|

시장보고서

상품코드

1851229

방음재 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Acoustic Insulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

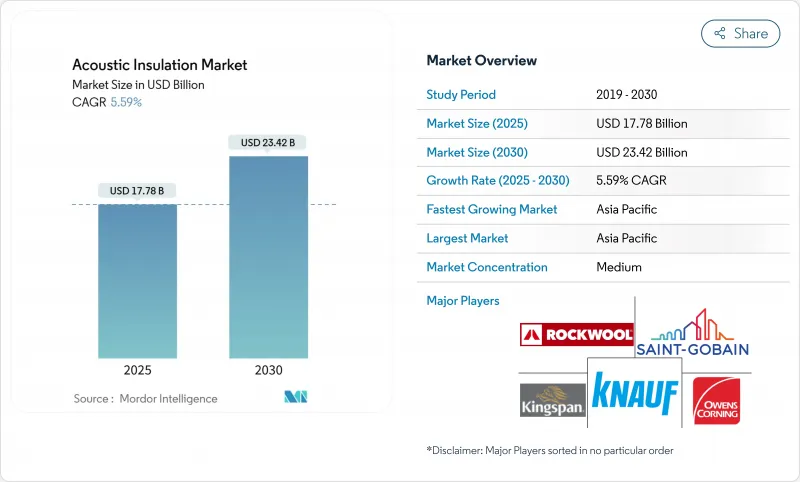

방음재 시장 규모는 2025년에 177억 8,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 5.59%를 나타낼 전망이며, 2030년에는 234억 2,000만 달러에 달할 것으로 예상됩니다.

각 주요 지역의 규제 당국은 소음 규제를 강화하고 있으며, 주택, 상업, 산업 프로젝트에서 소음재의 조기 사양화를 뒷받침하고 있습니다. 아시아태평양의 도시화, 선진국의 오픈 오피스 보급, 건축물 에너지 기준에 대한 음향 쾌적성의 통합으로, 소음 경감은 개설에서 핵심적인 설계 기준으로 전환하고 있습니다. 미네랄 울은 견고한 내화성과 높은 흡음성을 제공하기 위해 리더십을 유지하고 있으며, 폴리머 폼은 HVAC 엔지니어가 경량의 내습성 솔루션을 요구함에 따라 그 차이를 줄이고 있습니다. 한편, 제조업체 각사는 음향 성능을 그린 빌딩의 목표에 맞추기 위해, 탄소를 삭감한 배합이나 인증된 바이오 베이스의 함유량을 추구하고 있어, 이 조합이 방음재 시장의 경쟁을 형성하고 있습니다.

세계의 방음재 시장 동향과 인사이트

아시아 인프라 붐에 의한 소음 경감 의무화

중국, 인도, 동남아시아의 철도, 공항, 복합 시설에 대한 대규모 투자로 인해 얇고 고성능의 방음벽에 대한 수요가 높아지고 있습니다. 중국의 GB 50118 건축 기준법의 개정으로 2025년 1월부터 개발업체가 충족해야 하는 STC 기준치가 엄격해지고, 방음재 시장은 시험된 시스템을 대규모로 공급할 필요가 있습니다. 인도의 국가건축기준법의 단계적인 개정은 이 규제의 기세를 재현하는 것으로, 음향을 후기의 수정이 아니라 설계나 입찰의 초기 단계에 고정하는 것입니다. 집합 주택, 지하철 고가선, 물류 코리도 등에서는 지역의 소음에 대한 영향을 엄격히 체크하게 되어, 건축가는 폭넓은 주파수 대역을 차단하는 하이브리드 미네랄 울이나 폴리머 폼 복합재를 선택하게 되어 있습니다. 제조업체 각사는 물류시의 운송 소음을 삭감하고 대규모 인프라 용지의 리드 타임을 단축하기 위해 성장 회랑 근처에 생산을 집중시키고 있습니다. 그 결과, 컴플라이언스를 중시한 조달에 의해 기본적인 벌크롤로부터, 방음, 차열, 방화의 각 성능을 1개의 제품 라인에 정리한 인증 시스템으로, 가치의 이행이 가속하고 있습니다. 이 활동은 방음재 시장의 장기적인 수요 플로어를 확보하는 한편, 판매 채널은 사양 주도 모델로 재형성되고 있습니다.

