|

시장보고서

상품코드

1636538

전기자동차 배터리 제조 장비 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

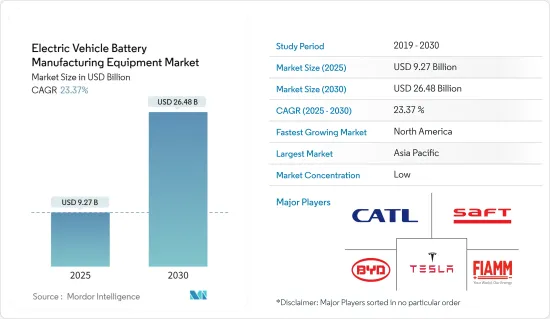

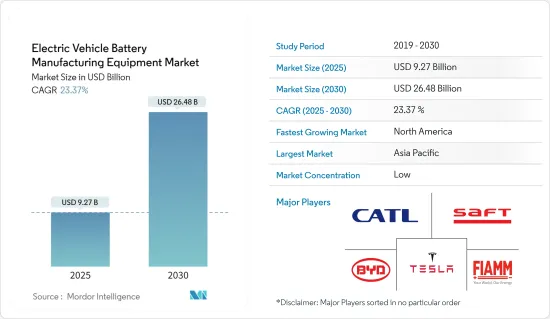

전기자동차 배터리 제조 장비 시장 규모는 2025년에 92억 7,000만 달러로 추정되고, 예측기간(2025-2030년)의 CAGR은 23.37%로 전망되며, 2030년에는 264억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 장기적으로는 전기자동차의 보급과 원료 배터리 재료의 비용 저하가 시장을 견인할 것으로 예상됩니다.

- 한편, 내연기관 자동차에 대한 장기적인 의존은 전기자동차로의 급속한 전환을 방해하고 시장 성장을 억제할 수 있습니다.

- 그러나, 고용량화와 저방전율화의 기술 진보가 진행됨으로써, 배터리 장비의 실현성과 효율성이 높아져, 전기자동차 배터리 제조 장비 시장에 거대한 기회가 생길 것으로 예상됩니다.

- 아시아태평양은 시장을 독점하고 있으며, 그 성장은 인도, 중국, 호주 등 국가에서의 투자 증가와 정부 정책의 촉진으로 이어지고 있습니다.

전기자동차 배터리 제조 장비 시장 동향

시장을 독점하는 전기차의 급속한 보급

- 가솔린과 천연가스의 비용 변동이 치열해지고, 각국에서 배기가스 규제의 요구가 높아지고 있기 때문에 종래의 자동차로부터 전기자동차(EV)로 주목이 옮겨지고 있습니다. 전기자동차는 효율이 높고 전기 요금이 싸기 때문에 가솔린과 디젤을 가득 채워 이동하는 것보다 전기자동차를 충전하는 것이 저렴하게 됩니다. 신재생 에너지를 사용하면 전기자동차가 보다 친환경적입니다.

- 게다가, 전기자동차 수요가 증가함에 따라, 자동차 제조업체는 각 자동차 부문에 대해 다양한 유형과 디자인의 전기자동차를 설계하고 판매량을 늘리고 있습니다. 이러한 자동차 설계의 커스터마이징은 자동차 제조업체 수요를 충족하는 배터리 제조에 큰 성장 기회를 제공합니다.

- 2023년 10월 BMW는 뮌헨 근처에 새로운 배터리 셀 파일럿 공장을 설립하여 '로컬 포 로컬' 배터리 공급망 및 생산 전략을 실현했습니다. BMW 셀 제조 역량 센터(CMCC)는 원통형 셀을 제조할 예정이며, 이로써 회사의 배터리 생산과 공급의 효율, 품질, 안정성이 높아질 것으로 기대되고 있습니다.

- 최근 전기자동차 유입은 예측 기간 동안 배터리 제조 장비 수요를 촉진할 것으로 예상됩니다. 국제에너지기구(IEA)에 따르면 2023년 세계 전기차의 총 판매량은 1,380만 대로 전년 1,020만 대에서 증가했습니다.

- 2030년까지 여러 국가가 전기차 점유율을 확대하기로 결정했습니다. 예를 들어 중국 등은 2030년까지 판매되는 자동차의 40%를 전기차로 만드는 것을 목표로 하고 있습니다. EV 인구 증가에 따라 배터리 수요도 크게 늘어날 것으로 예상됩니다. 국제에너지기구(IEA)에 따르면 2035년까지 EV용 배터리 수요는 2023년 대비 7배 증가할 것으로 예상됩니다.

- 이러한 시나리오를 고려하면 자동차 산업은 예측 기간 동안 가장 급성장하는 부문이 될 전망입니다.

아시아태평양은 시장의 현저한 성장이 기대

- 아시아태평양에서는 환경 문제 및 악화의 일환을 따르는 상황을 개선하는 기술에 대한 사람들의 의식이 높아지면서 전기자동차 배터리 제조 장비 시장이 지속적으로 상승하고 있습니다. 아시아태평양은 인구가 많고 경제가 급성장하고 있기 때문에 중국, 인도, ASEAN 국가 등의 국가가 시장을 견인하고 있으며, 아시아태평양의 배터리 수요는 꾸준히 성장할 것으로 예상됩니다.

- 중국은 전기자동차 산업이 활발하고 공급망 전체에서 업계를 선도하는 기업이 존재하고 경제가 급성장하고 있기 때문에 배터리 제조 장비 시장을 독점하고 있습니다. 이 지역은 세계의 리튬 이온 매장량의 대부분을 차지합니다. 국제에너지기구의 발표에 따르면 2023년 중국의 전기자동차 판매량은 전년 590만 대에서 약 810만 대로 증가했습니다. 이것은 아시아태평양에서 가장 높습니다.

- 아시아태평양에서 전기자동차 배터리 제조 기가팩터의 성장은 향후 몇 년동안 제조 장비 시장을 밀어 올 것으로 예상됩니다. 예를 들어, 2023년 1월, 리차지 인더스트리즈는 2024년까지 연간 2GWh, 2026년까지 6GWh의 전기자동차 배터리를 호주 질롱 지역에 건설한다고 발표했습니다. 3억 달러 상당의 이 거대 공장은 이 나라의 전기배터리 공급 밸류 체인을 개선할 것으로 기대되고 있습니다.

- 전기차 개발을 촉진하는 정부의 목표와 이니셔티브는 아시아태평양 시장 성장을 더욱 촉진할 수 있습니다. 예를 들어 인도에서는 2030년까지 전기자동차(EV)가 자가용차 판매의 30%, 상용차 판매의 70%, 이륜차 및 삼륜차 판매의 80%를 차지하는 것을 정부는 목표로 하고 있습니다.

- 따라서 아시아태평양은 전기자동차 배터리 제조 장비 시장에서의 생산 증가, 기술 진보, 정부 지원 정책 등으로 예측 기간 동안 시장을 독점할 것으로 예상됩니다.

전기자동차 배터리 제조 장비 산업 개요

전기자동차 배터리 제조 장비 시장은 단편화되어 있으며 여러 기업이 존재합니다. 주요 기업(순부동)에는 NEC, Duerr AG, Hitachi Ltd, Schuler AG, Buhler Holding AG 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 시장 규모 및 수요 예측(단위 : 달러)(-2029년)

- 최근 동향 및 개발

- 정부의 규제 및 정책

- 시장 역학

- 성장 촉진요인

- 전기자동차의 보급 확대

- 전지 원재료 비용의 저하

- 억제요인

- 내연 기관 자동차에 장기 의존

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 세분화

- 프로세스별

- 혼합

- 코팅

- 캘린더

- 슬릿 및 전극 가공

- 기타 프로세스

- 배터리별

- 리튬 이온

- 납축전지

- 니켈 수소 배터리

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 영국

- 스페인

- 북유럽 국가

- 터키

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 이집트

- 나이지리아

- 카타르

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 인수합병(M&A), 합작사업, 제휴 및 협정

- 주요 기업의 전략

- 기업 프로파일

- NEC Corporation

- Duerr AG

- Hitachi Ltd

- Schuler AG

- Buhler Holding AG

- Manz AG

- Sovema Group SpA

- Komatsu NTC Ltd

- KROENERT GmbH & Co. KG.

- List of Other Prominent Companies

- 시장 랭킹 분석

제7장 시장 기회 및 향후 동향

- 다양한 기술에서의 기술 진보 증가

The Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 9.27 billion in 2025, and is expected to reach USD 26.48 billion by 2030, at a CAGR of 23.37% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the increasing adoption of electric vehicles and the decline in the cost of raw battery materials are expected to drive the market.

- On the other hand, the long-term dependency on internal combustion engine vehicles could hinder the rapid transition to electric vehicles, which may restrain the growth of the market.

- However, the growing technological advancements in higher capacity and low discharge rates are expected to make battery equipment more feasible and efficient and create enormous opportunities for the electric vehicle battery manufacturing equipment market.

- Asia-Pacific dominates the market, and its growth will be linked to rising investments and conducive government policies in countries such as India, China, and Australia.

Electric Vehicle Battery Manufacturing Equipment Market Trends

Rapid Adoption of Electric Vehicles to Dominate the Market

- The increasing cost fluctuations of gasoline and natural gas and the growing demand for emission controls in various countries have shifted the focus from conventional vehicles to electric vehicles (EVs). Electric vehicles are more efficient, which, combined with the lower cost of electricity, makes charging an electric vehicle cheaper than filling up with petrol or diesel for your travel needs. Using renewable energy sources can make electric vehicles more eco-friendly.

- Moreover, as the demand for electric vehicles increases, automobile manufacturing companies are designing electric vehicles for all car segments in various types and designs to increase their sales. This customization in automobile design provides a significant growth opportunity for battery manufacturing to meet automobile manufacturers' demands.

- In October 2023, BMW established its new battery cell pilot plant near Munich to fulfill its 'local for local' battery supply chain and production strategy. BMW Cell Manufacturing Competence Center (CMCC) will manufacture cylindrical cells, which is expected to boost the company's efficiency, quality, and stability in battery production and supply.

- The influx of electric vehicles in recent years is expected to propel the demand for battery manufacturing equipment during the forecast period. According to the International Energy Agency (IEA), the total sales of electric vehicles worldwide were 13.8 million in 2023, an increase from 10.2 million the previous year.

- By 2030, several countries have decided to increase the share of electric vehicles. For instance, countries like China aim to have 40% of vehicles sold by 2030 to be electric. With the growth in the EV population, battery demand is expected to witness significant growth. According to the International Energy Agency, by 2035, EV battery demand is expected to increase by seven times compared to 2023.

- Considering such a scenario, the automotive industry is expected to be the fastest-growing segment during the forecast period.

Asia-Pacific is Expected to Witness Significant Growth in the Market

- The electric vehicle battery manufacturing equipment market is constantly rising in Asia-Pacific due to the rising public awareness of environmental issues and techniques to improve constantly deteriorating conditions. Due to the region's large population and fast-growing economy, the demand for batteries in Asia-Pacific is expected to grow steadily, with countries such as China, India, and the ASEAN countries driving the market.

- China dominates the battery manufacturing equipment market with a significant electric car industry, leading industry players across the supply chain, and a rapidly rising economy. The region has the majority of the world's lithium-ion reserves. As per the International Energy Agency, the sales of electric cars in China in 2023 were about 8.1 million, from 5.9 million in the previous year. This appeared to be the highest in Asia-Pacific.

- The growth of electric vehicle battery manufacturing gigafactors in Asia-Pacific is expected to push its manufacturing equipment market in the coming years. For instance, in January 2023, the Recharge Industries firm noted that it would construct close to 2 GWh of annual electric vehicle battery production by 2024 and 6 GWh by 2026 in Australia's Geelong region. The gigagactory worth USD 300 million is expected to improve the country's electric battery supply-value chain.

- Government targets and initiatives to expedite the development of electric vehicles could further drive market growth in Asia-Pacific. For instance, in India, by 2030, the government aims for electric vehicles (EVs) to make up 30% of private car sales, 70% of commercial vehicle sales, and 80% of sales of two- and three-wheelers.

- Hence, Asia-Pacific is expected to dominate the market during the forecast period due to increased production, technological advancements, and supportive government policies in the electric vehicle battery equipment manufacturing market.

Electric Vehicle Battery Manufacturing Equipment Industry Overview

The electric vehicle battery manufacturing equipment market is fragmented, with several players. Some of the major players (not in particular order) include NEC Corporation, Duerr AG, Hitachi Ltd, Schuler AG, and Buhler Holding AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing adoption of electric vehicles

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Long-term dependency on internal combustion engine vehicles

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendering

- 5.1.4 Slitting and electrode making

- 5.1.5 Other Processes

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Spain

- 5.3.2.3 NORDIC Countries

- 5.3.2.4 Turkey

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Thailand

- 5.3.3.5 Indonesia

- 5.3.3.6 Vietnam

- 5.3.3.7 South Korea

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 NEC Corporation

- 6.3.2 Duerr AG

- 6.3.3 Hitachi Ltd

- 6.3.4 Schuler AG

- 6.3.5 Buhler Holding AG

- 6.3.6 Manz AG

- 6.3.7 Sovema Group S.p.A

- 6.3.8 Komatsu NTC Ltd

- 6.3.9 KROENERT GmbH & Co. KG.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing technological advancements in various technologies