|

시장보고서

상품코드

1635378

다단 원심 펌프 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Multi-Stage Centrifugal Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

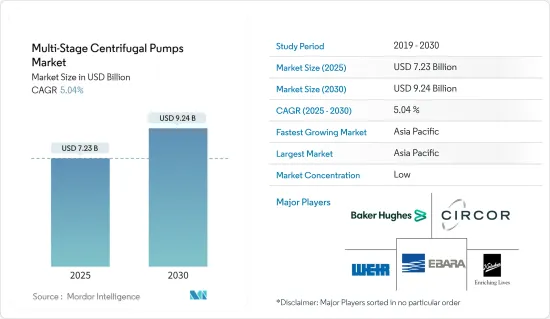

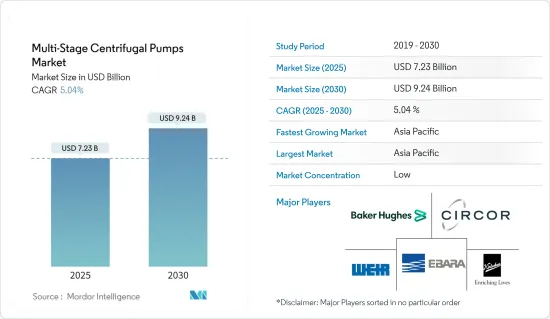

다단 원심 펌프 시장 규모는 2025년에 72억 3,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.04%로, 2030년에는 92억 4,000만 달러에 달할 것으로 예측됩니다.

수처리 프로젝트에 대한 투자, 석유 및 가스 산업의 확장, 에너지 효율적이고 강력한 다단 원심 펌프의 가용성이 예측 기간 중 시장 성장을 가속하고 있습니다.

산업 현장의 유체 이송에 다단 원심 펌프의 사용이 시장 성장을 주도하고 있습니다.

주요 하이라이트

- 다단 원심 펌프는 운동 에너지를 액체 수두로 변환하는 회전 장비입니다. 이 펌프는 정유공장, 석유 생산 플랫폼, 석유화학 플랜트, 발전소 및 기타 시설에서 응용되고 있습니다. 이 외에도 농업, 식품 가공, 주택 건설, 상수도 등에도 사용되고 있습니다.

- 여러 개의 임펠러가 있는 다단 원심 펌프는 수압을 순차적으로 증가시켜 동일한 크기의 단일 임펠러 펌프보다 더 높은 압력을 달성합니다. 또한 임펠러의 직경이 작고 간격이 좁기 때문에 이러한 펌프에 필요한 모터 마력이 줄어들어 성능과 효율성이 모두 향상됩니다. 펌프의 스테이지 수를 늘리면 최종 토출 압력이 높아집니다. 단계를 추가하면 이러한 펌프는 점차적으로 더 높은 압력을 달성 할 수 있지만 유량은 특정 분당 회전 수(RPM)에서 일정하게 유지됩니다. 이러한 장점은 다단 원심 펌프 시장의 성장을 가속하고 있습니다.

세계 수처리 및 폐수 관리의 새로운 동향이 시장에 성장 기회를 가져다 줄 것입니다.

주요 하이라이트

- 수처리 공장은 지역 사회가 깨끗하고 안전한 식수를 확보하는 데 있으며, 매우 중요합니다. 처리 단계를 통해 물을 이송하는 펌프와 펌프 시스템은 이러한 작업에서 핵심적인 역할을 합니다. 다단 펌프(다단 원심 펌프)는 수처리의 까다로운 요구사항에 맞는 효율적이고 신뢰할 수 있는 솔루션을 제공합니다.

- 다단 펌프는 고층 건물 및 역삼투압(RO) 시스템 급수부터 보일러 급수, 분무, 고압 세척 및 기타 수돗물 공급에 이르기까지 다양한 용도에 사용됩니다. 이러한 다용도성은 전 세계 수처리 플랜트 시장의 확대와 함께 시장 성장을 촉진하고 있습니다.

제품의 높은 초기 비용과 위조 위험은 시장의 주요 과제입니다.

주요 하이라이트

- 다단 원심 펌프는 초기 비용이 높다는 뚜렷한 단점이 있습니다. 복잡한 설계와 정밀한 엔지니어링이 필요하므로 이러한 펌프는 단일 단계 펌프보다 더 비쌉니다. 그러나 투자를 평가할 때 사용자는 이러한 초기 비용과 장기적인 운영상의 이점과 에너지 절감 효과를 비교하여야 합니다.

- 또한 비용 상승은 세분화된 시장을 압박하고 있으며, 시장 공급업체가 현지 생산품 및 수입 모조품과 경쟁하기 어렵게 만들고 있습니다. 따라서 소비자는 구매시 항상 경각심을 가지고 제품의 수명주기 비용의 중요성을 파악해야 합니다. 소비자는 초기 비용에만 집중하는 것이 아니라 제품수명주기 전반에 걸쳐 비용을 평가해야 합니다.

COVID-19 이후 재생에너지 프로젝트가 급증하고, 특히 집광형 태양광발전(CSP), 지열 발전소 등의 용도에서 다단 원심 펌프의 사용이 증가함에 따라 시장에 활로가 열리고 있으며, CSP 플랜트에서는 태양광을 집광하여 유체를 극한의 온도로 가열합니다. 극한의 온도까지 가열합니다. 그런 다음 다단 원심 펌프는 이 가열된 이송 유체를 열교환기를 통해 순환시켜 과열된 증기를 생성합니다. 이 증기가 터빈의 동력이 되어 시장의 성장 잠재력을 지원합니다.

다단 원심 펌프 시장 동향

석유 및 가스 산업이 가장 큰 최종사용자

- 다단 원심 펌프는 고압으로 유체를 이송하는 능력으로 유명하며 다양한 산업 분야에서 광범위하게 사용되고 있습니다. 특히 석유 및 가스 산업은 이 기술의 주요 채택자 중 하나입니다. 이 펌프는 일체형 케이스에 직렬로 쌓인 임펠러로 정의되며, 높은 토출 압력을 제공하는 데 탁월합니다. 이러한 특성은 석유 및 가스 파이프라인 운송 및 고압 주입 공정과 같은 승압 용도에 이상적입니다. 석유 및 가스 생산 활동에 대한 투자가 급증함에 따라 시장은 크게 성장할 준비가 되어 있습니다.

- 다단 원심 펌프는 액화 가스의 생산, 운송, 저장 및 유통에서 매우 중요합니다. 액화 가스는 기체 상태보다 더 쉽게 운송 및 저장할 수 있습니다. 이 액화 과정은 압축 또는 냉각을 통해 이루어집니다. 수요가 있을 때, 액화 가스는 압력을 해제하고 다시 기체화하여 펌프를 통해 소비 장비로 보내집니다. 또한 세계 여러 국가에서 액화 가스에 대한 수요가 증가하고 생산에 대한 투자가 증가함에 따라 시장 기회가 확대될 것으로 예상됩니다.

- 석유 및 가스 탐사 활동의 활성화와 생산 부문에 대한 투자 증가는 시장 성장을 가속할 것이며, 2023년 세계 석유 생산량은 2022년 9,420만 배럴에서 증가한 9,640만 배럴로 사상 최고치를 기록할 것으로 예상됩니다.

- 또한 IEA는 2023년 세계 석유 및 가스 업스트림 투자 규모가 11% 증가하여 전년도 4,740억 달러에서 5,280억 달러에 달할 것이라고 밝혔습니다. 예측에 따르면 2030년까지 총 공급 능력은 하루 1억 1,400만 배럴에 육박할 것으로 보입니다. 이러한 신흥 국가 시장 개척과 여러 지역의 탐사 투자 증가를 감안할 때, 시장은 큰 비즈니스 기회의 문턱에 서 있습니다.

- 또한 Baker Hughes Company에 따르면 북미는 석유 및 가스 시추기 보유량에서 세계를 선도하고 있으며, 2024년 8월 현재 이 지역에는 781개의 육상 시추기가 있고, 23개의 해상 시추기가 더 있으며, 2023년 세계 석유 시추기 수는 평균 1,800개를 돌파할 것으로 예상했습니다. 돌파했습니다.

- 여러 회사가 액화 가스의 생산, 운송, 저장 및 유통에 필수적인 액화 가스 펌프를 생산하고 있습니다. 이 펌프는 다양한 용도로 효과적인 가스 운송을 보장하기 위해 다양한 기능으로 설계되어 있습니다. 낮은 NPSH(순흡입 양정) 값 덕분에 이 펌프는 캐비테이션 없이 작동하며, 흡입 모드와 흡입 모드 모두에서 완벽한 이송을 유지합니다.IEA에 따르면 세계 가스 시장은 세계가 심각한 에너지 위기에서 점차 회복하면서 수요 및 공급 모두에 영향을 미치면서 변화하고 있습니다. 이러한 역학은 이 부문의 성장을 가속할 태세를 갖추고 있습니다.

- IEA에 따르면 2024년 세계 가스 수요는 2.5% 증가하여 1,000억 입방미터(bcm) 증가할 것으로 예상되며, 2023년의 따뜻한 기온과 달리 2024년에는 더 추운 겨울이 예상되어 주거 및 상업 부문 모두 난방 수요가 증가할 것으로 예상됩니다. 증가할 것으로 예상됩니다. 에너지 연구소의 데이터에 따르면 2023년 세계 액화천연가스 교역량은 5,490억 입방미터에 달할 것이며, 1970-2023년 이 수치는 5,460억 입방미터로 크게 증가할 것으로 예상됩니다. 또한 2023년에는 미국이 세계 최고의 LNG 수출국으로 부상할 것으로 예상됩니다.

아시아태평양이 큰 시장 점유율을 차지할 것으로 예상

- 급격한 도시화, 산업 발전, 인구 증가, 물 부족에 대한 우려가 높아지면서 아시아태평양의 상하수도 처리에 대한 투자 확대가 가속화되고 있습니다.

- 2024년 6월, 베올리아의 자회사이자 유명한 수처리 기술 서비스 기업인 베올리아 워터 테크놀러지스(Veolia Water Technologies)는 중국 최초의 이온 교환 재생 시설을 가동했습니다. 최첨단 기술을 갖춘 이 시설은 사용한 이온교환수지를 효율적으로 재활용하여 자원 최적화와 지속가능성에 대한 베올리아의 약속을 명확히 보여줍니다.

- 2024년 1월, 싱가포르 코스탈 그룹 산하 코스탈 에코 인더스트리(Koastal Eco Industries)는 베트남 남부 타이닌성에 폐수 처리 공장을 설치하기 위해 430만 달러 규모의 EPC(설계, 조달, 건설) 계약을 체결하였습니다. 이 시설은 하루 15,000 입방미터의 처리 용량을 자랑하며, TTC Group Joint Stock Company(JSC) 복합 기업 및 그 이름의 회사 프로젝트인 Thanh Thinh Thanh Cong 산업단지에서 나오는 모든 폐수를 처리할 것입니다.

- 또한 2024년 9월에는 호주를 대표하는 에너지 음료 브랜드인 V-에너지가 퀸즐랜드 입스위치(Queensland Ipswich)에 신설된 산토리 오세아니아의 멀티 음료 제조 시설에서 처음으로 생산될 예정이며, 2025년 중반에 완공될 예정입니다. 헥타르에 달하는 이 광활한 부지는 탄소 중립적이며, 40개 이상의 산토리 브랜드를 포함한 다양한 포트폴리오의 제조 및 유통의 중심 기지로서 역할을 할 준비가 되어 있습니다.

- 2024년 5월, Aurobindo Pharma의 자회사 TheraNym Biologics Pvt Ltd는 Merck Sharp &Dohme Singapore와 생물제제 위탁 생산 전문 마스터 서비스 계약을 체결하였습니다. 이 계약은 2024년 5월부터 유효하며, TheraNym은 국내외 시장용 생물제제를 생산할 수 있습니다. 또한 TheraNym은 인도 텔랑가나 주에 100억 루피를 투자하여 생물제제 제조 시설을 설립할 예정입니다.

- 2024년 10월, 구글은 태국에 데이터센터를 건설하기 위해 10억 달러를 투자할 것이라고 발표했습니다. 이 발표는 같은 주에 말레이시아에 소버린 클라우드 서비스를 제공하는 구글 클라우드의 다년 계약에 이어 이루어졌습니다. 또한 2024년 5월, 구글은 이미 SEA에 20억 달러를 투자하여 데이터센터를 설립하는 등 이미 큰 움직임을 보이고 있습니다. 수처리, 건설, 화학, 식품 및 음료 부문에서의 이러한 발전은 다단 원심 펌프 시장의 성장을 가속할 것으로 예상됩니다.

다단식 원심 펌프 산업 개요

다단 원심 펌프 시장은 여러 세계 및 지역적 기업이 치열한 경쟁을 벌이고 있는 시장입니다. 신규 진입 장벽이 높은 시장이지만, 여러 신규 시장 진출기업이 시장을 주도하고 있습니다.

Kirloskar Brothers Limited, Baker Hughes Company, Xylem Inc.와 같은 시장 리더들은 이미 구축된 판매망을 통해 시장 전체에 큰 영향력을 행사하고 있습니다.

대형 벤더와 관련된 브랜드 ID 확인은 세계 시장에서 다양한 제품 제공의 대명사가 되었습니다. 이들 기업은 시장 확대와 인수에 집중하면서 사업 규모를 지속적으로 확장하고 있습니다. 또한 시장의 많은 공급업체들은 미개척 영역을 개척하고 지속가능한 파트너십을 형성하기 위해 연구개발에 집중하고 있습니다. 지역적 확장 전략도 마찬가지입니다.

시장 성장을 지원하는 것은 에너지 효율이 높고 신뢰성이 높으며 작동 생산성이 높은 다단 원심 펌프의 개발로 인해 시장공급측 경쟁이 심화되고 있습니다. 전반적으로 조사 대상 시장공급업체 간 경쟁 업체 간의 적대적 관계는 높으며, 이는 예측 기간 중 변하지 않을 것으로 예상됩니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 산업 밸류체인 분석

- COVID-19의 부작용과 기타 거시경제 요인이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 신흥 국가에서 상하수도 관리에 대한 높은 수요

- 제품을 효율적으로 운영하기 위한 혁신적 기술의 통합 증가

- 시장이 해결해야 할 과제

- 그레이마켓 참여 기업 및 미조직 부문과의 경쟁 격화

제6장 시장 세분화

- 유형별

- 횡형 펌프

- 종형 펌프

- 최종사용자 산업별

- 석유 및 가스

- 화학

- 식품 및 음료

- 상하수도

- 제약

- 발전

- 금속·광업

- 기타

- 지역별

- 북미

- 유럽

- 아시아

- 호주·뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 개요

- Kirloskar Brothers Limited

- Baker Hughes Company

- Circor International Inc.

- Ebara Corporation

- The Weir Group

- Grundfos Holding

- Pentair Inc.

- Sulzer Ltd

- Tsurumi Manufacturing Co. Ltd

- Wilo SE

- Xylem Inc.

- KSB SE & Co. KgaA

제8장 투자 분석

제9장 시장의 미래

KSA 25.01.31The Multi-Stage Centrifugal Pumps Market size is estimated at USD 7.23 billion in 2025, and is expected to reach USD 9.24 billion by 2030, at a CAGR of 5.04% during the forecast period (2025-2030).

Investments in water treatment projects, expansion of the oil and gas industries, and the availability of highly energy-efficient and powerful multi-stage centrifugal pumps are driving market growth during the forecast period.

The Usage Of Multi-stage Centrifugal Pumps In Transporting Fluids At Industrial Sites Is Driving The Market Growth

Key Highlights

- A multi-stage centrifugal pump is a rotating device that transforms kinetic energy into a liquid head. These pumps find applications in facilities like refineries, oil production platforms, petrochemical plants, and power plants. Beyond these, they're also utilized in agriculture, food processing, residential construction, and water supply.

- Equipped with multiple impellers, multi-stage centrifugal pumps elevate water pressure sequentially, achieving higher pressures than their single impeller counterparts of the same size. Furthermore, with smaller impeller diameters and tighter clearances, these pumps demand less motor horsepower, enhancing both performance and efficiency. More stages in a pump result in a higher final discharge pressure. While adding stages allows these pumps to achieve progressively higher pressures, the flow rate remains constant at a specific revolutions per minute (RPM). This advantage is propelling the growth of the multi-stage centrifugal pump market.

The Emerging Trend Of Water Treatment And Wastewater Management Worldwide Creates A Growth Opportunity For The Market

Key Highlights

- Water treatment plants are pivotal in ensuring communities access clean and safe drinking water. The pumps and pumping systems transporting water through the treatment stages are central to these operations. Multi-stage pumps, or multi-stage centrifugal pumps, provide efficient and reliable solutions tailored to the rigorous demands of water treatment.

- Multi-stage pumps find diverse applications, from supplying water to high-rise buildings and reverse osmosis (RO) systems to feeding boilers, spraying, high-pressure cleaning, and other waterworks. This versatility bolsters the market's growth, paralleling the global expansion of water treatment plants.

