|

시장보고서

상품코드

1636595

오브젝트 스토리지 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Object-Based Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

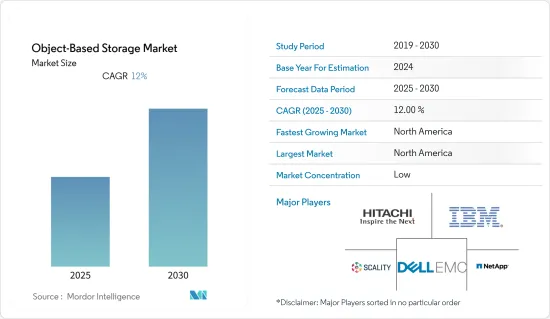

오브젝트 스토리지 시장은 예측 기간 동안 CAGR 12%를 기록할 전망입니다.

데이터를 파일 계층으로 관리하는 파일 시스템과 데이터를 섹터 및 트랙의 블록으로 관리하는 블록 스토리지와 같은 기존 스토리지 아키텍처와는 대조적으로 오브젝트 스토리지는 데이터를 오브젝트로 관리하는 컴퓨터 데이터 스토리지의 한 유형입니다.

주요 하이라이트

- 스토리지 시장은 데이터의 급격한 증가, 비즈니스의 급속한 디지털화 및 세계화, 모든 연결 및 수집 요구 사항 등 기업 IT의 새로운 과제를 해결하기 위해 진화하고 있습니다. 오브젝트 스토리지를 기반으로 하는 스토리지 인프라 시스템은 도입 수와 용량 모두 크게 증가하고 있으며 기업 데이터센터에서 비정형 데이터 증가에 대응하는 플랫폼으로 선택되고 있습니다.

- 신흥 및 기존 워크로드의 비정형 데이터를 빠르게 성장시키기 위해서는 수십 페타바이트의 스토리지를 제공할 수 있고 퍼블릭 클라우드 IaaS와의 하이브리드 클라우드 워크플로우를 활용할 수 있는 인프라 Software-Defined Storage가 추진하는 제품이 필요합니다. 새로운 구형 스토리지 회사는 기존의 스케일 업 스토리지 환경에서 비용, 민첩성 및 확장성 한계를 해결하기 위해 확장 가능한 오브젝트 스토리지 제품을 개발했습니다.

- 대부분의 조직은 파일 스토리지, 블록 스토리지, 오브젝트 스토리지와 같은 스토리지 유형을 결합하여 사용합니다. 그러나 속도, 확장성, 검색성, 보안, 데이터 무결성, 안정성 등의 이유로 오브젝트 스토리지의 사용이 급증하고 있습니다.

- 오브젝트 스토리지는 엄청난 양의 데이터를 집계하고 데이터 저장소에 필수적인 애플리케이션을 계층화하고 혁신을 촉진하는 고급 데이터 분석을 통해 랜섬웨어 공격으로부터 보호하려는 조직에 다양한 이점을 제공합니다.

- 오브젝트 스토리지 시장에 진입하는 일부 기업은 고객에게 인프라 구축 방법을 선택할 수 있도록 다양한 전개 옵션을 제공합니다. 표준 전개 옵션에는 턴키 고밀도 어플라이언스와 베어 메탈 업계 표준 하드웨어에 가상 머신 및 Docker 컨테이너로 전개하는 소프트웨어 전용 옵션이 있습니다. 이 시장의 기업은 x86 업계 표준 하드웨어에서 작동하도록 사전 인증된 소프트웨어 정의 스토리지로 제품을 제공하기 시작했습니다.

오브젝트 스토리지 시장 동향

클라우드 기반 배포가 시장 점유율을 독점

- 신흥 및 기존 워크로드의 비정형화된 데이터가 급속히 성장함에 따라 수십 페타바이트의 스토리지를 제공하고 퍼블릭 클라우드 IaaS와의 하이브리드 클라우드 워크플로우를 활용할 수 있는 인프라 소프트웨어 정의 스토리지를 통한 제품이 필요합니다. 새로운 구형 스토리지 회사는 기존의 스케일 업 스토리지 환경에서 비용, 민첩성 및 확장성 한계를 해결하기 위해 확장 가능한 오브젝트 스토리지 제품을 개발했습니다.

