|

시장보고서

상품코드

1636083

인도의 제조업 시장 - 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)India Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

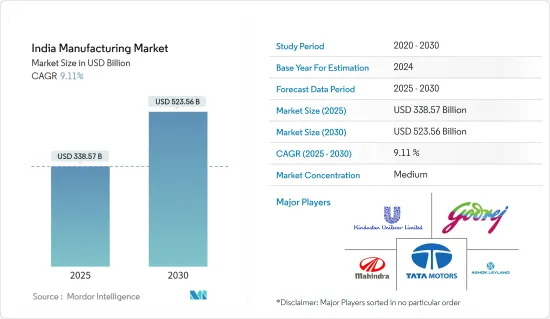

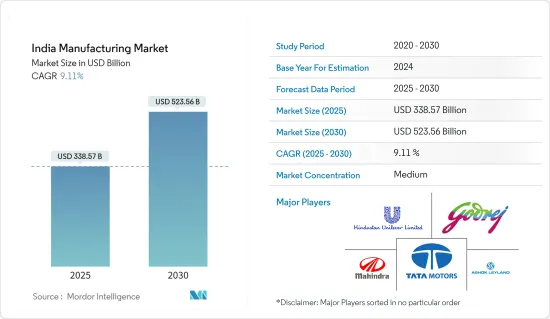

인도의 제조 시장 규모는 2025년에 3,385억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 9.11%로, 2030년에는 5,235억 6,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 인도의 제조업 시장은 유행기간에 다양한 단계를 거쳐 개척되어 GDP에 약 16-17% 기여해 국내 노동인구의 20% 가까이를 고용하고 있습니다. 외자에 매력적인 투자처가 되어, 다수의 휴대전화, 고급품, 자동차 브랜드가 국내에 제조 시설을 설립 또는 검토하고 있습니다. 물품 서비스세(GST)의 도입으로 인도는 GDP 2조 5,000억 달러, 인구 13억 2,000만 명의 단일 시장에 통합되어 투자자들의 큰 관심을 모으고 있습니다.

- 인도 휴대전화 전자기기협회(ICEA)에 따르면 인도는 전략적 시책 개입으로 노트북과 태블릿 단말의 누적 제조 능력을 2025년까지 1,000억 달러까지 끌어올릴 가능성이 있다고 합니다. 정부의 이니셔티브 중 중공업·공영기업성이 주도하는 SAMARTH Udyog Bharat 4.0은 특히 자본재 면에서 제조시장의 경쟁을 강화하는 것을 목적으로 하고 있습니다. 산업 회랑과 스마트 시티 개발에 주력하는 것은 전반적인 국가 발전을 촉진하는 정부의 헌신을 강조합니다.

- 인도는 2025년까지 GDP에서 차지하는 제조업의 비율을 25%로 하는 것을 목표로 한 국가 제조업 시책과 생산 연동 장려금(PLI) 제도 등의 노력을 통해 Industry 4.0을 향해 꾸준히 전진하고 있습니다. PLI 제도는 핵심 제조업을 세계 수준으로 끌어올리는 것을 목표로 하고 있습니다. 인도에서는 자동화된 공정 주도 제조업으로의 전환이 점차 진행되고 있어 효율성 향상과 생산 능력 강화가 기대되고 있습니다.

인도 제조업 시장 동향

정부지출 증가가 시장 성장을 뒷받침할 전망

제조업은 인도의 고성장 시장 중 하나로 부상하고 있습니다. 정부는 인도를 제조업의 허브로 지도에 올려 경제에 세계의 인지를 주기 위해 'Make in India' 프로그램을 시작했습니다. 예를 들어, Wistron Corp.는 인도의 Optiemus Electronics와 협력하여 랩톱 및 스마트폰과 같은 제품을 제조했으며, 'Make in India' 이니셔티브와 이 나라의 전자 장비 제조를 크게 뒷받침했습니다.

