|

시장보고서

상품코드

1636426

제로웨이스트 식료품점 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Zero-Waste Grocery Stores - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

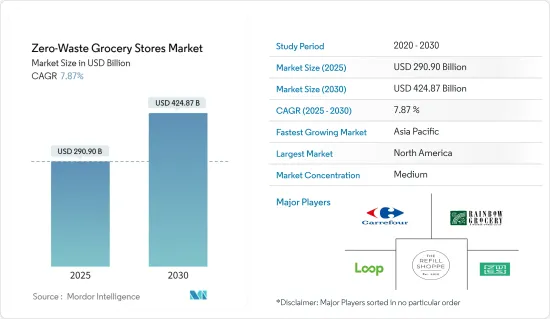

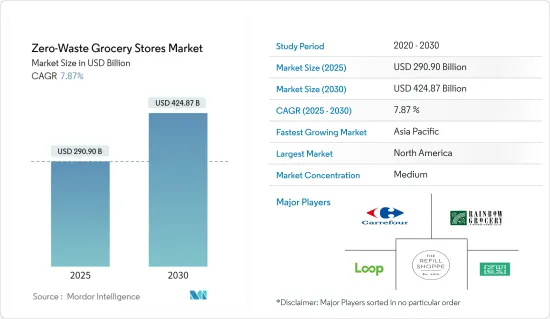

제로웨이스트 식료품점 시장 규모는 2025년 2,909억 달러, 2030년 4,248억 7,000만 달러에 달할 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 7.87%로 예상됩니다.

제로웨이스트 매장은 소매 상황을 재구성하고 플라스틱이나 포장을 사용하지 않는 쇼핑 경험을 고객에게 제공합니다. 이러한 점포는 주로 리필용이나 벌크 푸드 옵션에 중점을 두고, 쇼핑객에게 식품, 퍼스널케어, 클리닝 제품용의 용기를 지참하도록 촉구하고 있습니다. 이러한 점포의 수는 세계적으로 증가하고 있으며, 온라인 플랫폼에서 클라우드 펀딩을 모집하는 점포도 많습니다. 포장재를 사용하지 않을 뿐만 아니라, 폐기물 제로의 점포는 홀리스틱하고 지속 가능한 이념을 내걸고, 현지산이나 유기농의 상품을 폭넓게 소개합니다. 이 독특한 접근 방식은 전통적인 소매점과는 구별되는 점이며 틈새 시장을 개척합니다.

지속 가능한 쇼핑 운동의 최전선에 서 있는 제로웨이스트 식료품점은 컨셉뿐만 아니라 실천에 있어서도 성명을 내고 있습니다. 그 영향은 폐기물 감소에 대한 노력뿐만 아니라 주요 식료품 소매 체인의 반응을 자극하고 있기 때문에 분명합니다. 미국 슈퍼마켓은 식품 판매점의 불과 10%를 차지할 뿐임에도 불구하고 연간 식품 폐기량에 수십억 달러의 거액을 더했습니다. 또한 식품 포장만으로 매립 폐기물 전체의 23%를 차지합니다.

제로웨이스트 식료품점 시장 동향

제로웨이스트 식료품점은 슈퍼마켓/하이퍼마켓에서 성장하고 성장을 가속

다양한 상품을 제공하는 것으로 알려진 슈퍼마켓이나 하이퍼마켓에서는 유통 채널에 제로웨이스트 식료품점을 포함하는 움직임이 급증하고 있습니다. 이 매장은 랩, 가방, 빨대와 같은 기존 포장을 대체하는 것을 제공하여 일회용 플라스틱 사용을 방지하는 기회를 제공합니다. 그럼에도 불구하고, 전통적인 슈퍼마켓/하이퍼마켓은 특히 신선식품에서 여전히 인기있는 쇼핑 장소입니다. 특히 일회용 플라스틱 포장에서 벗어난 슈퍼마켓에서는 야채 매출이 현저하게 급증했습니다. 환경 면에서의 이점뿐만 아니라 폐기물을 0으로 만드는 것은 인건비, 에너지, 폐기 비용을 줄이고 기업에게 상당한 비용 절감을 초래합니다.

온라인 소매 채널은 예측 기간 동안 가장 빠르게 성장할 것으로 예상됩니다. 이 기세는 세계 온라인 쇼핑 증가로 인해 소비자 행동의 명확한 변화를 보여줍니다.

시장을 선도하는 북미

환경 의식이 높아짐에 따라 플라스틱 폐기물의 영향에 대한 감시의 눈도 엄격해지고 있습니다. 미국과 캐나다의 개인은 지속가능성을 향한 운동의 선두에 서 있습니다. 이러한 변화를 뒷받침하기 위해 이 지역 정부는 환경 폐기물을 관리하는 이니셔티브를 개발하고 있으며 향후 몇 년동안 시장이 크게 성장할 무대를 마련하고 있습니다. 점포가 적극적으로 폐기물을 삭감하고 있는 것은 분명하지만, 대기업 소매 슈퍼마켓 체인도 이 동향을 도입하고 있습니다.

슈퍼마켓만으로도 미국에서 연간 배출되는 식품 폐기물의 10%를 차지합니다. 또한 식품 포장은 매립 쓰레기의 23%를 차지합니다. Kea Food, Kroger, Walmart 등 대기업이 주도하는 '10x20X30 이니셔티브'를 통해 향후 10년간 식품 폐기물을 줄이는 것을 목표로 하고 있습니다. 2030년까지 이러한 주요 소매업체는 각각 20개 이상공급업체와 협력하여 폐기물 감소 노력을 더욱 추진하고자 합니다. 지속 가능한 쇼핑의 추진이 확대되어, 제로웨이스트 점포가 새로운 상식이 될 것입니다.

제로웨이스트 식료품점 업계 개요

제로웨이스트 식료품점 시장은 반 고착된 상황을 보여주고 있으며 현재 선택할 수 있는 옵션은 많지 않습니다. 이 보고서는 Rainbow Grocery, Loop, Zero Waste Eco Store, Carrefour, and The Refill Shoppe과 같은 주요 기업을 다루고 경쟁의 역학을 조사했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학과 인사이트

- 시장 개요

- 시장 성장 촉진요인

- 환경 의식의 고조가 시장을 견인

- 환경 친화적인 선택을 요구하는 소비자 수요가 시장의 성장을 가속

- 시장 성장 억제요인

- 초기설정 비용의 높이가 시장의 성장을 방해한다

- 점포에서의 위생 기준 유지를 위한 물류 과제

- 시장 기회

- 현지 생산자 및 공급업체와의 파트너십 가능성

- 온라인 판매를 위한 디지털 플랫폼의 활용

- 밸류체인 분석

- 업계의 매력 Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 업계의 기술적 진보에 관한 통찰

- 시장에 대한 COVID-19의 영향

제5장 시장 세분화

- 유통 채널별

- 슈퍼마켓/하이퍼마켓

- 전문점

- 온라인 스토어

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도 개요

- 기업 프로파일

- Rainbow Grocery

- Loop

- Zero Waste Eco Store

- Carrefour

- The Refill Shoppe

- Just Gaia

- Zero Muda

- EcoRefill

- ecoTopia

- Lidl*

제7장 향후 시장 동향

제8장 면책사항 및 출판사에 대해서

JHS 25.02.10The Zero-Waste Grocery Stores Market size is estimated at USD 290.90 billion in 2025, and is expected to reach USD 424.87 billion by 2030, at a CAGR of 7.87% during the forecast period (2025-2030).

Zero waste stores are reshaping the retail landscape, offering customers a plastic and packaging-free shopping experience. These stores primarily focus on refill and bulk options, encouraging shoppers to bring their containers for food, personal care, and cleaning products. The global count of such stores has surpassed, with many new ones seeking crowdfunding on online platforms. Beyond being packaging-free, zero-waste stores often champion a holistic, sustainable ethos, showcasing a range of local and organic products. This distinctive approach sets them apart from traditional retailers, carving a niche for themselves.

Zero-waste grocery stores, at the forefront of the sustainable shopping movement, are making a statement not just in concept but also in practice. Their impact is evident, not only in their waste reduction efforts but also in catalyzing responses from major retail grocery chains. Despite accounting for just 10% of food outlets, US supermarkets add massive billions of dollars to the total yearly food waste. Furthermore, food packaging alone constitutes 23% of all landfill waste.

Zero-Waste Grocery Stores Market Trends

Zero-Waste Grocery Stores Proliferate in Supermarkets and Hypermarkets, Propelling Growth

Supermarkets and hypermarkets, known for their diverse product offerings, have seen a surge in the inclusion of zero-waste grocery stores within their distribution channels. These stores present a unique opportunity to combat single-use plastic by offering alternatives to traditional packaging, such as plastic wraps, bags, and straws. Despite this, traditional supermarkets and hypermarkets remain popular shopping destinations, especially for fresh produce. Notably, supermarkets that transitioned away from single-use plastic packaging witnessed a remarkable surge in vegetable sales. Beyond the environmental benefits, going zero-waste also translates to significant cost savings for businesses, cutting down on labor, energy, and disposal expenses.

The online retail channel is poised for the swiftest growth during the forecast period. This momentum is fueled by the global uptick in online shopping, indicating a clear shift in consumer behavior.

North America Leading the Market

As environmental consciousness rises, so does the scrutiny of the repercussions of plastic waste. Individuals in the United States and Canada are spearheading the movement toward sustainability. Bolstering this shift, governments in the region have rolled out initiatives to manage environmental waste, setting the stage for significant market growth in the coming years. While it's evident that stores are actively reducing waste in their operations, major retail supermarket chains are also embracing this trend.

Supermarkets alone contribute to 10% of food waste produced annually in the United States. Additionally, food packaging constitutes a significant 23% of landfill waste. Through the "10x20X30 Initiative," spearheaded by major players like Kea Food, Kroger, and Walmart, the goal is to slash food waste over the next decade. By 2030, these leading retailers aim to collaborate with at least 20 suppliers each, furthering their waste reduction efforts. As the push for sustainable shopping gains momentum, zero-waste stores are set to become the new norm.

Zero-Waste Grocery Stores Industry Overview

The zero-waste grocery store market exhibits a semi-consolidated landscape, with only a handful of options available presently. The report delves into the competitive dynamics, highlighting key players such as Rainbow Grocery, Loop, Zero Waste Eco Store, Carrefour, and The Refill Shoppe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Environmental Consciousness Driving the Market

- 4.2.2 Consumer Demand for Eco-friendly Options Fuels Growth of the Market

- 4.3 Market Restraints

- 4.3.1 Higher Initial Setup Costs Hinder Growth of the Market

- 4.3.2 Logistical Challenges in Maintaining Hygiene Standards in Stores

- 4.4 Market Opportunities

- 4.4.1 Potential Partnerships with Local Producers and Suppliers

- 4.4.2 Leveraging Digital Platforms for Online Sales

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Distribution Channel

- 5.1.1 Supermarkets/Hypermarkets

- 5.1.2 Speciality Stores

- 5.1.3 Online Stores

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Italy

- 5.2.2.6 Spain

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Rainbow Grocery

- 6.2.2 Loop

- 6.2.3 Zero Waste Eco Store

- 6.2.4 Carrefour

- 6.2.5 The Refill Shoppe

- 6.2.6 Just Gaia

- 6.2.7 Zero Muda

- 6.2.8 EcoRefill

- 6.2.9 ecoTopia

- 6.2.10 Lidl*