|

시장보고서

상품코드

1851660

파일 무결성 모니터링(FIM) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)File Integrity Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

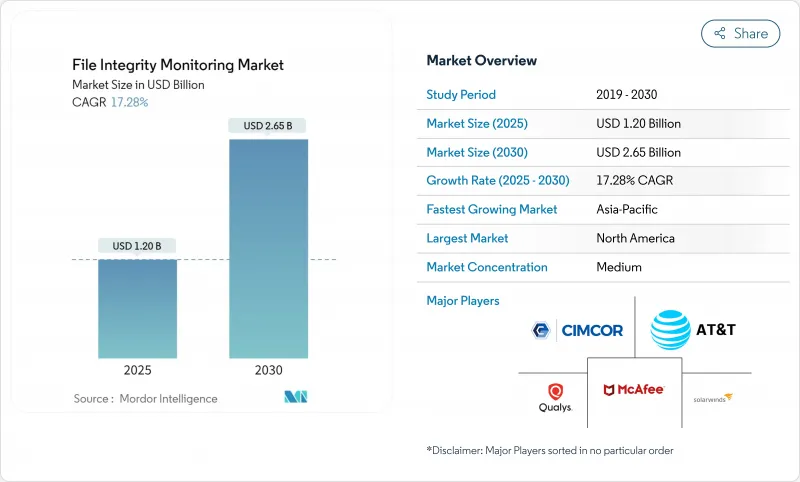

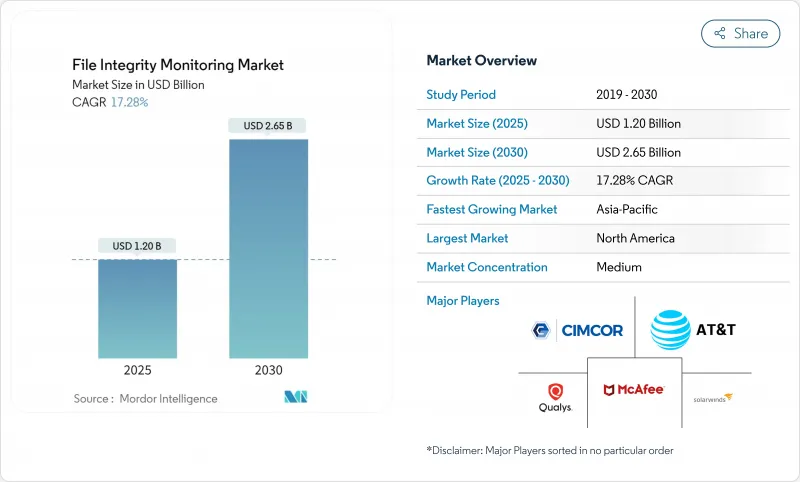

파일 무결성 모니터링 시장은 2025년에 12억 달러로 추정되고, 2030년에는 26억 5,000만 달러에 이를 것으로 예측되며, CAGR 17.28%로 견조한 성장세를 기록할 전망입니다.

그 기세는 세계적인 사이버 보안 규제 강화, 클라우드 워크로드의 급속한 확대, 경보 피로를 완화하는 AI 주도 보안 분석의 융합에 기인하고 있습니다. 기업은 횡방향 공격이나 랜섬웨어에 대해 더 이상 경계 중심의 제어로는 충분하지 않기 때문에 실시간 변화 감지를 선호합니다. 또한 파일 무결성 모니터링을 최소한의 권한으로 실시하기 위한 기반으로 간주하는 제로 트러스트 프레임워크에 대한 세계적인 축족도 수요의 추풍이 되고 있습니다. 업종에 상관없이 사이버 보험에 대한 가입 요건 증가와 운영 회복력에 대한 이사회 수준의 감시가 최신 클라우드 네이티브 감시 플랫폼의 채용을 더욱 강화하고 있습니다.

