|

시장보고서

상품코드

1637722

유럽의 카본블랙 시장 전망 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Europe Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

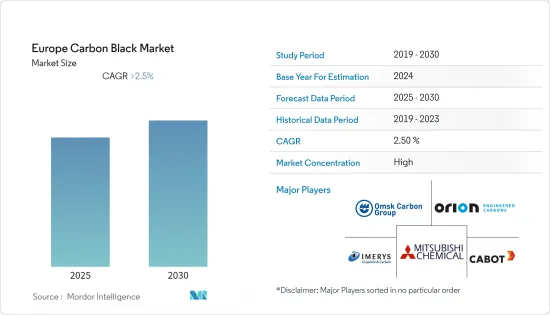

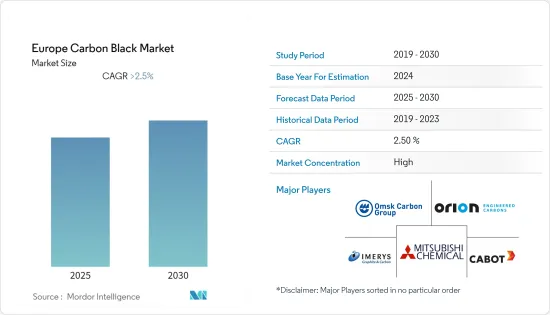

유럽의 카본블랙 시장은 예측 기간 동안 2.5% 이상의 연평균 성장율(CAGR)을 나타낼 것으로 예측됩니다.

이 지역에서의 COVID-19의 대유행으로 인해 수요와 생산성 저하, 공급망 혼란, 지역 봉쇄 등 시장은 부정적인 영향을 받았지만 2021년 시장은 큰 성장 를 나타내고 2022년도 계속 성장했습니다.

주요 하이라이트

- 중기적으로 시장을 이끄는 주요 요인은 유럽의 타이어 산업 성장, 섬유 및 섬유 산업에서의 응용 분야 증가, 특수 카본 블랙의 시장 침투 증가입니다.

- 반면, 친환경 타이어의 부상과 원자재 가격의 변동성은 예측 기간 동안 대상 산업의 성장을 제한 할 것으로 예상되는 주요 요인입니다.

- 전기자동차의 보급은 가까운 미래에 시장에 유리한 성장 기회를 가져올 것으로 예상됩니다.

- 독일은 가장 중요한 타이어 생산으로 인해이 지역 전체에서 시장을 지배했습니다. 또한 이 지역은 예측 기간 동안 가장 빠른 성장을 보일 것으로 예상됩니다.

유럽 카본블랙 시장 동향

타이어 및 산업용 고무 제품으로의 용도 확대

- 카본블랙은 고무 충전재로 사용되어 내마모성과 인장 강도를 비약적으로 향상시켜 타이어의 수명을 연장시킵니다.

- 또한 카본블랙은 타이어의 트레드와 벨트에서 열을 전도하여 타이어의 수명을 연장하는 효과도 있습니다. 또한 카본블랙은 타이어의 수명에 영향을 미치는 자외선과 오존으로부터 타이어를 보호합니다.

- 화학 엔지니어에 따르면 카본 블랙을 사용하지 않고 만든 타이어의 수명은 5000마일 이하일 가능성이 높다고 합니다. 결과적으로 대부분의 운전자는 1년에 1-2회 타이어를 교체해야 하는데, 이는 대부분의 소비자에게 바람직하지 않은 일입니다.

- 타이어 외에도 카본블랙은 컨베이어 벨트, 개스킷, 공기 스프링, 그로밋, 방진 장치, 호스 등 다양한 산업용 고무 제품의 성형품과 압출 성형품에 필요합니다. 카본블랙은 이러한 제품에 굽힘 강도를 부여합니다.

- 유럽에는 현재 91개 이상의 타이어 제조 시설, 15개의 R&D 센터, 12개의 주요 타이어 제조업체가 운영되고 있습니다. 또한 서유럽, 중부 및 동유럽 모두에서 승용차, 경상용차, 중대형 상용차의 생산 및 판매가 가까운 장래에 증가할 것으로 예상됩니다.

- 유럽 타이어 및 고무 제조업체 협회(ETRMA)가 발표한 통계에 따르면 교체용 타이어 시장은 2021년에 플러스 성장률을 기록했습니다. 소비자(승용차, SUV, 경상용차), 트럭, 모터 및 스쿠터 부문은 각각 14%, 12%, 14%의 성장률을 보였습니다.

- 앞서 언급 한 요인을 고려할 때 예측 기간 동안 타이어 및 산업용 고무 제품 부문에서 카본 블랙에 대한 수요가 증가 할 것으로 예상됩니다.

