|

시장보고서

상품코드

1636236

SLI용 납축배터리 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Lead Acid Battery For SLI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

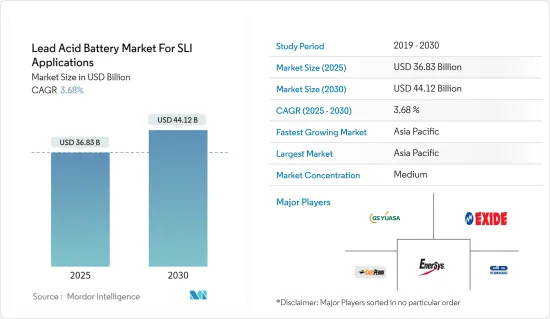

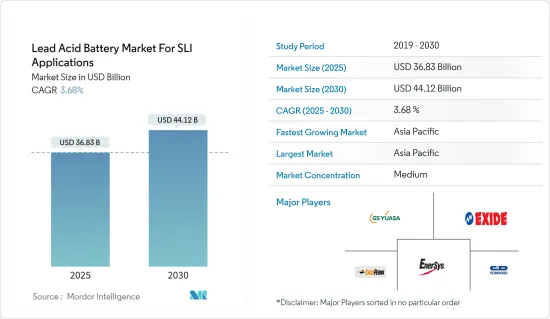

SLI용 납축배터리 시장은 예측 기간(2025-2030년) 동안 연평균 3.68%의 CAGR로 2025년 368억 3,000만 달러에서 2030년 441억 2,000만 달러로 성장할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 자동차 산업의 수요 증가와 납축배터리 재활용 시설 증가 등의 요인이 예측 기간 동안 시장을 견인할 것으로 보입니다.

- 반면, 대체 기술과의 경쟁은 예측 기간 동안 시장 성장을 저해할 것으로 보입니다.

- 기술의 발전은 향후 몇 년 동안 시장에 큰 비즈니스 기회를 가져올 것으로 예상됩니다.

- 아시아태평양은 이 지역의 여러 국가에서 전기자동차 보급률이 높아지면서 시장을 독점할 것으로 추정됩니다.

납축배터리 시장 동향

자동차 산업의 수요 증가

- 자동차 산업은 북미, 유럽, 아시아태평양을 중심으로 다양한 지역의 주요 산업 중 하나입니다. 이들 지역은 도시화가 진행 중이며, 자동차 수요를 견인하고 있어 SLI 배터리의 세계 최대 시장 중 하나입니다.

- 납축배터리는 전 세계 자동차 및 트럭 등 기존 내연기관 자동차에 탑재되는 모든 SLI 배터리 용도에 선택되는 기술입니다. 납축배터리는 기존 자동차의 SLI 응용 분야에서 가장 경제적으로 실현 가능한 양산 기술입니다. 자동차용 SLI 배터리의 90% 이상이 납축배터리 기반이며, 산업용 고정형 및 원동기 용도의 90% 이상(축전 용량 기준)이 납축배터리 기반입니다.

- 2023년 승용차 생산량은 중국이 약 2,610만대로 세계 1위. 2위인 일본은 약 780만 대를 생산했습니다. 이들 국가에는 SLI 배터리의 주요 수요처인 GS Yuasa Corporation, Camel Group 등 세계 최대 규모의 자동차 제조업체도 있습니다.

- 전 세계적으로, 특히 개발도상국에서 자동차 보유량이 증가함에 따라 기존 내연기관(ICE) 차량에 전력을 공급하기 위한 SLI용 배터리에 대한 수요도 함께 증가하고 있습니다.

- 기존 내연기관 자동차 시장은 향후 20-25년 동안 축소될 것으로 예상되지만, 자동차의 대체 기술에서 SLI 타입의 납축배터리는 차량 내 다양한 전자기기와 안전 기능에 전력을 공급하기 위해 계속 사용될 것으로 예상됩니다. 첨단 납 기반 배터리(흡수 유리 매트 또는 강화 침수형 배터리)는 주요 마이크로 하이브리드 자동차의 연비를 개선하기 위한 스타트-스톱 기능을 설명합니다. 스타트-스톱 시스템은 내연기관(ICE)이 제동 또는 휴식 시 자동으로 정지하여 연료 소비를 최대 5-10%까지 줄일 수 있습니다.

- OICA(Organisation Internationale des Constructeurs d'Automobiles)에 따르면, 2023년 세계 승용차 판매량은 6,527만 대에 달할 것으로 예상됩니다. 상용차 판매량은 2023년 2,745만 대에 달할 것입니다. 이는 SLI(시동, 조명, 점화) 용도의 납축배터리를 포함한 자동차 부품에 대한 수요가 강하다는 것을 보여줍니다.

- 이러한 자동차는 엔진 시동 및 차량 내 전자기기 전원 공급과 같은 중요한 기능을 SLI 배터리에 의존하고 있기 때문에 판매량이 지속적으로 증가하면서 납축배터리 수요를 견인하고 있습니다. 이러한 자동차 생산 및 판매의 급증은 세계 SLI용 납축배터리 시장을 유지하고 경우에 따라서는 시장을 견인할 것으로 예상됩니다.

중국이 시장을 독점할 것으로 예상

- 중국의 납축배터리 시장은 특히 시동, 조명, 점화(SLI) 분야에서 큰 성장이 예상됩니다. 이러한 시장 확대의 주요 원인은 팬데믹 이후 회복과 확장을 지속하고 있는 견조한 자동차 산업입니다.

- 자동차 산업은 신뢰할 수 있고 비용 효율적인 배터리를 요구하기 때문에 납축 배터리는 SLI 애플리케이션에 적합합니다. 이 배터리는 자동차 시동 모터, 조명 및 점화 시스템의 전원으로 필수적이며, 고성능과 긴 수명을 보장합니다.

- OICA(Organisation Internationale des Constructeurs d'Automobiles)에 따르면, 중국의 승용차 판매량은 2023년 2,606만 대에 달할 것으로 예상됩니다. 상용차 판매량은 2023년 403만 대에 달할 것으로 예상됩니다. 이에 따라 SLI용 납축배터리를 포함한 자동차 부품에 대한 수요가 발생했습니다.

- 재활용 공정의 개선과 배터리 성능 향상 등 납축배터리 기술의 혁신으로 인해 납축배터리의 경쟁은 치열해지고 있습니다. 리튬이온 배터리의 인기가 높아지고 있음에도 불구하고 납축배터리는 잘 구축된 공급망과 비용 효율성으로 인해 여전히 관련성이 높습니다.

- 자동차 배터리 애프터마켓이 확대되고 있으며, 소비자들은 기존 배터리를 교체하거나 업그레이드하는 경우가 증가하고 있습니다. 이러한 추세는 SLI 카테고리의 수요를 유지하고 시장의 지속적인 성장을 보장하는 데 매우 중요하며, Johnson Controls International PLC, Exide Technologies Inc. 등의 기업들이 시장을 선도하고 있으며, 경쟁 우위를 유지하기 위해 전략적 확장과 기술 혁신에 집중하고 있습니다.

- 전반적으로 중국의 납축배터리 시장은 성장 궤도를 유지할 것으로 예상됩니다. 자동차 산업의 지속적인 발전과 안정적인 수요, 전기자동차의 보급과 첨단 에너지 저장 솔루션에 대한 수요 증가는 이러한 성장을 촉진할 것으로 예상됩니다.

SLI용 납축배터리 산업 개요

SLI용 납축배터리 시장은 세분화되어 있습니다. 주요 참여 기업으로는 GS Yuasa Corporation, C&D Technologies Inc., East Penn Manufacturing Co. Inc., EnerSys, Exide Technologies 등이 있습니다(순서에 관계없이).

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 자동차 산업의 수요 확대

- 납축배터리 재활용 증가

- 성장 억제요인

- 대체 기술과의 경쟁

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 관계

제5장 시장 세분화

- 기술별

- 침수형

- VRLA(밸브 제어식 납축배터리)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 프랑스

- 스페인

- 북유럽

- 터키

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트

- 남아프리카공화국

- 이집트

- 나이지리아

- 카타르

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Johnson Controls International PLC

- Exide Technologies

- EnerSys

- East Penn Manufacturing Co. Inc.

- GS Yuasa Corporation

- Leoch International Technology Limited

- C&D Technologies Inc.

- NorthStar Battery Company LLC

- Camel Group Co. Ltd

- FIAMM Energy Technology SpA

- 시장 순위/점유율 분석

제7장 시장 기회와 향후 동향

- 기술의 진보

The Lead Acid Battery Market For SLI Applications Industry is expected to grow from USD 36.83 billion in 2025 to USD 44.12 billion by 2030, at a CAGR of 3.68% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing demand from the automotive industry and rising lead-acid battery recycling facilities are expected to drive the market during the forecast period.

- On the other hand, competition from alternative technologies is likely to hinder market growth during the forecast period.

- Nevertheless, technological advancements are expected to provide significant opportunities for the market in the coming years.

- Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across various countries in the region.

Lead Acid Battery Market Trends

Growing Demand in the Automotive Industry

- Automotive is one of the major industries in various regions, particularly in North America, Europe, and Asia-Pacific. Growing urbanization in these regions is driving the demand for automobiles, thus making it one of the largest markets for SLI batteries globally.

- A lead-acid battery is the technology of choice for all SLI battery applications in conventional combustion engine vehicles, such as cars and trucks, worldwide. Lead-acid batteries are the most economically viable mass-market technology for SLI applications in traditional vehicles. Over 90% of automotive SLI batteries are lead-acid based, and over 90% (by storage capacity) of industrial stationary and motive applications.

- In 2023, China led the world in passenger car production, with approximately 26.1 million units manufactured. Japan, the second-highest producer, produced around 7.8 million units. These countries are also home to some of the world's largest automobile manufacturers, such as GS Yuasa Corporation and Camel Group Co. Ltd, the major SLI battery consumers.

- With expanding vehicle ownership worldwide, especially in developing regions, there is a parallel rise in the need for SLI batteries to power traditional internal combustion engine (ICE) vehicles.

- Although the market for conventional internal combustion engine vehicles is expected to decline over the next 20 to 25 years, replacement car technologies are expected to continue using SLI-type lead-acid batteries to power various electronics and safety features within the vehicle. Advanced lead-based batteries (absorbent glass mat or enhanced flooded batteries) provide start-stop functionality to improve fuel efficiency in major micro-hybrid vehicles. In start-stop systems, the internal combustion engine (ICE) automatically shuts down under braking and rest, reducing fuel consumption by up to 5-10%.

- According to the OICA (Organisation Internationale des Constructeurs d'Automobiles), the global vehicle sales for passenger cars reached 65.27 million in 2023. The vehicle sales for commercial vehicles reached 27.45 million in 2023. This indicates a robust demand for automotive components, including lead-acid batteries for SLI (starting, lighting, and ignition) applications.

- As these vehicles rely on SLI batteries for essential functions like starting the engine and powering onboard electronics, the continued high sales volumes drive the demand for lead-acid batteries. This vehicle production and sales surge is expected to sustain and possibly boost the global lead-acid battery market for SLI applications.

China is Expected to Dominate the Market

- The lead-acid battery market in China, especially for starting, lighting, and ignition (SLI) applications, is set to witness significant growth. This expansion is primarily driven by the robust automotive industry, which continues to recover and expand post-pandemic.

- The automotive industry's demand for reliable, cost-effective batteries makes lead-acid batteries a preferred choice for SLI applications. These batteries are integral to powering start motors, lights, and ignition systems in vehicles, ensuring high performance and longevity.

- According to OICA (Organisation Internationale des Constructeurs d'Automobiles), China's vehicle sales for passenger cars reached 26.06 million in 2023. The sales for commercial vehicles reached 4.03 million in 2023. This created a demand for automotive components, including lead-acid batteries for SLI applications.

- Innovations in lead-acid battery technology, such as improved recycling processes and enhanced battery performance, have made these batteries more competitive. Despite the growing popularity of lithium-ion batteries, lead-acid batteries remain relevant due to their established supply chain and cost-effectiveness.

- The aftermarket for automotive batteries is growing, with consumers increasingly replacing and upgrading their existing batteries. This trend is critical for maintaining demand in the SLI category and ensuring sustained market growth. Companies like Johnson Controls International PLC, Exide Technologies Inc., and Amara Raja Batteries Ltd are leading the market, focusing on strategic expansions and technological innovations to retain their competitive edge.

- Overall, the lead-acid battery market in China is expected to maintain its growth trajectory. Continuous advancements and steady demand from the automotive industry, along with the increasing adoption of electric vehicles and the need for advanced energy storage solutions, are expected to drive this growth.

Lead Acid Battery Industry Overview

The lead acid battery market for SLI applications is fragmented. Some of the major players include (not in particular order) GS Yuasa Corporation, C&D Technologies Inc., East Penn Manufacturing Co. Inc., EnerSys, and Exide Technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumption

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand in the Automotive Industry

- 4.5.1.2 Increasing Lead-acid Battery Recycling

- 4.5.2 Restraints

- 4.5.2.1 Competition from Alternative Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Technology

- 5.1.1 Flooded

- 5.1.2 VRLA (Valve Regulated Lead-acid)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 Spain

- 5.2.2.4 NORDIC

- 5.2.2.5 Turkey

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Malaysia

- 5.2.3.6 Thailand

- 5.2.3.7 Indonesia

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Egypt

- 5.2.5.5 Nigeria

- 5.2.5.6 Qatar

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Johnson Controls International PLC

- 6.3.2 Exide Technologies

- 6.3.3 EnerSys

- 6.3.4 East Penn Manufacturing Co. Inc.

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Leoch International Technology Limited

- 6.3.7 C&D Technologies Inc.

- 6.3.8 NorthStar Battery Company LLC

- 6.3.9 Camel Group Co. Ltd

- 6.3.10 FIAMM Energy Technology SpA

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements

샘플 요청 목록