|

시장보고서

상품코드

1636271

남미의 전기자동차 배터리 재료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)South America Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

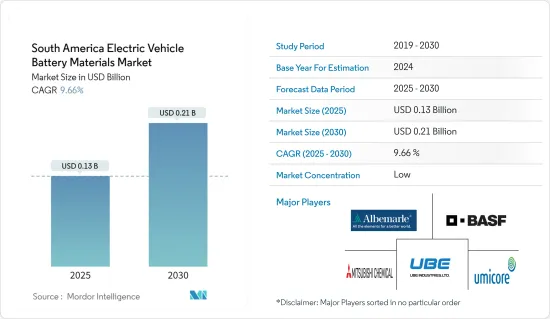

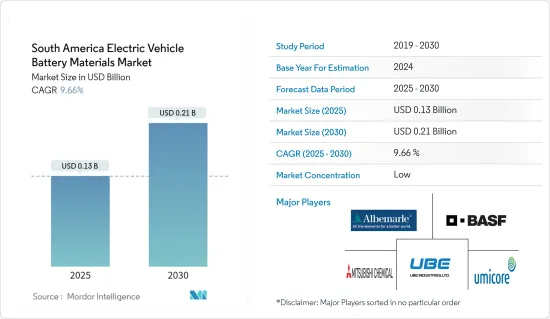

남미의 전기자동차 배터리 재료 시장 규모는 2025년에 1억 3,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 9.66%의 CAGR로 2030년에는 2억 1,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 전기자동차 판매량 증가와 정부 지원 정책 및 시책 등의 요인이 예측 기간 동안 남미 전기자동차 배터리 재료 시장의 가장 큰 촉진요인 중 하나가 될 것으로 예상됩니다.

- 반면, 배터리 재료 생산 설비가 부족하여 수입 의존도가 높아 예측 기간 동안 남미 전기자동차 배터리 재료 시장에 위협이 될 것입니다.

- 첨단 배터리 기술 개발을 위한 노력은 계속되고 있습니다. 이 요인은 향후 시장에 몇 가지 기회를 창출할 것으로 예상됩니다.

- 브라질은 큰 성장이 예상되며, 예측 기간 동안 가장 높은 성장률을 기록할 가능성이 높습니다. 이는 이 지역에 대규모 자동차 제조 및 판매 산업이 존재하기 때문입니다.

남미의 전기자동차 배터리 재료 시장 동향

리튬이온 배터리가 시장을 독점

- 남미의 전기자동차(EV)용 배터리 재료 시장은 리튬이온 배터리에 크게 의존하고 있습니다. 전기자동차 부문에서 가장 널리 사용되는 리튬이온 배터리는 에너지 밀도, 효율성, 내구성을 겸비하여 현대 전기자동차 기술의 핵심이 되었습니다.

- 지난 10년간 배터리 기술 및 제조 분야의 발전은 비용 절감뿐만 아니라 성능과 신뢰성을 증폭시켜 제조업체와 소비자에게 리튬이온 배터리의 매력을 높여왔습니다.

- 최근 몇 년 동안 리튬이온 배터리와 셀 팩의 가격은 하락 추세를 보이고 있으며, 최종사용자에 대한 매력이 증가하고 있으며, 2022년에 소폭 상승한 후 2023년에 가격이 다시 하락하여 리튬이온 배터리 팩은 139달러/kWh로 사상 최저치를 기록하여 14% 하락했습니다. 하락했습니다.

- 이 배터리 부문은 다양한 재료로 구성되어 있으며, 각 재료는 전체 배터리 성능에 중요한 역할을 합니다. 이러한 재료는 에너지 밀도, 사이클 수명, 열 안정성을 높이는 능력에 따라 선택됩니다. 특히, 니켈을 많이 함유한 양극 재료는 에너지 용량이 크고 항속거리 연장과 직결되기 때문에 선호됩니다.

- 이 지역의 전기자동차에 대한 의욕이 높아지면서 리튬이온 배터리 수요가 급증하고 있으며, 배터리 제조업체들이 소재 생산 시설에 대한 투자를 늘리고 있습니다. 이러한 전략적 전환은 국내 및 세계 리튬 배터리 수요 증가에 대응하기 위한 것입니다. 현재 진행 중인 배터리 기술의 발전과 함께 전기자동차의 보급이 증가함에 따라 시장은 지속적인 성장을 이룰 준비가 되어 있습니다.

- 예를 들어, 2023년 4월, 세계 최고의 전기자동차(EV) 제조업체인 중국의 BYD는 2억 9,000만 달러를 투자하여 칠레 안토파가스타 지역에 리튬 양극 공장을 건설할 예정입니다. 이 발표는 칠레의 경제 개발 기관인 CORFO에 의해 이루어졌으며, BYD 칠레는 칠레 정부로부터 공인된 리튬 생산업체로 지정되었다고 CORFO가 확인했습니다. 이 인증으로 BYD 칠레는 탄산리튬을 우선적으로 할당받을 수 있습니다.

- 따라서 예측 기간 동안 리튬이온 배터리 부문이 이 시장에서 우위를 점할 것으로 예상됩니다.

괄목할 만한 성장세를 보이는 브라질

- 브라질은 풍부한 천연자원과 성장하는 산업 역량을 활용하여 남미 전기자동차(EV) 배터리 재료 시장에서 매우 중요한 역할을 하고 있습니다. 특히 리튬, 니켈, 흑연 등 주요 배터리 재료의 막대한 매장량을 보유한 브라질은 전기자동차 부품의 지역 및 세계 공급망에서 잠재적인 강국으로 자리매김하고 있습니다.

- 브라질의 리튬 광상은 미나스 제라이스 주와 세아라 주에 집중되어 있으며, 이 중요한 배터리용 금속에 대한 수요 확대에 편승하려는 국내외 광산 회사들의 큰 관심을 받고 있습니다.

- Energy Institute Statistical Review of World Energy에 따르면, 2023년 리튬 매장량은 4,900톤에 달할 것으로 예상됩니다. 이는 2022년에 기록된 2,600톤에서 크게 증가한 것으로, 88.5%라는 놀라운 성장률을 반영합니다. 이러한 급격한 증가는 중국의 리튬 매장량이 많다는 것을 강조하는 것으로, 특히 전기자동차와 관련하여 급성장하고 있는 배터리 재료 시장에 좋은 징조라고 할 수 있습니다.

- 브라질의 니켈 매장량은 주로 고이아스 주에 위치하고 있어 전기자동차 배터리 재료의 전략적 중요성을 더욱 높이고 있습니다. 또한, 브라질은 미나스 제라이스, 바이아, 세아라 주에 상당한 양의 흑연 광상을 보유하고 있어 리튬이온 배터리용 음극재 생산에 중요한 위치를 차지하고 있습니다.

- 브라질 정부는 전기자동차 배터리 재료 부문의 전략적 중요성을 인식하고 개발을 촉진하기 위해 다양한 이니셔티브를 시행하고 있습니다. 이러한 이니셔티브에는 투자 인센티브, R&D 지원, 지속가능한 채굴 관행 및 현지 부가가치 창출을 촉진하기 위한 규제 프레임워크 등이 포함됩니다.

- 예를 들어, 2024년 4월, 시그마 리튬은 전략적 움직임으로 브라질의 그린테크 산업 플랜트 2단계에 1억 달러의 자본 지출을 결정했습니다. 이번 투자로 2025년까지 연간 5극 제로 그린 리튬 생산능력을 27만 톤에서 52만 톤으로 확대할 예정입니다. 시그마 이사회가 승인한 이번 증설로 시그마는 약 180만 대의 전기자동차(EV)를 연료로 사용할 수 있는 충분한 리튬 정광을 생산할 수 있게 됐습니다.

- 국가광업청(ANM)은 배터리 재료 프로젝트 승인 절차를 간소화했습니다. 동시에 브라질개발은행(BNDES)은 전기자동차 공급망에 관련된 기업들을 지원하기 위한 융자 프로그램을 설립했습니다. 이러한 조치로 인해 국내외 투자를 유치하기 시작했으며, 주요 광산업체 및 배터리 제조업체들이 브라질에서 사업 기회를 모색하고 있습니다.

- 따라서 브라질은 앞서 언급한 바와 같이 예측 기간 동안 큰 성장을 이룰 것으로 예상됩니다.

남미의 전기자동차 배터리 재료 산업 개요

남미 전기자동차 배터리 재료 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 BASF SE、Mitsubishi Chemical Group Corporation、UBE Corporation、Albemarle Corporation、Umicore SA 등이 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 범위

- 시장 정의

- 조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부 정책 및 규정

- 시장 역학

- 성장 촉진요인

- 전기자동차 판매 성장

- 정부 지원 정책 및 규정

- 성장 억제요인

- 배터리 재료 생산 시설의 부족

- 성장 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 소비자의 협상력

- 신규 참여업체의 위협

- 대체품의 위협 제품·서비스

- 경쟁 기업 간의 경쟁 관계

- 투자 분석

제5장 시장 세분화

- 배터리 유형

- 리튬이온 배터리

- 납축배터리

- 기타

- 재료

- 양극

- 음극

- 전해액

- 분리막

- 기타

- 지역

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

제6장 경쟁 구도

- M&A, 합작투자, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Sumitomo Chemical Co., Ltd.

- Albemarle Corporation

- YOUME

- BYD Co., Ltd.

- Arkema SA

- Nichia Corporation

- 기타 저명한 기업 리스트

- 시장 순위/점유율(%) 분석

제7장 시장 기회와 향후 동향

- 배터리 기술의 진보

The South America Electric Vehicle Battery Materials Market size is estimated at USD 0.13 billion in 2025, and is expected to reach USD 0.21 billion by 2030, at a CAGR of 9.66% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the South America Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the lack of battery material production facilities, leading to heavy reliance on imports, poses a threat to the South America Electric Vehicle Battery Materials Market during the forecast period.

- Nevertheless, continued efforts are being made to develop advanced battery technology. This factor is expected to create several opportunities for the market in the future.

