|

시장보고서

상품코드

1636491

독일의 전기자동차 전지 전해액 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Germany Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

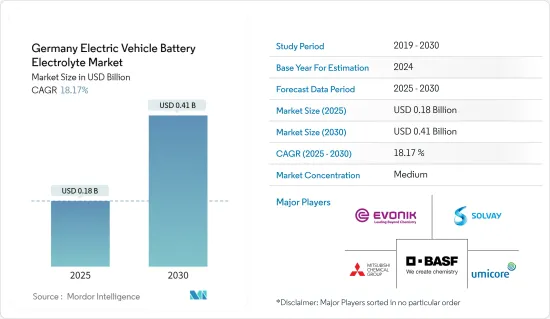

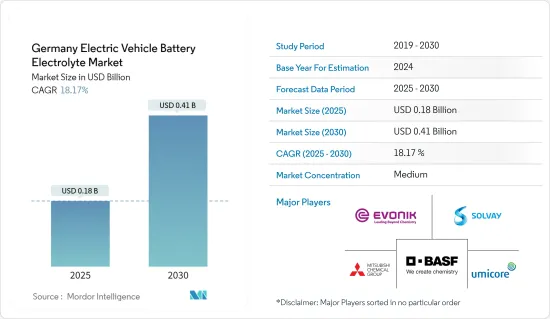

독일 전기차용 전지 전해액 시장 규모는 2025년 1억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 18.17%로, 2030년에는 4억 1,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 동지역 전체에서 전기자동차의 보급이 진행되고 있어 전지 제조를 위한 정부의 지원 시책이나 투자가 예측 기간중의 독일의 전기자동차용 전지 전해액 시장 수요를 견인할 것으로 예상됩니다.

- 한편, 전해액 생산에 사용되는 주요 원료의 기타 국가에 대한 의존성은 독일 전기자동차 전지 전해액 시장의 성장을 억제할 것으로 예상됩니다.

- 특히 고성능 또는 장거리 EV를 위해 전지 성능, 안전성 및 수명을 향상시키는 전해액 배합의 혁신은 가까운 미래에 독일 전기자동차 전지 전해액 시장에 큰 성장 기회를 창출할 것으로 예상됩니다.

독일 전기자동차 전지 전해액 시장 동향

리튬 이온 전지가 큰 점유율을 차지할 전망

- 독일은 전기자동차(EV)의 유럽 최고 시장입니다. 독일에서는 보조금, 세제 우대 정책, 배기 가스 절감 목표 등에 대한 엄격한 규제 등 정부의 이니셔티브에 의해 전기 이동성에 대한 대처가 강화되고 있습니다. EV의 보유 대수가 확대됨에 따라, 리튬 이온 전지, 나아가서는 그 기능에 필수적인 전해액 수요도 확대되고 있습니다.

- 또한 리튬 이온 전지의 재료 가격이 하락함에 따라 각 제조업체는 EV용 전지 생산에 대한 투자를 확대하고 있습니다. 이러한 생산량 증가는 전해액을 비롯한 필수 전지 부품 수요를 자연스럽게 증가시킵니다.

- 예를 들어, 2023년 리튬 이온 전지 팩의 비용은 전년보다 14% 하락해 139달러/kWh로 안정되었습니다. 이러한 전지 가격 하락은 합리적인 가격의 EV로 이어지고, 대중화를 가속시켜 전기자동차 시장 점유율을 상승시킵니다. 이러한 수요 증가는 전해질을 중심으로 하는 전지 부품의 소비 증가를 나타낼 뿐만 아니라, 전지 성능의 향상을 목표로 한 기술 진보를 뒷받침하고 있습니다.

- 게다가 독일은 양극, 음극, 전해질을 포함한 리튬 이온 전지용 재료의 수입 의존도를 낮추는 것을 목표로 공급망 격차를 줄이기 위해 적극적으로 노력하고 있습니다. EV용 전지 제조와 리튬 생산의 양면에서 대규모 투자 계획이 진행 중이기 때문에 리튬 이온 전지 부품, 특히 전해액 수요가 현저해질 것으로 예상됩니다.

- 예를 들어, 2024년 5월, Rock Tech Lithium Inc.는 독일 구벤에 리튬 정제소를 설립할 수 있는 인가를 받았습니다. 이 정제소는 전기자동차 전지 및 에너지 저장 시스템에 필수적인 성분인 수산화리튬의 생산 능력 약 2만 4,000톤을 자랑할 것으로 예측되고 있습니다.

- 또 다른 움직임으로, 2024년 2월 Automotive Cells Company(ACC)는 프랑스, 독일, 이탈리아에 걸쳐 있는 3개의 리튬 이온 전지 기가팩토리를 설립하기 위해 47억 달러의 자금을 모았습니다. ACC는 2030년까지 리튬 이온 전지의 생산량이 200만개를 초과할 것으로 예측했습니다. 이러한 전략적 투자는 향후 수년간 리튬 이온 전지용 전해액 수요를 증대시킬 것으로 예상됩니다.

- 이러한 동향을 근거로 리튬 이온 전지용 전해액 부문은 예측 기간 중에 크게 상승할 것으로 예상됩니다.

전지 제조 투자가 시장을 견인하는 전망

- Volkswagen, BMW, Daimler(Mercedes-Benz)와 같은 선도적인 자동차 기업의 본거지인 독일에서는 이러한 선도기업이 전기자동차(EV) 개발에서 크게 앞서고 있습니다. 이들 제조업체는 보유 차량의 상당 부분을 전동화할 계획으로 EV 전지와 이에 필수적인 전해액 수요를 급증시키고 있습니다.

- EV 부문에 대한 투자를 강화하기 위해 독일 정부는 일련의 인센티브와 보조금을 전개하고 있습니다. 전기차 판매가 계속 증가하는 가운데 정부는 자국 내 전지 제조를 더욱 강화하기 위한 추가 조치를 발표할 것으로 예상됩니다. 국제에너지기구의 데이터는 이 동향을 돋보이게 합니다. 2023년 독일 전지 전기자동차(BEV) 판매량은 52만대에 달했으며 2022년 47만대에서 현저하게 증가했습니다.

- 이에 발맞춰 복수의 전지 제조업체가 독일에서 파트너십을 맺어 보다 효율적일 뿐만 아니라 전체적인 성능도 향상시킨 EV용 전지 생산을 목표로 하고 있습니다. 이러한 진보의 중심이 바로 선진적인 전지 전해액 배합 기술입니다. 이러한 최첨단 배합 기술은 전지 수명과 안전성을 늘릴 뿐만 아니라 에너지 밀도도 향상시켜 산업의 미래 혁신에 중요한 역할을 담당하고 있습니다.

- 2024년 5월 유명 전지 제조업체인 VARTA는 15개 기업과 대학으로 구성된 컨소시엄을 주도했습니다. ENTISE 프로젝트를 중심으로 하는 이 제휴는 나트륨 이온 기술의 잠재력을 활용하여 산업 용도를 위한 고성능 친환경 전지 제조에 전념하고 있습니다. 독일 연방연구교육부로부터 약 750만 유로의 보조금을 얻어 컨소시엄은 2027년 중반까지 프로젝트의 최종 단계를 마무리할 계획입니다.

- 에너지 밀도와 안전성이 뛰어난 것으로 여겨지는 고체 전지로 산업이 전환하면서 전해액의 요건도 변화할 것으로 예상됩니다. 최근 기업 간의 협정이 잇따르고 있어 자동차 영역에서 급증하는 고체 전지 수요에 부응하려는 산업의 노력이 부각되고 있습니다.

- 예를 들어, 2024년 7월 Volkswagen Group의 전지 부서인 Powerco는 QuantumScape와 계약을 맺고 QuantumScape의 선구적인 고체 리튬 금속 전지 기술을 산업 최전선에 도입했습니다. 이러한 제휴는 고체 전지에 대한 수요 증가를 나타낼 뿐만 아니라, EV용 전지의 생산에 있어서 전해액의 안정적인 공급의 필요성을 강조하고 있습니다.

- 이러한 신흥국 시장의 개척과 자금의 유입을 감안하면, EV용 전지의 생산 능력을 강화하는 것을 목적으로 하는 투자는 시장을 활성화시킬 것으로 예상됩니다.

독일 전기자동차 전지 전해질 산업 개요

독일 전기자동차 전지 전해액 시장은 완만합니다. 동시장의 주요 기업(순서부동)에는 Evonik Industries AG, BASF SE, Solvay SA, Umicore SA, Mitsubishi Chemical Group Corporation 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 2029년까지 시장 규모와 수요 예측(단위 : 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 촉진요인

- 전기자동차 보급 확대

- 전지 제조를 위한 정부의 지원 시책과 투자

- 억제요인

- 전해액 제조에 사용되는 주요 원료의 타국 의존도

- 촉진요인

- 공급망 분석

- PESTLE 분석

- 투자 분석

제5장 시장 세분화

- 전지 유형

- 리튬 이온

- 납축전지

- 기타 전지 유형

- 전해질 유형

- 액체 전해질

- 겔 전해질

- 고체 전해질

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 개요

- Evonik Industries AG

- BASF SE

- Solvay SA

- Mitsubishi Chemical Group.

- Umicore SA

- Targray Industries Inc.

- 3M Company

- NEI Corporation

- Cabot Corporation

- 삼성SDI

- 기타 유력 기업 목록

- 시장 순위 분석

제7장 시장 기회와 앞으로의 동향

- 전해질 제제 혁신

The Germany Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.18 billion in 2025, and is expected to reach USD 0.41 billion by 2030, at a CAGR of 18.17% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing adoption of electric vehicles and supportive government policies and investments towards battery manufacturing across the region are expected to drive the demand for the Germany electric vehicle battery electrolyte market during the forecast period.

- On the other hand, the dependence on other countries for key raw materials used in the production of electrolytes is expected to restrain the growth of the Germany electric vehicle battery electrolyte market.

- Nevertheless, the innovation in electrolyte formulations that improve battery performance, safety, and lifespan, particularly for high-performance or long-range EVs, creates significant growth opportunities in the Germany electric vehicle battery electrolyte market in the near future.

Germany Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery is Expected to Have a Major Share

- Germany stands as one of Europe's foremost markets for electric vehicles (EVs). The nation's push towards electric mobility is bolstered by government initiatives, including subsidies, tax incentives, and stringent regulations like emission reduction targets. As the fleet of EVs expands, so does the demand for lithium-ion batteries, and by extension, the electrolytes integral to their function.

- Moreover, as the prices of materials for lithium-ion batteries decline, manufacturers are ramping up investments in EV battery production. This uptick in production naturally amplifies the demand for essential battery components, notably electrolytes.

- For example, in 2023, the cost of lithium-ion battery packs saw a 14% drop from the previous year, settling at USD 139/kWh. This decline in battery prices translates to more affordable EVs, spurring adoption and expanding the market share for electric vehicles. Such heightened demand not only signals increased consumption of battery components, especially electrolytes but also propels technological advancements aimed at enhancing battery performance.

- Additionally, Germany is actively working to bridge supply chain gaps, aiming to lessen its dependence on imported materials for lithium-ion batteries, including cathodes, anodes, and electrolytes. With ambitious investment plans on the horizon for both EV battery manufacturing and lithium production, a pronounced demand for lithium-ion battery components, particularly electrolytes, is anticipated.

- For instance, in May 2024, Rock Tech Lithium Inc. secured approval to set up a lithium refinery in Guben, Germany. This refinery is projected to boast a capacity of approximately 24,000 tonnes of lithium-hydroxide, a crucial ingredient for electric car batteries and energy storage systems.

- In another move, February 2024 saw Automotive Cells Company (ACC) amass USD 4.7 billion in funding to establish three lithium-ion battery gigafactories spread across France, Germany, and Italy. ACC projects that by 2030, its production will exceed 2 million lithium-ion batteries. Such strategic investments are poised to amplify the demand for lithium-ion battery electrolytes in the coming years.

- Given these dynamics, the lithium-ion battery electrolyte segment is set for a significant upswing in the forecast period.

Investments Towards Battery Manufacturing is Expected to Drive the Market

- Germany, home to automotive titans like Volkswagen, BMW, and Daimler (Mercedes-Benz), is witnessing these giants make substantial strides in electric vehicle (EV) development. With plans to electrify a significant portion of their fleets, these manufacturers are fueling a burgeoning demand for EV batteries and their essential electrolytes.

- To bolster investments in the EV sector, the German government has rolled out a suite of incentives and subsidies. As electric vehicle sales continue to rise, it's anticipated that the government will unveil additional policies to further bolster domestic battery manufacturing. Data from the International Energy Agency highlights this trend: in 2023, Germany's battery electric vehicle (BEV) sales reached 0.52 million units, a notable increase from 0.47 million in 2022.

- In tandem, several battery manufacturers are forging partnerships in Germany, aiming to produce EV batteries that are not only more efficient but also enhance overall performance. At the heart of these advancements are advanced battery electrolyte formulations. These cutting-edge formulations not only extend battery life and safety but also elevate energy density, marking them as key players in the industry's future innovations.

- Highlighting the collaborative spirit, in May 2024, VARTA, a prominent battery manufacturer, spearheaded a consortium of 15 companies and universities. This alliance, centered around the project ENTISE, is dedicated to crafting high-performance, eco-friendly cells for industrial applications, harnessing the potential of sodium-ion technology. With a financial backing of approximately EUR 7.5 million in grants from Germany's Federal Ministry of Research and Education, the consortium aims to wrap up the project's final phase by mid-2027.

- As the industry pivots towards solid-state batteries, heralded for their superior energy density and safety, there's an anticipation of a shift in electrolyte requirements. Recent years have seen a flurry of agreements among companies, underscoring the industry's commitment to meeting the surging demand for solid-state batteries in the automotive realm.

- For instance, in July 2024, Volkswagen Group's battery arm, Powerco, inked a deal with QuantumScape to bring QuantumScape's pioneering solid-state lithium-metal battery technology to the industrial forefront. Such collaborations not only signal a rising demand for solid-state batteries but also underscore the need for a consistent supply of electrolytes in EV battery production.

- Given these developments and the influx of funding, the anticipated investments aimed at bolstering EV battery production capacity are set to invigorate the market.

Germany Electric Vehicle Battery Electrolyte Industry Overview

The Germany electric vehicle battery electrolyte market is moderate. Some of the major players in the market (in no particular order) include Evonik Industries AG, BASF SE, Solvay SA, Umicore SA, and Mitsubishi Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Supportive Government Policies and Investments Towards Battery Manufacturing

- 4.5.2 Restraints

- 4.5.2.1 The Dependence on Other Countries for Key Raw Materials Used in the Production of Electrolytes

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Evonik Industries AG

- 6.3.2 BASF SE

- 6.3.3 Solvay SA

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Umicore SA

- 6.3.6 Targray Industries Inc.

- 6.3.7 3M Company

- 6.3.8 NEI Corporation

- 6.3.9 Cabot Corporation

- 6.3.10 Samsung SDI

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Innovation in Electrolyte Formulations