소음공해를 규제하는 정부규제

정책의 틀은 단순한 데시벨의 한계를 넘어 종합적인 건강 기반 지표로 옮겨가고 있습니다. 유럽연합(EU)은 자동차 소음에 관한 환경 소음 지령과 규칙 No.540/2014를 갱신하고, 회원국에 대하여 2026년까지 주요 도로, 철도, 공항의 회랑을 매핑하여 처리할 것을 의무화했습니다. 미국에서는 휴면 상태에 있던 소음 규제법을 시행하기 위해 환경 보호국(EPA)에 대해 계속 중인 소송이 국가 기준에 관한 논의를 재연시켜 이미 복합 용도의 허가에 음향 조사를 의무화하고 있는 지자체를 활기차고 있습니다. 규제가 강화됨에 따라 조달 팀은 현재 준수를 증명하는 제 3 자 인증서를 요구하고 있으며 전체 문서 패키지가있는 공급업체에게는 가격이 비싸고 있습니다. EU의 일부 주에서는 미네랄 울 공동 장벽을 차열 및 차음 파티션으로 인정하고 있으며, 방음재 시장에서 가격 결정력을 강화하는 이중 가치 제안을 창출하고 있습니다.

불안정한 석유 화학 원료가 발포 플라스틱의 비용 패리티에 영향

이소시아네이트와 발포제의 가격 상승은 폴리머 폼과 미네랄 울의 비용 차이를 확대하여 확립된 프로젝트 예산을 혼란시킵니다. 가격에 민감한 시장의 계약자는 발포 스티롤의 시세가 급등하면 저급 섬유 배트로 대체하게 되어 폴리우레탄이나 압출법 폴리스티렌 라인의 단기 수요를 절감하고 있습니다. 이에 대해 연구팀은 재생 PET, 사탕수수 비가스 폴리올, 바이오 CO2 팽창제를 사용하여 폼을 개량하여 원유 가격의 변동에 대항하고 있습니다. 그러나 스케일업은 여전히 편차를 보이고 있으며 그 변동은 2026년까지 지속될 것으로 예상되기 때문에 폼의 성능은 여전히 높은 평가를 받고 있어도 폼의 보급이 억제될 것입니다.

부문 분석

미네랄 울은 2024년 매출의 38%를 차지하며 고유의 내화성, 강력한 저주파 흡수성, 진화하는 안전 기준에의 적합성 등이 뒷받침했습니다. ROCKWOOL사는 2024년에 판매되는 스톤 울 시스템에 의해 평생 에너지가 818TWh 절약되고 동시에 세계 180만 명의 학생의 학습 환경이 개선될 것으로 추정했습니다. 유리 울은 경량, 비용 효율성, 현장 절단의 용이성, 특히 그라디언트 지붕 주택에서 그 뒤를 이어집니다. HVAC 엔지니어가 습기 제어와 복잡한 덕트 형상에 대한 유연한 적합성을 선호하기 때문에 고분자 발포체의 CAGR은 가장 빠른 6%를 기록했지만 원료 변동으로 인해 보급이 완만해졌습니다. 천연섬유 카테고리는 저탄소 건축 계획에서 진행되고 있으며, IndiTherm 박쥐와 같은 제품은 두께 50mm에서 40dB의 감소를 실현하고 음의 구현 탄소 스코어를 달성했습니다. 포름알데히드를 제거하고 바이오 인증을 획득한 개질 바인더는 미네랄 울이 경쟁 압력을 견디는 데 도움이 되고, 방음재 시장은 균형 잡힌 재료의 다양성을 유지하고 있습니다.

지역 분석

2024년 매출 점유율은 아시아태평양이 36%를 차지했고 중국, 인도, 신흥 ASEAN 경제권이 메가레일 코리도, 스마트 시티 존, 고층 주택 클러스터를 추진하는 가운데 2030년까지의 CAGR은 7.50%를 나타낼 것으로 예측됩니다. 중국에서는 소음 상승에 대한 지역사회의 반발이 외관의 STC 기준을 엄격히 하도록 현지 당국을 추진하여 고밀도의 스톤 울제 커튼월 인서트의 대량 수주로 이어지고 있습니다. 주에 의한 장려책에 뒷받침된 인도의 도시 주택 추진책도 마찬가지로 방음 적합을 임의로부터 의무에 끌어올려, 글라스울 롤이나 경량간 칸막이 킷 수요를 밀어 올리고 있습니다.

2024년에는 북미가 오피스의 적극적인 리노베이션과 시정촌의 소음 조례 시행 강화를 통해 세계 매출에 크게 기여했습니다. 지자체의 계획 담당자는 복합 용도의 허가에 소음 영향 조사를 요구하게 되어 있어 건축가는 비용과 LEED 크레딧의 균형을 잡기 위해 하이브리드 미네랄 울과 재생 PET 패널로 대응하고 있습니다. 커튼월 스판드렐용 프리미엄 에어로겔 테이프는 체적률이 외관의 두께를 압박하는 밀집한 도심부에서 인기를 끌고 있습니다.

EU의 환경 소음 지침은 2026년까지 소음 맵과 행동 계획의 갱신을 요구하고 있습니다. 집합 주택과 교통의 요점은 미네랄 울의 공동 장벽과 엄격한 방화 등급에 적합한 높은 NRC 천장 클라우드를 이용함으로써 큰 혜택을 받고 있습니다. 중동 및 아프리카은 강력한 성장을 이루고 있으며, 특히 걸프 협력 회의 국가에서는 경기장, 지하철, 공항 터미널에 세계 수준의 음향 기준을 도입하고 있습니다. 남미에서는 브라질이 글라스울 버트를 사용한 맨션의 개수로 매출에 크게 공헌하고 있으며, 아르헨티나에서는 인지도의 향상과 함께 모듈식 벽 패널의 채용이 서서히 진행되고 있습니다. 이러한 다양한 지역 정세는 방음재 시장의 세계적인 확산을 부각시켜 시장의 순환 변동에 대한 회복력을 가져오고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인프라 붐이 아시아의 소음 경감 의무화를 뒷받침

- 소음 공해 억제를 위한 정부 규제와 주택용도에서의 채용 급증

- 신흥국 수요 증가

- 오픈 플랜 오피스의 성장이 천장 및 파티션 차음 패널 수요 촉진

- 시장 성장 억제요인

- 발포 플라스틱의 비용 패리티를 좌우하는 휘발성 석유 화학 원료

- 신흥 시장에 있어서 에어로겔 담요의 시공 기술 격차

- 다층 복합 폐기물 스트림에 대한 재활용 대응 압력

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 소재 유형별

- 미네랄 울

- 글라스 울

- 폴리머 폼

- 천연재

- 설치 구역별

- 벽 및 파티션

- 바닥 및 하부 바닥

- 천장 및 지붕

- HVAC 덕트 및 파이프 랩

- 최종 사용자 업계별

- 주거용 건물

- 상업용 건물

- 운송

- 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- 3M

- Armacell

- Aspen Aerogels, Inc.

- BASF SE

- Cabot Corporation

- CSR Pty Limited

- Fletcher Insulation

- Huntsman International LLC

- Hush Acoustics

- Johns Manville

- Kingspan Group

- Knauf Group

- Owens Corning

- Recticel Insulation

- ROCKWOOL A/S

- Saint-Gobain

- Siderise Group

- Sika AG

- Trelleborg AB

- Xella International(Etex Group)

제7장 시장 기회와 향후 전망

KTH 25.11.12The Acoustic Insulation Market size is estimated at USD 17.78 billion in 2025, and is expected to reach USD 23.42 billion by 2030, at a CAGR of 5.59% during the forecast period (2025-2030).