독일이 시장을 독점

- 독일은 유럽에서 카본 블랙의 선도적인 시장이 될 것으로 예상됩니다. 타이어, 고무, 인쇄 잉크, 플라스틱 등 다양한 최종 사용 산업에서 카본 블랙에 대한 수요가 증가하면서 독일의 카본 블랙 시장을 주도할 것으로 예상됩니다.

- 독일은 유럽 최대의 일반 고무 제품(GRG)과 타이어 생산국입니다. Continental AG, Dunlop GmbH, Michelin Reifenwerke AG & Co KGaA, Pirelli Deutschland GmbH, Freudenberg Group 등이 국내 타이어 및 비타이어 제품의 주요 제조업체입니다. 독일 타이어 산업의 선도 기업들은 유럽 시장 변화에 대응하여 확장과 축소를 동시에 실시했습니다.

- 독일은 유럽에서 가장 유명한 자동차 산업 국가입니다. 이 나라는 유럽 자동차 시장을 선도하고 있으며, 41개의 조립 공장과 엔진 생산 공장이 있으며, 유럽 자동차 생산 전체의 3분의 1에 기여하고 있습니다.

- OICA(국제자동차제조업협회)에 따르면 2021년에는 전년 대비 12% 감소한 33,08,692대의 차량을 생산하여 단기적으로 이 부문의 카본 블랙 수요를 제한했습니다.

- 그러나 독일의 자동차 산업을 발전시키고 현재 상황을 개선하기 위해 2021년 11월 새 연립 정부는 2030년까지 연간 약 160만 대에 해당하는 150억 대의 배터리 전기차를 독일에 도입하겠다는 목표를 발표했습니다. 이 정책적 지원은 카본 블랙을 포함한 자동차 부문의 화학 및 소재에 대한 수요를 강화할 것으로 예상됩니다.

- 2022년 독일에 본사를 둔 인쇄 잉크 전문가인 엡슈타인은 포장재의 장기 공급업체인 GFV Verschlusstechnik GmbH &Co.KG와 공동으로 UV 잉크 및 코팅을 위한 새로운 플라스틱을 개발했습니다. 스마트 인쇄 솔루션, 모든 기판 잉크, 디지털 인쇄 기술이 독일 인쇄 잉크 시장의 성장을 주도하고 이 부문에서 사용되는 카본블랙 수요에 긍정적인 영향을 미칠 것으로 예상됩니다.

- 이러한 긍정적인 특성은 예측 기간 동안 독일 카본블랙 시장을 주도할 것으로 예상됩니다.

유럽의 카본블랙 산업 개요

유럽의 카본블랙 시장은 통합되어있습니다. 이 시장의 주요 진출기업(무순서)에는 카봇(Kabot) Corporation, 미쓰비시(Mitsubishi) Chemical Corporation, Omsk Carbon Group, Orion Engineered Carbons, Imerys Graphite & Carbon 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 유럽에서의 타이어 산업의 성장

- 섬유 산업에서의 용도의 확대

- 스페셜티 블랙 시장 침투 증가

- 억제요인

- 그린 타이어의 상승

- 원료 가격의 변동

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 유형

- 퍼니스 블랙

- 가스 블랙

- 램프 블랙

- 서멀 블랙

- 용도

- 타이어 및 산업용 고무 제품

- 플라스틱

- 토너와 인쇄 잉크

- 코팅

- 섬유

- 기타

- 지역

- 독일

- 영국

- 이탈리아

- 프랑스

- 러시아

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%), 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Birla Carbon

- Black Bear Carbon BV

- Cabot Corporation

- Cancarb

- Carbon Black Kft.

- Continental Carbon Company

- Imerys Graphite & Carbon

- Mitsubishi Chemical Corporation

- Omsk Carbon Group

- Orion Engineered Carbons

- PHILLIPS CARBON BLACK LIMITED

- Tokai Carbon Co. Ltd.

제7장 시장 기회와 앞으로의 동향

- 전기자동차의 보급 확대

The Europe Carbon Black Market is expected to register a CAGR of greater than 2.5% during the forecast period.

The market was/is negatively impacted due to the COVID-19 pandemic in the region, including decreased demand and productivity, supply chain disruptions, and regional lockdowns; however, the market showed significant growth in 2021 and continued to grow in 2022.

Key Highlights

- Over the medium term, the major factor driving the market studied is the growing tire industry in Europe, growing application in fiber and textile industries, and increasing market penetration of specialty carbon black.

- On the flip side, the rising prominence of green tires and volatility in the prices of raw materials are the key factors anticipated to restrain the growth of the target industry over the forecast period.

- Adopting electric cars will likely create lucrative growth opportunities for the market soon.

- Germany dominated the market across the region due to the most significant production of tires. Also, the region is projected to witness the fastest growth during the forecast period.

Europe Carbon Black Market Trends

Increasing Application for Tires and Industrial Rubber Products

- Carbon black is used as a filler in rubber; it dramatically improves abrasion resistance and tensile strength, resulting in a tire that lasts longer.

