|

시장보고서

상품코드

1631611

미국의 멀티테넌트(코로케이션) 데이터센터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)US Multi-Tenant (Colocation) Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

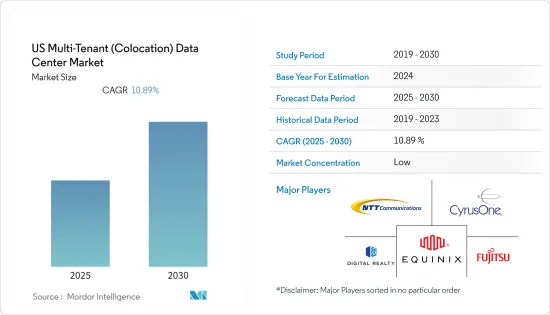

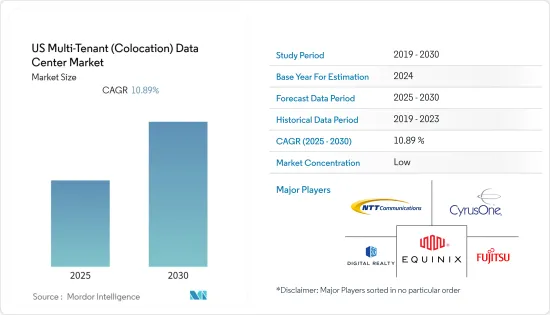

미국의 멀티테넌트 데이터센터 시장은 예측 기간 동안 10.89%의 CAGR을 기록할 것으로 예상됩니다.

미국 멀티테넌트(코로케이션) 데이터센터 시장은 예측 기간 동안 10.89%의 CAGR을 기록할 것으로 예상됩니다.

주요 하이라이트

- 미국은 데이터센터 수가 가장 많은 국가 중 하나입니다. 미국에서는 대형 하이퍼스케일 테넌트의 사업 확대로 인해 멀티테넌트 데이터센터 임대 활동이 활발하게 이루어지고 있습니다.

- IoT, 인공지능 등의 분야에서 기술의 급속한 발전과 함께 데이터센터의 트래픽이 증가하고 있습니다. 시스코의 예측에 따르면, 네트워크에 연결된 기기는 2018년 27억 대에서 2023년 46억 대에 달할 것이라고 합니다. 또한 스마트폰은 올해까지 전체 네트워크 연결 기기의 7%를 차지할 것으로 예상됩니다.

- 정부, 소매, 의료, IT, 통신 등 최종사용자 수직 분야의 급속한 디지털화도 국내 멀티테넌트 시장의 지평을 넓히고 있습니다. 정부의 디지털화 전략은 국가가 완전한 디지털 운영으로 나아가고 있음을 보여주는 한 예입니다.

- 그러나 규제 상황과 엄격한 보안 요구사항에 대한 의존도가 높아지면서 HIPAA, PCI DSS와 같은 표준이 표준 체크포인트가 되는 등 국내 시장에 악영향을 미치고 있습니다.

- 버지니아 북부와 실리콘밸리와 같은 시장은 각각 5.1%, 1.6%의 공실률을 기록하고 있지만, 전력과 토지의 제약이 여전히 영향을 미치고 있습니다. 변전소 납품 지연이 버지니아 북부가 겪고 있는 문제의 주요 원인이며, 발전량 부족은 아닙니다. 실리콘밸리에는 공급측과 발전측의 전력 문제가 모두 존재합니다. 이 때문에 이미 공급에 제약이 있는 시장에서는 새로운 성장이 어려워질 수 있습니다. 두 시장 모두 필요한 지역의 제한된 개발 가능한 토지를 보완하기 위해 더 많은 수직 다층 데이터센터 건물을 기대하고 있습니다.

