|

시장보고서

상품코드

1630287

밸브 및 액추에이터 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Valves And Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

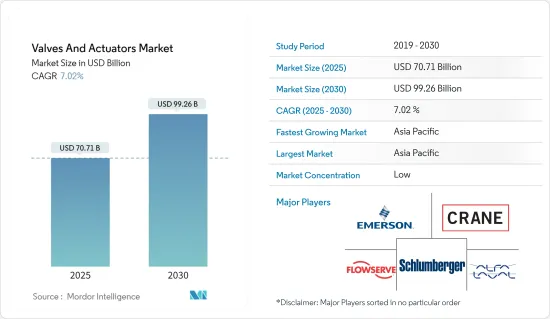

밸브 및 액추에이터 시장 규모는 2025년에 707억 1,000만 달러로 추정됩니다. 예측 기간 중(2025-2030년)의 CAGR은 7.02%로, 2030년에는 992억 6,000만 달러에 도달할 것으로 예상됩니다.

밸브 및 액추에이터 시장에는 석유, 가스 및 발전 산업용 공급업체가 공급하는 다양한 밸브 및 액추에이터가 포함됩니다. 시장 규모는 각 업계 공급업체가 창출하는 수익에 따라 결정됩니다.

제어 밸브는 석유 및 가스 탐사 프로젝트, 운송 파이프라인 구상, 지속적인 유지 보수 활동으로 인해 수요가 증가하고 있습니다. 이 시장은 스마트 액추에이터 개발에 대한 길을 여는 첨단 기술의 추진에 힘입어 급성장을 목표로 하고 있습니다. 이 스마트 액추에이터는 센서, 모터, 통신 모듈 및 컨트롤러를 원활하게 통합합니다. 그 적응성에 의해 조정, 셋업, 분리가 용이하고, 다양한 산업 분야의 로봇의 정평이 되고 있습니다.

밸브 및 액추에이터 기술이 발전함에 따라 엔지니어는 정확한 성능을 실현하고 전력 소비를 줄이고 환경으로 이산화탄소 배출을 최소화하는 솔루션을 선호합니다. 이러한 종래의 밸브 기술의 과제에 대한 대처가 시장의 성장에 박차를 가하고 있습니다.

해수에서 염분과 미네랄을 제거하는 해수 담수화는 다양한 산업에 필수적입니다. 제조업, 식품가공, 농업 등의 산업은 깨끗한 물에 대한 의존도를 높이고 있으며, 물 부족 증가에 대한 중요한 해결책으로 해수 담수화에 대한 수요가 높아지고 있습니다.

밸브 및 액추에이터는 수처리 플랜트, 발전, 정유소, 광업, 식품 생산에 매우 중요합니다. 그러나 이러한 부품에 대한 수요는 특히 선진국에서 산업 성장의 침체로 인해 정체되고 있습니다.

전반적으로 많은 산업에 필수적인 밸브 및 액추에이터 시장은 전력 산업 및 화학 산업 수요 증가, 해수 담수화 활동의 필요성 및 첨단 기술의 도입으로 성장하고 있습니다.

밸브 및 액추에이터 시장 동향

석유 및 가스 부문이 주요 시장 점유율을 차지

- 석유 및 가스 부문은 액추에이터가 파이프라인을 통한 석유 및 가스의 흐름을 조정하고, 안전 시스템을 유지하며, 상류와 하류 모두에서 많은 작업을 자동화하는 데 필수적이기 때문에 액추에이터 시장의 중요한 산업 부문입니다. 액추에이터는 신뢰성이 높고 오래 지속되고 정확한 제어 시스템의 필요성 때문에 업계에서 널리 사용됩니다. 이는 점점 복잡해지는 채굴 및 정제 과정에서 특히 그렇습니다. 석유 및 가스 시설의 안전하고 효과적인 기능을 보장하기 위해 이 범주의 액추에이터는 밸브 자동화 방분 장치 및 기타 중요한 장비 제어와 같은 응용 분야에 사용됩니다.