정부는 시장 성장을 위한 건전한 환경을 촉진하기 위해 몇 가지 이니셔티브를 취하고 있습니다. 연방 예산에서 정부는 240억 3,000만 루피(3억 1,500만 달러)를 전자와 IT 하드웨어 제조 촉진에 할당했습니다. 반도체 제조 PLI는 7,600억 루피(97억 1,000만 달러)로 설정되어 인도를 이 중요한 부품의 세계 주요 생산국 중 하나로 만드는 것을 목표로 하고 있습니다.

인도 제조 시장은 인구 증가를 배경으로 급속한 성장을 이루고 있습니다. 투자 증가와 'Make in India'와 같은 노력으로 이 나라는 세계의 제조 거점으로 자리매김하고 있습니다. 2023년도 제조업 시장의 연간 생산 성장률은 4.7%입니다.

제조업의 조부가가치는 꾸준히 증가하고 있지만, 서비스업에 비해 아직 늦어지고 있습니다. 기업이 이 지역에 제조시설을 설립 또는 설립 중입니다. 또한 Apple도 인도에서 사업을 시작하여 중국에서 생산의 다각화를 도모하고 있습니다.

영세·중소·중견기업(MSMEs)은 인도가 농업 중심 경제에서 공업화 경제로 이행하는 데 중요한 역할을 하고 있습니다. 경제 성장과 고용창출을 추진하는 MSME의 중요성이 부각되고 있습니다.

자동차산업의 성장이 시장을 견인

인도는 세계 최대의 트랙터 생산국, 세계 제2위의 버스 생산국, 세계 제3위의 대형 트럭 생산국이며, 세계의 대형차 시장에서 중요한 지위를 차지하고 있습니다. 생산 대수는 2,293만 대로 견조한 내수와 큰 수출 가능성을 보여줍니다.

2023년 11월의 승용차 총 판매 대수는 33만 4,130대로, 2022년 11월에 비해 3.7%의 미증이 되었습니다. 이 급증은 11월의 승용차 판매 대수로서는 최고를 기록했습니다. 2023년도의 인도의 자동차 수출 대수는 476만 1,487대가 되어, 세계의 자동차 시장에 있어서의 인도의 강한 존재감이 한층 더 나타났습니다.

이륜차는 인도에서 생산되는 주요 차종으로 국내에서 판매되는 자동차의 대부분을 차지합니다. 이 카테고리에는 이륜차, 스쿠터, 원동기가 포함됩니다. 스쿠터와 전동 이륜차이며 많은 선도적인 제조업체들이 전동 차량 생산에 나서고 있습니다.

예를 들어 2023년 1월 인도의 주요 자동차 기업인 Mahindra and Mahindra Ltd는 마하라슈트라 주 정부의 전기자동차 산업 진흥 계획 하에 전기자동차를 위한 1,000억 루피(12억 2,674만 달러)의 투자 승인 를 발표했습니다.

인도 제조업 개요

인도의 제조 시장은 세분화되어 있으며 세계 기업과 현지 기업이 혼재하고 있습니다. Godrej Group 등이 있습니다. 시장의 주요 기업은 보다 나은 제품과 서비스를 고객에게 제공하기 위해 주요 개발 전략으로 제품 출시, 제휴, 사업 확대, 인수를 채용하고 있습니다. 2022년 12월, Tata Motors의 자회사인 Tata Passenger Electric Mobility는 Sanand에 있는 Ford India의 차량 제조 공장을 72억 5,700만 루피(8,901만 달러)로 인수했습니다. 이 인수에 의해 연산 30만대, 연간 42만대까지 확대 가능한 최신예의 제조 능력이 추가될 전망입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 현재의 시장 시나리오

- 정부의 대처에 관한 통찰

- 최근 산업의 중요한 투자와 개발 동향에 대한 통찰

- 인도의 제조 클러스터에 대한 통찰

- 인도 제조업의 역사에 관한 통찰

- COVID-19가 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 정부는 "Make in India"의 깃발 아래 몇 가지 이니셔티브를 도입

- 인도는 숙련 노동자의 풍부한 수영장을 자랑해, 다양한 부문의 기업의 제조 시설 설립을 촉진

- 시장 성장 억제요인/과제

- 경제 상황의 변동

- 인프라 제한

- 공급망의 혼란

- 시장 기회

- MSME에 대한 정부의 지원

- 높아지는 국내 수요

- 수출 가능성

- 산업의 매력 - Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제6장 시장 세분화

- 소유자별

- 공적 섹터

- 민간 부문

- 공동섹터

- 협동조합 부문

- 사용 원료별

- 농업 관련 산업

- 광물 기반 산업

- 최종 사용자 산업

- 자동차산업

- 제조업

- 섬유 및 의류

- 소비자용 전자 기기

- 건설업

- 음식

- 기타 최종 산업

제7장 경쟁 구도

- 기업 프로파일

- Tata Motors Ltd

- Mahindra & Mahindra Limited

- Ashok Leyland

- Hindustan Unilever Limited

- Godrej group

- Maruti Suzuki Limited

- Tata Steel Limited

- Larsent & Toubro Limited

- Apollo Tyres

- Moser Baer*

- 기타 기업

제8장 시장의 미래

제9장 부록

JHS 25.01.31The India Manufacturing Market size is estimated at USD 338.57 billion in 2025, and is expected to reach USD 523.56 billion by 2030, at a CAGR of 9.11% during the forecast period (2025-2030).

Key Highlights

- India's manufacturing market underwent various phases of development during the pandemic, contributing approximately 16-17% to the GDP and employing nearly 20% of the country's workforce. It has become an attractive destination for foreign investments, with numerous mobile phone, luxury, and automobile brands establishing or considering manufacturing facilities in the country. The implementation of the Goods and Services Tax (GST) unified India into a single market with a GDP of USD 2.5 trillion and a population of 1.32 billion, attracting significant investor interest.

- According to the Indian Cellular and Electronics Association (ICEA), India has the potential to ramp up its cumulative manufacturing capacity for laptops and tablets to USD 100 billion by 2025 through strategic policy interventions. Among the government's initiatives, SAMARTH Udyog Bharat 4.0, led by the Ministry for Heavy Industries & Public Enterprises, aims to enhance the manufacturing market's competitiveness, particularly in terms of capital goods. The focus on developing industrial corridors and smart cities underscores the government's commitment to fostering holistic national development.

- India is steadily advancing toward Industry 4.0 through initiatives such as the National Manufacturing Policy, which targets a 25% share of manufacturing in GDP by 2025, and the Production Linked Incentive (PLI) scheme. The PLI scheme aims to elevate the core manufacturing sector to global standards. The gradual transition to automated and process-driven manufacturing in India is anticipated to enhance efficiency and bolster production capabilities.

India Manufacturing Market Trends

Growing Government Spending is Expected to Boost the Market's Growth

Manufacturing has emerged as one of India's high-growth markets. The government launched the 'Make in India' program to place the country on the map as a manufacturing hub and give global recognition to the economy. For instance, Wistron Corp. collaborated with India's Optiemus Electronics to manufacture products such as laptops and smartphones, significantly boosting the 'Make in India' initiative and electronics manufacturing in the country.

The government has taken several initiatives to promote a healthy environment for the growth of the market. In the Union Budget, the government allocated INR 2,403 crores (USD 315 million) to the promotion of electronics and IT hardware manufacturing. The PLI for semiconductor manufacturing was set at INR 760 billion (USD 9.71 billion) to make India one of the major global producers of this crucial component.

India's manufacturing market is experiencing rapid growth, driven by the expanding population. Increased investments and initiatives like 'Make in India' have positioned the country as a global manufacturing hub. In FY 2023, the manufacturing market saw an annual production growth rate of 4.7%.

Although the gross value added by the manufacturing sector has been steadily increasing, it still lags behind the services sector. However, with the potential of a vast consumer base, global giants like Siemens, HTC, and Toshiba have either established or are in the process of establishing manufacturing facilities in the region. Apple has also initiated operations in India, diversifying its production away from China.

