, and push contractors toward more training and equipment investment that favors two-component systems.

Rising Concerns Over GHG Emissions

Corporate net-zero goals merge with building-owner cost targets, highlighting spray foam's ability to cut heating-and-cooling energy by up to 10% according to the EPA's Energy Star program. Installed Building Products reported a 55% CO2 reduction from spray foam use since 2020 while materially increasing output, showing the technology's decoupling of growth from emissions. Manufacturers such as Johns Manville logged double-digit drops in absolute emissions even as energy-saving product volumes rose, underscoring alignment between sustainability and profitability.

Competition from Fiberglass and Cellulose

Cost-focused residential builders still default to fiberglass batts, supported by long-standing installer networks and low equipment requirements. Home Innovation Research Labs data showed an 11% to 8% pullback in spray foam share amid multifamily growth and material cost saving, highlighting price sensitivity. Fiberglass makers are narrowing performance gaps with higher-density offerings, while cellulose leverages recycled content branding to appeal to eco-minded consumers. Spray foam suppliers must therefore sharpen value messaging around lifecycle energy savings to overcome higher upfront spend.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Cold-Chain and Refrigerated Logistics

- ESG-Linked Green-Bond Financing for SPF Upgrades

- Regulations and Restrictions on Di-Isocyanates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment anchored by two-component high-pressure systems held a 37.62% spray polyurethane foam market share in 2024, reflecting consistent on-site mixing, superior R-values, and code acceptance in commercial construction. BASF's new isocyanate and TPU lines in Zhanjiang strengthen local supply chains, reinforcing the segment's dominance in Asia-Pacific. Semi-rigid spray foam is expanding at a 7.19% CAGR as infrastructure projects need flexibility for vibration and temperature swings. One-component cans address small-project convenience, while low-pressure kits cover sensitive substrates where reduced exothermic heat is critical.

A push for integrated brands illustrates competitive strategy: Holcim's Enverge(R) label merges Gaco(TM) and SES(TM) portfolios, giving installers a single specification path for roof, wall, and specialty foams. Product diversification frames cross-selling opportunities, with semi-rigid innovations aimed at solar-ready roofs and bridge decks, and intumescent-infused systems targeting fire-resistance regulations. Suppliers that maintain broad catalogs and regional technical centers remain best positioned to seize specification wins.

The Spray Polyurethane Foam Market Report is Segmented by Product Type (Two-Component High-Pressure Spray Foam, Two-Component Low-Pressure Spray Foam, and More), Application (Insulation, Waterproofing, Asbestos Encapsulation, Sealant, Other Application), End-Use Industry (Residential Buildings, Commercial Buildings, Industrial and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific captured 48.19% of spray polyurethane foam market share in 2024 and is forecast to climb at 7.66% CAGR, driven by rapid urbanization, factory expansions, and energy-code adoption. China's real-estate slowdown redirects stimulus toward urban renewal, boosting retrofit insulation spend, while India's HVAC sector is set to hit USD 30 billion by 2030 on a 15.8% CAGR pathway, raising demand for building envelope upgrades. Japan and South Korea enforce stringent envelope requirements in seismic zones, favoring lightweight, high-adhesion insulation such as spray foam. ASEAN nations expand cold-chain capacity for seafood and vaccine storage, pulling regional demand upward. BASF's multi-year USD 19.5 billion Asia-Pacific investment plan exemplifies supplier confidence in the region's absorption capacity.

North America remains a mature but stable arena where federal HFC phase-outs harmonize compliance and keep specification complexity low. Canada's cold climates sustain thick-layer attic spray foam usage, while Mexico emerges as the world's fourth-largest polyurethane consumer on near-shoring momentum and automotive manufacturing growth. Consolidation among contractors enables national builders to standardize envelope solutions across the US and Canada, reinforced by TopBuild's network expansion.

Europe's net-zero directives and renovation wave stimulate demand despite tepid macro-economics. Di-isocyanate training rules introduce friction but ultimately favor well-capitalized manufacturers with robust EHS programs. Covestro's DreamResource project introduces rigid foam containing 20% CO2 as feedstock, demonstrating European leadership in circular chemistry. University of Liege advances isocyanate-free foams with 70-90% biobased content, underscoring regional academic-industry collaboration. In South America and the Middle East and Africa, energy-efficiency codes are tightening gradually; early movers in Brazil, Saudi Arabia, and the UAE adopt spray foam in commercial megaprojects, signaling future volume uplift.

- BASF

- Accella Polyurethane Systems

- Carlisle Spray Foam Insulation

- Covestro AG

- Dow

- FOAM-LOK (Firestone)

- GACO

- Huntsman Corporation LLC

- ISOTHANE LTD

- Johns Manville

- NCFI Polyurethanes

- Rhino Linings

- SOPREMA Canada.

- SWD Urethane

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict Building-Energy Codes and Retrofit Mandates

- 4.2.2 Rising Concerns over GHG Emissions

- 4.2.3 Growth in Cold-Chain and Refrigerated Logistics

- 4.2.4 ESG-linked green bond financing for SPF upgrades

- 4.2.5 High-lift Foam Demand for Solar-Ready Roofs

- 4.3 Market Restraints

- 4.3.1 Competition from Fiberglass and Cellulose

- 4.3.2 Regulations and Restrictions on Di-isocyanates

- 4.3.3 HFO Blowing-agent Supply Volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Two-Component High-Pressure Spray Foam

- 5.1.2 Two-Component Low-Pressure Spray Foam

- 5.1.3 One-Component Foam (OCF)

- 5.1.4 Semi-Rigid Spray Foam

- 5.2 By Application

- 5.2.1 Insulation

- 5.2.2 Waterproofing

- 5.2.3 Asbestos Encapsulation

- 5.2.4 Sealant

- 5.2.5 Other Application (Concrete Lifting / Void Filling, etc.)

- 5.3 By End-use Industry

- 5.3.1 Residential Buildings

- 5.3.2 Commercial Buildings

- 5.3.3 Industrial and Infrastructure

- 5.3.4 Agriculture and Specialty

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Accella Polyurethane Systems

- 6.4.3 Carlisle Spray Foam Insulation

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 FOAM-LOK (Firestone)

- 6.4.7 GACO

- 6.4.8 Huntsman Corporation LLC

- 6.4.9 ISOTHANE LTD

- 6.4.10 Johns Manville

- 6.4.11 NCFI Polyurethanes

- 6.4.12 Rhino Linings

- 6.4.13 SOPREMA Canada.

- 6.4.14 SWD Urethane

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment