|

시장보고서

상품코드

1636472

북미의 전기자동차 배터리 제조 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

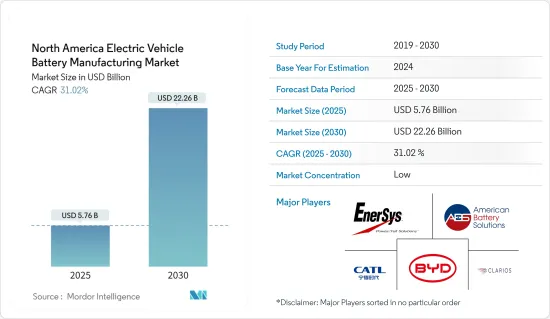

북미 전기자동차 배터리 제조 시장 규모는 2025년 57억 6,000만 달러, 2030년 222억 6,000만 달러로 추정되며, 예측 기간(2025-2030년)중 CAGR은 31.02%에 달할 것으로 예측됩니다.

주요 하이라이트

- 향후 수년간 북미의 전기자동차 배터리 제조 시장은 정부의 지원 정책과 정책에 밀려온 전기자동차의 보급 확대에 의해 크게 견인될 전망입니다.

- 그러나 아시아태평양의 확립된 배터리 시장과의 경쟁은 북미의 전기자동차 배터리 제조 시장에 과제가 되고 있습니다.

- 그러나 북미 국가가 배터리 제조 공급망의 현지화를 추진함에 따라 시장 성장 기회가 많이 드러나고 있습니다.

- 미국 정부의 배터리 제조 강화에 대한 노력이 강화되고 전기자동차 채용이 급증하고 있기 때문에 미국이 시장을 선도하게 되어 가장 큰 성장이 예상됩니다.

북미 전기자동차 배터리 제조 시장 동향

EV 배터리가 크게 성장

- 기술의 진보, 규제의 뒷받침, 소비자의 선호도의 진화에 힘입어 EV 배터리 북미 시장은 특히 배터리 전기자동차(BEV) 부문에서 강력한 급성장을 이루고 있습니다. 배터리 구동 전기 파워트레인에서만 작동하는 BEV는 지속 가능한 운송으로의 세계 이동에 매우 중요한 역할을 합니다.

- 북미에서는 자동차 제조업체와 정책 입안자가 야심찬 온실가스 배출 감축을 약속하는 가운데 BEV 분야가 성장하게 됩니다. 이산화탄소 배출량을 억제하고 엄격한 배출 기준을 준수하려고 하는 움직임이 BEV의 생산과 보급을 뒷받침하고 있습니다. BEV는 하이브리드 자동차와 달리 테일파이프 배출이 없는 것이 특징입니다.

- 국제에너지기구(IEA)의 보고에 따르면 전기차 판매량은 2021년 이후 급상승해 72만 7,730대와 2배 이상 증가했습니다. 그 기세는 계속되어 2022년에는 111만 7,719대가 판매되고, 2023년에는 158만 4,113대로 도약했습니다. 이 판매 붐은 이러한 자동차의 주력 전원인 리튬 이온 배터리 수요 급증과 밀접한 관계가 있습니다.

- 북미의 급성장하는 배터리 제조 능력은 BEV 부문의 성공에 필수적입니다. 배터리 부품과 원재료를 수입에 의존하는 지정학적 및 물류적 장애물을 감안할 때, 강력한 국내 공급망의 확립은 중요성을 증가시키고 있습니다. 이에 따라 북미 시장에서는 투자가 활발해지고 있으며, 여러 기업이 지역 전체에 '기가팩토리'를 설립하고 있습니다.

- 그 일례로 Honda Motor은 캐나다의 온타리오주에서 전기차와 배터리의 생산 체제를 강화하기 위해 110억 달러를 투입해 2028년까지 조업을 개시할 계획입니다. 이 야심찬 시도는 Honda에게 가장 큰 캐나다 투자이며 연간 생산량 24만대의 전기차와 36기가와트 배터리를 목표로 하고 있습니다.

- 이러한 전략적 위치 시설은 종종 자동차 제조 기지 근처에 있으며 규모의 경제를 달성하고 생산 비용을 억제하며 소비자에게 BEV를 널리 보급하는 데 매우 중요합니다. 자동차 생산 거점에 가깝기 때문에 공급망이 유동적이며 저스트 인 타임 생산이 가능합니다.

- 이러한 역학을 고려하면, 배터리 전기자동차 부문은 향후 몇 년동안 크게 성장할 전망입니다.

시장을 독점하는 미국

- 미국은 역동적인 혁신, 정책 지원 및 전략적 투자를 특징으로 하는 북미 전기자동차 배터리 제조 시장에서 매우 중요한 선수입니다. 전기자동차 배터리 시장은 보다 지속가능한 교통 생태계로의 전환이라는 국가적 요구에 따라 빠르게 확대되고 있습니다. 소비자와 제조업체 모두를 대상으로 한 정부의 상당한 인센티브가 이러한 전환을 지원합니다.

- 전기자동차 구매세액공제와 연구개발을 위한 다액자금제공 등 연방정책은 기술 혁신을 촉진하고 전기자동차 채용을 늘리도록 설계되었습니다. 또한 인플레이션 감축법과 같은 최근의 법률은 전기자동차 배터리의 국내 생산을 촉진하기 위한 중요한 조항을 포함하고 있으며, 기업이 국내에 제조 시설을 설립하기 위한 재정적 인센티브를 제공합니다.

- 예를 들어 미국 환경 방위 기금에 따르면 2023년 향후 예정될 배터리 생산 시설의 발표 용량을 합하면 약 131GWh가 됩니다. 예측에 따르면 이 수치는 급증하고 2025년에는 738GWh에 달할 수 있으며 연간 성장률은 154%를 초과합니다. 이 확장은 전기자동차 배터리 제조 시장에 큰 영향을 미치며 전기자동차 수요 증가에 대응할 수 있습니다.

- 기술 혁신은 미국 전기자동차 배터리 제조 시장의 핵심입니다. 미국의 기업 및 연구 기관은 에너지 밀도, 안전성 및 수명주기의 상당한 개선을 약속하는 고체 배터리를 포함한 차세대 배터리 기술 개발의 최전선에 있습니다.

- 예를 들어 2023년 3월 미국 에너지부 산하 아르곤 국립연구소는 리튬공기 배터리의 선구자가 되었습니다. 이 기술 혁신은 전기차의 항속거리가 크게 연장될 것으로 기대되고 있습니다. 이 배터리의 잠재적인 용도는 자동차나 국내 항공기의 동력원에서 장거리 트럭의 운행 촉진까지 다양합니다. 주목해야할 것은 이 설계가 액체 전해액과 관련된 과열 및 발화의 위험을 없애 기존의 배터리에 있던 심각한 안전 문제를 해결하는 것입니다.

- 미국에서 전기자동차 배터리 제조 시장의 확대를 지원하는 것은 충전 인프라 네트워크의 확대입니다. 주요 교통 통로 및 도시 지역의 급속 충전 옵션 등 충전소의 종합적인 네트워크를 미국에서 개발하기 위해 많은 투자가 이루어지고 있습니다. 또한 무선 충전 및 초고속 충전과 같은 충전 기술의 혁신이 사용자 경험을 더욱 향상시키고 거리에서 증가하는 전기자동차를 지원하기 위해 검토되고 있습니다.

- 따라서 앞서 언급했듯이 예측 기간 동안 미국이 시장의 지배적인 지역이 될 것으로 예상됩니다.

북미 전기자동차 배터리 제조 업계 개요

북미의 전기자동차 배터리 제조 시장은 반 파편화되었습니다. 이 시장의 주요 기업(순부동)은 BYD, Contemporary Amperex Technology Co.Limited, American Battery Solutions, Inc., EnerSys, Clarios입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모 및 수요 예측(단위: 달러)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 전기자동차의 보급 확대

- 지원적인 정부의 규제와 정책

- 억제요인

- 기존 시장과의 경쟁

- 성장 촉진요인

- 공급망 분석

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 세분화

- 배터리별

- 리튬 이온

- 납축

- 니켈 수소

- 기타

- 형상별

- 각형

- 가방형

- 원통형

- 차량별

- 승용차

- 상용차

- 기타

- 추진별

- 배터리 전기자동차

- 하이브리드 전기자동차

- 플러그인 하이브리드 전기자동차

- 지역별

- 미국

- 캐나다

- 기타 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- American Battery Solutions, Inc.

- EnerSys

- GS Yuasa Corporation

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- Sionic Energy

- Clarios LLC

- 기타 주요 기업 목록

- 시장 랭킹/공유(%) 분석

제7장 시장 기회와 앞으로의 동향

- 공급망의 현지화

The North America Electric Vehicle Battery Manufacturing Market size is estimated at USD 5.76 billion in 2025, and is expected to reach USD 22.26 billion by 2030, at a CAGR of 31.02% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the North American electric vehicle battery manufacturing market is poised to be significantly driven by the region's increasing adoption of electric vehicles, bolstered by supportive government policies and regulations.

- However, competition looms from established battery markets in the Asia Pacific, presenting a challenge to North America's electric vehicle battery manufacturing landscape.

- Yet, as North American countries push for localized battery manufacturing supply chains, they unveil a plethora of opportunities for the market's growth.

- With the United States government's intensified efforts to bolster battery manufacturing and the surging adoption of electric vehicles, the United States is set to lead the market and is projected to witness the most substantial growth.

North America Electric Vehicle Battery Manufacturing Market Trends

Battery Electric Vehicle to Witness Significant Growth

- Driven by technological advancements, regulatory backing, and evolving consumer preferences, the North American market for electric vehicle batteries is witnessing a robust surge, particularly in the battery electric vehicles (BEV) segment. BEVs, which operate exclusively on battery-powered electric powertrains, play a pivotal role in the global shift towards sustainable transportation.

- In North America, as automakers and policymakers commit to ambitious greenhouse gas emission reductions, the BEV segment is set for growth. The push to curb carbon footprints and adhere to strict emission standards is propelling the production and uptake of BEVs, which stand out by having no tailpipe emissions, unlike their hybrid counterparts.

- Electric vehicle sales, as reported by the International Energy Agency, have seen a meteoric rise since 2021, more than doubling to 727,730 units. The momentum continued with 1,117,719 units sold in 2022, and a leap to 1,584,113 units in 2023. This sales boom is closely linked to the surging demand for lithium-ion batteries, the mainstay power source for these vehicles.

- North America's burgeoning battery manufacturing capacity is crucial for the BEV segment's success. Given the geopolitical and logistical hurdles of depending on imported battery components and raw materials, the establishment of strong domestic supply chains takes on heightened significance. In response, the North American market is witnessing a flurry of investments, with several companies setting up 'gigafactories' across the region.

- As a case in point, Honda Motor is channeling a hefty USD 11 billion into bolstering its electric vehicle and battery production footprint in Ontario, Canada, with plans to commence operations by 2028. This ambitious endeavor, Honda's largest Canadian investment to date, aims for an annual output of 240,000 electric vehicles and 36 gigawatt-hours of batteries.

- These strategically located facilities, often near automotive manufacturing centers, are pivotal for achieving economies of scale, curbing production costs, and broadening the accessibility of BEVs to consumers. Their proximity to automotive hubs ensures a fluid supply chain and supports just-in-time production.

- Given these dynamics, the battery-electric vehicle segment is on track for substantial growth in the coming years.

United States to Dominate the Market

- The United States is a pivotal player in the North American electric vehicle battery manufacturing market, characterized by dynamic technological innovation, policy support, and strategic investments. The market for electric vehicle batteries is rapidly expanding, driven by a national imperative to transition to a more sustainable transportation ecosystem. Substantial government incentives aimed at both consumers and manufacturers support this shift.

- Federal policies, such as tax credits for electric vehicle purchases and substantial funding for research and development, are designed to spur innovation and increase the adoption of electric vehicles. Furthermore, recent legislation, such as the Inflation Reduction Act, includes significant provisions to promote the domestic production of electric vehicle batteries, providing financial incentives for companies to establish manufacturing facilities within the country.

- For instance, according to the United States Environmental Defense Fund, in 2023, the combined announced capacity of upcoming battery production facilities totaled about 131 GWh. Projections indicate this figure will surge, potentially hitting 738 GWh by 2025, translating to an annual growth rate exceeding 154%. This expansion significantly impacts the Electric Vehicle Battery Manufacturing Market, enabling it to meet the increasing demand for electric vehicles.

- Technological innovation is at the core of the United States electric vehicle battery manufacturing market. American companies and research institutions are at the forefront of developing next-generation battery technologies, including solid-state batteries, which promise significant improvements in energy density, safety, and lifecycle.

- For instance, in March 2023, the Argonne National Laboratory, under the United States Department of Energy, pioneered a lithium-air battery. This innovation holds the promise of substantially extending the range of electric vehicles. The battery's potential applications are vast, from powering cars and domestic airplanes to facilitating long-haul truck operations. Notably, this design addresses a critical safety concern prevalent in traditional batteries, as it eliminates the risk of overheating and fire associated with liquid electrolytes.

- A growing network of charging infrastructure supports the expansion of the electric vehicle battery manufacturing market in the United States. Significant investments are being made to develop a comprehensive network of charging stations across the country, including fast-charging options along major transportation corridors and in urban areas. Additionally, innovations in charging technology, such as wireless and ultra-fast charging, are being explored to improve the user experience further and support the growing number of electric vehicles on the road.

- Therefore, as mentioned above, the United States is expected to be the dominant region in the market during the forecast period.

North America Electric Vehicle Battery Manufacturing Industry Overview

The North America Electric Vehicle Battery Manufacturing Market is semi-fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd, Contemporary Amperex Technology Co. Limited, American Battery Solutions, Inc., EnerSys, and Clarios.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Supportive Government Regulations and Policies

- 4.5.2 Restraints

- 4.5.2.1 Competition From Established Markets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 American Battery Solutions, Inc.

- 6.3.4 EnerSys

- 6.3.5 GS Yuasa Corporation

- 6.3.6 LG Chem Ltd

- 6.3.7 Exide Industries

- 6.3.8 Panasonic Corporation

- 6.3.9 Sionic Energy

- 6.3.10 Clarios LLC

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Localization of Supply Chains