- 현재 비구조화된 스토리지 시장은 IT 리더들이 퍼블릭 클라우드의 민첩성, 효율성, 클라우드 컴퓨팅 기능을 활용하려고 하기 때문에 하이브리드 클라우드의 워크플로우와 기능을 수용하도록 진화하고 있습니다. 오브젝트 스토리지 분야는 양면 시장으로 간주됩니다. 오브젝트 스토리지 영역 프로토콜 제공업체와 응용프로그램으로 구성된 이러한 프로토콜의 여러 소비자가 있습니다.

- Amazon S3 API가 오브젝트 스토리지의 사실상 표준이 될 때까지는 소비자보다 공급자가 많았습니다. 또한 엔터프라이즈 데이터센터에서 오브젝트 스토리지 플랫폼을 활용하는 회사는 Amazon S3를 채택했습니다. Amazon S3는 퍼블릭 클라우드에서 자주 사용되는 프로토콜이지만, 그 이유는 개발자 커뮤니티가 있기 때문입니다.

- 여러 제공업체와 소비자가 Amazon S3를 사용합니다. AWS와 같은 퍼블릭 클라우드 서비스를 활용함으로써 오브젝트 스토리지 시장에 큰 고객 의식이 생겼습니다. 모드 2 웹 및 모바일 애플리케이션을 개발하는 소프트웨어 개발자는 때때로 이러한 애플리케이션을 기업 데이터센터로 되돌려야 합니다. 엔터프라이즈 IT 부서는 데이터 및 애플리케이션 제어를 요구하고 소프트웨어 개발자는 인프라와 프로그래밍 방식으로 상호 작용하는 효율적인 방법을 찾고 있습니다.

- 오브젝트 스토리지는 다른 스토리지 옵션과 비교하여 데이터 공유와 일관성이 우수합니다. 블록 기반 및 파일 기반 데이터 스토리지에서 한 애플리케이션의 인스턴스가 다른 인스턴스가 생성한 부분 데이터를 볼 수 있습니다. 애플리케이션 개발자는 결국 이 문제를 피하기 위해 영구 잠금이 필요합니다. 그러나 이러한 계획에는 성능 및 정밀도 문제와 같은 고유한 문제가 있습니다.

북미가 큰 시장 성장을 차지합니다.

- 북미는 예측 기간을 통해 세계 시장을 확대할 것으로 예상됩니다. 이 지역의 클라우드 오브젝트 스토리지 시장은 해당 지역의 주요 기업 통합으로 검토 기간 동안 성장할 것으로 예상됩니다. 또한 이 지역에서는 대규모 데이터의 출입이 많기 때문에 대기업과 중소기업에 의한 클라우드 스토리지 서비스의 이용이 증가하고 있습니다.

- 시장 확대의 요인 중 하나는 인터넷 트래픽과 사용자 생성 컨텐츠 증가이며, 북미는 국제적으로 가장 많은 ip 트래픽이 발생하고 있습니다. 시스코는 이 지역의 iP 트래픽이 작년까지 연간 21% 증가한 108.4EB에 이를 것으로 예측했습니다.

- 또한 이 지역에는 IBM 및 Dell과 같은 오브젝트 스토리지의 유명 공급업체가 여러 개 있습니다. 이 요소는 이 지역에서 오브젝트 스토리지를 더 많이 사용하는 데 도움이 됩니다. 통합 파일 및 블록, SAN, NAS에 비해 오브젝트 스토리지는 더 많은 미국 기업이 구매할 것으로 보입니다. 4분의 1은 온프레미스 스토리지를 확장했으며 절반 가까이 클라우드 스토리지를 강화하고 있습니다.

- BFSI 업계는 비즈니스 전략의 변화로 서비스 적응과 혁신을 강요하고 있습니다. 세계 은행 서비스 제공업체가 클라우드 스토리지 솔루션을 도입하고 있습니다. 미국 은행 협회에 따르면 금융기관의 90% 이상이 은행 업무의 일부 또는 전부에 클라우드 기술을 활용하고 있습니다.

오브젝트 스토리지 산업 개요

오브젝트 스토리지 시장은 단편화되어 있어 꽤 경쟁이 치열하여 복수의 기업로 구성되어 있지만, 현재는 소수의 대형 기업이 시장을 독점하고 있습니다. 많은 기업들이 이 기술을 다루고 있는 이유는 다른 스토리지 옵션에 비해 많은 장점이 있기 때문입니다. 주요 기업으로는 Hitachi Vantara Corp., NetApp Inc., IBM Corporation(Red Hat), Scality Inc., Dell EMC 등이 있습니다. 최근의 동향으로서는 다음과 같은 것이 있습니다.

- 2022년 11월-Cloudian은 데이터 클라우드 제공업체인 Snowflake와 공동으로 온프레미스 데이터 레이크 스토리지 HyperStore를 발표했습니다. Cloudian 및 Snowflake 고객은 사설 클라우드 또는 하이브리드 클라우드 구성으로 온프레미스에 배포되어 HyperStore에 저장된 데이터에 액세스할 수 있습니다. HyperStore는 엔터프라이즈 데이터센터 내에 퍼블릭 클라우드의 규모와 단순성을 제공하여 성능 향상, 완벽한 보안 제어, 데이터 주권 및 저비용을 제공합니다. HyperStore는 S3을 완벽하게 준수하도록 처음부터 개발되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 업계의 매력도-Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 경쟁 기업간 경쟁 관계

- 시장 성장 촉진요인

- 오브젝트 기반 솔루션(특히 대규모 스토리지용)의 낮은 취득 비용

- 멀티클라우드 데이터 관리, ML 스토리지 분석 도입 등의 기술적 진보

- 시장의 과제

- 종래의 스토리지 관행으로부터의 변화에 대한 저항

- 파일 vs 블록 vs 오브젝트 기반 스토리지 비교 분석

- 오브젝트 스토리지의 주요 이용 사례-빅 데이터, 웹 앱, 백업 아카이브, 부정 방지 등

- COVID-19가 시장에 미치는 영향

제5장 시장 세분화

- 유형별

- 클라우드 기반

- 온프레미스

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제6장 경쟁 구도

- 기업 프로파일

- Hitachi Vantara Corp

- NetApp Inc.

- IBM Corporation(Red Hat)

- Scality Inc.

- Dell EMC

- Cloudian, Inc.

- Caringo Inc.

- StorageCraft Technology Corp

- WesternDigital Corp

- SwiftStack Inc.

- SUSE

- OpenIO(OVHcloud)

제7장 투자 분석

제8장 시장의 미래

AJY 25.02.12The Object-Based Storage Market is expected to register a CAGR of 12% during the forecast period.

In contrast to conventional storage architectures like file systems, which manage data as a file hierarchy, and block storage, which manages data as blocks inside sectors and tracks, object storage is a type of computer data storage that maintains data as objects.

Key Highlights

- The storage market is evolving to address new challenges in enterprise IT, such as exponential data growth, rapid digitalization and globalization of business, and requirements to connect and collect everything. Storage infrastructure systems based on object storage are growing significantly in both the number and capacity of deployments and are becoming the platform of choice to address the growth of unstructured data in enterprise data centers.

- The steep growth of unstructured data for emerging and established workloads requires products driven by infrastructure software-defined storage that can deliver tens of petabytes of storage and potentially leverage hybrid cloud workflow with public cloud IaaS. New and established storage companies are developing scalable object storage products to address cost, agility, and scalability limitations in traditional scale-up storage environments.

- Most organizations use a mix of storage types: file storage, block storage, and object storage. But the use of object storage is surging for several reasons: speed, scalability, searchability, security, data integrity, and reliability.

- Object storage provides various benefits for organizations that want to aggregate vast amounts of data, essential layer applications on top of that data store, conduct advanced data analytics that drives innovation, and protect against ransomware attacks.

- Several companies in the market for object storage are offering mixed deployment options to give customers choices in how they deploy infrastructure. Standard deployment options include turnkey high-density appliances or software-only options deployed on bare-metal industry-standard hardware as virtual machines or on docker containers. Companies in this market are increasingly offering their products as software-defined storage pre-certified to run on x86 industry-standard hardware.

Object-Based Storage Market Trends

Cloud based Deployment to Dominate the Market Share

- The steep growth of unstructured data for emerging and established workloads requires products driven by infrastructure software-defined storage that can deliver tens of petabytes of storage and potentially leverage hybrid cloud workflow with public cloud IaaS. New and established storage companies are developing scalable object storage products to address cost, agility, and scalability limitations in traditional scale-up storage environments.

- The current unstructured storage market is evolving to embrace hybrid cloud workflows and capabilities as IT leaders are looking to take advantage of public cloud agility, efficiency, and cloud computing capabilities. The object storage segment is considered a two-sided market. There are multiple providers of object storage protocols and consumers of these protocols consisting of applications.

- There were several providers than consumers until the Amazon S3 API became the de facto standard for object storage. Also, companies utilizing object storage platforms in enterprise data centers adopted Amazon S3, a protocol prominently used in the public cloud, because of the developer community around it.

- Several providers and consumers are using Amazon S3. Utilizing public cloud services like AWS has brought significant customer awareness to the object storage market. Software developers building Mode 2 web and mobile applications sometimes must repatriate these applications back to enterprise data centers. Enterprise IT seeks control of data and applications, while software developers seek efficient ways of programmatically interacting with infrastructure.

- Object storage excels at data sharing and consistency compared to other storage options. One instance of an application may wind up seeing partial data produced by another example in block-based and file-based data storage. Application developers ultimately require persistent locks to work around this problem. However, such plans have their own unique set of problems, including performance and accuracy issues.

North America to account for significant market growth.

- North America is expected to expand the global market through the projected period. The region's cloud object storage market is anticipated to grow throughout the review period due to the regional main players' consolidation. Additionally, the region's use of cloud storage services by large and small & medium organizations has increased due to the region's large-scale influx and outflow of enormous data.

- One of the factors driving the market's expansion is the growth of internet traffic and user-generated content, and the North American area sees the most I.P. traffic internationally. Cisco projects that the region's I.P. traffic will grow by 21% annually to 108.4 EB by last year.

- Additionally, the area is home to several well-known vendors in object storage, including IBM and Dell. This element aids in the greater use of Object-based storage in the area. Compared to unified file/block, SAN, and NAS, object storage will be purchased by more U.S. businesses. A quarter is expanding on-premises storage, while nearly half are boosting cloud storage.

- The BFSI industry is forced to adapt and innovate its services due to the change in business strategy. Worldwide, banking service providers are implementing cloud storage solutions. More than 90% of financial institutions, according to the American Bankers Association, use cloud technology for some or all of their banking operations.

Object-Based Storage Industry Overview

The object-based storage market is fragmented and fairly competitive and consists of several players, with a few major players currently dominating the market. Many companies are working on this technology due to its numerous advantages over other storage options. Some major players are Hitachi Vantara Corp, NetApp Inc., IBM Corporation (Red Hat), Scality Inc., and Dell EMC. Some of the recent developments include that, in

- November 2022, in collaboration with Snowflake, a provider of data clouds, Cloudian announced the opening of its HyperStore on-premises data lake storage. Customers of Cloudian and Snowflake will now have access to data deployed on-premises in a private cloud or hybrid cloud configuration and kept on HyperStore. HyperStore offers the scale and simplicity of a public cloud inside a company's data center, delivering improved performance, complete control over security, data sovereignty, and lower cost. HyperStore was created from the ground up to be fully S3 compliant.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.3 Market Drivers

- 4.3.1 Low acquisition costs of object-based solutions (especially for large-scale storage)

- 4.3.2 Technological advancements such as multi-cloud data management and introduction of ML In storage analytics

- 4.4 Market Challenges

- 4.4.1 Resistance to Change From the Traditional Storage Practices

- 4.5 Comparative Analysis of File vs Block vs Object-based storage

- 4.6 Key Use-cases for Object-based Storage - Big Data, Web-apps, Backup Archives, Fraud Prevention, etc.

- 4.7 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Cloud-based

- 5.1.2 On-Premise

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia

- 5.2.4 Australia and New Zealand

- 5.2.5 Latin America

- 5.2.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Hitachi Vantara Corp

- 6.1.2 NetApp Inc.

- 6.1.3 IBM Corporation (Red Hat)

- 6.1.4 Scality Inc.

- 6.1.5 Dell EMC

- 6.1.6 Cloudian, Inc.

- 6.1.7 Caringo Inc.

- 6.1.8 StorageCraft Technology Corp

- 6.1.9 WesternDigital Corp

- 6.1.10 SwiftStack Inc.

- 6.1.11 SUSE

- 6.1.12 OpenIO (OVHcloud)