- 석유 및 가스 분야에서는 깊은 해양에서의 탐사·생산 활동이 증가하여 해중 액추에이터 수요가 대폭 증가했습니다. 가혹한 수중 환경에서는 장비를 작동하기 위해 해중 액추에이터가 필요합니다. 최근의 발전은 이러한 액추에이터의 신뢰성과 내구성을 높이고 부식 환경, 고압 및 저온을 견딜 수 있도록 하는 것을 목표로 하고 있습니다. 예를 들어, 액추에이터 제조업체인 Rotork는 심해 프로젝트의 요구사항을 충족하기 위해 성능과 수명을 향상시킨 고급 해중 전동 액추에이터를 개발했습니다.

- 조업 효율과 안전성을 향상시키기 위해, 석유 및 가스 분야에서는 디지털·액추에이터나 스마트·액추에이터의 채용이 가속하고 있습니다. 이러한 스마트 액추에이터의 센서 및 통신 기능은 실시간 모니터링, 진단 및 제어를 가능하게 합니다. 업계 선두의 Emerson Electric이 제조하는 베티스 RTS 지능형 전동 액추에이터는 고급 진단 기능과 원격 조작 기능을 갖추고 있습니다. 이를 통해 석유 및 가스 사업을 더욱 효과적으로 관리할 수 있습니다.

- 산업용 밸브에는 게이트 밸브, 글로브 밸브, 볼 밸브, 나비 밸브, 체크 밸브, 압력 밸브, 다이어프램 밸브 등 다양한 형상과 크기가 있으며, 각각 다른 기능을 갖추고 있습니다. 상업 건설과 자동화 프로젝트가 점점 더 밸브에 의존하게 됨에 따라, 산업용 가스 밸브에 대한 수요는 향후 수년에 걸쳐 상승할 것으로 예상됩니다. 이러한 급증은 기술의 진보, 산업화와 도시화의 진전, 기존 시설의 확장에 의해 촉진됩니다.

- 2024년 2월, 세일럼시의 3,000가구가 도시가스배급(CGD) 네트워크 하에 국내 파이프식 천연가스(D-PNG)에 등록되었습니다. Indian Oil Corporation Limited(IOCL)는 1,550 가구에 미터를 설치했습니다.

- Baker Hughes에 따르면, 북미는 세계적으로 석유 및 가스의 리그를 받아들이고 있습니다. 2024년 5월 현재 이 지역에는 700개의 육상 리그와 22개의 해상 리그가 있습니다. 2023년에는 세계 석유 장비 수가 평균 1,800기를 넘었습니다.

- 탐사·생산 활동에 있어서 신뢰할 수 있는 제어 시스템의 필요성, 성장하는 LNG 인프라, 세계의 에너지 수요 모두가, 석유 및 가스 분야가 액추에이터의 주요 성장 분야로서 성장을 계속하고 있는 것에 기여하고 있습니다. 최근 해저 액추에이터와 스마트 액추에이터의 기술 동향과 환경 컴플라이언스와 안전성에 중점을 둔 이 분야는 까다로운 시장에서 탄력성을 강화하고 있습니다.

큰 성장을 기록하는 아시아태평양

- 중국은 제조 효율성을 높이고 인건비를 줄이기 위해 산업 자동화에 많은 투자를 하고 있습니다. 공장이 고급 자동화 프로세스로 전환함에 따라 이러한 시스템에 필수적인 부품인 액추에이터의 요구가 커지고 있습니다.

- "Made in China 2025" 계획과 같은 중국 정부의 이니셔티브는 자동화, 기술 연구 개발 및 투자에 대한 주력을 강조합니다. 오토메이션 장비를 독일이나 일본에서 수입에 의존하고 있기 때문에 "Made in China" 구상은 국내 생산을 강화하고 시장의 성장을 뒷받침하는 것을 목적으로 하고 있습니다.

- 인도는 2025년까지 GDP에서 차지하는 제조업의 비율을 25%로 끌어올리는 것을 목표로 하는 국가 제조 정책과 핵심 제조업을 세계 제조업 수준과 동등하게 발전시키기 위해 2022년에 시작된 제조 산업용 PLI 체계와 같은 인도 정부의 이니셔티브을 통해 Industry 4.0으로의 길을 서서히 걷고 있습니다. 인도의 제조업은 보다 자동화된 프로세스 주도의 제조업으로 점차 이동하고 있어, 이것에 의해 제조업의 효율화와 생산량 증가가 전망되어 시장 성장의 원동력이 되고 있습니다.

- 또한, 통상산업성·에너지성은 중소기업에 의한 스마트 공장 기술의 도입·확장을 지원하는 대처를 강화하고 있습니다. 한국기술정보진흥원을 통해 스마트제조혁신실을 설립하였습니다. 또한 2025년까지 10가지 중요한 산업이 4,500개의 스마트 공장을 보유하고자 합니다. 이러한 정부의 적극적인 조치는 시장 성장을 자극하는 태세를 갖추고 있습니다.

- 동남아시아에서는 수요 증가에 대응하기 위한 가스탐사활동이 활발해지고 있으며, 이 지역의 석유 및 가스회사들 사이에서 다양한 유형의 밸브에 대한 요구가 높아질 것으로 예상됩니다. 말레이시아와 인도네시아는 남부 안다만 블록에서 Mubadala Energy의 중요한 발견을 포함하여 업스트림 발견의 성공을 보고합니다.

밸브 및 액추에이터 산업 개요

밸브 및 액추에이터 시장은 적당히 단편화되어 있으며 수십년의 경험을 가진 국내외 벤더가 진입하고 있습니다. 벤더는 견고한 시장 경쟁 전략을 채택하고 있으며 시장에서의 존재감을 유지하기 위해 많은 투자를 실시했습니다.

주요 공급업체는 혁신적인 기술을 적극적으로 도입하고 있습니다. 시장의 다른 유력한 기업은 소비자를 매료시키는 통합 솔루션을 강조합니다. 이와는 대조적으로, 중소 벤더와 신흥 벤더는 비용 효과를 우선시하고 경쟁 구도를 격화시키고 있습니다. 공공 부문이 성숙에 가까워지고 있는 현재, 그 초점은 민간부문으로 옮겨가고 있습니다.

품질 인증, 다양한 제품 제공, 경쟁력있는 가격 설정, 기술 전문 지식 등 주요 요인이 신규 계약을 획득하는 데 매우 중요합니다. 경쟁업체 간의 적대관계는 여전히 높고 예측기간 동안 계속될 것으로 예측됩니다.

시장의 주요 기업으로는 Emerson Electric Co., Schlumberger Limited, Alfa Laval Corporate AB, Flowserve Corporation, Crane Co. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 산업 밸류체인 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 스마트 밸브와 액추에이터의 응용을 촉진하는 기술의 진보

- 해수 담수화 수요 증가

- 시장 성장 억제요인

- 선진국의 산업 성장 정체

제6장 시장 세분화 : 액추에이터

- 유형별

- 유압식

- 공압식

- 전기식

- 기계식

- 기타 유형

- 업계별

- 석유 및 가스

- 발전

- 화학

- 물 및 폐수

- 광업

- 기타 최종 사용자 업계별

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 아시아

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

- 북미

제7장 시장 세분화 : 밸브

- 유형별

- 볼

- 나비

- 게이트/글로브/체크

- 플러그

- 컨트롤

- 기타 유형

- 업계별

- 석유 및 가스

- 발전

- 화학

- 물 및 폐수

- 광업

- 기타 최종 사용자 업계별

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제8장 경쟁 구도

- 기업 프로파일

- Emerson Electric Co.

- Schlumberger Limited

- Alfa Laval Corporate AB

- Flowserve Corporation

- Crane Co.

- Rotork PLC

- Metso Oyj

- KITZ Corporation

- IMI Critical Engineering

- Samson Controls Inc.

제9장 투자 분석

제10장 시장 기회와 앞으로의 동향

KTH 25.02.05The Valves And Actuators Market size is estimated at USD 70.71 billion in 2025, and is expected to reach USD 99.26 billion by 2030, at a CAGR of 7.02% during the forecast period (2025-2030).