- COVID-19는 코로케이션 서비스 제공업체들의 건설 및 확장 계획에 혼란을 가져왔습니다. 단기적으로는 전염병으로 인해 건설 및 확장 일정이 불투명해졌습니다. 봉쇄로 인한 인력에 대한 직접적인 영향 외에도 엄격한 절차 지침의 영향으로 업무에 차질을 빚고 있습니다.

미국의 멀티테넌트(코로케이션) 데이터센터 시장 동향

헬스케어 분야가 큰 비중을 차지

- 헬스케어 산업은 방대한 양의 데이터를 생성합니다. 많은 의료 부문은 임상시험이나 여러 외래 환자 기록에서 데이터를 수집하고, 이를 통해 의미 있는 분석을 도출하고자 합니다. 그러나 이러한 데이터 수집에 관여하는 많은 병원들은 관련 인프라를 갖추지 못하고 있습니다.

- 그 결과, 많은 헬스케어 기관들은 기업의 비용 구조를 줄이고, 완전한 규제 준수와 효율적인 솔루션을 제공해야 한다는 압박에 직면해 있으며, 생성되는 데이터의 양 증가에 대한 제약에 직면해 있습니다. 데이터센터 코로케이션은 모든 기업에게 비용 절감을 위한 적절한 대안을 제공합니다.

- 정부는 의료 시설의 디지털 프로세스 도입으로 전환을 지원하고 있습니다. 이는 멀티테넌트 데이터센터 시장에 새로운 기회를 창출하고 있습니다.

- 2022년 6월, 미국 보건복지부(HHS)의 의료정보기술조정관실(ONC)은 미국의 공중보건정보학 및 데이터 과학을 강화하기 위해 8,000만 달러 규모의 공중보건정보학 및 기술 인력 개발 프로그램(PHIT 인력 프로그램)을 설립한다고 발표하였습니다.

- 비상장 헬스케어 기업이 멀티테넌트 데이터센터 제공업체와 파트너십을 맺고 새로운 클라우드 및 공간 관리 기능을 활용할 것으로 확인된 가운데, 2022년 2월 선가드 가용성 서비스는 NYU Langone Health를 위한 코로케이션 데이터센터의 완공을 발표했습니다. 이 1MW 규모의 시설은 5,000평방피트 면적에 2N의 이중화 기능을 갖추고 있으며, 버티브의 DSE 고효율 데이터센터 냉각 솔루션을 사용하고 있습니다. 이 데이터센터를 통해 NYU Langone은 공간, 전력 및 지출을 보다 효율적으로 관리할 수 있게 되었습니다. 또한, 이 의료 센터는 퍼블릭 클라우드 및 SaaS 제공업체에 접근할 수 있게 되었습니다.

클라우드 애플리케이션 도입 확대가 시장 주도

- 국내 클라우드 기반 솔루션에 대한 수요는 기술 적용과 소비자의 클라우드 지향성 증가로 인해 급증하고 있습니다. 이 기술을 통해 사용자는 원격지에서도 데이터에 접근할 수 있습니다.

- 온프레미스 인프라를 구축하고 유지하는 것보다 데이터를 클라우드로 이전하여 비용과 리소스를 절약하는 것이 중요하다는 인식이 확산되면서 클라우드 기반 솔루션에 대한 수요가 증가하고 있습니다. 이에 따라 클라우드 기반 컨택센터 서비스 도입이 새롭게 증가하고 있습니다.

- 퍼블릭 클라우드에 대한 지출은 모든 종류의 기업에서 이용이 증가하고 있으며, 이제 IT 예산의 중요한 항목이 되었습니다. 연간 1,200만 달러 이상을 클라우드에 지출하는 기업은 전체의 37%, 120만 달러 이상을 지출하는 기업은 전체의 80%에 달합니다. 중소기업은 워크로드 수가 적고 규모도 작기 때문에 클라우드 비용이 저렴합니다. 그러나 지난해에 비해 120만 달러 이상을 지출하는 중소기업은 53%로 38%에서 증가했습니다.

- Flexera 2022 State of the Cloud Report에 따르면, COVID-19의 영향으로 클라우드 이용이 현재 계획된 이용량을 초과할 수 있다는 의견이 여러 기업에서 일치했습니다. 기업들은 온라인 사용 증가에 따른 수요 증가에 대응해야 하며, 그 결과 현재 클라우드 기반 애플리케이션에 필요한 여분의 용량을 확보해야 합니다. 기업의 59% 이상이 클라우드 사용이 계획보다 크게 증가할 것으로 예상하고 있으며, 중소기업(SME)의 약 50%는 클라우드 사용이 확대될 것으로 예상하고 있습니다.

- COVID-19 사태로 인해 많은 비즈니스 패러다임이 바뀌었음에도 불구하고, 대부분의 응답자들은 클라우드 도입의 주요 요인으로 기업의 성장과 혁신을 꼽았습니다. 클라우드는 또한 기업이 폐쇄적인 상황과 일관성 없는 IT 인프라를 극복하는 데 중요한 역할을 했으며, 보다 빠른 개발, 시장 출시 속도, 민첩성 및 대응력을 향상시키는 데 중요한 역할을 했습니다.

미국의 멀티테넌트(코로케이션) 데이터센터 산업 개요

데이터센터 코로케이션 시장은 많은 기업이 존재하기 때문에 세분화되어 있습니다. Digital Realty Trust, Inc., NTT Communications, IBM Corporation, CyrusOne, Fujitsu Americas Inc., Equinix Networks 등이 이 시장의 주요 업체로 꼽힙니다. 또한, 치열한 경쟁에 직면한 많은 시장 기업들은 시장 지위를 유지하고 시장 침투율을 높이기 위해 제휴, 개발 등 다양한 전략을 채택하고 있습니다.

2023년 1월, Equinix는 코로케이션 데이터센터 사업자 중 최초로 데이터센터 내 작동 온도 범위를 확대하여 총 전력 소비를 줄이기 위해 노력했습니다. Equinix는 보다 효율적인 냉각을 실현하고 하이엔드 운영 환경을 유지하면서 탄소 배출량을 줄이기 위해 열 운영과 관련된 세계 로드맵을 개발하고 있습니다. 공급망의 지속가능성이 현대 기업의 환경 이니셔티브에 필수적인 요소로 떠오르고 있는 가운데, Equinix의 수천 명의 고객이 데이터센터 운영에 따른 Scope 3 탄소 배출량을 줄일 수 있을 것으로 기대됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

- 업계 밸류체인 분석

- COVID-19가 멀티테넌트 데이터센터 산업에 미치는 영향

- 멀티테넌트 형태 프로바이더에 의한 하이퍼스케일 데이터센터에의 주요 투자 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 클라우드 서비스 채용 확대에 의한 시장 활성화

- 도매·데이터센터 멀티테넌트·공간의 성장에 밤수요 증가(기반은 낮은 것)

- 데이터 규제에 대한 대응 중시 상승과 멀티테넌트 형태 시설 비용 효율 높이가 중소기업 로의 도입을 촉진

- 시장 성장 억제요인

- 규제 상황과 엄격한 보안 요건에 대한 의존

제6장 시장 세분화

- 솔루션 유형별

- 도매 멀티테넌트

- 리테일 멀티테넌트

- 조직 규모별

- 중소기업

- 대기업

- 업계별

- BFSI

- 제조업

- IT·통신

- 헬스케어 및 생명과학

- 정부기관

- 엔터테인먼트와 미디어

- 기타 최종 이용 업계별

제7장 경쟁 구도

- 기업 개요

- Digital Reality Trust, Inc.

- NTT Communications

- Equinix Networks

- Fujitsu Americas Inc.(Fujitsu Ltd)

- CyrusOne

- Rackspace Inc.

- IBM Corporation

- Internap Corporation

- Coresite Reality Corporaton

- CenturyLink Inc.

- Quality Technology Services

- KDDI Corporation

제8장 투자 분석

제9장 시장 기회와 향후 동향

ksm 25.02.06The US Multi-Tenant Data Center Market is expected to register a CAGR of 10.89% during the forecast period.

The United States multi-tenant (colocation) data center market is expected to register a CAGR of 10.89% during the forecast period.

Key Highlights

- The United States is one of the major countries in terms of the number of data centers. The multi-tenant data center leasing activity in the United States has been increasing due to the expansion activities of some of the major hyperscale tenants operating there.

- The growing data center traffic, in parallel to the rapid technology advancements in areas such as IoT and Artificial Intelligence, among others, is leading to an increase in the data traffic in the country. According to Cisco forecasts, there will be 4.6 billion networked devices by 2023, rising from 2.7 billion in 2018. In addition, smartphones are expected to account for 7% of all networked devices by the current year.

- The rapid digitization in end-user verticals such as government, retail, healthcare, IT, and Telecom is also expanding the horizon for the multi-tenant market in the country. The government's digitization strategy is an example that the country is moving towards complete digital operations.

- However, challenges such as a heightened dependence on the regulatory landscape & stringent security requirements have adversely impacted the market in the country. The standards such as HIPAA, PCI DSS, and others prevail as standard checkpoints.

- Markets like Northern Virginia and Silicon Valley, with 5.1% and 1.6% vacancy rates, respectively, are still impacted by electricity and land constraints. Delays in the delivery of the substations are the leading cause of the challenges Northern Virginia is experiencing, not a lack of power production. Both delivery-side and generation-side electricity problems exist in Silicon Valley. This could make it difficult for new growth in a market where supply is already constrained. Both markets expect more vertical, multi-story data center buildings to compensate for the limited amount of developable land in necessary districts.

- The pandemic resulted in disruptions in construction & expansion plans for colocation service providers. In the short term, the pandemic has created uncertainty regarding construction and expansion timelines. With a direct effect on labor due to lockdowns, the allied crunch caused in the operations was also partly due to stringent guidelines of procedures.

US Multi-Tenant (Colocation) Data Center Market Trends

Healthcare Sector Accounts for Significant Share

- The healthcare industry generates enormous amounts of data. Many healthcare departments are collecting data from clinical trials and several outpatient records to analyze and derive meaningful analysis from such data. However, most hospitals involved in such data collection are not equipped with relevant infrastructure.

- As a result, many healthcare institutes face pressure to reduce a company's cost structure, to deliver full regulatory compliance and efficient solutions, with constraints about the increasing amount of data generated. Datacenter collocation provides a suitable alternative to enable cost-saving means for any firm.

- The government has supported the growing transition of healthcare facilities to adopt digital processes. This has presented an influx of new opportunities for the market of multi-tenant data centers.

- In June 2022, the United States Department of Health and Human Services (HHS) Office of the National Coordinator for Health Information Technology (ONC) announced the establishment of a USD 80 million Public Health Informatics & Technology Workforce Development Program (PHIT Workforce Program) to strengthen US public health informatics and data science.

- Privatized healthcare companies are observed partnering with multi-tenant data center providers to leverage new cloud and space management capabilities. In February 2022, Sungard Availability Services announced the completion of a colocation data center for NYU Langone Health. The 1MW facility has 5,000 square feet of raised floor space, 2N redundancy, and utilizes Vertiv's DSE High-Efficiency data center cooling solution. The data center helped NYU Langone manage its space, power, and spending more effectively. It also allowed the medical center to access public clouds and SaaS providers.

Growing Adoption of Cloud Applications is Expected to Drive the Market

- The demand for cloud-based solutions in the country is surging due to the growing application of technology and consumer propensity toward the cloud. This technology allows the user to access the data from remote locations.

- The increasing realization among companies about the importance of saving money and resources by moving their data to the cloud rather than building and maintaining on-premise infrastructure is driving the demand for cloud-based solutions. Hence, the adoption of cloud-based contact center services is increasing with new.

- Public cloud spending has increased for businesses of all kinds due to increased usage, and it is now a sizeable line item in IT budgets. Enterprises reported spending over USD 12 million annually in 37% of cases and over USD 1.2 million in clouds in 80% of cases. SMBs would have cheaper cloud costs since they have fewer and smaller workloads. However, 53% of SMBs spent more than $1.2 million compared to last year, an increase from 38%.

- According to the Flexera 2022 State of the Cloud Report, several enterprises agreed that their cloud usage might exceed the planned use at present, owing to the impact of the COVID-19 pandemic. Enterprises are forced to meet increased demand as online usage grows, resulting in the need for the extra capacity required for current cloud-based applications. Over 59% of enterprises expect their cloud usage to be significantly higher than planned, and about 50% of small- and medium-sized enterprises (SMEs) expect their cloud usage to escalate.

- Even though the COVID-19 pandemic changed many business paradigms, most respondents cited company growth and transformation as the main forces behind cloud adoption. Cloud also played a crucial part in assisting businesses to survive lockdown situations and inconsistent IT infrastructure, allowing them to develop more quickly and improve speed to market, agility, and responsiveness.

US Multi-Tenant (Colocation) Data Center Industry Overview

The data center colocation market is fragmented due to the presence of many players. Some of the prominent players in the market include Digital Realty Trust, Inc., NTT Communications, IBM Corporation, CyrusOne, Fujitsu Americas Inc., and Equinix Networks, among others. Moreover, in the face of intense competition, many market players are adopting various strategies to maintain their position and increase their market penetration, such as partnerships and developments. Recent developments include:

In January 2023, Equinix, Inc. became the first colocation data center operator to commit to reducing its total power consumption by increasing the operating temperature ranges within its data centers. Equinix is developing a global roadmap for thermal operations to achieve more efficient cooling and reduce carbon impacts while maintaining its high-end operating environment. As supply chain sustainability becomes an essential aspect of modern businesses' environmental initiatives, it is expected to enable thousands of Equinix customers to reduce their Scope 3 carbon emissions associated with data center operations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on Multi-tenant Data Center Industry

- 4.5 Analysis of key investments made by multi-tenant providers in hyperscale data centers

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Cloud Services is expected to flourish the market

- 5.1.2 Increasing Growth in Wholesale Datacenter Multi-tenant Spaces to propel demand (albeit from a lower base)

- 5.1.3 Increased Emphasis on Compliance with Data Regulations and Cost-Effective Nature of Multi-tenant Facilities to Drive Adoption among SME's

- 5.2 Market Restraints

- 5.2.1 Dependence on Regulatory Landscape & Stringent Security Requirements

6 MARKET SEGMENTATION

- 6.1 By Solution type

- 6.1.1 Wholesale Multi-tenant

- 6.1.2 Retail Multi-tenant

- 6.2 By Size of the organization

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 By End-user Vertical

- 6.3.1 BFSI

- 6.3.2 Manufacturing

- 6.3.3 IT and Telecom

- 6.3.4 Healthcare & Lifesciences

- 6.3.5 Government

- 6.3.6 Entertainment and Media

- 6.3.7 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Digital Reality Trust, Inc.

- 7.1.2 NTT Communications

- 7.1.3 Equinix Networks

- 7.1.4 Fujitsu Americas Inc. (Fujitsu Ltd)

- 7.1.5 CyrusOne

- 7.1.6 Rackspace Inc.

- 7.1.7 IBM Corporation

- 7.1.8 Internap Corporation

- 7.1.9 Coresite Reality Corporaton

- 7.1.10 CenturyLink Inc.

- 7.1.11 Quality Technology Services

- 7.1.12 KDDI Corporation