|

시장보고서

상품코드

1635459

유럽의 납축배터리 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Lead-acid Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

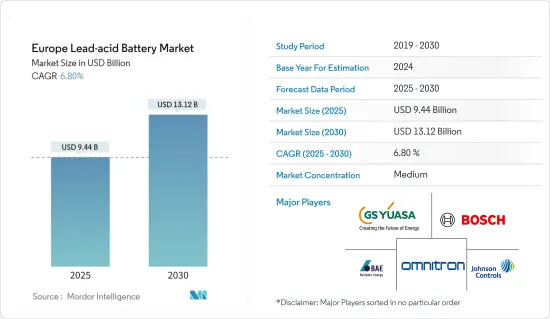

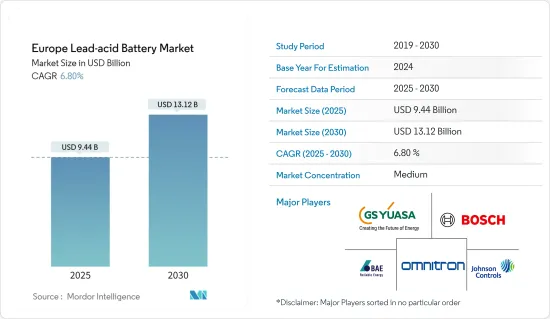

유럽의 납축배터리 시장 규모는 2025년 94억 4,000만 달러로 추정되며, 2030년에는 131억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 6.8%의 CAGR을 기록할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 자동차 부문의 성장과 배터리 에너지 저장 시스템(BESS) 채택 등의 요인이 예측 기간 동안 유럽 납축배터리 시장을 견인할 것으로 예상됩니다.

- 반면, 리튬이온 배터리의 채택 증가와 전기자동차 판매 증가는 향후 몇 년간 납축배터리 시장의 성장을 억제할 가능성이 높습니다.

- 그럼에도 불구하고, 오프그리드 태양광발전 설비 투자의 증가는 유럽 납축배터리 시장에 큰 비즈니스 기회를 가져다 줄 것으로 추정됩니다.

- 독일은 자동차 제조업체의 존재감이 높기 때문에 유럽 납축배터리 시장을 독점할 가능성이 높습니다.

유럽의 납축배터리 시장 동향

SLI 배터리 부문 시장을 장악하고 있는 SLI 배터리 부문

- 시동, 조명, 점화(SLI) 배터리는 지난 100년 동안 거의 모든 자동차에 장착되어 왔습니다. 일반적으로 SLI 배터리는 자동차 엔진 시동이나 가벼운 전기 부하를 실행하는 등 짧은 시간 동안 전력을 공급하는 데 사용됩니다.

- SLI 배터리는 자동차 용으로 설계되었기 때문에 항상 자동차 충전 시스템과 함께 장착되어 자동차를 사용할 때 항상 배터리에 충전과 방전의 연속적인 사이클이 있습니다. 12 볼트 배터리는 50 년 이상 가장 일반적으로 사용되어 왔지만, 평균 전압은 14 볼트에 가깝습니다. 평균 전압은 14볼트에 가깝다.

- 또한, 통신 산업은 전화 및 인터넷 서비스 전송을 위해 주로 정교한 휴대폰 타워 및 현장 시설의 정교한 네트워크에 의존하고 있습니다. 효율적인 운영을 위해 이러한 타워와 현장 시설은 일정하고 안정적인 전력 공급이 필요합니다. 일반적으로 전력망에서 공급되는 전력은 유선 네트워크의 경우 -48V, 무선 네트워크의 경우 24V의 직류(DC) 전력으로 변환됩니다. 통신 산업에서 사용되는 배터리에는 VRLA, NiCd, Li-ion 등이 있습니다.

- 최근 몇 년 동안 SLI 배터리는 유럽 지역의 자동차 부문 OEM 및 애프터마켓의 수요 증가로 인해 큰 수요를 보이고 있습니다. 이 배터리는 주로 시동 모터, 조명, 점화 시스템 및 기타 내연 기관의 전원으로 사용되며, 고성능, 긴 수명 및 비용 효율성을 보장합니다.

- 또한 2022년에는 독일, 프랑스, 영국이 승용차 판매의 주요 국가입니다. 독일의 승용차 판매량은 약 265만대, 프랑스는 약 160만대, 영국은 약 160만대입니다.

- 또한, EU 전체에서 2022년 신차 판매량은 약 930만대로 전년 대비 4.6% 감소할 것으로 예상됩니다. 그러나 오래된 자동차의 오래된 SLI 배터리 교체가 시장을 견인할 것으로 예상됩니다.

