|

시장보고서

상품코드

1630294

반도체용 배터리 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Batteries For Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

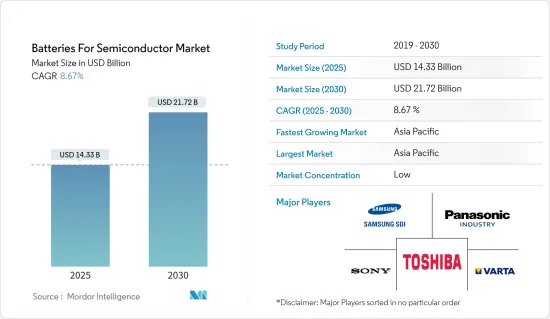

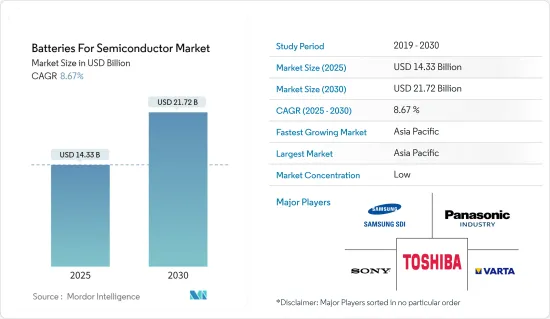

반도체용 배터리 시장 규모는 2025년 143억 3,000만 달러로 추정 및 예측되며, 예측 기간(2025-2030년) 동안 8.67%의 CAGR로 2030년에는 217억 2,000만 달러에 달할 것으로 예상됩니다.

장기적으로는 전기자동차의 보급과 휴대폰 수요 증가가 예측 기간 동안 시장을 견인할 것으로 보입니다.

한편, 낮은 에너지 밀도, 짧은 수명, 느린 충전 능력과 같은 배터리의 기술적 문제는 예측 기간 동안 시장 성장을 저해할 것으로 예상됩니다.

에너지 저장 시스템의 채택이 증가함에 따라 반도체용 배터리 시장은 큰 비즈니스 기회를 창출할 것으로 예상됩니다.

아시아태평양은 대규모 배터리 제조 인프라가 존재하기 때문에 소비자용 배터리 시장에서 아시아태평양이 지배적인 지역이 될 것으로 예상됩니다.

반도체용 배터리 시장 동향

전기자동차 부문이 큰 수요를 확보할 것으로 예상

- 전기자동차(EV) 시장 부문은 최근 몇 년 동안 크게 성장하여 반도체 시장의 배터리 수요에 큰 영향을 미치고 있으며, 환경적 이점과 기술 발전으로 인해 EV가 계속 인기를 얻고 있기 때문에 효율적이고 신뢰할 수 있는 배터리의 필요성이 가장 중요해지고 있습니다. 이러한 수요의 급증은 반도체 시장 전체에 파급효과를 가져와 업계 이해관계자들에게 새로운 기회와 도전과제를 창출하고 있습니다.

- 국제에너지기구(IEA)에 따르면 2022년 세계 전기자동차는 증가 추세에 있으며, 세계 플러그인 경전기자동차 누적 판매량은 약 1,020만대로 2021-2022년 56.9%의 성장률을 기록했으며, 2018-2022년 사이에 5배 증가하였다고 합니다. 증가하였습니다.

- EV 시장 부문의 성장을 뒷받침하는 주요 요인 중 하나는 환경 문제에 대한 전 세계인의 인식이 높아진 것입니다. 정부와 소비자들은 보다 깨끗하고 지속가능한 운송 수단을 옹호하고 있으며, EV는 실행 가능한 솔루션으로 부상하고 있습니다. 이에 따라 전기자동차 보급을 촉진하기 위한 다양한 혜택, 세금 감면, 규제 등이 시행되고 있습니다. 그 결과, 자동차 제조업체들은 전기자동차 생산에 집중하고 있으며, 이는 반도체 시장에서 첨단 배터리 기술에 대한 수요를 증가시키고 있습니다.

- 예를 들어, 캐나다 정부는 2023년 1월, 2026년부터 캐나다에서 판매되는 자동차의 최소 20%를 전기자동차로 전환하겠다고 발표했습니다. 이 발표는 캐나다가 설정한 이산화탄소 배출량 목표를 달성하기 위해 캐나다에서 전기자동차 보급을 촉진하기 위해 발표되었습니다. 정부는 또한 전국적으로 전기자동차 배터리를 생산하는 기업에 생산 장려금을 제공한다고 발표했습니다.

- 전기자동차 시장 부문의 성장 궤적은 반도체 산업에 연쇄적인 영향을 미치고 시장 관계자들에게 다양한 기회를 가져다주고 있습니다. 반도체 제조업체는 전기자동차 배터리, 배터리 관리 시스템, 전력전자에 필요한 첨단 부품과 칩을 개발 및 공급할 수 있는 기회를 얻게 됩니다. 이는 수익 잠재력을 높이고 확대되는 전기자동차 시장에 자본을 투자할 수 있는 기회로 이어집니다.

- 전기자동차 판매량 증가와 정부의 정책적 지원으로 반도체용 배터리의 연구개발 활동은 더욱 활발해질 것으로 예상됩니다.

아시아태평양이 시장 성장의 상당 부분을 차지

- 아시아태평양의 반도체용 배터리 시장은 세계 반도체 산업에 큰 영향을 미치는 매우 중요하고 역동적인 지역입니다. 이 광활하고 다양한 지역에는 많은 국가들이 포함되어 있으며, 각 국가마다 고유한 경제 및 기술 전망을 가지고 있습니다. 아시아태평양 반도체 시장의 배터리 수요는 급속한 산업화, 소비자 전자제품의 사용 증가, 전기자동차 시장의 급성장 등의 요인으로 인해 꾸준히 증가하고 있습니다.

- 아시아태평양의 반도체용 배터리 수요의 중요한 원동력 중 하나는 소비자 전자제품의 급격한 성장입니다. 이러한 성장의 원동력은 특히 중국, 인도 등의 국가에서 가처분 소득의 증가와 중산층 인구의 급격한 증가에 기인합니다. 이러한 소비자들은 스마트폰, 노트북 및 기타 개인용 전자기기를 점점 더 많이 사용하고 있으며, 이에 따라 이러한 기기에 전력을 공급하는 첨단 반도체 배터리의 필요성이 증가하고 있습니다. 소비자 전자제품이 일상 생활의 필수적인 부분으로 자리 잡으면서 아시아태평양의 반도체 제조업체들은 이 성장 시장 부문에서 이익을 얻을 수 있는 기회를 포착할 수 있습니다.

- 또한 아시아태평양에서는 전기자동차의 도입이 크게 증가하고 있습니다. 환경 지속가능성에 대한 관심이 높아지고, 전기자동차를 장려하는 정부 인센티브가 증가함에 따라 중국과 같은 국가는 전기자동차 시장에서 중요한 진입자가 되고 있습니다.

- 예를 들어, 중국자동차공업협회(AMMA)에 따르면 2023년 5월 현재 중국은 전기자동차(EV) 최대 시장으로 플러그인하이브리드차(PHEV) 79만 3,000대, 배터리전기자동차(BEV) 214만 6,000대가 판매될 것으로 추산됩니다. 년에는 배터리 전기자동차 판매량이 545만 대에 달해 가장 많은 판매량을 기록할 것으로 예상됩니다. 예측 기간 동안 세계 최대의 전기자동차 시장으로 남을 것으로 예상됩니다.

- 전기자동차는 전력과 배터리 성능을 관리하기 위해 효율적이고 신뢰할 수 있는 반도체 부품이 필요하기 때문입니다. 따라서 전기자동차 시장의 성장은 아시아태평양의 반도체 배터리 제조업체들에게 큰 기회를 제공하고 있습니다.

- 결론적으로, 반도체 시장에서 아시아태평양의 배터리 시장 부문은 역동적이고 빠르게 발전하고 있습니다. 가전제품과 전기자동차가 주도하는 이 지역의 반도체용 배터리 수요 증가는 제조업체들에게 큰 비즈니스 기회를 제공하고 있습니다. 따라서, 위의 점으로 미루어 볼 때, 아시아태평양은 예측 기간 동안 반도체용 배터리 시장을 주도할 것으로 보입니다.

반도체용 배터리 산업 개요

반도체용 배터리 시장은 고도로 세분화되고 통합되어 있습니다. 주요 기업으로는 삼성SDI, Sony Corporation, Panasonic Corporation, Varta AG, Toshiba Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부 규제와 시책

- 시장 역학

- 성장 촉진요인

- 모바일 기기 수요 증가

- 전기자동차 보급

- 성장 억제요인

- 기술적 과제 유무

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 종류

- 리튬이온

- 니켈 수소

- 리튬이온 폴리머

- 나트륨 이온 배터리

- 용도

- 가전제품

- 전기자동차

- 에너지 저장 시스템

- 기타 최종사용자 용도

- 시장 분석 : 지역별(2028년까지 시장 규모와 수요 예측)

- 북미

- 미국

- 캐나다

- 기타 북미

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 칠레

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Samsung SDI Co Ltd.

- Sony Corporation

- Panasonic Corporation

- Varta AG

- Toshiba Corporation

- EnerSys

- GS Yuasa Corporation

- Faradion Limited

- Routejade

- TianJin Lishen Battery Joint-Stock Co. Ltd.

- Market Ranking/Share Analysis

제7장 시장 기회와 향후 동향

- 에너지 저장 시스템 혁신

The Batteries For Semiconductor Market size is estimated at USD 14.33 billion in 2025, and is expected to reach USD 21.72 billion by 2030, at a CAGR of 8.67% during the forecast period (2025-2030).

Over the long term, the increasing adoption of electric vehicles and demand for mobile phones are expected to drive the market during the forecasted period.

On the other hand, technological challenges of batteries, like low energy density, lower lifespan, and slower charging capacity, are expected to hinder the growth of the market during the forecasted period.

Nevertheless, the increasing adoption of energy storage systems is expected to create huge opportunities for the Batteries for Semiconductor Market.

Asia-Pacific is expected to be a dominant region for the Consumer Battery Market due to the presence of a large battery manufacturing infrastructure in the region.

Semiconductor Battery Market Trends

The Electric Vehicle Segment is Expected to Witness Significant Demand

- The electric vehicle (EV) market segment has witnessed substantial growth in recent years, and this has had a significant impact on the demand for batteries in the semiconductor market. As EVs continue to gain popularity due to their environmental benefits and technological advancements, the need for efficient and reliable batteries has become paramount. This surge in demand has generated a ripple effect throughout the semiconductor market, creating new opportunities and challenges for stakeholders in the industry.

- According to the International Energy Agency, global electric vehicles are on the rise in 2022; the cumulative plug-in light electric vehicle sales globally were around 10.2 million units, recording a growth rate of 56.9% between 2021 and 2022 and a fivefold increase between 2018 and 2022.

- One of the key drivers behind the growth of the EV market segment is the increasing global awareness of environmental concerns. Governments and consumers are advocating for cleaner and more sustainable modes of transportation, and EVs have emerged as a viable solution. This has led to various incentives, tax breaks, and regulations promoting the adoption of electric vehicles. As a result, automakers are shifting their focus towards EV production, thus bolstering the demand for advanced battery technologies within the semiconductor market.

- For instance, in January 2023, the Government of Canada announced that at least 20% of the vehicles sold in the country will be electric vehicles from 2026, and it will gradually increase to 60% in 2030 and reach 100% by the end of 2035. This announcement was made to increase the adoption of electric vehicles in the country to meet the carbon emission targets set by Canada. The government has also announced offering production incentives to companies manufacturing electric vehicle batteries nationwide.

- The electric vehicle market segment's growth trajectory has a cascading effect on the semiconductor industry, creating a range of opportunities for market players. Semiconductor manufacturers have a chance to develop and supply the cutting-edge components and chips required for EV batteries, battery management systems, and power electronics. This translates to increased revenue potential and the chance to capitalize on the expanding EV market.

- With the increasing sales of electric vehicles and the supportive government policies, the segment is expected to increase further, increasing the research and development activities in the battery for semiconductor segment.

Asia-Pacific Account for Significant Market Growth

- The Asia-Pacific market segment for batteries in the semiconductor market is a pivotal and dynamic region with significant implications for the global semiconductor industry. This vast and diverse region encompasses many countries, each with its unique economic and technological landscape. The demand for batteries in the semiconductor market within the Asia Pacific region has been steadily rising, driven by factors that include rapid industrialization, increasing consumer electronics usage, and the burgeoning electric vehicle market.

- One of the critical drivers for the demand for semiconductor batteries in the Asia-Pacific region is the exponential growth in consumer electronics. This growth is driven by rising disposable incomes and a surging middle-class population, especially in countries like China and India. These consumers are increasingly adopting smartphones, laptops, and other personal electronic devices, which, in turn, fuels the need for advanced semiconductor batteries to power these gadgets. As consumer electronics become an integral part of everyday life, semiconductor manufacturers in the Asia-Pacific region are poised to benefit from this growing market segment.

- Additionally, the Asia-Pacific region has witnessed a substantial uptick in electric vehicle adoption. With an increasing focus on environmental sustainability and government incentives to promote electric vehicles, countries like China have become significant players in the electric vehicle market.

- For instance, according to the China Association of Automobile Manufacturers (AMMA), as of May 2023, China is the largest market for electric vehicles (EV), with an estimated 0.793 million plug-in hybrid Electric vehicles (PHEVs) and 2.146 million battery electric vehicles (BEVs) being sold. In 2022, the country recorded the highest sales of battery electric vehicles, with 5.45 million. It is expected to remain the world's largest electric car market during the forecast period.

- This, in turn, has led to soaring demand for advanced batteries in the semiconductor market, as EVs require efficient and reliable semiconductor components to manage power and battery performance. The growth of the electric vehicle market, therefore, offers substantial opportunities for semiconductor battery manufacturers in the Asia-Pacific region.

- In conclusion, the Asia-Pacific market segment for batteries in the semiconductor market is a dynamic and rapidly evolving landscape. The region's growing demand for semiconductor batteries, driven by consumer electronics and electric vehicles, offers significant opportunities for manufacturers. Therefore, per the above points, the Asia-Pacific region will dominate the battery for semiconductor market during the forecasted period.

Semiconductor Battery Industry Overview

The batteries for semiconductor market are highly fragmented and consolidated. The major companies (in no particular order) include Samsung SDI Co Ltd, Sony Corporation, Panasonic Corporation, Varta AG, and Toshiba Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Mobile Devices

- 4.5.1.2 Rising Adaption of Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Availability of Technical Challenges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Lithium-Ion

- 5.1.2 Nickel-Metal Hydride

- 5.1.3 Lithium-Ion Polymer

- 5.1.4 Sodium-Ion Battery

- 5.2 End-User Application

- 5.2.1 Consumer Electronics

- 5.2.2 Electric Vehicles

- 5.2.3 Energy Storage System

- 5.2.4 Other End-User Applications

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 India

- 5.3.2.3 Japan

- 5.3.2.4 South Korea

- 5.3.2.5 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Chile

- 5.3.4.2 Brazil

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Samsung SDI Co Ltd.

- 6.3.2 Sony Corporation

- 6.3.3 Panasonic Corporation

- 6.3.4 Varta AG

- 6.3.5 Toshiba Corporation

- 6.3.6 EnerSys

- 6.3.7 GS Yuasa Corporation

- 6.3.8 Faradion Limited

- 6.3.9 Routejade

- 6.3.10 TianJin Lishen Battery Joint-Stock Co. Ltd.

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation in Energy Storage System