- Furthermore, the carbon black helps conduct heat away from the tread and belts of the tires, extending the tire's lifespan. The carbon black also protect the tires from UV radiation and ozone, which can affect tire life.

- Carbon black in tires has the benefit of making rubber compositions more electrically conductive. According to chemical engineers, a tire built without carbon black would likely last 5000 miles or less. As a result, most drivers would have to replace their tires one to two times per year, which would be undesirable to most consumers.

- Other than tires, carbon black is also required for various molded and extruded industrial rubber products, such as conveyor belts, gaskets, air springs, grommets, vibration isolation devices, and hoses. It provides flex strength in such products.

- Europe has more than 91 tire manufacturing facilities, 15 R&D centers, and 12 leading tire manufacturers which are currently in operation. Furthermore, the production and sales of passenger cars, light commercial vehicles, and medium and heavy commercial vehicles in all of Western, Central, and Eastern Europe are expected to increase in the near future.

- As per the stats released by The European Tyre & Rubber Manufacturers Association (ETRMA), the replacement tire market registered a positive growth rate in 2021. The consumer (passenger cars, SUVs, and light commercial vehicles), truck, and motor & scooter segments reported 14%, 12%, and 14% growth respectively.

- Therefore, considering the aforementioned factors, the demand for carbon black is expected to rise from the tires and industrial rubber products segment during the forecast period.

Germany to Dominate the Market

- Germany is expected to be the leading market for carbon black in Europe. The increasing demand for carbon black from various end-use industries, such as tire, rubber, printing inks, and plastic, is expected to drive the carbon black market in Germany.

- Germany is the largest producer of general rubber goods (GRG) and tires in Europe. Continental AG, Dunlop GmbH, Michelin Reifenwerke AG & Co KGaA, Pirelli Deutschland GmbH, Freudenberg Group, etc., are some of the major manufacturers of the tire and non-tire products in the country. The major players in the German tire industry are expanding and contracting simultaneously in response to market changes in Europe.

- Germany has the most prominent automotive industry in Europe. The country leads the European automotive market, with 41 assembly and engine production plants that contribute to one-third of the total automobile production in Europe.

- According to OICA (International Organization of Motor Vehicle Manufacturers), in 2021, the country produced 33,08,692 vehicles, which decreased by 12% from the previous year; thereby, it restricted the demand for carbon black from this segment in the short term.

- However, to advance the automotive sector in Germany and improve its current situation, the new coalition government in November 2021 announced a target to bring in 15 billion battery electric vehicles in the country by 2030, equivalent to around 1.6 million battery vehicles a year. The initiatives are expected to bolster the demand for chemicals and materials in the automotive sector, including carbon black.

- In 2022, Eppstein, a Germany-based specialist in Printing ink, innovated a new plastic for its UV inks and coatings along with its long-term supplier of packaging material, GFV Verschlusstechnik GmbH & Co. KG. Smart printing solutions, ink for all substrates, and digital printing technology are likely to drive the growth of the printing inks market in Germany, thereby positively affecting the demand for carbon black utilized in this segment.

- Such positive attributes are expected to drive the market for carbon black in Germany through the forecast period.

Europe Carbon Black Industry Overview

The Europe Carbon Black Market is consolidated in nature. Some of the major players in the market (in no particular order) include Cabot Corporation, Mitsubishi Chemical Corporation, Omsk Carbon Group, Orion Engineered Carbons, and Imerys Graphite & Carbon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Tire Industry in Europe

- 4.1.2 Growing Application in Fiber and Textile Industries

- 4.1.3 Increasing Market Penetration of Specialty Black

- 4.2 Restraints

- 4.2.1 Rising Prominence of Green Tires

- 4.2.2 Volatility in Prices of Raw Materials

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Furnace Black

- 5.1.2 Gas Black

- 5.1.3 Lamp Black

- 5.1.4 Thermal Black

- 5.2 Application

- 5.2.1 Tires and Industrial Rubber Products

- 5.2.2 Plastics

- 5.2.3 Toners and Printing Inks

- 5.2.4 Coatings

- 5.2.5 Textile Fibers

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Russia

- 5.3.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Birla Carbon

- 6.4.2 Black Bear Carbon B.V.

- 6.4.3 Cabot Corporation

- 6.4.4 Cancarb

- 6.4.5 Carbon Black Kft.

- 6.4.6 Continental Carbon Company

- 6.4.7 Imerys Graphite & Carbon

- 6.4.8 Mitsubishi Chemical Corporation

- 6.4.9 Omsk Carbon Group

- 6.4.10 Orion Engineered Carbons

- 6.4.11 PHILLIPS CARBON BLACK LIMITED

- 6.4.12 Tokai Carbon Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth in the Adoption of Electric Cars