Micro, small, and medium enterprises (MSMEs) play a crucial role in India's transition from an agriculture-based economy to an industrialized one. The contribution of MSMEs to India's GDP has remained stable in recent years, highlighting their importance in driving economic growth and job creation.

Growth of the Automotive Industry is Driving the Market

India holds a prominent position in the global heavy vehicles market, as it is the largest producer of tractors, the second-largest manufacturer of buses, and the third-largest producer of heavy trucks globally. In FY 2022, India's automobile production amounted to 22.93 million vehicles, indicating a robust domestic demand and significant export potential.

In November 2023, total passenger vehicle sales amounted to 334,130 units, marking a slight increase of 3.7% compared to November 2022. This surge represented the highest sales recorded for passenger vehicles in November. In FY 2023, India's automobile exports totaled 4,761,487 units, further demonstrating the country's strong presence in the global automotive market.

Two-wheelers are the dominant vehicle type manufactured in India, constituting the majority of automobiles sold domestically. This category includes motorcycles, scooters, and mopeds. The future growth trajectory of this sector is anticipated to be driven by electric scooters and motorcycles, with many major manufacturers venturing into electric vehicle production.

For instance, in January 2023, Mahindra and Mahindra Ltd, a leading automotive company in India, announced the approval of their investment of INR 10,000 crores (USD 1,226.74 million) for electric vehicles under the government of Maharashtra's industrial promotion scheme for electric vehicles.

India Manufacturing Industry Overview

The Indian manufacturing market is fragmented, with a mix of global and local players. Some of the major players present in the market include Tata Motors Ltd, Mahindra & Mahindra Limited, Ashok Leyland, Hindustan Unilever Limited, and Godrej Group. Major companies in the market adopt product launches, partnerships, business expansions, and acquisitions as key developmental strategies to offer better products and services to customers. For instance, in December 2022, Tata Passenger Electric Mobility, a subsidiary of Tata Motors, completed the acquisition of Ford India's vehicle manufacturing plant in Sanand for INR 725.7 crores (USD 89.01 million). This acquisition was expected to provide an additional state-of-the-art manufacturing capacity of 300,000 units per annum, scalable to 420,000 units per annum.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Insights into Government Initiatives

- 4.3 Insights into Recent Significant Investments and Developments the Industry

- 4.4 Insights into Manufacturing Clusters in India

- 4.5 Insights into History of Manufacturing Industry in India

- 4.6 Impact of the COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The government has introduced several initiatives under the banner of "Make in India"

- 5.1.2 India boasts a sizable pool of skilled labor, facilitating the establishment of manufacturing facilities for companies in various sectors

- 5.2 Market Restraints/Challenges

- 5.2.1 Fluctuating economic conditions

- 5.2.2 Infrastructure limitation

- 5.2.3 Supply chain disruptions

- 5.3 Market Opportunities

- 5.3.1 Government Support for MSMEs

- 5.3.2 Growing Domestic Demand

- 5.3.3 Export Potential

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Ownership

- 6.1.1 Public Sector

- 6.1.2 Private Sector

- 6.1.3 Joint Sector

- 6.1.4 Cooperative Sector

- 6.2 By Raw Materials Used

- 6.2.1 Agro Based Industries

- 6.2.2 Mineral Based Industries

- 6.3 End-user Industries

- 6.3.1 Automotive

- 6.3.2 Manufacturing

- 6.3.3 Textile and Apparel

- 6.3.4 Consumer electronics

- 6.3.5 Construction

- 6.3.6 Food and Beverages

- 6.3.7 Other End-use Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Tata Motors Ltd

- 7.2.2 Mahindra & Mahindra Limited

- 7.2.3 Ashok Leyland

- 7.2.4 Hindustan Unilever Limited

- 7.2.5 Godrej group

- 7.2.6 Maruti Suzuki Limited

- 7.2.7 Tata Steel Limited

- 7.2.8 Larsent & Toubro Limited

- 7.2.9 Apollo Tyres

- 7.2.10 Moser Baer*

- 7.3 Other Companies