- 이상의 내용을 종합해 볼 때, SLI 배터리 부문은 예측 기간 동안 유럽 납축배터리 시장을 독식할 것으로 예상됩니다.

시장을 독점하고 있는 독일

- 독일은 세계 최대의 승용차 및 상용차 생산국 중 하나입니다. 수십 년 동안 자동차 산업은 독일 경제의 주요 부문입니다.

- 또한 모든 주요 자동차 제조업체가 독일에 진출하여 독일은 자동차 산업의 혁신 허브로서 세계적으로 인정받고 있으며, 2022년 독일은 유럽 제1의 자동차 시장으로 승용차 생산량의 약 26%, 신차 등록대수의 약 20%를 차지할 것으로 예상됩니다.

- 또한 2022년 6월 독일은 EU가 2035년까지 EU 지역에서 ICE 차량 신차를 금지하는 것에 반대하는 목소리를 냈으며, ICE 차량은 폭스바겐, BMW, 메르세데스 등 독일 대기업이 생산하는 자동차 재고의 상당 부분을 차지하고 있습니다. 또한 독일의 승용차 판매량은 2022년 약 265만 대에 달할 것으로 예상됩니다.

- 독일은 세계적으로도 고도로 발전된 시장으로 여겨지고 있으며, 유럽연합(EU)의 금융 강국이기도 합니다. 따라서 데이터센터의 수도 많으며, 2023년 말 기준 국내에는 522개 이상의 데이터센터가 운영되고 있습니다. 또한, 자동화와 5G 네트워크의 발달로 인해 데이터센터의 수요는 독일에 있습니다.

- 독일에서는 자동차, 데이터센터, 통신 산업에 대한 투자 증가로 인해 납축배터리에 대한 수요가 증가하고 있습니다. 리튬이온 배터리와 같은 대체품도 존재하지만, 납축배터리의 수요는 이 모든 산업에서 여전히 많습니다. 납축배터리는 수명이 길고 안전성이 높으며 장기적으로도 성능이 우수하기 때문에 데이터센터, 자동차, 통신 산업에서 가장 먼저 선택되고 있습니다.

- 이와 같이 독일의 자동차 및 데이터센터 산업의 이러한 모든 발전은 예측 기간 동안 납축배터리 시장을 견인할 것으로 보입니다.

유럽의 납축배터리 산업 개요

유럽 납축배터리 시장은 반분절화되어 있습니다. 이 시장의 주요 기업으로는 BAE Batterien GmbH, Exide Technologies Inc, GS Yuasa Corporation, Johnson Controls International PLC, Omnitron Griese GmbH 등이 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부 규제와 정책

- 시장 역학

- 성장 촉진요인

- 자동차 판매 증가

- 배터리 에너지 저장 시스템(BESS) 채용 확대

- 성장 억제요인

- 리튬이온 배터리 중시 상승

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 용도별

- SLI(시동, 점등, 점화)용 배터리

- 고정형 배터리(통신, UPS, 에너지 저장 시스템(ESS) 등)

- 휴대용 배터리(가전제품 등)

- 기타 용도

- 기술별

- 침수형

- VRLA(밸브 제어 납축배터리)

- 지역별

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 북유럽

- 터키

- 러시아

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Johnson Controls International PLC

- Exide Technologies Inc.

- GS Yuasa Corporation

- Robert Bosch GmbH

- Omnitron Griese GmbH

- BAE Batterien GmbH

- Amara Raja Batteries Ltd

- Leoch International Technology Limited

- Panasonic Corporation

- Market Ranking/Share Analysis

제7장 시장 기회와 향후 동향

- 오프그리드 솔라 설치 투자 증가

The Europe Lead-acid Battery Market size is estimated at USD 9.44 billion in 2025, and is expected to reach USD 13.12 billion by 2030, at a CAGR of 6.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing automotive sector and adoption of battery energy storage systems (BESS) are expected to drive the lead-acid battery market in Europe during the forecast period.

- On the other note, rising adoption of lithium-ion batteries and increasing electric vehicle sales are likely to restrain the growth of the lead-acid battery market over the coming years.

- Nevertheless, increased off-grid solar installation investment is estimated to provide a significant opportunity for the lead acid market in Europe.

- Germany is likely to dominate the lead acid battery market in Europe due to the higher presence of automobile manufacturers in the country.