Regulatory authorities in every major region are tightening noise-control rules, propelling early-stage specification of sound-dampening materials in residential, commercial, and industrial projects. Urbanization in Asia-Pacific, the proliferation of open-plan offices in developed economies, and the integrating of acoustic comfort into building energy codes have moved noise mitigation from an afterthought to a core design criterion. Mineral wool retains leadership because it offers robust fire resistance and high sound absorption, and polymeric foams are closing the gap as HVAC engineers demand lightweight, moisture-tolerant solutions. Meanwhile, manufacturers are pursuing carbon-reduced formulations and certified biobased content to align acoustic performance with green-building targets, a combination shaping the competitive playbook in the acoustic insulation market.

Global Acoustic Insulation Market Trends and Insights

Infrastructure Boom-Driven Noise Mitigation Mandates in Asia

Massive investment in rail, airport, and mixed-use real estate across China, India, and Southeast Asia is amplifying demand for low-profile yet high-performance acoustic barriers. China's updated GB 50118 building code introduces stricter STC thresholds that developers must meet from January 2025, forcing the acoustic insulation market to supply tested systems at scale. India's phased amendments to its National Building Code replicate this regulatory momentum, locking acoustics into early design and tender stages instead of late-cycle fixes. Multi-tower housing, elevated metro lines, and logistics corridors are now heavily scrutinized for community noise impact, which is pushing architects toward hybrid mineral-wool and polymeric-foam composites that block wide frequency ranges. Manufacturers are localizing production near growth corridors to cut transport noise during logistics and to shorten lead times for large infrastructure lots. Consequently, compliance-driven procurement is accelerating value migration from basic bulk rolls toward certified systems that bundle acoustic, thermal, and fire performance attributes within one product line. This activity is securing a long-run demand floor for the acoustic insulation market while re-shaping sales channels toward specification-led models.

Government Regulations for Controlling Noise Pollution

Policy frameworks are moving beyond simple decibel caps to holistic health-based indicators, forcing specifiers to document absorption coefficients, STC ratings, and life-cycle profiles. The European Union has refreshed the Environmental Noise Directive and Regulation No 540/2014 on vehicle noise, obliging member states to map and treat major road, rail, and airport corridors by 2026. In the United States, ongoing litigation against the EPA to enforce the dormant Noise Control Act has reignited debate on national standards, energizing municipalities that already require acoustic studies for mixed-use permitting. As regulations solidify, procurement teams now demand third-party certificates that prove compliance, opening premium price territory for suppliers with complete documentation packages. Coupling of acoustic standards with energy codes is also growing; several EU states now recognise mineral-wool cavity barriers as both thermal and sound partitions, generating dual-value propositions that fortify pricing power in the acoustic insulation market.

Volatile Petrochemical Feedstock Impacting Foamed-Plastic Cost Parity

Surging prices for isocyanates and blowing agents widen cost differentials between polymeric foams and mineral wool, disrupting established project budgets. Contractors in price-sensitive markets now substitute lower-grade fibre batts when foam quotes spike, trimming short-term demand for polyurethane and extruded polystyrene lines. In response, research teams are reformulating foams with recycled PET, sugarcane bagasse polyols, and bio-CO2 expansion to insulate against crude-oil price swings. Yet scale-up remains uneven, and volatility is expected to persist through 2026, tempering foam uptake even as performance credentials remain strong.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Demand from Emerging Economies