- Brazil is expected to witness significant growth and will likely register the highest growth during the forecast period. This is due to the presence of a significant vehicle manufacturing and sales industry in the region.

South America Electric Vehicle Battery Materials Market Trends

Lithium-ion Batteries to Dominate the Market

- The South American electric vehicle (EV) battery materials market hinges significantly on lithium-ion batteries. These batteries, being the most prevalent in the electric vehicle realm, stand out for their blend of energy density, efficiency, and durability, making them a linchpin in modern electric vehicle technology.

- Over the past decade, strides in battery technology and manufacturing have not only cut costs but also amplified performance and reliability, heightening the appeal of lithium-ion batteries to manufacturers and consumers.

- In recent years, there has been a downward trend in lithium-ion battery and cell pack prices, enhancing their allure to end-users. After a slight uptick in 2022, prices dipped again in 2023, with lithium-ion battery packs hitting a historic low of USD 139/kWh, marking a 14% drop.

- This battery segment comprises a range of materials, each playing a vital role in the battery's overall performance. These materials are selected for their ability to boost energy density, cycle life, and thermal stability, which are crucial factors for the automotive sector. Notably, nickel-rich cathode materials are favored for their high energy capacity, directly translating to extended driving ranges-a key selling point for consumers and market competitiveness.

- The region's growing electric vehicle appetite has triggered a surge in lithium-ion battery demand, prompting battery manufacturers to invest in material production facilities. This strategic shift aims to meet the rising demand for lithium batteries, both domestically and globally. Coupled with ongoing battery tech advancements, the market is poised for sustained growth as electric vehicle adoption climbs.

- For instance, in April 2023, China's BYD Co Ltd, the world's leading electric vehicle (EV) manufacturer, is set to construct a lithium cathode factory in Chile's Antofagasta region with an investment of USD 290 million. This announcement was made by Chile's economic development agency, CORFO. BYD Chile has been designated as a recognized lithium producer by the Chilean government, as confirmed by CORFO. This recognition grants the company privileged access to preferential rates for lithium carbonate allocations.

- Given these factors, the dominance of the lithium-ion battery segment in the market is projected for the forecast period.

Brazil to Witness Significant Growth

- Brazil plays a pivotal role in the South American electric vehicle (EV) battery materials market, leveraging its abundant natural resources and growing industrial capabilities. The country's vast reserves of critical battery materials, particularly lithium, nickel, and graphite, position it as a potential powerhouse in the regional and global supply chain for electric vehicle components.

- Brazil's lithium deposits, concentrated in the states of Minas Gerais and Ceara, have attracted significant attention from both domestic and international mining companies seeking to capitalize on the growing demand for this crucial battery metal.

- The Energy Institute Statistical Review of World Energy reported that in 2023, the country's lithium reserves stood at 4.9 thousand tonnes of lithium content. This marked a significant increase from the 2.6 thousand tonnes recorded in 2022, reflecting an impressive growth rate of 88.5%. Such a surge underscores the nation's substantial lithium reserves, a factor that bodes well for the burgeoning battery material market, especially in the context of electric vehicles.

- The country's nickel reserves, primarily found in the state of Goias, further enhance its strategic importance in the electric vehicle battery materials landscape. Additionally, Brazil boasts substantial graphite resources, with significant deposits located in Minas Gerais, Bahia, and Ceara, positioning the country as a critical player in the production of anode materials for lithium-ion batteries.

- The Brazilian government has recognized the strategic importance of the electric vehicle battery materials sector and has implemented various initiatives to foster its development. These efforts include investment incentives, research and development support, and regulatory frameworks aimed at promoting sustainable mining practices and local value addition.

- For instance, in April 2024, Sigma Lithium, in a strategic move, has greenlit a USD 100 million capital expenditure for Phase 2 of its Greentech Industrial Plant in Brazil. By 2025, this investment aims to ramp up the annual production capacity of its Quintuple Zero Green Lithium from 270,000 tons to an impressive 520,000 tons. With the expansion, sanctioned by Sigma's board, the company is poised to churn out sufficient lithium concentrate to fuel an estimated 1.8 million electric vehicles (EVs).

- The National Mining Agency (ANM) has streamlined licensing processes for battery material projects. At the same time, the Brazilian Development Bank (BNDES) has established financing programs to support companies involved in the electric vehicle supply chain. These measures have begun to attract both domestic and foreign investments, with several major mining companies and battery manufacturers exploring opportunities in the country.

- Therefore, Brazil is expected to witness significant growth during the forecast period, as mentioned above.

South America Electric Vehicle Battery Materials Industry Overview

The South America Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Albemarle Corporation, and Umicore SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Lack of Battery Material Production Facility

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Mitsubishi Chemical Group Corporation

- 6.3.3 UBE Corporation

- 6.3.4 Umicore SA

- 6.3.5 Sumitomo Chemical Co., Ltd.

- 6.3.6 Albemarle Corporation

- 6.3.7 YOUME

- 6.3.8 BYD Co., Ltd.

- 6.3.9 Arkema SA

- 6.3.10 Nichia Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology