|

시장보고서

상품코드

1636223

유럽의 전기자동차용 리튬 이온 배터리 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Europe Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

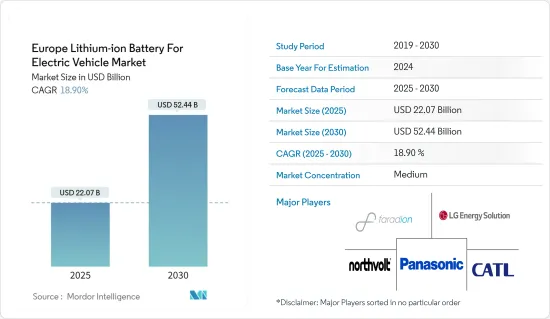

유럽의 전기자동차용 리튬 이온 배터리 시장 규모는 2025년에 220억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 18.9%로, 2030년에는 524억 4,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 스웨덴, 핀란드, 영국에서 전기자동차의 보급이 진행되고 있으며, 정부 정책이 전기자동차용 리튬 이온 배터리 수요를 주도 할 것으로 예측됩니다.

- 한편 대체 배터리 기술의 대두와 원재료의 수급 불균형이 예측기간 중 시장성장을 방해할 것으로 예상됩니다.

- 그럼에도 불구하고 전기자동차에 고체 리튬 이온 배터리의 채택이 증가하고 있기 때문에 유럽의 전기자동차 시장에서 리튬 이온 배터리에 큰 비즈니스 기회가 생길 것으로 예상됩니다.

- 영국은 영국 내 전기자동차 채택 증가로 인해 전기자동차용 리튬 이온 배터리 시장을 독점할 것으로 예상됩니다.

유럽의 전기자동차용 리튬 이온 배터리 시장 동향

배터리 전기자동차(BEV) 부문이 큰 성장

- 배터리 전기 자동차(BEV)는 일반적으로 전기 모터가 장착된 전기 자동차라고도 합니다. BEV는 일반적으로 내연기관(ICE), 연료 탱크 또는 배기관을 포함하지 않고 추진을 위해 전기에 의존하는 완전 전기 자동차입니다. 차량의 에너지는 그리드에서 충전되는 배터리 팩에서 공급됩니다. BEV는 기존 가솔린 차량에서 발생하는 유해한 배기관 배출이나 대기오염 위험을 발생시키지 않기 때문에 무공해 차량입니다.

- 국제에너지기구(IEA)에 따르면 2023년 유럽 내 배터리 전기차 판매량은 220만 대에 달할 것으로 예상됩니다. 현재 유럽 각국에서 다양한 종류의 차량이 출시되고 있으며, 하이브리드화 및 전동화 수준이 높아지고 있습니다. 하이브리드 전기 자동차(HEV), 플러그인 하이브리드 전기 자동차, 전기 자동차(EV) 등 다양한 유형의 차량이 있습니다.

- 또한 파리 기후 협약의 창시자인 유럽은 최근 몇 년간 높은 성장세를 기록하면서 내연기관 자동차에서 전기차로의 전환을 촉진했습니다. 이러한 발전은 결국 이 지역에 리튬 이온 배터리가 보급될 수 있는 길을 열어주었습니다.

- 영국, 독일, 프랑스를 비롯한 여러 국가에서 배터리 전기 자동차(BEV) 도입을 촉진하기 위해 세금 공제 및 보조금과 같은 정책을 시행하고 있습니다. 이와 함께 많은 주에서는 내연기관(ICE) 차량을 단계적으로 퇴출하고 전기차를 보급하겠다는 공격적인 목표를 설정하고 있습니다. 따라서 BEV 채택이 급증하면서 향후 몇 년 동안 리튬 이온 배터리에 대한 수요가 크게 증가할 것으로 예상됩니다.

- 유럽 각국의 여러 정부는 향후 몇 년 동안 전기차 도입을 촉진할 계획입니다. 2024년 5월, 프랑스 정부는 자국 자동차 제조업체들이 10년 말까지 전기 또는 하이브리드 자동차 200만 대를 생산한다는 목표를 세웠습니다. 재무부 브리핑에 따르면 업계는 정부와의 새로운 중기 계획 협약에 따라 2027년까지 80만 대의 전기 자동차 판매라는 중간 목표에 합의할 예정입니다.

- 또한 몇몇 자동차 제조업체는 같은 기간 동안 전기 경형 유틸리티 차량 판매를 연간 10만 대까지 늘리는 것을 목표로 하고 있습니다. 이러한 발전은 유럽 도로에서 증가하는 배터리 전기 자동차를 지원하기 위해 리튬 이온 배터리와 같은 충전식 전기 자동차 배터리에 대한 막대한 수요를 창출할 것으로 예상됩니다.

- 위의 성장 요인들로부터, BEV 부문은 예측 기간 동안 상당한 성장이 예상됩니다.

시장을 독점할 것으로 예상되는 영국

- 영국의 전기 자동차 산업은 탄소 배출을 줄이고 지속 가능한 운송을 촉진하기 위한 정부 규제와 정책에 힘입어 빠르게 성장하고 있습니다. 영국 정부는 2050년까지 순배출량 제로를 달성한다는 광범위한 전략 하에 2030년까지 휘발유 및 디젤 자동차 신규 판매 금지와 같은 야심찬 목표를 설정했습니다.

- 이러한 전환을 지원하기 위해 정부는 전기자동차 보조금, 가정용 및 공공 충전 인프라 보조금 등 다양한 인센티브를 시행하고 있습니다. 이러한 정책은 소비자의 재정적 부담을 완화했을 뿐만 아니라 제조업체가 전기 모델 공급을 늘리도록 장려했습니다.

- 게다가 국제에너지기구(IEA)에 따르면 영국의 배터리식 전기차 판매량은 2023년 30만대에 달할 전망입니다. 또한 영국 정부는 대중화에 필수적인 전기자동차 및 배터리 인프라를 지원하는 데 필요한 인프라의 확장에 주력하고 있습니다. 여기에는 급속 충전소의 수를 크게 늘리려는 국가 전체 충전 네트워크에 대한 많은 투자가 포함됩니다. EV 주차 요금 인하와 런던 등 도시 지역의 교통 체증 면제와 같은 정책은 전기자동차의 매력을 더욱 높여줍니다. 정부의 헌신은 가정용 충전기 설치에 자금을 제공하고 EV 소유의 실용성을 높이는 EV Home Charge Scheme(EVHS)과 같은 프로젝트를 지원하고 있기 때문에 분명합니다.

- 또한 국제에너지기구(IEA)에 따르면 2023년 영국의 배터리 전기 자동차 판매량은 30만 대에 달할 것으로 예상됩니다. 또한 영국 정부는 전기 자동차 및 배터리 인프라를 지원하는 데 필요한 인프라를 확장하는 데 주력하고 있으며, 이는 광범위한 채택에 매우 중요합니다. 여기에는 고속 충전소의 수를 크게 늘리기 위해 전국에 걸쳐 충전 네트워크에 대한 상당한 투자가 포함됩니다. 전기차 주차 요금 감면, 런던과 같은 도시 지역의 혼잡 통행료 면제 등의 정책은 전기 자동차의 매력을 더욱 높이고 있습니다. 정부의 의지는 가정용 충전기 설치에 자금을 지원하여 전기차 소유의 실용성을 높이는 전기차 홈 충전 제도(EVHS)와 같은 프로젝트에 대한 지원에서 분명하게 드러납니다.

- 또한, 2023년 11월 영국 정부는 2030년까지 세계적으로 경쟁력 있는 배터리 공급망을 구축하기 위해 5천만 유로의 정부 자금을 배정하는 새로운 배터리 전략을 포함한 20억 유로(25억 달러) 규모의 첨단 제조 계획을 발표했습니다. 이 계획은 자동차 제조업체들이 배터리 전기 자동차(BEV) 생산으로의 전환을 지원하기 위해 배터리 생산을 현지화함으로써 공급망의 탄력성을 구축하는 것을 목표로 합니다.

- 따라서 위에서 언급 한 사항에 따라 영국은 예측 기간 동안 유럽 전기자동차용 리튬 이온 배터리 시장에서 지배적인 국가가 될 것으로 예상됩니다.

유럽의 전기자동차용 리튬 이온 배터리 산업 개요

유럽의 전기자동차용 리튬 이온 배터리 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 파나소닉 홀딩스, Faradion Limited(영국), Contemporary Amperex Technology(CATL), LG Energy Solution Ltd, Northvolt AB 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 리튬 이온 배터리 가격 하락

- 전기자동차의 보급 확대

- 억제요인

- 새로운 대체 배터리 기술

- 성장 촉진요인

- 공급망 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 차량 유형별

- 승용차

- 상용차

- 기타 차량(오토바이, 스쿠터 등)

- 추진 유형별

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 자동차(PHEV)

- 하이브리드 전기자동차(HEV)

- 지역별

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 노르딕

- 러시아

- 터키

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Panasonic Holdings Corporation

- Faradion Limited(UK)

- Contemporary Amperex Technology Co. Ltd(CATL)

- LG Energy Solution Ltd

- Northvolt AB

- BMZ GmbH

- Saft Groupe SA

- FIAMM Energy Technology

- VARTA AG

- Samsung SDI Co. Ltd

- Tesla Inc.

- 기타 주요 기업 일람(회사명, 본사, 관련 제품 및 서비스, 연락처 등)

- 시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

- 전기자동차에 고체 리튬 이온 배터리 채택

The Europe Lithium-ion Battery For Electric Vehicle Market size is estimated at USD 22.07 billion in 2025, and is expected to reach USD 52.44 billion by 2030, at a CAGR of 18.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of electric vehicles across Sweden, Finland, and the United Kingdom and supportive government policies and initiatives are expected to drive the demand for the lithium-ion battery in electric vehicles market during the forecast period.

- On the other hand, the emerging alternative battery technologies and the demand-supply mismatch of raw materials are expected to hinder the market's growth during the forecast period.

- Nevertheless, the increasing adoption of solid-state lithium-ion batteries for electric vehicles is anticipated to create vast opportunities for lithium-ion batteries in the European electric vehicles market.

- The United Kingdom is expected to dominate the lithium-ion battery for electric vehicles market due to the increasing adoption of electric vehicles in the country.

Europe Lithium-ion Battery for Electric Vehicle Market Trends

Battery Electric Vehicles (BEVs) Segment to Witness Significant Growth

- Battery electric vehicles (BEVs) are also commonly known as electric vehicles with an electric motor. BEVs are fully electric vehicles that typically do not include an internal combustion engine (ICE), fuel tank, or exhaust pipe and rely on electricity for propulsion. The vehicle's energy comes from the battery pack, which is recharged from the grid. BEVs are zero-emission vehicles, as they do not generate harmful tailpipe emissions or air pollution hazards caused by traditional gasoline-powered vehicles.

- According to the International Energy Agency (IEA), battery electric vehicle sales in Europe amounted to 2.2 million units in 2023. Various vehicle types are now available across European countries, featuring increasing degrees of hybridization and electrification. There are various types of vehicles, including hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles, and electric vehicles (EVs).

- Moreover, as the initiator of the Paris Climate Pact, Europe promoted the shift from internal combustion vehicles to EVs while registering high growth over recent years. Such developments, in turn, create avenues for the penetration of lithium-ion batteries in the region.

- Several countries, including the United Kingdom, Germany, and France, are rolling out initiatives such as tax credits and subsidies to drive the adoption of battery electric vehicles (BEVs). In tandem, numerous states are setting aggressive goals to phase out internal combustion engine (ICE) vehicles in favor of electric cars. Consequently, this surge in BEV adoption is poised to significantly elevate the demand for lithium-ion batteries over the coming years.