The valves and actuators market encompasses various valves and actuators supplied by vendors catering to oil and gas and power generation industries. Market size is determined by the revenue generated by these vendors across industries.

Control valves see heightened demand from oil and gas exploration projects, transportation pipeline initiatives, and ongoing maintenance activities. The market is witnessing a surge, fueled by the push for advanced technologies, paving the way for the development of smart actuators. These smart actuators integrate sensors, motors, communication modules, and controllers seamlessly. Their adaptability allows for easy adjustments, setups, or dismantling, making them a staple in robots across various industries.

As valve and actuator technology advances, engineers prioritize solutions that deliver precise performance, consume less power, and minimize the environmental carbon footprint. This commitment to address the challenges of traditional valve technologies is fueling market growth.

Desalination, which is the process of removing salts and minerals from salty water, is essential for various industries. Industries such as manufacturing, food processing, and agriculture rely more on clean water, leading to a growing demand for desalination as a key solution to increasing water scarcity.

Valves and actuators are pivotal in water treatment plants, power generation, refineries, mining, and food production. Yet, demand for these components has stagnated, particularly in developed nations, due to sluggish industrial growth.

Overall, the valve and actuators market, integral to many industries, is growing, owing to rising demand from the power and chemical industries, the need for desalination activities, and the adoption of advanced technologies.

Valves And Actuators Market Trends

The Oil and Gas Segment Holds Major Market Share

- The oil and gas segment is an important contributor to the actuators market because actuators are essential for regulating the flow of gas and oil through pipelines, maintaining safety systems, and automating a number of tasks in both upstream and downstream operations. Actuators have become widely used in the industry due to the necessity for dependable, long-lasting, and accurate control systems. This is especially true in the increasingly complicated extraction and refining processes. To ensure the safe and effective functioning of oil and gas facilities, actuators in this category are utilized in applications such as valve automation blowout preventers and control of other essential equipment.

- The oil and gas segment increased exploration and production activities in deeper oceans, which has resulted in a major increase in demand for subsea actuators. Extreme underwater environments require subsea actuators to operate equipment. Recent advancements aim to make these actuators more dependable and durable, allowing them to resist corrosive environments, high pressures, and low temperatures. For example, in order to meet the requirements of deep-water projects, Rotork, an actuator manufacturer, has developed advanced subsea electric actuators that offer improved performance and longevity.

- To improve operational efficiency and safety, the oil and gas segment is embracing digital and smart actuation systems at an increasing rate. These smart actuators' sensors and communication capabilities enable real-time monitoring, diagnostics, and control. The Bettis RTS intelligent electric actuators, manufactured by the major industry player Emerson Electric, offer advanced diagnostic features and remote-control capabilities. This allows for more effective administration of oil and gas operations.

- Industrial valves are available in numerous shapes and sizes, including gate, globe, ball, butterfly, check, pressure, and diaphragm valves, each serving distinct functions. As commercial construction and automation projects increasingly rely on them, the demand for industrial gas valves is projected to rise in the coming years. This surge is fueled by technological advancements, heightened industrialization and urbanization, and the expansion of existing facilities.

- In February 2024, 3,000 households in Salem City were registered for domestic piped natural gas (D-PNG) under the city gas distribution (CGD) network. Indian Oil Corporation Limited (IOCL) has installed meters at 1,550 households.

- According to Baker Hughes, North America hosts oil and gas rigs globally. As of May 2024, the region boasted 700 land and 22 offshore rigs. In 2023, the global count of oil rigs surpassed 1,800 units on average.

- The necessity for dependable control systems in exploration and production activities, the growing LNG infrastructure, and the world's need for energy all contribute to the oil and gas segment's continued growth as a key growth area for actuators. Recent subsea and smart actuator technology developments and a strong emphasis on environmental compliance and safety have strengthened the segment's resilience in a challenging market.

Asia-Pacific to Register Major Growth

- China is investing significantly in industrial automation to enhance manufacturing efficiency and reduce labor costs. As factories transition to advanced automated processes, there is an increasing need for actuators, which are essential components in these systems.

- China's government initiatives, like the "Made in China 2025" plan, underscore its focus on automation, technology R&D, and investment. Given the reliance on imports from Germany and Japan for automation equipment, the "Made in China" initiative aims to strengthen domestic production and boost the market's growth.

- India is gradually progressing on the road to Industry 4.0 through the Government of India's initiatives like the National Manufacturing Policy, which aims to increase the share of manufacturing in GDP to 25% by 2025, and the PLI scheme for manufacturing, which was launched in 2022 to develop the core manufacturing industry at par with global manufacturing standards. The manufacturing industry in India is gradually shifting to more automated and process-driven manufacturing, which is expected to increase efficiency and boost production in the manufacturing industry, thereby driving market growth.

- Moreover, the Ministry of Trade, Industry, and Energy is strengthening its efforts by supporting SMEs in adopting and expanding smart factory technologies. They have established the Smart Manufacturing Innovation Office through the Korea Technology and Information Promotion Agency. Also, 10 significant industries are targeted to boast 4,500 smart factories by 2025. Such proactive government measures are poised to stimulate the market's growth.

- The increase in gas exploration activities in Southeast Asia to meet rising demand is expected to drive the need for various types of valves among oil and gas companies in the region. Malaysia and Indonesia have reported successful upstream discoveries, including a significant find by Mubadala Energy in the South Andaman Block.

Valves And Actuators Industry Overview

The valves and actuators market is moderately fragmented, featuring local and international vendors with decades of experience. Vendors are adopting robust competitive strategies, heavily investing in advertising to maintain their market presence.

Leading vendors are actively introducing innovative technologies. Other prominent players in the market are emphasizing integrated solutions to captivate consumers. In contrast, smaller and emerging vendors prioritize cost-benefit advantages, heightening the competitive landscape. With the public sector nearing maturity, a substantial focus is shifting toward the private sector.

Key factors like quality certification, diverse product offerings, competitive pricing, and technical expertise are pivotal in securing new contracts. The competitive rivalry remains high and is projected to persist during the forecast period.

Some of the major players in the market are Emerson Electric Co., Schlumberger Limited, Alfa Laval Corporate AB, Flowserve Corporation, and Crane Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technological Advancements Propelling Application of Smart Valves and Actuators

- 5.1.2 Increase in Demand for Desalination Activities

- 5.2 Market Restraints

- 5.2.1 Stagnant Industrial Growth in Developed Countries

6 MARKET SEGMENTATION - ACTUATORS

- 6.1 By Type

- 6.1.1 Hydraulic

- 6.1.2 Pneumatic

- 6.1.3 Electric

- 6.1.4 Mechanical

- 6.1.5 Other Types

- 6.2 By End-user Vertical

- 6.2.1 Oil and Gas

- 6.2.2 Power Generation

- 6.2.3 Chemical

- 6.2.4 Water and Wastewater

- 6.2.5 Mining

- 6.2.6 Other End User Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East Africa

- 6.3.1 North America

7 MARKET SEGMENTATION - VALVES

- 7.1 By Type

- 7.1.1 Ball

- 7.1.2 Butterfly

- 7.1.3 Gate/Globe/Check

- 7.1.4 Plug

- 7.1.5 Control

- 7.1.6 Other Types

- 7.2 By End-user Vertical

- 7.2.1 Oil and Gas

- 7.2.2 Power Generation

- 7.2.3 Chemical

- 7.2.4 Water and Wastewater

- 7.2.5 Mining

- 7.2.6 Other End User Verticals

- 7.3 By Geography

- 7.3.1 North America

- 7.3.2 Europe

- 7.3.3 Asia

- 7.3.4 Australia and New Zealand

- 7.3.5 Latin America

- 7.3.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Emerson Electric Co.

- 8.1.2 Schlumberger Limited

- 8.1.3 Alfa Laval Corporate AB

- 8.1.4 Flowserve Corporation

- 8.1.5 Crane Co.

- 8.1.6 Rotork PLC

- 8.1.7 Metso Oyj

- 8.1.8 KITZ Corporation

- 8.1.9 IMI Critical Engineering

- 8.1.10 Samson Controls Inc.