Europe Lead-acid Battery Market Trends

SLI Battery Segment to Dominate the Market

- Starting, lighting, and ignition (SLI) batteries have been in almost every car for the past 100 years. Generally, SLI batteries are used for short power bursts, such as starting a car engine or running light electrical loads.

- SLI batteries are designed for automobiles and, therefore, are always installed with the vehicle's charging system, which means that there is a continuous cycle of charge and discharge in the battery whenever the vehicle is in use. The 12-volt batteries have been the most commonly used for more than 50 years; however, their average voltage is close to 14-volt.

- Also, the telecom industry is primarily dependent on an elaborate network of mobile phone towers and field facilities for the transmission of phone calls and internet services. For their efficient operations, these towers and field facilities require a constant and highly reliable supply of electric power, usually from the electrical grid converted to direct current (DC) power at -48 volts for wired networks and +24 volts for wireless networks. The batteries used in the telecom industry include VRLA, NiCd, and Li-ion, among others.

- In the last couple of years, the SLI batteries witnessed significant demand due to the growing demand from OEMs and aftermarkets from the automotive sector in the European region. These batteries primarily mostly utilized power start motors, lights, ignition systems, or other internal combustion engines while ensuring high performance, long life, and cost-efficiency.

- Moreover, in 2022, Germany, France and United kingdom are the leading countries in terms of sales of passengers cars. Germany's passenger car sales amounted to around 2.65 million units. in fracne it was around 1.6 million and United kingdom is was around 1.6 million.

- Also, around 9.3 million new passenger cars were sold across the European Union in 2022, which is 4.6% less than the previous year. However, the replacement of the old SLI batteries in old vehicles is anticipated to drive the the market.

- Owing to the above points, SLI Battery Segement is expected to dominate Europe lead-acid battery market during the forecast period.

Germany to Dominate the Market

- Germany is one of the world's largest manufacturing countries for passenger and commercial vehicles. For several decades the automobile industry has been a key sector in the German economy.

- Moreover, Germany has been recognized worldwide as an Innovation hub for the automotive industry, as all major automobile manufacturers have a presence in the country. In 2022, Germany is Europe's number one automotive market, accounting for around 26% of all passenger cars manufactured and approximately 20% of all new car registrations.

- Also, In June 2022, Germany, raised its voice against the EU ban on new ICE vehicles in the region by 2035. The ICE vehicles form a considerable part of the vehicle stock manufactured by major players in Germany like Volkswagen, BMW, and Mercedes. Moreover, Germany's passenger car sales amounted to around 2.65 million units in 2022.

- Germany is considered a highly developed market in the world, and it is the financial powerhouse of the European Union. This, resulting a higher number of data centres, and as of the end of 2023, there were more than 522 active data centres in the country. Furthermore, due to automation and development meant of the 5G network, the demand for the data centre is in Germany.

- The demand for lead acid batteries is rising in Germany due to increased investment in the automobile, data centre and telecommunication industry. Though there is the presence of substitutes, such as lithium-ion batteries, there is still more demand for lead acid batteries from all these industries. The lead acid battery has a long life, safety and good performance in the long run, which makes them the first choices in the data centre, automobile and telecommunication industry.

- Thus all these development in Germany in the automobile and data centre industry is likely to drive the lead acid market during the forecast period.

Europe Lead-acid Battery Industry Overview

The Europe lead-acid battery market is semi fragmented. Some of the key players (in no particular order) in the market include BAE Batterien GmbH, Exide Technologies Inc., GS Yuasa Corporation, Johnson Controls International PLC, Omnitron Griese GmbH, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Sales of Automobiles

- 4.5.1.2 Growing Adoption of Battery Energy Storage Systems (BESS)

- 4.5.2 Restraints

- 4.5.2.1 Rising Emphasis on Lithium-Ion Batteries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 SLI (Starting, Lighting, Ignition) Batteries

- 5.1.2 Stationary Batteries (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.1.3 Portable Batteries (Consumer Electronics, etc.)

- 5.1.4 Other Applications

- 5.2 Technology

- 5.2.1 Flooded

- 5.2.2 VRLA (Valve Regulated Lead-acid)

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 NORDIC

- 5.3.7 Turkey

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Johnson Controls International PLC

- 6.3.2 Exide Technologies Inc.

- 6.3.3 GS Yuasa Corporation

- 6.3.4 Robert Bosch GmbH

- 6.3.5 Omnitron Griese GmbH

- 6.3.6 BAE Batterien GmbH

- 6.3.7 Amara Raja Batteries Ltd

- 6.3.8 Leoch International Technology Limited

- 6.3.9 Panasonic Corporation

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increased Off-Grid Solar Installation Investment