- Several governments across European countries plan to boost the adoption of EVs in the coming years. In May 2024, the French government set a goal for the nation's carmakers to produce two million electric or hybrid vehicles by the end of the decade. Under a new medium-term planning agreement with the government, the industry is set to agree to an interim goal of 800,000 electric vehicle sales by 2027, according to a Finance Ministry briefing.

- Also, several carmakers aim to increase sales of electric light utility vehicles to 100,000 annually over the same period. Such developments are expected to create a vast demand for rechargeable EV batteries, such as lithium-ion batteries, to support the growing number of battery electric vehicles on European roads.

- Due to the abovementioned factors, the BEV segment is expected to witness significant growth over the forecast period.

United Kingdom Expected to Dominate the Market

- The UK electric vehicle industry has experienced rapid growth, significantly propelled by government regulations and incentives aimed at reducing carbon emissions and promoting sustainable transport. The UK government has set ambitious targets, such as the ban on new petrol and diesel cars by 2030, under its broader strategy to achieve net-zero emissions by 2050.

- To support this transition, the government has implemented various incentives, including grants for electric cars and subsidies for home and public charging infrastructure. These policies have not only eased the financial burden on consumers but have also encouraged manufacturers to increase their offerings of electric models.

- Furthermore, according to the International Energy Agency (IEA), the sales of battery electric vehicles in the United Kingdom stood at 0.3 million units in 2023. Also, the UK government has focused on expanding the necessary infrastructure to support electric vehicles and battery infrastructure, which is crucial for widespread adoption. This includes substantial investments in charging networks across the nation, with the aim to significantly increase the number of fast-charging stations. Policies such as reduced parking fees for EVs and exemptions from congestion charges in urban areas like London have further boosted the attractiveness of electric vehicles. The government's commitment is evident in its backing of projects like the Electric Vehicle Homecharge Scheme (EVHS), which provides funding for home charger installations, enhancing the practicality of owning an EV.

- Moreover, in November 2023, the UK government announced the EUR 2 billion (USD 2.5 billion) Advanced Manufacturing Plan, which includes a new Battery Strategy that will see EUR 50 million of government funding allocated to deliver a globally competitive battery supply chain by 2030. The move aims to build supply chain resilience as vehicle makers localize battery production in support of the increasing transition to the production of battery electric vehicles (BEVs).

- Moreover, manufacturers are responding to the supportive regulatory framework by committing to electric-only production lines and investing in local manufacturing of EVs and batteries, indicating a robust future trajectory for the UK electric vehicle batteries industry.

- Therefore, as per the abovementioned points, the United Kindom is expected to be the dominant country in the European lithium-ion battery for electric vehicles market during the forecast period.

Europe Lithium-ion Battery for Electric Vehicle Industry Overview

The European lithium-ion battery for electric vehicles market is semi-fragmented. Some key players in the market include Panasonic Holdings Corporation, Faradion Limited (UK), Contemporary Amperex Technology Co. Ltd (CATL), LG Energy Solution Ltd, and Northvolt AB.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Declining Lithium-ion Battery Prices

- 4.5.1.2 Increasing Adoption of Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Emerging Alternative Battery Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

- 5.1.3 Other Vehicles (Bikes, Scooters, etc.)

- 5.2 Propulsion Type

- 5.2.1 Battery Electric Vehicles (BEVs)

- 5.2.2 Plug-in Hybrid Electric Vehicles (PHEVs)

- 5.2.3 Hybrid Electric Vehicles (HEVs)

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 United Kingdom

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 NORDIC

- 5.3.7 Russia

- 5.3.8 Turkey

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Holdings Corporation

- 6.3.2 Faradion Limited (UK)

- 6.3.3 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.3.4 LG Energy Solution Ltd

- 6.3.5 Northvolt AB

- 6.3.6 BMZ GmbH

- 6.3.7 Saft Groupe SA

- 6.3.8 FIAMM Energy Technology

- 6.3.9 VARTA AG

- 6.3.10 Samsung SDI Co. Ltd

- 6.3.11 Tesla Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Solid-state Lithium-ion Batteries for Electric Vehicles