Initial High Cost Of The Product And The Risk Of Counterfeiting Are The Major Challenges In The Market

Key Highlights

- Multi-stage centrifugal pumps have a notable drawback with their higher initial cost. Due to their intricate design and the demand for precision engineering, these pumps are more expensive than their single-stage counterparts. However, when evaluating the investment, users must weigh the long-term operational advantages and energy savings that can counterbalance this upfront expense.

- Moreover, increasing costs are putting pressure on the fragmented market, making it difficult for the market vendors to compete with locally produced and imported counterfeit products. Consequently, consumers must remain vigilant about their purchases and grasp the significance of the product-life-cycle cost. Consumers must evaluate expenses throughout a product's life cycle rather than concentrating solely on the upfront cost.

Post-COVID-19, the surge in renewable energy projects has opened avenues for the market, particularly with the rising use of multi-stage centrifugal pumps in applications like concentrated solar power (CSP) and geothermal plants. In CSP plants, sunlight is concentrated to heat a fluid to extreme temperatures. Multi-stage centrifugal pumps then circulate this heated transfer fluid through heat exchangers, generating superheated steam. This steam powers turbines, underscoring the market's growth potential.

Multi-Stage Centrifugal Pumps Market Trends

Oil and Gas Industry to be the Largest End User

- Multistage-centrifugal pumps, known for their capability to transfer fluids at elevated pressures, find extensive use across various industrial sectors. Notably, the Oil and Gas industry stands out as a primary adopter of this technology. Defined by their series-stacked impellers within a unified casing, these pumps excel in delivering heightened discharge pressures. This attribute renders them ideal for boosting applications, including the pipeline transportation of oil and gas and high-pressure injection processes. As investments in oil and gas production activities surge, the market is poised for significant growth.

- Multistage-centrifugal pumps are crucial during the production, transport, storage, and distribution of liquefied gases. Liquefied gases can be transported and stored more easily than in their gaseous state. This liquefaction process is achieved through compression or cooling. When there's demand, the liquefied gas is regasified by releasing pressure and then delivered to consuming units using pumps. Moreover, the increasing demand for liquefied gases across various countries in the world and increased investments in production will enhance the market opportunities.

- Heightened oil and gas exploration activities, coupled with escalating investments in production fields, are set to propel the market's growth. In 2023, global oil production achieved a record high of 96.4 million barrels per day, marking an increase from 94.2 million barrels per day in 2022.

- Furthermore, the IEA highlighted a notable 11% rise in global upstream oil and gas investments for 2023, amounting to a substantial USD 528 billion, a jump from the previous year's USD 474 billion. Projections indicate that total supply capacity could be near 114 million barrels a day by 2030. Given these significant developments and the rise in exploration investments across multiple regions, the market stands on the brink of substantial opportunities.

- Further, according to Baker Hughes, North America leads the world in hosting oil and gas rigs. As of August 2024, the region boasted 781 land rigs and an additional 23 offshore rigs. In 2023, the global count of oil rigs surpassed 1,800 units on average.

- Several companies manufacture liquefied gas pumps, essential for the production, transport, storage, and distribution of liquefied gases. These pumps, designed with various features, ensure effective gas conveyance across these diverse applications. Thanks to their low NPSH (Net Positive Suction Head) values, these pumps operate without cavitation, maintaining full conveyance in both suction and intake modes. According to IEA, the global gas market is transitioning as the world slowly recovers from a significant energy crisis, impacting both supply and demand. Such dynamics are poised to fuel growth in this segment.

- According to IEA, in 2024, global gas demand is projected to rise by 2.5%, equating to an increase of 100 billion cubic meters (bcm). With a colder winter anticipated in 2024, contrasting the mild temperatures of 2023, there's an expected uptick in demand for space heating across both residential and commercial sectors. Data from the Energy Institute reveals that in 2023, the global trade volume for liquefied natural gas reached 549 billion cubic meters. Notably, from 1970 to 2023, this figure saw a substantial increase of 546 billion cubic meters. Furthermore, in 2023, the United States emerged as the dominant player, being the world's leading LNG exporting nation.

Asia Pacific is Expected to Hold Significant Market Share

- Rapid urbanization, industrial growth, a rising population, and heightened concerns about water scarcity are fueling the expansion of investments in water and wastewater treatment across the Asia-Pacific region.

- In June 2024, Veolia Water Technologies, a subsidiary of Veolia and a prominent player in water treatment technologies and services, inaugurated its inaugural ion exchange regeneration facility in China. Equipped with cutting-edge technology, the facility efficiently recycles spent ion exchange resins, underscoring Veolia's commitment to resource optimization and sustainability.

- In January 2024, Koastal Eco Industries Co., Ltd., part of Singapore's Koastal Group, inked a USD 4.3-million EPC (engineering, procurement, and construction) contract to establish a wastewater treatment plant in Tay Ninh, a southern province of Vietnam. This facility, boasting a daily capacity of 15,000 cubic meters, will handle all wastewater from the Thanh Thanh Cong Industrial Zone, a project of the TTC Group Joint Stock Company (JSC) conglomerate and its namesake company.

- Additionally, in September 2024, V Energy, Australia's leading energy drink brand, became the inaugural beverage produced at Suntory Oceania's newly established multi-beverage manufacturing facility in Ipswich, Queensland. Set to be fully operational by mid-2025, this expansive 17-hectare site, boasting carbon neutrality, is poised to serve as the central manufacturing and distribution hub for Suntory's diverse portfolio, encompassing over 40 brands.

- In May 2024, Aurobindo Pharma's subsidiary, TheraNym Biologics Pvt Ltd, inked a master service agreement with Merck Sharp & Dohme Singapore, focusing on the contract manufacturing of biologicals. This agreement, effective from May 2024, empowers TheraNym to manufacture biologicals for both domestic and international markets. Additionally, TheraNym is set to invest INR 1,000 crore in establishing a biologics manufacturing facility in Telangana, India.

- In October 2024, Google unveiled a USD 1 billion investment for building a data center in Thailand, aiming to address the surging demands for cloud storage and AI tools in Southeast Asia (SEA). This announcement followed closely on the heels of Google Cloud's multi-year agreement to deliver sovereign cloud services to Malaysia, made in the same week. Additionally, in May 2024, Google had already made a significant move into SEA with a USD 2 billion investment for another data center. Such developments in water treatment, construction, chemicals, and food and beverage sectors are expected to drive growth in the multi-stage centrifugal pumps market.

Multi-Stage Centrifugal Pumps Industry Overview

The multi-stage centrifugal pump market comprises several global and regional players vying for attention in a contested space. Although the market studied poses high barriers to entry for new players, several new entrants have gained traction.

Market leaders, such as Kirloskar Brothers Limited, Baker Hughes Company, Xylem Inc., and others, have a considerable influence on the overall market, with access to well-established distribution networks.

The brand identity associated with the major vendors has become synonymous with various product offerings in the global market. These firms have continuously expanded their operational scales by focusing on market expansions and acquisitions. Furthermore, many vendors in the market are dedicating their R&D efforts to capturing unexplored domains and forming partnerships for sustainability. The same is true for geographic expansion strategies.

Market growth is supported by the development of highly energy-efficient, reliable, and operationally productive multi-stage centrifugal pumps, which increase competition in the market's supply side. Overall, the intensity of competitive rivalry among the vendors in the market studied is expected to be high and remain the same over the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Demand for Water and Wastewater Management in Developed Countries

- 5.1.2 Growing Integration of Innovative Technologies to Efficiently Operate Product

- 5.2 Market Challenges

- 5.2.1 Increased Competition from Grey Market Players and Unorganized Sector

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Horizontal Pumps

- 6.1.2 Vertical Pumps

- 6.2 By End-User Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemicals

- 6.2.3 Food and Beverage

- 6.2.4 Water and Wastewater

- 6.2.5 Pharmaceutical

- 6.2.6 Power Generation

- 6.2.7 Metal and Mining

- 6.2.8 Other End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Kirloskar Brothers Limited

- 7.1.2 Baker Hughes Company

- 7.1.3 Circor International Inc.

- 7.1.4 Ebara Corporation

- 7.1.5 The Weir Group

- 7.1.6 Grundfos Holding

- 7.1.7 Pentair Inc.

- 7.1.8 Sulzer Ltd

- 7.1.9 Tsurumi Manufacturing Co. Ltd

- 7.1.10 Wilo SE

- 7.1.11 Xylem Inc.

- 7.1.12 KSB SE & Co. KgaA