|

시장보고서

상품코드

1636563

유럽의 전기자동차(EV) 충전 설비 시장 전망 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

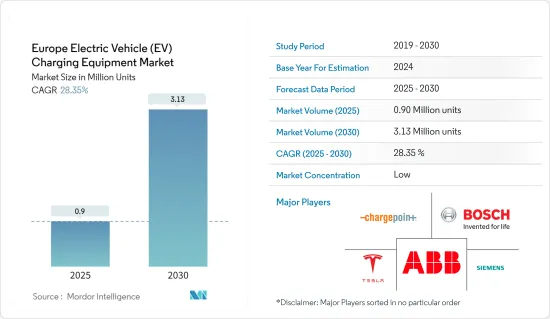

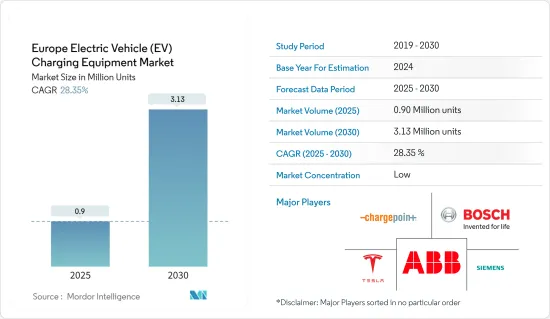

유럽의 전기자동차 충전 설비 시장 규모는 2025년 90만대로 추정되며 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 28.35%를 나타낼 전망이며, 2030년에는 313만대에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 전기차의 보급 확대나 정부의 정책적 노력, EV충전 인프라 강화에 대한 대처 등의 요인이 예측기간 중 EV충전 기기 시장을 주도할 것으로 예측됩니다.

- 반대로 충전소 설치와 관련된 설치 비용과 유지 보수 비용이 높아 예측 기간 동안 시장 성장을 방해할 수 있습니다.

- 그러나 급성장하는 유럽 시장의 종합적인 EV 충전 설비에 대한 수요는 EV 충전 장비의 기술적 발전와과 함께 예측 기간 동안 유럽 EV 충전 설비 시장에 큰 기회를 가져다줍니다.

- 전기자동차의 보급을 촉진하는 적극적인 정책적 지원을 가진 독일은 유럽에서 주목할만한 성장을 이룰 전망입니다.

유럽의 전기자동차(EV) 충전 설비 시장 동향

배터리 전기자동차 부문이 시장을 독점

- 일반적으로 전기자동차로 알려진 배터리 전기자동차(BEV)는 전기 모터에 전력을 공급하기 위해 큰 배터리 팩을 사용합니다. 충전을 위해 이러한 차량은 전기자동차 공급 설비(EVSE)에 연결됩니다.

- 완전한 전기자동차인 BEV는 보통 내연 기관(ICE), 연료 탱크, 배기관이 없습니다. 그리드로 충전된 배터리 팩에서 에너지를 얻고 있습니다. 무공해 차량인 BEV는 기존 가솔린 차량에서 발행하는 유해한 가스를 배출하지 않으므로 대기 오염을 줄일 수 있습니다.

- 유럽의 자동차 산업은 큰 전환기를 맞이하고 있으며 배터리 전기자동차(BEV)의 인기가 높아지고 있습니다. 기술의 발전, 정부의 주도, 환경 인식 증가에 힘입어, BEV는 기후 변화와 싸우고 화석 연료에 대한 의존을 줄이기 위한 실행 가능한 솔루션으로 부상하고 있습니다.

- 국제에너지기구(IEA)의 데이터에 따르면 EU에서의 BEV 판매 대수는 2023년에 약 160만대에 달하고, 2022년 120만대에서 33% 증가했습니다. 또한 EU의 BEV 총 재고량은 약 460만 대까지 증가하고 있습니다. BEV 판매량이 급증함에 따라 유럽에서는 충전 인프라 수요가 높아지고 있습니다.

- 또한 일부 유럽 정부는 향후 몇 년동안 EV의 보급을 촉진하는 전략을 세웠습니다. 예를 들어, 프랑스 정부는 2024년 5월 자국 자동차 제조업체들에게 10년 후까지 200만대의 전기자동차 또는 하이브리드 자동차를 생산하는 야심찬 목표를 세웠습니다. 정부와의 새로운 중기 협정의 일환으로 자동차 산업은 2027년까지 80만대의 전기자동차 판매라는 중간 목표를 목표로 하고 있으며, 이는 2022년 20만대에서 크게 급증했습니다. 또한 자동차 제조업체는 전기자동차(EV)의 연간 판매량을 2022년 1만 6,500대에서 10만대로 끌어올리는 것을 목표로 하고 있습니다. 이러한 야심적인 목표는 이 지역에서 EV 충전 장치 수요를 크게 증가시키는 것입니다.

- 유럽자동차공업회(ACEA)에 따르면 EU에서는 2023년에 약 15만 곳(주 평균 3,000 곳 이하)의 공공 충전소가 설치되어 총 63만 곳 이상이 될 전망입니다. 이에 대해 유럽위원회는 2030년까지 약 350만 곳의 충전소를 설립을 목표로 내걸고 있습니다. 이를 달성하기 위해서는 연간 약 41만 곳(매주 약 8,000 곳)의 공공 충전소를 설치해야 합니다.

- 반대로 ACEA는 2030년까지 880만 곳의 충전소가 필요할 것으로 예측했습니다. 이 수요를 충족시키기 위해서는 현재의 8배에 해당하는 연간 120만대(매주 2만2,000대 이상)의 충전 설비의 설치가 필요합니다. 이러한 야심찬 목표는 유럽에서 BEV 시장의 성장과 이에 따른 EV 충전 설비에 대한 수요의 급증을 강조합니다.

- 최근 중국의 유명한 자동차 제조업체 여러 회사가 유럽에서 제조 및 조립 공장을 설립하는 데 관심을 보이고 있으며 경쟁력 있는 가격의 자동차 판매를 확대하고 유럽 자동차 제조업체에 대항하는 것을 목표로하고 있습니다. 예를 들어, Chery Auto는 2024년 4월 스페인의 EV 모터스(EV Motors)와의 합작으로 카탈루냐 지방에 유럽 최초의 생산 시설을 설립한다고 발표했으며, 또한 지난 10년간 영국에 자동차 공장을 건설할 가능성에 대해서도 협의가 진행되고 있습니다.

- 2023년 세계 유수의 EV 제조업체인 BYD는 헝가리에 최초의 유럽 생산 거점을 건설하고 3년 후 조업을 시작할 계획을 발표했습니다. 이 발전은 유럽 시장을 지원하며 배터리 EV와 플러그인 하이브리드를 모두 생산할 것입니다. 이러한 개발은 BEV 제조 섹터를 강화하고 EV 충전 인프라에 대한 수요를 높일 것으로 예상됩니다.

- 이러한 움직임 속에서 BEV 부문은 향후 몇 년동안 유럽의 EV 충전 설비 시장을 선도해 나갈 것으로 예상됩니다.

현저한 성장을 이루는 독일

- 독일은 전기자동차(EV) 장비와 인프라를 급속히 확대하고 있으며 EV 산업에 대한 국가의 노력이 가속되고 있음을 보여주고 있습니다. 국제에너지기구(IEA)에 따르면 2023년 말까지 독일은 약 10만 8,000개소의 EV 충전소를 공개적으로 이용할 수 있게 한다고 합니다. 그 집계는 급속 충전 설비가 약 2만 1,000기, 저속 충전 설비가 약 8만 7,000기입니다. 특히 2023년에는 1만 6,000개 이상의 저속 충전소와 6,000개 급속 충전소가 추가되었습니다.

- 독일 정부는 2030년 말까지 전국에 100만 곳의 공공 충전 포인트를 설치하는 것을 목표로 하는 야심찬 계획을 가지고 있습니다. 그러나 2023년 후반 시점에서 이 목표의 약 11%만 달성되었습니다. 이 차이을 해소하기 위해 공공 EV 충전소의 대폭적인 증가가 향후 몇 년동안 예상되어 EV 충전 장비 시장의 급성장을 시사하고 있습니다.

- 정부는 공공 공간에서 주택 및 상업시설에 이르기까지 다양한 장소에서 EV 충전 설비의 설치를 적극적으로 승인하고 있습니다. 이 노력은 도로를 달리는 전기자동차 증가에 대응하고 EV 충전 장비 수요를 촉진하고 있습니다. EV 충전 인프라의 확대는 독일에 있어서 매우 중요하며, 주행거리에 대한 불안을 해소하고 접근성을 향상시킴으로써, 보다 많은 소비자의 전기차로의 전환을 촉진하는 것을 목적으로 하고 있습니다.

- 2024년 2월 유럽의 유명한 EV 충전 회사인 Fastned는 독일 고속도로를 따라 34개의 급속 충전소를 설치할 수 있는 인가를 받았습니다. 도이츄란트 네츠입찰의 일환인 이 노력은 EV 충전 인프라 강화에 대한 독일의 노력을 보여줍니다. Fastned는 2030년까지 유럽 전역에 1,000곳의 급속 충전소을 설치하는 야심찬 목표를 향해 전진하고 있습니다.

- 독일에서는 EV 인프라를 강화하고 급증하는 충전 설비 수요에 대응하기 위한 전략으로 자사에서 EV 충전 허브를 설치하는 기업이 늘고 있습니다. 이러한 허브는 EV의 보급을 촉진할 뿐만 아니라 이산화탄소 배출을 억제하고 지속가능한 운송 솔루션을 지지하는 역할을 담당하고 있습니다.

- 2023년 11월, Mercedes-Benz는 독일 맨하임에 최초의 자체 제조 충전 허브를 개설했습니다. 이 사업은 10년 후까지 2,000개 이상의 충전소을 설치하고 10,000개 이상의 급속 충전소를 설치하는 Mercedes-Benz의 세계 목표에 부합합니다.

- 독일은 또한 지속 가능한 운송에 대한 헌신을 강화하기 위해 주유소에서 EV 충전 설비 설치를 추진하고 있습니다. 이 의무화는 청정 에너지 차량을 홍보할 뿐만 아니라 보다 광범위한 기후 변화 문제를 다루고 있습니다.

- 2023년 9월 독일 올라프 숄츠 총리는 총 주유소의 80%에 최소 150킬로와트의 급속 충전 옵션을 제공해야 한다는 법을 제정할 것이라고 발표했습니다.

- 이러한 개발 상황을 감안할 때 독일 전기차(EV) 충전 설비 시장은 EV 보급률 상승, 왕성한 투자, 정부의 지원 시책과 목표에 힘입어 큰 성장이 예상됩니다.

유럽의 전기자동차(EV) 충전 설비 산업 개요

유럽의 전기자동차(EV) 충전 장비 시장은 절반으로 단절되었습니다. 이 시장의 주요 기업(무순서)에는 ABB Ltd, Robert Bosch GmbH, ChargePoint Inc., Siemens AG, Tesla Inc. 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위 : 대)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 전기차의 보급과 관련 투자 확대

- 정부의 이니셔티브에 뒷받침된 EV충전 인프라 증강에의 대처

- 억제요인

- 충전소 설치에 따른 높은 설치 비용과 유지 보수 비용

- 성장 촉진요인

- 공급망 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협 제품 및 서비스

- 경쟁 기업간 경쟁 관계

- 투자 분석

제5장 시장 세분화

- 차종

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 자동차(PHEV)

- 하이브리드 전기자동차(HEV)

- 신청

- 가정용 충전

- 직장 충전

- 공공 충전

- 충전 유형

- AC 충전(레벨 1 및 레벨 2)

- DC충전

- 지역

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- ABB Ltd

- Robert Bosch GmbH

- Delta Electronics Inc.

- Siemens AG

- Tesla Inc.

- ChargePoint Inc.

- Enphase Energy, Inc.

- Powercharge

- Ampure

- Exicom Tele-Systems Ltd

- Schneider Electric SE

- Eaton Corporation

- 기타 저명한 기업 일람

- 시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

- EV충전 장비의 기술 발전

- 신흥 유럽 시장에서 견고한 EV 충전 네트워크의 필요성

The Europe Electric Vehicle Charging Equipment Market size is estimated at 0.90 million units in 2025, and is expected to reach 3.13 million units by 2030, at a CAGR of 28.35% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing adoption of electric vehicles and the efforts to enhance EV charging infrastructure supported by government initiatives are expected to drive the EV charging equipment market during the forecast period.

- Conversely, the market's growth during the forecast period may be stunted by the high installation and maintenance costs tied to setting up charging stations.

- However, the burgeoning European markets' demand for a comprehensive EV charging network, coupled with technological strides in EV charging equipment, presents substantial opportunities for the Europe EV charging equipment market during the forecast period.

- Germany, with its proactive initiatives promoting electric vehicle adoption, is poised for notable growth in the European landscape.

Europe Electric Vehicle (EV) Charging Equipment Market Trends

Battery Electric Vehicles Segment to Dominate the Market

- Battery electric vehicles (BEVs), commonly known as electric vehicles, utilize a sizable traction battery pack to power their electric motors. To recharge, these vehicles connect to electric vehicle supply equipment (EVSE).

- BEVs, being entirely electric, typically lack an internal combustion engine (ICE), fuel tank, or exhaust pipe. They derive their energy from a grid-recharged battery pack. As zero-emission vehicles, BEVs do not produce the harmful tailpipe emissions associated with traditional gasoline-powered cars, thus mitigating air pollution.

- Europe's automotive industry is undergoing a significant shift, with battery electric vehicles (BEVs) gaining traction and popularity. Driven by technological advancements, governmental backing, and heightened environmental awareness, BEVs are emerging as a viable solution to combat climate change and lessen dependence on fossil fuels.

- Data from the International Energy Agency (IEA) reveals that BEV sales in the European Union reached approximately 1.6 million units in 2023, marking a 33% increase from 1.2 million units in 2022. Furthermore, the total BEV stock in the EU has climbed to around 4.6 million units. As BEV sales surge, the demand for charging infrastructure in Europe intensifies.

- Moreover, several European governments are strategizing to amplify EV adoption in the upcoming years. For instance, in May 2024, the French government set an ambitious target for its automakers: to produce two million electric or hybrid vehicles by the decade's end. As part of a new medium-term agreement with the government, the industry aims for an interim target of 800,000 electric vehicle sales by 2027, a significant jump from 200,000 in 2022. Additionally, carmakers are setting their sights on boosting electric light utility vehicle sales to 100,000 annually, up from 16,500 in 2022. Such ambitious goals are poised to drive a substantial demand for EV charging equipment in the region.

- According to the European Automobile Manufacturers' Association (ACEA), the EU saw the installation of only about 150,000 public charging points in 2023 (averaging less than 3,000 weekly), bringing the total to over 630,000. In contrast, the European Commission aims for a target of around 3.5 million charging points by 2030. Achieving this would necessitate an installation rate of approximately 410,000 public charging points annually (or nearly 8,000 weekly), nearly three times the current rate.

- Conversely, ACEA projects a need for 8.8 million charging points by 2030. Meeting this demand would require an annual installation of 1.2 million chargers (or over 22,000 weekly), which is eight times the current rate. Such ambitious targets underscore the growing BEV market in Europe and the corresponding surge in demand for EV charging equipment.

- In recent years, several prominent Chinese automakers have expressed interest in establishing manufacturing and assembly plants in Europe, aiming to boost sales of competitively priced vehicles and challenge their European counterparts. For instance, in April 2024, Chery Auto, China's leading automaker by export volume, announced a joint venture with Spain's EV Motors to inaugurate its inaugural European manufacturing facility in Catalonia, with production slated to commence later in 2024. Furthermore, discussions are underway for potential car factories in Britain this decade.

- In 2023, BYD, the world's foremost EV manufacturer, declared plans for its maiden European production base in Hungary, set to commence operations in three years. This facility will cater to the European market, producing both battery EVs and plug-in hybrids. Such developments are anticipated to bolster the BEV manufacturing sector, subsequently amplifying the demand for a robust EV charging infrastructure.

- Given these dynamics, the BEV segment is poised to lead the European EV charging equipment market in the coming years.

Germany to Witness a Significant Growth

- Germany has been rapidly expanding its electric vehicle (EV) equipment and infrastructure, mirroring the nation's increasing embrace of the EV industry. According to the International Energy Agency (IEA), by the close of 2023, Germany boasted approximately 108,000 publicly available EV charging points. This tally comprised around 21,000 fast chargers and 87,000 slow chargers. Notably, in 2023, Germany added over 16,000 public slow charging points and 6,000 public fast charging points.

- The German government has ambitious plans, targeting the installation of 1 million public charging points nationwide by the end of 2030. Yet, as of late 2023, only about 11% of this target has been met. To bridge this gap, a substantial increase in public EV charging points is anticipated in the coming years, signaling a burgeoning market for EV charging equipment.

- The government is actively approving EV charging installations in diverse locales, from public spaces to residential and commercial properties. This initiative has spurred demand for EV charging equipment, catering to the rising number of electric vehicles on the roads. Expanding the EV charging infrastructure is pivotal for Germany, as it aims to alleviate range anxiety and enhance accessibility, thereby encouraging more consumers to transition to electric vehicles.

- In February 2024, Fastned, a prominent European EV charging firm, received approval to establish 34 fast-charging sites along Germany's highways. This initiative, part of the "Deutschlandnetz" tender, underscores Germany's commitment to bolstering its EV charging infrastructure. Fastned's move is a stride towards its ambitious goal of 1,000 fast charging stations across Europe by 2030.

- Companies in Germany are increasingly setting up their own EV charging hubs, a strategy to bolster the nation's EV infrastructure and cater to the surging demand for charging equipment. These hubs not only promote EV adoption but also play a role in curbing carbon emissions and championing sustainable transport solutions.

- In November 2023, Mercedes-Benz inaugurated its inaugural proprietary charging hub in Mannheim, Germany. This venture aligns with the company's global ambition of establishing over 2,000 charging stations by decade's end, featuring upwards of 10,000 fast-charging points.

- Germany is also pushing for EV chargers at gas stations, reinforcing its commitment to sustainable transport. This mandate not only promotes clean energy vehicles but also addresses broader climate change challenges.

- In September 2023, German Chancellor Olaf Scholz announced a forthcoming law stipulating that 80% of all service stations must offer fast-charging options, with a minimum capacity of 150 kilowatts.

- Given these developments, the EV charging equipment market in Germany is poised for significant growth, buoyed by rising EV adoption, robust investments, and supportive government policies and targets.

Europe Electric Vehicle (EV) Charging Equipment Industry Overview

The Europe electric vehicle (EV) charging equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include ABB Ltd, Robert Bosch GmbH, ChargePoint Inc., Siemens AG, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in Units, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles and Related Investments

- 4.5.1.2 Efforts to Boost EV Charging Infrastructure Supported by Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Installation Costs Associated With Setting Up Charging Stations And Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Battery Electric Vehicle (BEV)

- 5.1.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.1.3 Hybrid Electric Vehicle (HEV)

- 5.2 Application

- 5.2.1 Home Charging

- 5.2.2 Workplace Charging

- 5.2.3 Public Charging

- 5.3 Charging Type

- 5.3.1 AC Charging (Level 1 and Level 2)

- 5.3.2 DC Charging

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Nordic

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Robert Bosch GmbH

- 6.3.3 Delta Electronics Inc.

- 6.3.4 Siemens AG

- 6.3.5 Tesla Inc.

- 6.3.6 ChargePoint Inc.

- 6.3.7 Enphase Energy, Inc.

- 6.3.8 Powercharge

- 6.3.9 Ampure

- 6.3.10 Exicom Tele-Systems Ltd

- 6.3.11 Schneider Electric SE

- 6.3.12 Eaton Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technology Advancement in the EV Charging Equipment

- 7.2 Need for a Robust EV Charging Network in the Emerging European Markets