세계의 파일 무결성 모니터링 시장 동향 및 인사이트

규제 준수 의무화

금융기관은 2025년 5월 뉴욕 DFS 파트 500의 개정을 통해 특권 액세스 모니터링 및 다중 요소 인증을 의무화하고 감사 추적의 증거로 파일 무결성 시스템이 필수적입니다. 연방 에너지 규제위원회는 벌크 전기 시스템의 운영 기술에 내부 모니터링을 확대하는 NERC CIP-015-1을 승인했습니다. SEC의 사건 공개 규칙에서 상장 기업은 중요한 사이버 이벤트를 4영업일 이내에 보고해야 하며 실시간 변화 감지 요구사항이 요구됩니다. 또한 결제 회사는 2025년 3월까지 PCI DSS 4.0의 로깅 및 모니터링 기준을 충족해야 하며, 파일 무결성 관리를 핵심 인프라로 자리매김하고 있습니다.

데이터 침해 증가 및 고도화

세계 정보 유출의 평균 비용은 2024년에 488만 달러로 상승했고, 2025년에는 500만 달러에 이를 것으로 예상되며, 의료 인시던트의 피크는 977만 달러입니다. 자격 증명의 남용은 여전히 지배적인 공격 벡터이며 공개된 정보에서 종종 불분명하기 때문에 파일 수준의 세밀한 모니터링의 가치가 부각되었습니다. 소매업 및 접객 사업자는 인시던트의 39%가 타사 공급업체에서 발생했으며 82%가 인위적 실수와 관련되어 있다고 보고했으며 공급망 시각화가 시급합니다. 보안 운영에 AI와 자동화를 도입한 기업은 침해 1건당 평균 222만 달러를 절약하고 있어 노이즈를 필터링하여 대응을 신속화하는 머신러닝 주도의 FIM에 대한 투자가 유효하다는 것을 보여줍니다.

높은 도입 및 유지보수 비용

신흥 시장의 중소기업은 보안에 연간 50만 달러 미만을 할당하는 경우가 많으며 위협이 증가하고 있음에도 불구하고 엔터프라이즈급 FIM을 정당화하기가 어렵습니다. 마이그레이션 시 레거시 시스템과 최신 시스템을 병렬로 운영하면 비용이 두 배로 늘어나며 기술 부족으로 효율적인 도입을 방해합니다. 유럽 기업들은 IT 예산의 9%를 보안에 충당하고 있지만, 89%가 NIS 2 의무화에 대응하기 위해 더 많은 직원이 필요하다고 응답하고 있으며, 비용으로 인한 도입 장벽이 부각되고 있습니다.

부문 분석

대기업은 2024년 매출의 4분의 3 이상을 차지했으며, 규제 모니터링과 복잡한 하이브리드 환경이 대규모 도입을 촉진하는 방법을 보여줍니다. 이러한 기업은 분산 데이터센터 및 멀티클라우드를 운영하며 수천 개의 엔드포인트에서 지속적인 변경을 감지해야 합니다. 또한 재무체질을 강화함으로써 AI를 활용한 애널리틱스에 투자할 수 있어 오감지율을 줄이고 대응을 신속하게 할 수 있습니다. 한편, 중소기업 CAGR은 가장 빠른 17.40%로 성장을 지속하고 있으며, 도입 시간을 단축하고 유지관리를 아웃소싱하는 구독 기반 플랫폼이 원동력이 되고 있습니다. 아시아태평양의 정부 보조금으로 초기 비용이 절감되는 반면 사이버 보험 회사는 보험 증권 발행을 위해 파일 무결성 관리를 규정합니다.

중소기업의 비즈니스 기회는 마법사 중심의 설치 인터페이스, 관리형 서비스 및 엄청난 자본 지출을 피하는 활용 기반 가격 설정으로 열립니다. 그럼에도 불구하고 예산과 인재 간의 격차는 여전히 존재합니다. 많은 중소기업들은 여전히 보안 전담 직원을 갖지 않고 사업을 전개하고 있기 때문에 튜닝 및 인시던트 처리는 공급자의 전문 지식에 의존하고 있습니다. 공급업체는 감사를 견딜 수 있는 증거를 유지하면서 기술 요구사항을 압축하기 위한 규칙 세트, 자동화된 기준선 및 AI 가이드를 통한 조사 워크플로우를 지원합니다.

클라우드 제공 제품은 2024년에 69.20%의 매출을 차지하며, 18.90%의 연평균 복합 성장률(CAGR)로 성장을 이끌고 있는데, 이는 SaaS와 Infrastructure-as-Code를 향한 광범위한 기업의 리팩토링을 반영하고 있습니다. 최신 플랫폼은 탄력적인 확장성과 API 통합을 제공하여 보안 팀이 하이퍼스케일 제공업체로부터 네이티브 원격 측정을 이어받아 에이전트를 늘리지 않고 무결성 평가를 거듭할 수 있습니다. 통합된 대시보드는 PCI, GDPR(EU 개인정보보호규정) 및 HIPAA 프레임워크의 컴플라이언스 매핑을 간소화합니다.

온프레미스 도구는 데이터 주권 및 부문화된 네트워크를 유지해야 하는 고도로 규제된 기관에도 적합합니다. 하이브리드 유형의 도입은 온프레미스 로그를 클라우드 호스팅 분석 엔진에 통합하여 이러한 수요를 브리징합니다. 예를 들어 OkCupid를 AWS로 마이그레이션하면 Terraform을 활용하여 최소한의 맞춤 코드로 클라우드 네이티브 FIM 파이프라인을 구축하여 상용 제품보다 총 비용을 절감했습니다. 클라우드 보안 포스처 관리와 파일 무결성 기능의 융합은 제품 경계를 모호하게 만들고 SaaS로의 전환을 더욱 가속화합니다.

파일 무결성 모니터링 시장은 조직 규모별(중소기업, 대기업), 설치 모드별(온프레미스, 클라우드), 전개 형태별(에이전트 기반, 에이전트 없는/클라우드 네이티브), 최종 사용자 산업별(소매, 은행, 금융서비스 및 보험(BFSI), 접객, 헬스케어, 정부 기관 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 성숙한 사이버 규제와 포춘 1000 기업에 의한 다액의 보안 지출을 배경으로 2024년 매출의 28.9%를 창출했습니다. 미국은 세계 사이버 보안 예산의 40% 이상을 차지하고 있으며, 금융기관은 보호에 2자리 IT 예산을 나누고 있으며 계속 주도권을 잡고 있습니다. 캐나다는 정보 유출 통지 요건의 조화를 추진하고 있으며, 멕시코의 핀테크법은 기본적인 보안 의무를 높이고 지역 수요를 강화하고 있습니다.

아시아태평양은 각국 정부가 서비스를 디지털화하고 소블린 클라우드에 투자하고 있기 때문에 CAGR 17.2%에서 가장 급성장하고 있는 지역입니다. 일본 최초의 사이버 보안에 특화된 투자 펀드와 S&J와 Cyleague HD와 같은 파트너십은 관리된 감지 능력을 확대하고 정교한 구매자 시장을 돋보이게 합니다. 중국의 데이터 현지화 규범이 국내 벤더에 의한 중요한 산업용 컴플라이언스 대응 FIM 구축에 박차를 가합니다. 싱가포르로 대표되는 ASEAN의 금융 허브는 디지털 뱅킹의 성장을 지원하기 위해 고급 모니터링을 채택하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 규제 준수의 의무

- 데이터 침해 증가 및 고도화

- 클라우드 워크로드의 확대에는 클라우드 네이티브 FIM이 필요

- 저렴한 SaaS형 FIM의 중소기업 채용

- 코드 무결성을 위한 DevSecOps 파이프라인 통합

- ROI를 높이는 AI에 의한 소음 저감

- 시장 성장 억제요인

- 높은 도입 비용 및 유지 보수 비용

- 운용 경보 피로 및 스킬 부족

- 컨테이너 및 마이크로서비스의 맹점

- 이뮤터블 인프라로의 이행에 의해 파일 레벨의 모니터링 필요성 저하

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모 및 성장 예측

- 조직 규모별

- 중소기업

- 대기업

- 전개 모드별

- 온프레미스

- 클라우드

- 설치 모드별

- 에이전트 기반

- 에이전트리스 및 클라우드 네이티브

- 최종 사용자 업계별

- 소매

- BFSI

- 접객

- 헬스케어

- 정부기관

- 엔터테인먼트 및 미디어

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- McAfee

- Cimcor

- Qualys

- ATandT

- SolarWinds

- LogRhythm

- New Net Technologies

- Trend Micro

- Trustwave

- Ionx Solutions

- Splunk

- Software Diversified Services

- IBM

- Securonix

- Bitdefender

- Tripwire

- Rapid7

- Wazuh

- ManageEngine(Zoho)

- Tanium

- Netwrix

- Cisco Systems

제7장 시장 기회 및 향후 전망

AJY 25.11.24The file integrity monitoring market stands at USD 1.20 billion in 2025 and is forecast to reach USD 2.65 billion by 2030, registering a robust 17.28% CAGR.

Momentum stems from tighter global cybersecurity regulations, rapid cloud workload expansion and the convergence of AI-driven security analytics that reduce alert fatigue. Enterprises are prioritizing real-time change detection because perimeter-centric controls no longer suffice against lateral attacks and ransomware. Demand also benefits from a global pivot toward zero-trust frameworks that regard file integrity monitoring as foundational for least-privilege enforcement. Across industries, rising cyber-insurance prerequisites and board-level scrutiny of operational resilience further propel the adoption of modern, cloud-native monitoring platforms.

Global File Integrity Monitoring Market Trends and Insights

Regulatory Compliance Mandates

Financial institutions face the May 2025 New York DFS Part 500 amendment that requires privileged-access oversight and multi-factor authentication, making file integrity systems critical for audit-trail evidence. The Federal Energy Regulatory Commission approved NERC CIP-015-1, extending internal monitoring to operational technology in bulk electric systems. Updated HIPAA rules add encryption and multi-factor authentication for electronic protected health information, strengthening demand for integrity monitoring in healthcare.SEC incident-disclosure rules compel listed companies to report material cyber events within four business days, driving real-time change detection requirements. Payment firms must also satisfy PCI DSS 4.0 logging and monitoring criteria by March 2025, positioning file integrity controls as core infrastructure.

Rising Data-Breach Volume and Sophistication

Average global breach costs climbed to USD 4.88 million in 2024 and are set to hit USD 5.00 million in 2025, with healthcare incidents peaking at USD 9.77 million. Credential abuse remains the dominant attack vector, often obscured in public disclosures, underscoring the value of granular file-level monitoring. Retail and hospitality operators report 39% of incidents emanating from third-party vendors, and 82% link to human error, raising urgency for supply-chain visibility. Enterprises implementing AI and automation within security operations saved USD 2.22 million per breach on average, validating investment in machine-learning-driven FIM that filters noise and accelerates response.

High Implementation and Maintenance Costs

SMEs in emerging markets often allocate under USD 500,000 a year to security, making enterprise-grade FIM difficult to justify despite rising threats. Parallel operation of legacy and modern systems during migrations doubles expenses, while skill shortages hamper efficient deployment. European firms devote 9% of IT budgets to security, yet 89% say they need more staff to meet NIS 2 mandates, highlighting cost-driven adoption barriers.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Workload Expansion Needs Cloud-Native FIM

- AI-Driven Noise-Reduction Boosting ROI

- Container and Micro-Services Blind-Spots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large enterprises generated over three-quarters of 2024 revenue, underlining how regulatory scrutiny and complex hybrid environments drive sizeable deployments. These organizations run distributed data centers and multicloud estates that require continuous change detection across thousands of endpoints. Financial muscle also allows investment in AI-powered analytics that shrink false-positive rates and accelerate response. Meanwhile, SMEs post the fastest 17.40% CAGR, powered by subscription-based platforms that compress onboarding time and outsource upkeep. Government grants in Asia Pacific lower the initial outlay, while cyber-insurance carriers increasingly stipulate file integrity controls for policy issuance.

The SME opportunity is being unlocked by wizard-driven setup interfaces, managed services and usage-based pricing that sidestep heavy capital expense. Yet budget and talent gaps persist; many small firms still operate without dedicated security staff and therefore rely on provider expertise for tuning and incident handling. Vendors respond with curated rule sets, automated baselining and AI-guided investigation workflows that compress skill requirements while maintaining audit-ready evidence.

