|

시장보고서

상품코드

1635353

전력 산업용 밸브 시장 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Global Valves in Power Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

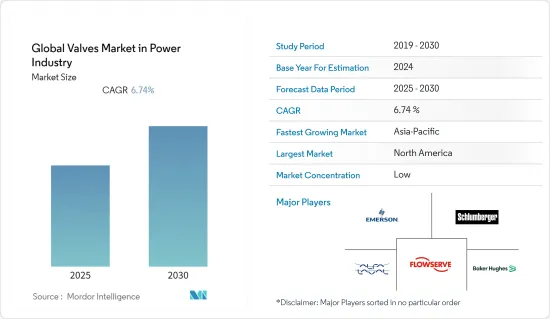

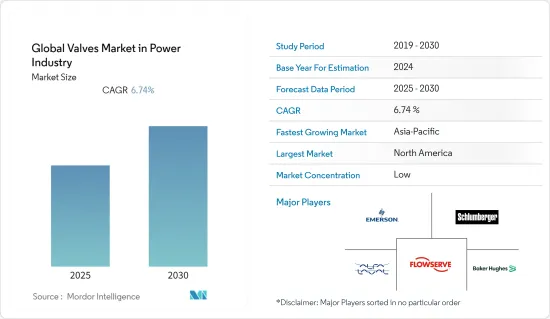

세계의 전력 산업용 밸브 시장은 예측 기간 중 CAGR 6.74%를 기록할 전망

주요 하이라이트

- 기후 변화 및 전력 생산을 위한 더 나은 재생하고 덜 손상된 자원을 개발해야 할 필요성으로 인해 전력 소비가 증가하고 있습니다. 이에 따라 발전소용 산업용 밸브 제조업체들은 전력 생산 효율을 향상시킬 수 있는 공정 기계를 찾고 있습니다.

- 또한 인수 및 제휴와 같은 전략적 개발 증가는 성장률을 강화하도록 설정되어 있습니다. 예를 들어 2022년 4월 Vexve Armatury Group은 오스트리아 및 독일 시장에서 전력, 가스 및 야금 부문에 ARMATURY Group 밸브를 판매하는 Armatury Group GmbH를 인수했습니다. 이번 인수로 Vexve Armatury Group은 특히 DACH 지역(독일, 오스트리아, 스위스)에서의 입지를 강화했습니다.

- COVID-19는 공급망에 혼란을 가져왔고, 가동이 중단된 에너지 생산에 큰 영향을 미쳤습니다. 그러나 그 영향은 단기적인 것입니다.

- 추가 비용과 함께 밸브 교체 비용이 많이 듭니다. 장비를 분해하고 다시 조립해야 합니다. 밸브 재고 관리에 필요한 인력과 자재에도 비용이 발생합니다. 또한 오래된 밸브를 폐기할 때 발생하는 환경 파괴로 인한 비용도 발생합니다. 이 모든 것은 직원들의 초과 근무로 인한 고객에 대한 추가 비용과 시설의 일시적인 가동 중단으로 인한 매출 손실에 더해 발생하는 비용입니다. 이것이 시장 성장 억제요인으로 작용하고 있습니다.

밸브의 전력 부문 시장 동향

성장하는 전력 부문이 시장 성장의 원동력이 될 것으로 전망

- 발전 용도는 각기 다른 유량 제어 요구 사항이 필요합니다. 따라서 발전소의 특정 파이프라인 시스템에는 다양한 밸브가 포함될 수 있습니다. 발전소용 산업용 밸브도 파이프라인 시스템의 특정 영역에서 발생하는 작업에 따라 다양한 역할을 수행해야 합니다.

- 또한 재생 에너지 플랜트의 다양성으로 인해 공정의 한쪽에는 저온 및 저압 원료가 사용되고 다른 쪽에는 고온 및 고압 증기가 사용되는 등 각 공정마다 다른 밸브가 필요합니다. 이러한 플랜트에서는 관련 정확한 임무에 따라 특정 활동을 수행하기 위해 다양한 유형의 밸브를 사용하는 것은 드문 일이 아닙니다.

- 원자력발전소에서는 유체 유속을 제어하기 위해 제어 밸브를 자주 사용하며, 한 원자력발전소의 주요 회로에는 1,500개 이상의 제어 밸브가 있습니다. 제어 밸브를 통해 유속을 정확한 양의 증기와 물로 전달하여 원자력발전소의 에너지 효율을 보장 할 수 있습니다. 원자로는 전 세계 전력의 약 10%를 생산하고 있습니다. 현재 발전 용량의 약 15%에 해당하는 55기의 원자로가 현재 건설 중입니다.

- 또한 원자력발전소 개발에 대한 정부의 지원이 확대되고 있는 것도 시장 성장률을 높이는 요인으로 작용하고 있습니다. 예를 들어 미국 정부는 2021년 11월 초당파적 인프라 법안을 발표했습니다. 이 법은 미국 에너지부(DOE)가 청정 에너지 경제로의 전환을 지원하기 위해 620억 달러 이상의 자금을 지원하며, 미국 최대 단일 청정 전원인 원자력을 활용하도록 규정하고 있습니다. 이 법안에는 2028년까지 미국내 2기의 첨단 원자로를 실증할 수 있도록 약 25억 달러가 포함되어 있으며, 민간 원자력 크레딧 프로그램을 시작하기 위한 60억 달러가 포함되어 있습니다.

북미가 시장의 주요 점유율을 차지할 것으로 분석됨

- 북미는 발전소의 존재감이 크기 때문에 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 또한 미국은 가동 중인 원자로가 가장 많습니다. 미국에는 92기의 원자로가 가동 중이며 총 용량은 94.7GWe에 달할 전망입니다. 캐나다에는 총 13.6GWe의 순 용량을 가진 19기의 원자로가 가동 중이며, 2020년 미국과 캐나다의 원자력발전소는 각각 14.6%와 19.7%의 전력을 생산했다(출처: 세계원자력협회).

- 또한 발전용 밸브에 첨단 기술을 통합하기 위한 협력 관계가 증가함에 따라 예측 기간 중 시장 성장률을 높일 것으로 분석됩니다. 예를 들어 2021년 5월 Curtiss-Wright의 원자력 사업부는 Exelon Generation Company LLC와 밸브 프로그램의 성능 데이터를 라이선스하는 계약을 체결했다고 발표했습니다. 성능 데이터를 사용하여 StressWave 초음파 누출 감지 기술의 효율성을 개선하고 미국 원자력발전소 및 발전 부문 전반에 걸쳐 밸브 평가, 분석 및 성능 베스트 프랙티스의 채택을 촉진하기 위해 협력할 예정입니다.

- 아시아태평양은 예측 기간 중 괄목할 만한 성장을 이룰 것으로 분석됩니다. 전력 부문의 큰 수요가 시장을 주도하는 요인입니다. 예를 들어 2021년중국의 발전량은 8조 1,100억 킬로와트시(KWh)로 전년 대비 8.1% 증가했으며, 2021년발전량은 2019년보다 11% 증가하여 지난 2년동안 평균 5.4% 증가했으며, 12월중국의 풍력, 태양 광 및 원자력 에너지 생산량은 각각 전년 대비 30.1%, 18.8%, 5.4% 증가했습니다, 전년 대비 각각 30.1%, 18.8%, 5.7% 증가했다(출처: 중국 국가통계국(NBS)).

- 또한 발전 부문 수요를 충족시키기 위한 제품 혁신 증가는 시장의 요구에 더욱 기여하고 있으며, 2022년 5월 ARMATURY 그룹은 필리핀의 수력 발전 시설을 위해 DN이 1,800-2,000개의 버터플라이 밸브 3종을 생산했다고 발표했습니다. 차단 밸브인 버터플라이 밸브 L32.71 PN 10과 PN 6은 파이프라인을 통과하는 작동 매체의 통로를 완전히 열고 닫을 수 있습니다.

밸브 산업의 전력 부문 개요

세계의 전력 산업용 밸브 시장은 세분화되어 있고 경쟁이 치열한 것으로 분석됩니다. 각 회사는 시장 점유율과 수익성을 높이기 위해 전략적 공동 구상을 활용하고 있습니다. 제조업체들은 M&A를 통해 제품군을 개선하고 더 큰 시장 점유율을 확보할 수 있을 것입니다. 주요 기업으로는 Emerson Electric Co., Schlumberger Limited, Alfa Laval Corporate AB, Flowserve Corporation, Crane Co. 등이 있습니다.

- 2021년 12월-Severn과 LB Bentley를 포함한 고급 밸브 엔지니어링 및 제조 전문 다국적 기업인 Severn Group은 까다로운 용도를 위한 금속 시트 누출 방지 격리 밸브 제품 설계 및 제조의 선구자인 Severn ValveTechnologies를 인수했습니다. 이번 계약은 Severn Group이 산업 에너지 산업을 위한 가혹한 서비스 밸브 분야의 세계적인 선도 기업이 되겠다는 목표를 향한 발판이며, Severn 및 LB Bentley와 함께 ValveTechnologies는 더 큰 그룹의 일원으로서 더 많은 리소스와 지식을 활용할 수 있게 되었습니다. 더 많은 자원과 지식을 활용할 수 있게 되지만, 경영적으로는 독립성을 유지합니다.

- 2021년 6월 - Neles Corp는 Flowrox의 밸브 및 펌프 사업을 인수하는 자산 인수 계약을 체결했습니다. 양사는 광업, 광물 처리, 야금, 건설, 에너지, 환경 및 화학 산업을 위한 밸브 및 펌프 솔루션을 개발 및 제조하고 있습니다. 이러한 솔루션에는 핀치 밸브, 나이프 게이트 밸브, 페리스터 펌프 등이 포함됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자·소비자의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 강도

- 밸류체인/공급망 분석

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 세계 경제에서 전력 부문의 성장

- 전력 산업에서 스마트 밸브의 채택

- 시장 성장 억제요인

- 표준화된 시책의 결여와 높은 교환 비용

제6장 시장 세분화

- 유형별

- 볼

- 버터플라이

- 게이트/글러브/체크

- 플러그

- 컨트롤

- 기타

- 지역

- 북미

- 유럽

- 아시아태평양

- 기타

제7장 경쟁 구도

- 기업 개요

- Emerson Electric Co.

- Schlumberger Limited

- Alfa Laval Corporate AB

- Flowserve Corporation

- Crane Co.

- Baker Hughes

- Valmet Oyj

- KITZ Corporation

- IMI Critical Engineering

- L&T Valves Limited

제8장 투자 분석

제9장 향후 동향

KSA 25.01.31The Global Valves Market in Power Industry is expected to register a CAGR of 6.74% during the forecast period.

Key Highlights

- Power consumption is increasing due to climate change and the need to develop better, renewable, and less damaging resources to create electricity. Due to this, manufacturers of industrial valves for the power plant sector look for process machinery that can improve the effectiveness of electricity production.

- Further, the growing strategic developments such as acquisitions, collaborations, and so on are set to bolster the growth rate. For instance, in April 2022, Vexve Armatury Group acquired Armatury Group GmbH, a distributor of ARMATURY Group valves in the Austrian and German markets for the power, gas, and metallurgy sectors. Through the acquisition, Vexve Armatury Group's position is strengthened, particularly in the DACH region (Germany, Austria, Switzerland).

- COVID-19 has created supply chain disruptions and has significantly impacted energy production during the lockdowns. However, the impact has been short-term.

- Along with additional expenses, valve replacement adds up. Equipment needs to be taken apart and then put back together. The personnel and materials required to manage valve inventory control have a cost. Additionally, there can be a fee for the environmental damage caused by the disposal of old valves. All of this is on top of the additional costs for customers caused by employee overtime and the revenue lost due to the facility having to shut down, even momentarily. This acts as a restraint on the market.

Power Sector in Valves Market Trends

Growing Power Sector is Expected to Cater the Market Growth

- A different set of flow control requirements are needed for each kind of power generation application. That so, a power plant's particular pipeline system may contain a wide variety of valves. Industrial valves for power plants also need to play diverse roles depending on the operations occurring in a specific area of the pipe system.

- Moreover, due to the diversity of renewable energy plants, different valves are needed for different processes, such as low temperature, low-pressure raw material at one end of the process and high temperature, high-pressure steam at the other. It's not unusual for these plants to use various valve types to carry out particular activities, depending on the exact duties involved.

- In nuclear power plants, control valves are frequently employed to control fluid flux, and the principal circuit of one nuclear power plant contains more than 1500 control valves. They enable the flux to be directed to a precise amount of steam or water, ensuring the nuclear power plant's energy efficiency. Nuclear power reactors generate around 10% of the world's electricity. A total of 55 more reactors, or roughly 15% of the current capacity, are now being built.

- Further, the growing government aid in developing nuclear power plants is set to boost the market growth rate. For instance, in November 2021, the US government announced The Bipartisan Infrastructure Law that includes over USD 62 billion for the US Department of Energy (DOE) to assist in the country's transition to a clean energy economy, which provides for utilizing nuclear energy, the country's greatest single source of clean power. The law includes around USD 2.5 billion to enable the demonstration of two advanced American reactors by 2028 and USD 6 billion to launch a Civil Nuclear Credit program.

North America is Analyzed to Major Share in the Market

- North America is expected to hold the major share in the market owing to the significant presence of the power generation plants. Moreover, The United States has the most operational nuclear reactors. The 92 operating nuclear reactors in the USA have a net combined capacity of 94.7 GWe. With a total net capacity of 13.6 GWe, Canada has 19 nuclear reactors that are currently in operation. Nuclear power plants produced 14.6% and 19.7% of the nation's electricity in 2020 in the US and Canada, respectively (Source: World Nuclear Association).

- Further, the growing collaborations in integrating advanced technologies in the valves in power generation are analyzed to boost the market growth rate during the forecast period. For instance, in May 2021, The Nuclear Division of Curtiss-Wright stated that it had reached a contract with Exelon Generation Company LLC to license the firm's valve program performance data. Curtiss-Wright will use the performance data in collaboration with Exelon Generation to improve the efficiency of its StressWave ultrasonic leak detection technology and encourage the adoption of best practices in valve assessment, analysis, and performance throughout the U.S. nuclear fleet and the power generation sector.

- Asia-Pacific is analyzed to grow at a significant rate during the forecast period. The significant demand from the power sector is a driving factor for the market. For instance, in 2021, China generated 8.11 trillion kilowatt-hours (KWh), an increase of 8.1 percent from the previous year. Power generation in 2021 increased by 11% from 2019, making the average rise over the last two years 5.4%. In December, China's wind, solar, and nuclear energy production increased year over year by 30.1%, 18.8%, and 5.7%, respectively (Source: National Bureau of Statistics (NBS)).

- Moreover, the growing product innovations to meet the demand in the power generation sector further contribute to the market's need. In May 2022, The ARMATURY Group announced that the company had manufactured three butterfly valves with DNs ranging from 1,800 to 2,000 for the Philippine hydroelectric power facility. As shut-off valves, butterfly valves L32.71 PN 10 and PN 6 will completely open or close the passage of the working medium through the pipeline.

Power Sector in Valves Industry Overview

The Global Valves Market in Power Industry is fragmented and is analyzed to be highly competitive. The companies are leveraging strategic collaborative initiatives to increase market share and profitability. Manufacturers should be able to improve their product ranges and get a larger market share through mergers and acquisitions. Major firms include Emerson Electric Co., Schlumberger Limited, Alfa Laval Corporate AB, Flowserve Corporation, and Crane Co., among others.

- December 2021- Severn Group, a multinational company of dedicated high-end valve engineering and manufacturing companies that includes Severn and LB Bentley, has acquired ValvTechnologies, a pioneer in the design and manufacture of metal-seated, zero-leakage isolation valve products for demanding applications. The agreement is a milestone toward Severn Group's goal of being the leading global expert in severe service valves for the industrial and energy industries. Along with Severn and LB Bentley, ValvTechnologies will remain operationally independent while gaining access to a larger pool of resources and knowledge as a larger group member.

- June 2021- Neles Corp has inked an asset acquisition agreement to buy Flowrox's valve and pump operations. The companies develop and produce valve and pump solutions for the mining, minerals processing, metallurgy, construction, energy, environmental, and chemical industries. These solutions include pinch valves, knife gate valves, and peristatic pumps.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Force Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Assessment of the Impact of COVID -19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Power Sector in the Global Economy

- 5.1.2 Adoption of Smart Valves in the Power Industry

- 5.2 Market Restraints

- 5.2.1 Lack of Standardized Policies and High Replacement Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Ball

- 6.1.2 Butterfly

- 6.1.3 Gate/Globe/Check

- 6.1.4 Plug

- 6.1.5 Control

- 6.1.6 Other Types

- 6.2 Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Emerson Electric Co.

- 7.1.2 Schlumberger Limited

- 7.1.3 Alfa Laval Corporate AB

- 7.1.4 Flowserve Corporation

- 7.1.5 Crane Co.

- 7.1.6 Baker Hughes

- 7.1.7 Valmet Oyj

- 7.1.8 KITZ Corporation

- 7.1.9 IMI Critical Engineering

- 7.1.10 L&T Valves Limited