|

시장보고서

상품코드

1630335

유럽의 인쇄 포장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Printed Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

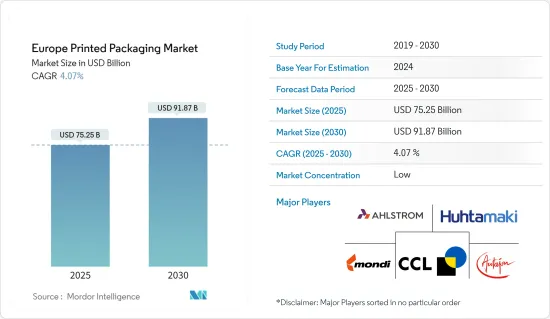

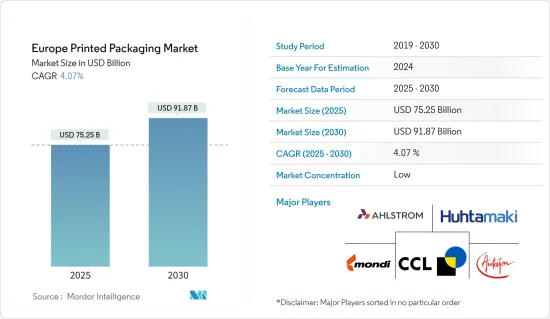

유럽의 인쇄 포장 시장 규모는 2025년 752억 5,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 4.07%의 CAGR로 2030년에는 918억 7,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 유럽의 인쇄 포장 시장은 몇 가지 주요 트렌드와 소비자 수요를 통해 진화하고 있습니다. 지속가능한 포장으로의 전환이 주요 촉진요인이며, 소비자 선호도 및 규제 요구 사항으로 인해 재활용 가능, 생분해성 및 플라스틱이 없는 포장을 포함한 친환경 솔루션에 대한 수요가 증가하고 있습니다. 이에 따라 특히 환경 영향에 대한 우려가 큰 음료 및 식품 산업에서 종이 기반 및 식물 기반 재료의 채택이 증가하고 있습니다.

- 인쇄 기술은 개인화된 맞춤형 포장 솔루션을 가능하게함으로써 시장을 변화시키고 있습니다. 이 기술을 통해 제조업체는 특정 소비자 요구사항이나 한정판 제품에 대응하기 위해 가변적인 디자인, 소량 생산, 비용 효율적인 인쇄를 할 수 있게 되었습니다. 소비자들이 개성 있는 포장 경험을 원하고 있는 가운데, E-Commerce 부문이 이러한 트렌드를 주도하고 있습니다.

- 예를 들어, 2024년 7월 Siegwerk는 유럽 시장 최초의 UV 플렉소 탈묵 시스템인 CIRKIT CLEARPRIME UV E02를 출시했습니다. 이 시스템은 UV 인쇄된 감압 라벨(PSL)을 탈묵하는 솔루션을 제공하여 포장의 재활용 가능성을 높입니다. 비식품 포장용으로 개발된 이 프라이머 기술은 라벨이 부착된 플라스틱 포장의 재활용성을 향상시킵니다. 이를 통해 비식품 포장 용도로 재사용할 수 있는 고품질의 재활용 제품을 생산할 수 있습니다.

- E-Commerce의 성장으로 포장 요구 사항이 재구성되어 제품의 무결성을 유지하면서 운송 비용을 최적화하기 위해 보호적이면서도 가벼운 솔루션의 필요성이 강조되고 있습니다. 이에 따라 운송 보호 및 비용 효율성을 제공하는 골판지 및 연포장재에 대한 수요가 증가하고 있으며, E-Commerce 기업들은 온라인 구매 시 개봉 경험을 향상시키기 위해 고급스러운 포장 디자인에 투자하고 있습니다.

- 유럽 시장에서는 QR 코드, RFID 태그, 증강현실(AR) 구성요소는 제품 정보를 제공하고, 추적성을 향상시키며, 대화형 경험을 창출하는 등 제조업체들이 혁신적인 기능을 통합하여 혁신적인 포장 기술이 부상하고 있습니다. 이러한 기술은 소비자의 관심을 높이는 동시에, 특히 식품 및 제약 산업에서 공급망 관리와 제품 인증을 지원합니다.

- 소비자의 건강 의식이 높아짐에 따라 규제 기준을 충족하는 안전 포장에 대한 수요가 증가하고 있습니다. 식품 및 의약품 포장은 제품의 무결성을 보장하고 오염을 방지하며 성분 및 유효기간 정보를 명확하게 표시해야 합니다. 또한, 안전과 보안을 우선시하는 부문에서는 개봉 방지 포장과 어린이용 포장의 채택이 증가하고 있습니다. 이러한 신흥국 시장 개척은 소비자 선호도, 기술 발전, 규제 요건에 대한 시장의 적응을 반영하고 있습니다.

유럽의 인쇄 포장 시장 동향

음료 산업이 큰 비중을 차지

- 유럽 음료 산업에서 인쇄 포장에 대한 수요는 소비자 선호도 변화, 지속가능성 트렌드, 기술 발전 등을 배경으로 지속적으로 증가하고 있습니다. 인쇄 포장은 경쟁이 치열한 시장에서 브랜드의 중요한 차별화 요소가 되고 있습니다. 음료 제조업체들이 매장에서의 입지를 확보하기 위해 경쟁하는 가운데, 적절한 포장은 마케팅 전략에 필수적인 요소로 자리 잡고 있습니다. 인쇄된 라벨과 포장은 특히 주류와 같은 프리미엄 부문에서 그래픽, 질감 및 마감을 통해 제품의 식별과 품질을 전달합니다.

- 인쇄 포장에 대한 수요 증가는 지속가능성에 대한 관심이 높아졌기 때문입니다. 유럽 소비자들의 환경 의식은 브랜드가 환경에 미치는 영향을 줄이도록 촉구하고 있습니다. 그 결과 재활용 가능한 재료, 생분해성 잉크, 지속가능한 인쇄 공정 등 환경 친화적인 포장 솔루션이 채택되고 있습니다. 유럽연합(EU)의 포장 폐기물 지침은 음료 부문을 지속가능한 관행으로 끌어올렸습니다. 기업들은 현재 효율적인 재료 재사용과 재활용을 보장하기 위해 순환 경제 원칙에 부합하는 포장을 우선시하고 있습니다.

- 음료 부문에서는 인쇄 포장을 통한 개인화 및 프리미엄화가 강조되고 있습니다. 브랜드는 다양한 소비자 취향을 충족시키기 위해 고유한 한정판 디자인이나 지역 한정 변형을 만들 수 있습니다. 디지털 인쇄 기술은 생산 시간 단축, 비용 효율적인 소량 생산, 디자인 유연성을 통해 이러한 맞춤화를 가능하게 합니다. 이 때문에 소비자들이 고급 포장을 제품의 품질과 연관 짓는 크래프트 맥주, 와인, 주류 부문에서 인쇄 포장에 대한 수요가 증가하고 있습니다.

- 인쇄 기술의 발전은 음료 포장에 변화를 가져왔습니다. 디지털 인쇄는 유리, 알루미늄, 플라스틱에 고품질 인쇄가 가능하기 때문에 점점 더 많이 채택되고 있습니다. 이 기술은 소량 생산 및 계절별 출시용 맞춤형 포장을 효율적으로 생산할 수 있게 해줍니다. 디지털 인쇄는 기존 방식에 비해 폐기물과 에너지 소비를 줄여 산업의 지속가능성 목표를 지원하며, QR 코드와 증강현실(AR)을 포함한 인터랙티브한 포장 기능은 소비자와의 혁신적인 소통을 가능하게 합니다.

- 규제 압력과 소비자 행동은 음료 부문에서 인쇄 포장의 미래를 형성합니다. 폐기물을 최소화하고 재활용을 촉진하기 위한 유럽 정부의 포장 규제 강화로 인해 제조업체는 지속가능한 재료와 공정을 채택하고 있습니다. 재활용 정보와 지속가능성에 대한 노력을 효과적으로 전달할 수 있는 포장에 대한 수요가 증가하고 있습니다. 인쇄된 라벨은 규제 준수를 촉진하고 환경에 민감한 소비자들에게 어필할 수 있습니다. 유럽 음료 인쇄 포장 시장은 지속가능성 요구 사항, 기술 혁신 및 브랜딩 요구 사항을 통해 계속 진화하고 있습니다.

- 프랑스 주류 시장의 인쇄 포장 수요는 2023년 7월부터 2024년 6월까지 수량과 직접적인 상관관계가 있습니다. 맥주와 라이트 맥주는 13억 1,244만 병으로 가장 큰 부문을 차지하고 있으며, 제품 차별화를 위해 광범위한 인쇄 포장 솔루션이 필요합니다. 사이다는 4,634만 병으로 개성 있는 포장 디자인이 요구됩니다. 증류주 및 리큐어는 2억 7,588만 병으로 디테일한 라벨과 고급스러운 마감의 세련된 인쇄 포장이 필요하며, 1억 5,753만 병의 식전주 카테고리는 제품의 특징을 강조하기 위해 인쇄 포장을 활용하고 있습니다. 1억 9,162만 병의 스파클링 와인과 샴페인은 인쇄 포장을 사용하여 프리미엄 포지셔닝을 전달하고 있습니다. 이러한 전체 카테고리의 성장은 브랜드 가시성과 시장에서의 존재감을 높이기 위한 인쇄 포장 솔루션에 대한 수요를 지속적으로 촉진하고 있습니다.

독일, 괄목할 만한 성장 전망

- 음료, 제약, 화장품, 소비재, E-Commerce 등 몇 가지 주요 산업이 독일 인쇄 포장 시장을 주도하고 있습니다. 음료 및 식품 부문은 지속가능성을 최우선으로 하여 카톤, 라벨, 연질 포장 등 브랜딩을 위한 기능성 포장에 대한 수요가 증가하고 있습니다. 제약 산업은 주로 인쇄된 종이 용기, 라벨, 인서트, 고품질, 변조 방지, 정보가 풍부한 포장에 대한 요구로 인해 인쇄된 종이 용기, 라벨, 인서트에 대한 큰 수요를 창출하고 있습니다.

- 화장품 및 퍼스널케어 제품은 기능성과 미적 감각을 위해 인쇄 포장을 활용하고 있으며, 튜브, 라벨, 고급 종이 용기 및 친환경 소재의 채택이 증가하고 있습니다. 가정용품, 전자제품, 의류 등 소비재 부문은 제품 차별화, 물류 및 온라인 소매를 위해 인쇄 포장을 필요로 합니다.

- 독일 화장품 시장은 2021-2023년 꾸준한 성장세를 보이고 있으며, 이는 시장 금액 증가에 반영되어 2021년 시장 규모는 14억 7,400만 달러로 2022년 15억 4,470만 달러로 성장하고 2023년에는 17억 2,200만 달러로 성장할 것으로 예상됩니다. 1억 7,200만 달러로 더욱 확대될 것입니다. 이러한 성장은 스킨케어 및 미용 제품에 대한 소비자 수요 증가, 프리미엄 및 지속가능한 화장품에 대한 지출 증가, 개인화된 포장에 대한 소비자 선호도 증가에 기인합니다.

- 시장 성장은 지속가능성으로의 전환을 반영하고 있으며, 독일 소비자들은 환경 친화적이고 윤리적으로 생산된 화장품을 원하고 있습니다. 이러한 추세는 재활용 가능한 재료 및 생분해성 포장과 같은 포장 혁신을 촉진하고 브랜드 차별화를 위한 필수 요소로 자리 잡았으며, E-Commerce가 중요한 유통 채널로 부상하고 화장품 온라인 쇼핑이 대유행 기간과 그 이후에 크게 증가하여 시각적으로 매력적이고 기능적인 인쇄 포장에 대한 수요를 창출하고 있습니다. 시각적으로 매력적이고 기능적인 인쇄 포장에 대한 수요를 창출하고 있습니다.

- 디지털 인쇄 기술은 고급 및 대중 화장품 브랜드에 대한 맞춤형 포장 옵션을 가능하게함으로써 시장 개척을 강화했습니다. 이러한 첨단 포장은 주로 개인화 된 한정판 제품을 통해 포장 제조업체가 특정 소비자 선호도를 충족시킬 수 있는 기회를 창출하고 있습니다.

- E-Commerce는 온라인 소매 업체들이 브랜드화되고 내구성이 뛰어나며 재활용이 가능한 배송 재료를 찾고 있기 때문에 인쇄 포장에 대한 수요가 증가하고 있습니다. 이 부문에서는 맞춤형 상자와 브랜드 메일러가 주류입니다. 자동차 및 산업 부문은 지속적으로 인쇄 포장 솔루션을 요구하고 있으며, 주로 부품 및 구성요소에 골판지 상자와 라벨을 사용합니다.

- 소비자 선호도와 유럽연합의 포장 폐기물 규제에 영향을 받은 시장은 모든 부문에서 지속가능성을 향한 큰 변화를 보이고 있습니다. 독일 기업들은 재활용, 생분해성 및 재생 가능한 재료를 포장 솔루션에 도입하고 있습니다. 디지털 인쇄 기술은 환경 문제 및 브랜딩 요구 사항을 충족하는 맞춤형 소량 포장 생산을 가능하게 합니다. 시장은 지속가능성과 혁신을 기본 동력으로 삼아 계속 진화하고 있습니다.

유럽의 인쇄 포장 산업 개요

유럽의 인쇄 포장 시장은 Amcor Group, Mondi plc, CCL Industries Inc. 등 유수의 기업들이 국내 및 해외에서 사업을 전개하고 있어 세분화되어 있습니다. 전략적 성장을 위한 합병, 인수, 관련 사업 및 사업부문의 통합은 포장 산업에서 반복적으로 나타나는 시장 동향입니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 인쇄 산업의 기술 진보 확대

- 최종사용자용 포장 용도 확대

- 시장 성장 억제요인

- 원료 가격 변동과 인쇄 포장 비용에 대한 영향

제6장 시장 세분화

- 인쇄 기술별

- 오프셋·리소그래피

- 그라비어 인쇄

- 플렉소 인쇄

- 디지털 인쇄

- 스크린 인쇄

- 잉크 유형별

- 용제형 잉크

- UV 경화형 잉크

- 수성 잉크

- 포장 유형별

- 라벨

- 플라스틱

- 유리

- 금속

- 종이·판지

- 용도별

- 화장품·재택의료

- 식품 및 음료

- 의약품

- 기타

- 국가별

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 폴란드

- 네덜란드

제7장 경쟁 구도

- 기업 개요

- Mondi plc

- Ahlstrom Oyj

- Autajon Group

- Huhtamaki Oyj

- CCL Industries Inc.

- Clondalkin Group Holdings BV

- Constantia Flexibles Group GmbH

- Amcor Group

- Smurfit Westrock plc

- DS Smith PLC

- International Paper Company

제8장 투자 분석

제9장 시장 기회와 향후 동향

ksm 25.01.23The Europe Printed Packaging Market size is estimated at USD 75.25 billion in 2025, and is expected to reach USD 91.87 billion by 2030, at a CAGR of 4.07% during the forecast period (2025-2030).

Key Highlights

- The Europe printed packaging market is evolving through several key trends and consumer demands. The shift toward sustainable packaging is a primary driver, with consumer preferences and regulatory requirements increasing demand for eco-friendly solutions, including recyclable, biodegradable, and plastic-free packaging. This has increased the adoption of paper-based and plant-based materials, particularly in the food and beverage industry, where environmental impact concerns are significant.

- Printing technologies are transforming the market by enabling personalized and customized packaging solutions. This technology allows manufacturers to produce small-batch, cost-effective print runs with variable designs to meet specific consumer requirements and limited-edition products. The e-commerce sector mainly demonstrates this trend, as consumers seek distinctive packaging experiences.

- For instance, in July 2024, Siegwerk introduced CIRKIT CLEARPRIME UV E02, its first UV flexo deinking system for the European market. The system provides a solution for deinking UV-printed pressure-sensitive labels (PSL) and enhances package recyclability. The primer technology, developed for non-food packaging applications, improves the recyclability of labeled plastic packaging. It enables the production of high-quality recyclates suitable for reuse in non-food packaging applications.

- E-commerce growth has reshaped packaging requirements, emphasizing the need for protective yet lightweight solutions to optimize shipping costs while maintaining product integrity. This has increased demand for corrugated cardboard and flexible packaging materials that provide transit protection and cost efficiency. E-commerce companies also invest in premium packaging designs to enhance the unboxing experience for online purchases.

- Innovative packaging technologies emerge in the European market as manufacturers integrate innovative features. QR codes, RFID tags, and augmented reality components provide product information, improve traceability, and create interactive experiences. These technologies enhance consumer engagement while supporting supply chain management and product authentication, particularly in the food and pharmaceutical industries.

- Consumer health consciousness has intensified the demand for safety-compliant packaging that meets regulatory standards. Food and pharmaceutical packaging must ensure product integrity, prevent contamination, and display evident ingredient and expiration information. The market also shows increased adoption of tamper-evident and child-resistant packaging in sectors prioritizing safety and security. These developments reflect the market's adaptation to consumer preferences, technological progress, and regulatory requirements.

Europe Printed Packaging Market Trends

Beverage Industries to Hold Significant Share

- The demand for printed packaging in the European beverage sector continues to grow, driven by evolving consumer preferences, sustainability trends, and technological advancements. Printed packaging serves as a key differentiator for brands in a competitive market. As beverage companies compete for shelf presence, adequate packaging has become essential to their marketing strategy. Printed labels and packaging communicate product identity and quality through graphics, textures, and finishes, particularly in premium segments like alcoholic beverages.

- The increased demand for printed packaging stems from a heightened focus on sustainability. European consumers' environmental awareness has compelled brands to reduce their environmental impact. This has resulted in adopting eco-friendly packaging solutions, including recyclable materials, biodegradable inks, and sustainable printing processes. The European Union's Packaging and Packaging Waste Directive has pushed the beverage sector toward sustainable practices. Companies now prioritize packaging aligned with circular economy principles to ensure efficient material reuse and recycling.

- The beverage sector emphasizes personalization and premiumization through printed packaging. Brands can create unique, limited-edition designs and region-specific variants to meet diverse consumer preferences. Digital printing technologies enable this customization through faster production times, cost-effective small runs, and design flexibility. This has increased printed packaging demand in craft beer, wine, and spirits segments, where consumers associate premium packaging with product quality.

- Printing technology advances have transformed beverage packaging. Digital printing has gained adoption for its ability to produce high-quality prints on glass, aluminum, and plastic. This technology enables efficient production of customized packaging for small batches and seasonal releases. Digital printing reduces waste and energy consumption compared to traditional methods, supporting industry sustainability goals. Interactive packaging features, including QR codes and augmented reality, enable innovative consumer engagement.

- Regulatory pressures and consumer behavior shape printed packaging's future in the beverage sector. European governments' stricter packaging regulations to minimize waste and promote recycling have led manufacturers to adopt sustainable materials and processes. Demand has increased for packaging that effectively communicates recycling information and sustainability initiatives. Printed labels facilitate regulatory compliance and appeal to environmentally conscious consumers. The printed packaging market in European beverages continues to evolve through sustainability requirements, technological innovation, and branding needs.

- The French alcoholic beverage market's printed packaging demand correlates directly with sales volumes from July 2023 to June 2024. Beer and light beer, with 1,312.44 million units, represent the largest segment, requiring extensive printed packaging solutions for product differentiation. The cider segment, accounting for 46.34 million units, generates demand for distinct packaging designs. Spirits and liqueurs, at 275.88 million units, require sophisticated printed packaging with detailed labels and premium finishes. The aperitifs category, with 157.53 million units, utilizes printed packaging to emphasize product characteristics. Sparkling wine and champagne, representing 191.62 million units, rely on printed packaging to communicate premium positioning. The growth across these categories continues to drive the demand for printed packaging solutions to enhance brand visibility and market presence.

Germany is Expected to Witness Significant Growth

- Several key industries, including food and beverages, pharmaceuticals, cosmetics, consumer goods, and e-commerce, drive the printed packaging market in Germany. The food and beverage sector requires functional packaging for branding purposes, including cartons, labels, and flexible packaging, with sustainability as a primary focus. The pharmaceutical industry generates substantial demand through its requirements for high-quality, tamper-evident, and information-rich packaging, primarily using printed folding cartons, labels, and inserts.

- Cosmetics and personal care products utilize printed packaging for functionality and aesthetic appeal, incorporating tubes, labels, and premium folding cartons, with increasing adoption of eco-friendly materials. The consumer goods sector, encompassing household items, electronics, and apparel, requires printed packaging for product differentiation, logistics, and online retail purposes.

- The cosmetics market in Germany has experienced steady growth from 2021 to 2023, as reflected by the increasing market value. In 2021, the market was valued at USD 14.74 billion, growing to USD 15.47 billion in 2022 and further expanding to USD 17.22 billion in 2023. This growth stems from rising consumer demand for skincare and beauty products, increased spending on premium and sustainable cosmetic products, and consumer preference for personalized packaging.

- The market growth reflects a shift toward sustainability, with German consumers seeking eco-friendly and ethically produced cosmetics. This trend drives packaging innovations, including recyclable materials and biodegradable packaging, which have become essential brand differentiators. E-commerce has emerged as a significant sales channel, with online cosmetics shopping increasing substantially during and after the pandemic, creating demand for visually appealing and functional printed packaging.

- Digital printing technologies have enhanced the market's development by enabling customized packaging options for luxury and mass-market cosmetic brands. This advancement has created opportunities for packaging manufacturers to address specific consumer preferences, mainly through personalized and limited-edition products.

- E-commerce has increased the demand for printed packaging as online retail companies seek branded, sturdy, and recyclable shipping materials. Custom boxes and branded mailers dominate this segment. The automotive and industrial sectors consistently demand printed packaging solutions, primarily using corrugated boxes and labels for parts and components.

- The market demonstrates a substantial shift toward sustainability across all sectors, influenced by consumer preferences and European Union packaging waste regulations. German companies implement recyclable, biodegradable, and renewable materials in their packaging solutions. Digital printing technologies enable customized, short-run packaging production that addresses environmental concerns and branding requirements. The market continues to evolve, with sustainability and innovation as fundamental drivers.

Europe Printed Packaging Industry Overview

Europe's Printed Packaging market is fragmented because many players run their businesses at national and international levels, with significant players like Amcor Group, Mondi plc, CCL Industries Inc.and among others. Mergers, acquisitions, and collaboration of relevant businesses and business units for strategic growth have been recurring market trends in the packaging industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Technological Advancement in the Printing Industry

- 5.1.2 Expanding End-user Packaging Applications

- 5.2 Market Restraint

- 5.2.1 Fluctuations in Raw Material Prices and Their Impact on the Cost of Printed Packaging

6 MARKET SEGMENTATION

- 6.1 By Printing Technology

- 6.1.1 Offset Lithography

- 6.1.2 Rotogravure

- 6.1.3 Flexography

- 6.1.4 Digital Printing

- 6.1.5 Screen Printing

- 6.2 By Ink Type

- 6.2.1 Solvent-based Ink

- 6.2.2 UV-curable Ink

- 6.2.3 Aqueous Ink

- 6.3 By Packaging Type

- 6.3.1 Label

- 6.3.2 Plastic

- 6.3.3 Glass

- 6.3.4 Metal

- 6.3.5 Paper and Paperboard

- 6.4 By Application

- 6.4.1 Cosmetic and Homecare

- 6.4.2 Food and Beverage

- 6.4.3 Pharmaceutical

- 6.4.4 Other Applications

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 Germany

- 6.5.3 France

- 6.5.4 Spain

- 6.5.5 Italy

- 6.5.6 Poland

- 6.5.7 Netherlands

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mondi plc

- 7.1.2 Ahlstrom Oyj

- 7.1.3 Autajon Group

- 7.1.4 Huhtamaki Oyj

- 7.1.5 CCL Industries Inc.

- 7.1.6 Clondalkin Group Holdings BV

- 7.1.7 Constantia Flexibles Group GmbH

- 7.1.8 Amcor Group

- 7.1.9 Smurfit Westrock plc

- 7.1.10 DS Smith PLC

- 7.1.11 International Paper Company