Cloud offerings held 69.20% revenue in 2024 and lead growth at an 18.90% CAGR, reflecting the broader enterprise refactoring toward SaaS and infrastructure-as-code. Modern platforms deliver elastic scale and API integration, letting security teams inherit native telemetry from hyperscale providers and layer integrity assessments without agent sprawl. Unified dashboards simplify compliance mapping across PCI, GDPR and HIPAA frameworks.

On-premises tools remain relevant for highly regulated institutions that must maintain data sovereignty or segmented networks. Hybrid deployments bridge those demands by feeding on-premises logs into cloud-hosted analytics engines. As an illustration, OkCupid's migration to AWS leveraged Terraform to spin up a cloud-native FIM pipeline with minimal custom code and lower total cost than commercial alternatives. The convergence of cloud security posture management with file integrity functionality is blurring product boundaries and further accelerating migration to SaaS.

File Integrity Monitoring Market is Segmented by Organization Size (Small and Medium Enterprises, Large Enterprises), Deployment Type (On-Premise, Cloud), Installation Mode (Agent-Based, Agentless/Cloud Native), End-User Industry (Retail, BFSI, Hospitality, Healthcare, Government, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 28.9% of 2024 revenue on the back of mature cyber regulations and heavy security spending by Fortune 1000 enterprises. The United States channels more than 40% of global cybersecurity budgets, and financial institutions carve out double-digit IT allocations for protection, ensuring continued leadership. Canada promotes harmonized breach-notification requirements, and Mexico's fintech law raises baseline security obligations, reinforcing regional demand.

Asia Pacific is the fastest-growing territory at 17.2% CAGR as governments digitize services and invest in sovereign cloud. Japan's first cybersecurity-focused investment fund and partnerships such as S&J with Cyleague HD expand managed detection capacity, highlighting a sophisticated buyer market. China's data-localization norms spur domestic vendors to build compliance-ready FIM for critical industries. ASEAN's finance hubs, led by Singapore, adopt advanced monitoring to support digital banking growth.

- McAfee

- Cimcor

- Qualys

- ATandT

- SolarWinds

- LogRhythm

- New Net Technologies

- Trend Micro

- Trustwave

- Ionx Solutions

- Splunk

- Software Diversified Services

- IBM

- Securonix

- Bitdefender

- Tripwire

- Rapid7

- Wazuh

- ManageEngine (Zoho)

- Tanium

- Netwrix

- Cisco Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory compliance mandates

- 4.2.2 Rising data-breach volume and sophistication

- 4.2.3 Cloud workload expansion needs cloud-native FIM

- 4.2.4 SME adoption of affordable SaaS FIM

- 4.2.5 DevSecOps pipeline integration for code integrity

- 4.2.6 AI-driven noise-reduction boosting ROI

- 4.3 Market Restraints

- 4.3.1 High implementation and maintenance costs

- 4.3.2 Operational alert fatigue and skill shortage

- 4.3.3 Container and micro-services blind-spots

- 4.3.4 Shift to immutable infrastructure lowering need for file-level monitoring

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Organization Size

- 5.1.1 Small and Medium Enterprises

- 5.1.2 Large Enterprises

- 5.2 By Deployment Type

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Installation Mode

- 5.3.1 Agent-Based

- 5.3.2 Agentless / Cloud Native

- 5.4 By End-user Industry

- 5.4.1 Retail

- 5.4.2 BFSI

- 5.4.3 Hospitality

- 5.4.4 Healthcare

- 5.4.5 Government

- 5.4.6 Entertainment and Media

- 5.4.7 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 McAfee

- 6.4.2 Cimcor

- 6.4.3 Qualys

- 6.4.4 ATandT

- 6.4.5 SolarWinds

- 6.4.6 LogRhythm

- 6.4.7 New Net Technologies

- 6.4.8 Trend Micro

- 6.4.9 Trustwave

- 6.4.10 Ionx Solutions

- 6.4.11 Splunk

- 6.4.12 Software Diversified Services

- 6.4.13 IBM

- 6.4.14 Securonix

- 6.4.15 Bitdefender

- 6.4.16 Tripwire

- 6.4.17 Rapid7

- 6.4.18 Wazuh

- 6.4.19 ManageEngine (Zoho)

- 6.4.20 Tanium

- 6.4.21 Netwrix

- 6.4.22 Cisco Systems

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment