|

시장보고서

상품코드

1630381

동남아시아의 재생에너지 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Southeast Asia Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

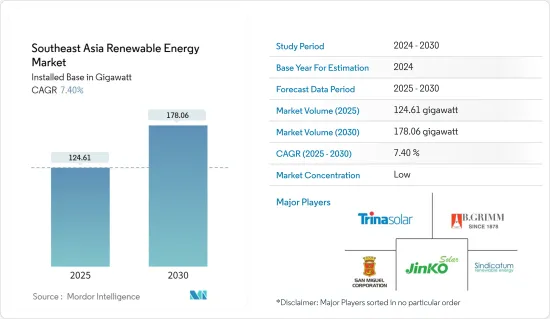

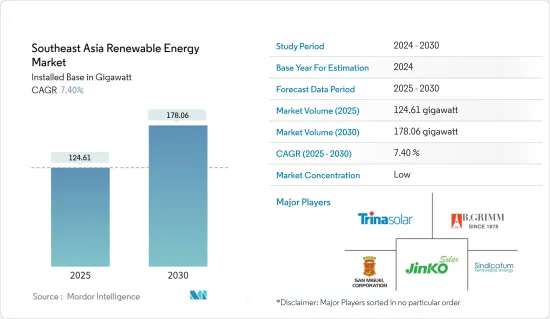

동남아시아의 재생에너지 시장 규모(설비용량 기준)는 2025년 124.61기가와트에서 2030년 178.06기가와트로 확대될 것이며, 예측 기간(2025-2030년) 동안 7.4%의 CAGR을 기록할 것으로 예상됩니다.

주요 하이라이트

- 동남아시아에서는 석탄 화력 발전이 주류를 이루고 있습니다. 그러나 재생에너지 발전 및 배터리 비용은 최근 몇 년 동안 석탄 화력 발전소의 자금 고갈과 함께 큰 폭의 하락을 기록했습니다. 이는 예측 기간 동안 동남아시아의 재생에너지 부문을 견인할 것으로 예상됩니다.

- 그러나 국제 기업의 투자 부족과 프로젝트 실용화 지연은 시장 성장을 저해할 것으로 예상됩니다.

- 동남아시아 지역에는 증가하는 에너지 수요를 충족시키기에 부족한 화석연료 자원이 존재하기 때문에 재생에너지 설비가 이 지역의 증가하는 에너지 수요를 해결할 수 있는 큰 기회를 창출할 수 있습니다.

- 베트남은 재생에너지 잠재력이 높아 예측 기간 동안 이 지역의 재생에너지 시장에서 우위를 점할 것입니다.

동남아시아의 재생에너지 시장 동향

태양에너지 부문이 괄목할만한 성장세를 기록

- 동남아시아는 가장 빠르게 성장하는 태양광 시장 중 하나이며, 태양광 산업의 세계 확장에 있어 가장 유망한 지역 중 하나이며, 2023년에는 베트남과 태국이 이러한 움직임의 최전선에 서서 이 지역에서 가장 많은 신규 태양광발전 용량을 설치하게 될 것입니다. 2023년 베트남의 태양광발전 설비용량은 1,707만kW, 태국의 설비용량은 318만kW에 달할 것으로 예상됩니다.

- 전력 수요 증가, 풍부한 태양광 자원, 유리한 재생에너지 관련 정책은 이 지역의 태양광발전 산업의 성장을 촉진하고 있습니다.

- 또한, 이 지역의 여러 국가 정책 입안자들은 태양광발전 및 인프라 투자를 촉진하는 활동 등 에너지 부문의 안전하고 저렴한 지속가능한 경로를 보장하기 위한 노력을 강화하고 있습니다.

- 2024년 4월, 필리핀 에너지부(DoE)는 태양광발전량을 2GW로 전환할 계획을 발표했습니다. 필리핀 정부는 2024년에 최소 4,165MW의 재생에너지와 재래식 전원을 혼합한 발전 프로젝트가 가동될 것으로 예상하고 있습니다. 여기에는 1,985MW의 태양광발전 설비의 상업 가동이 포함되며, 이 중 약 495MW는 이미 시험 가동 및 시운전 단계에 있으며, 6월까지 966.3MW가 추가로 가동될 것으로 예상됩니다.

- 그러나 동남아시아의 태양광발전(PV) 누적 용량은 2024년까지 35.8기가와트(GW)까지 증가할 수 있습니다. 각국이 설정한 높은 태양광발전 목표가 이를 뒷받침하고 있습니다. 신흥국들이 전력 믹스에서 재생에너지의 비중을 크게 늘리려는 움직임을 보이고 있어, 향후 5년에서 15년 사이에 이 지역에서 부유식 태양광발전소(PV) 개발이 활발해질 것으로 예상됩니다. 특히 태국과 베트남에서 개발 계획이 진행 중이며, 인도네시아, 싱가포르, 미얀마에서는 소규모 부유식 태양광발전소 개발이 제안되고 있습니다.

- 따라서, 위와 같은 관점에서 볼 때, 태양 에너지는 예측 기간 동안 동남아시아의 재생에너지 시장에서 큰 성장을 이룰 것으로 예상됩니다.

시장 독식하는 베트남

- 베트남은 수력, 태양광, 풍력, 바이오매스, 폐기물 등 재생에너지의 잠재력이 높습니다. 바이오매스와 수력발전은 현재 베트남에서 이용되는 재생에너지의 두 가지 주요 원천입니다. 정부는 2025년까지 11GW의 풍력발전과 20GW의 태양광발전을 도입하는 것을 목표로 하고 있으며, 이는 시장 성장을 촉진할 것으로 예상됩니다.

- 석탄화력발전소 및 대규모 수력발전소 개발을 둘러싼 환경 문제, 자금 조달 제약, 천연가스 산업 발전 지연, 정부의 원자력발전 프로젝트 중단 결정 등은 베트남에서 태양광 및 풍력발전의 성장 기회가 될 것으로 예상됩니다. 또한, 베트남의 재생에너지 프로젝트 개발에는 외국인 투자 규제가 적용되지 않기 때문에 베트남의 재생에너지 부문은 과거 해외 투자로 인해 성장세를 이어왔습니다.

- 베트남은 아시아에서 가장 빠르게 경제가 성장하고 있는 국가 중 하나이며, 이에 따라 국내 전력 수요도 증가하고 있습니다. 급성장하는 산업과 인구 증가로 인한 전력 수요는 향후 신규 발전소 건설을 초과하여 심각한 전력 부족을 초래할 것으로 예상되며, 2030년까지 현재 설치된 5,400만kW의 두 배 이상인 1억 3,000만kW의 발전 설비가 설치될 것으로 예상됩니다. 설치될 전망입니다.

- 베트남의 에너지 수요는 향후 5년간 매년 10%씩 증가할 것으로 예상되며, 필요한 발전 용량은 두 배로 증가할 것으로 예상됨에 따라 베트남은 재생에너지 발전량을 늘리는 등 에너지 믹스를 다양화하기 위한 노력을 기울이고 있습니다. 옥상 태양광발전 시장은 베트남의 막대한 에너지 수요를 충족시키는 데 중요한 역할을 할 것으로 기대됩니다.

- 2024년 1월 베트남전력(EVN)은 하노이에서 열린 제46회 베트남-라오스 양자협력 정부간위원회에서 라오스 26개 수력발전소로부터 2,689MW의 전력을 구매하는 19건의 전력 구매 계약을 체결했습니다. 이번 계약 체결은 베트남과 라오스의 전력 협력의 심화를 보여주었습니다.

- 이상으로 볼 때, 예측 기간 동안 베트남은 이 지역의 재생에너지 시장을 독점할 것으로 예상됩니다.

동남아시아의 재생에너지 산업 개요

동남아시아의 재생에너지 시장은 비교적 세분화되어 있습니다. 이 시장의 주요 기업으로는 Sindicatum Renewable Energy Company Pte Ltd, Trina Solar, Jinko Solar Holding, B.Grimm Group, San Miguel Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 동남아시아의 재생에너지 믹스(2023년)

- 재생에너지 설비 용량과 2029년까지 예측(단위 : GW)

- 최근 동향과 개발

- 정부 시책, 목표, 규제와 시책

- 시장 역학

- 성장 촉진요인

- 재생에너지 발전에 대한 투자 증가

- 유리한 정부 시책

- 성장 억제요인

- 재생에너지 초기 비용이 높다

- 성장 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 유형별

- 태양광

- 풍력

- 수력

- 바이오에너지

- 기타

- 지역별

- 베트남

- 인도네시아

- 필리핀

- 태국

- 말레이시아

- 기타 동남아시아 지역

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd

- Sindicatum Renewable Energy Company Pte Ltd

- Trina Solar Co. Ltd

- San Miguel Corporation

- B.Grimm Group

- Thanh Thanh Cong(TTC) Group

- BCPG Public Company Limited(BCPG)

- Gulf Energy Development PCL

- 시장 순위/점유율(%) 분석

제7장 시장 기회와 향후 동향

- 동남아시아의 해상 풍력발전 포텐셜과 프로젝트

The Southeast Asia Renewable Energy Market size in terms of installed base is expected to grow from 124.61 gigawatt in 2025 to 178.06 gigawatt by 2030, at a CAGR of 7.4% during the forecast period (2025-2030).

Key Highlights

- Coal-fired power generation is the dominant form of power generation in Southeast Asia. However, renewable power generation and battery costs registered a significant decline in recent years, combined with the drying up of the finances for coal-fired power plants. This is expected to drive the renewable energy sector in Southeast Asia during the forecast period.

- However, the lack of international companies' investments and the delay in the practical deployment of projects are expected to hinder the market's growth.

- The Southeast Asian region has insufficient indigenous fossil fuel resources to meet its growing energy demand, thus creating significant opportunities for renewable energy installations, which can then solve the region's ever-increasing energy demand.

- Vietnam has a high potential for renewable energy, thus creating its dominance in the region's renewable energy market during the forecast period.

Southeast Asia Renewable Energy Market Trends

Solar Energy Segment to Witness Significant Growth

- Southeast Asia is becoming one of the fastest-growing solar energy markets and one of the most promising regions in the global expansion of the solar energy industry. In 2023, Vietnam and Thailand were at the forefront of this movement, with the region's highest amount of new PV capacity installed. In 2023, Vietnam's installed solar energy capacity stood at 17.07 GW, while Thailand's installed solar capacity stood at 3.18 GW.

- The increasing demand for electricity, the abundance of solar resources in the region, and favorable renewable-related policies are some of the factors that have been favoring the growth of the solar industry in the region.

- In addition, policymakers across different countries in the region have been intensifying their efforts to ensure a secure, affordable, and sustainable pathway for the energy sector, which includes activities to facilitate investment in solar power generation and infrastructure.

- In April 2024, the Philippines Department of Energy (DoE) announced its plans to switch to 2 GW of solar power generation. The government expects at least 4,165 MW of power projects to come online in 2024 in a mix of renewable and conventional sources. This includes the start of commercial operation of 1,985 MW of solar capacities, of which some 495 MW are already in the testing and commissioning stage, and an additional 966.3 MW should come online by June.

- However, Southeast Asia's cumulative solar photovoltaic (PV) capacity could increase to 35.8 gigawatts (GW) by 2024. The high solar power generation targets set by various nations lend support to this. The region is expected to witness the development of floating solar photovoltaic (PV) power plants over the next 5 to 15 years, as countries in the region are looking to substantially increase their share of renewable energy in the power mix. Moreover, development plans are in progress, particularly in Thailand and Vietnam, while smaller utility-scale floating PV developments are being proposed in Indonesia, Singapore, and Myanmar.

- Therefore, owing to the points listed above, solar energy is expected to witness significant growth in the Southeast Asian renewable energy market during the forecast period.

Vietnam to Dominate the Market

- Vietnam has a high potential for renewable energy, including hydro, solar, wind, biomass, and waste. Biomass and hydropower are the two major sources of renewable energy currently used in Vietnam. The government aims to install 11 GW of wind power and 20 GW of solar power capacity by 2025, which is expected to foster the growth of the market.

- The environmental concerns and constraints in financing over the development of coal-fired and large-scale hydropower plants, the slow development of the natural gas industry, and the government's decision to suspend nuclear power projects are expected to provide an opportunity for the growth of solar and wind power in the country. Moreover, the renewable energy sector in the country has witnessed growth in the past, owing to investment from overseas, as there are no foreign ownership restrictions that apply to the development of renewable energy projects in Vietnam.

- Vietnam is one of the fastest-growing economies in Asia, and thus, the power demand in the country is increasing. The nation's demand for electricity, pushed up by its booming industry and a growing population, is expected to outstrip the construction of new power plants in the future, causing severe power shortages. By 2030, the country is expected to install 130 GW of electricity generation facilities, more than double the 54 GW currently installed.

- With Vietnam's energy demand projected to increase by 10% annually in the next five years and the required power capacity to double, the country has been taking initiatives to diversify its energy mix, including plans to generate more power from renewable sources. The rooftop solar market is expected to play a crucial role in helping Vietnam meet its massive energy needs.

- In January 2024, State utility Vietnam Electricity (EVN) entered 19 power purchase agreements for the acquisition of 2,689 MW of electricity from 26 hydropower plants in Laos during the 46th meeting of the Vietnam-Laos Intergovernmental Committee for Bilateral Cooperation in Hanoi. The signing of the agreements demonstrated deeper cooperation in electricity between Vietnam and Laos.

- Thus, owing to the points listed above, Vietnam is expected to dominate the renewable energy market in the region during the forecast period.

Southeast Asia Renewable Energy Industry Overview

The Southeast Asian renewable energy market is moderately fragmented. Some of the major companies in the market (in no particular order) include Sindicatum Renewable Energy Company Pte Ltd, Trina Solar Co. Ltd, Jinko Solar Holding Co. Ltd, B.Grimm Group, and San Miguel Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definiton

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Southeast Asia Renewable Energy Mix, 2023

- 4.3 Renewable Energy Installed Capacity and Forecast in GW, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies, Targets, and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Increasing Investments in Renewable Energy Generation

- 4.6.1.2 Favorable Government Policies

- 4.6.2 Restraints

- 4.6.2.1 Initial Cost of Renewable Energy Is High

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Solar

- 5.1.2 Wind

- 5.1.3 Hydro

- 5.1.4 Bioenergy

- 5.1.5 Other Types

- 5.2 By Geography

- 5.2.1 Vietnam

- 5.2.2 Indonesia

- 5.2.3 Philippines

- 5.2.4 Thailand

- 5.2.5 Malaysia

- 5.2.6 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Canadian Solar Inc.

- 6.3.2 JinkoSolar Holding Co. Ltd

- 6.3.3 Sindicatum Renewable Energy Company Pte Ltd

- 6.3.4 Trina Solar Co. Ltd

- 6.3.5 San Miguel Corporation

- 6.3.6 B.Grimm Group

- 6.3.7 Thanh Thanh Cong (TTC) Group

- 6.3.8 BCPG Public Company Limited (BCPG)

- 6.3.9 Gulf Energy Development PCL

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Southeast Asia's Offshore Wind Potential and Projects