- Growth of Open-Plan Offices Spurring Ceiling & Partition Acoustic Panels

- Installation Skill Gap for Aerogel Blankets in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral wool generated 38% of 2024 revenue, propelled by inherent fire resistance, robust low-frequency absorption, and compatibility with evolving safety codes. ROCKWOOL estimates that stone-wool systems sold in 2024 will save 818 TWh of lifetime energy while enhancing learning conditions for 1.8 million students worldwide. Glass-wool follows closely thanks to lightweight, cost efficiency, and ease of cutting on job sites, especially in pitched-roof housing. Polymeric foams post the quickest 6% CAGR as HVAC engineers prioritise moisture control and flexible fit for complex duct geometries, though feedstock volatility moderates uptake. Natural-fiber categories are advancing in low-carbon building schemes, with products like IndiTherm batts delivering a 40 dB reduction at 50 mm thickness and negative embodied carbon scores. Reformulated binders that eliminate formaldehyde and achieve biobased certification are helping mineral wool withstand competitive pressure, ensuring the acoustic insulation market maintains balanced material diversity.

The Acoustic Insulation Market Report is Segmented by Material Type (Mineral Wool, Glass Wool, and More), Installation Zone (Wall and Partition, Floor and Sub-Floor, and More), End-User Industry (Residential Construction, Commercial Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with a 36% revenue share in 2024, and the region is forecast to log a 7.50% CAGR through 2030 as China, India, and emerging ASEAN economies advance mega-rail corridors, smart-city zones, and high-rise residential clusters. China's community backlash against elevated noise has spurred local authorities to enforce stricter facade STC benchmarks, translating into bulk orders for dense stone-wool curtain-wall inserts. India's urban housing drive, backed by state incentives, similarly elevates acoustic compliance from optional to mandatory, swelling demand for glass-wool rolls and lightweight partition kits.

In 2024, North America significantly contributed to global revenue, driven by proactive office retrofits and heightened enforcement of municipal noise ordinances. Municipal planners increasingly require noise-impact studies for mixed-use permits, and architects respond with hybrid mineral-wool and recycled-PET panels to balance cost and LEED credits. Premium aerogel tapes for curtain-wall spandrels are gaining traction in dense city cores where floor-area ratios pressure facade thickness.

Europe remains a key player in regulatory advancements, with the EU's Environmental Noise Directive driving the requirement for updated noise maps and action plans by 2026. Multi-family housing and transport hubs are benefiting significantly, utilizing mineral-wool cavity barriers and high-NRC ceiling clouds that comply with stringent fire classifications. The Middle East and Africa region is experiencing robust growth, particularly in Gulf Cooperation Council states, which are incorporating world-class acoustic standards into their stadiums, metros, and airport terminals. South America contributes notably to sales, with Brazil leading through condominium retrofits favoring glass-wool batts, while Argentina is gradually adopting modular wall panels as awareness increases. This diverse regional landscape highlights the global scope of the acoustic insulation market and provides resilience against market cyclicality

- 3M

- Armacell

- Aspen Aerogels, Inc.

- BASF SE

- Cabot Corporation

- CSR Pty Limited

- Fletcher Insulation

- Huntsman International LLC

- Hush Acoustics

- Johns Manville

- Kingspan Group

- Knauf Group

- Owens Corning

- Recticel Insulation

- ROCKWOOL A/S

- Saint-Gobain

- Siderise Group

- Sika AG

- Trelleborg AB

- Xella International (Etex Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Boom-Driven Noise Mitigation Mandates in Asia

- 4.2.2 Government Regulations for Controlling Noise Pollution and Surge in Adoption in Residential Application

- 4.2.3 Rise in Demand from Emerging Economies

- 4.2.4 Growth of Open-Plan Offices Spurring Ceiling and Partition Acoustic Panels

- 4.3 Market Restraints

- 4.3.1 Volatile Petrochemical Feedstock Impacting Foamed-Plastic Cost Parity

- 4.3.2 Installation Skill Gap for Aerogel Blankets in Emerging Markets

- 4.3.3 Recycling Compliance Pressures on Multilayer Composite Waste Streams

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Mineral Wool

- 5.1.2 Glass Wool

- 5.1.3 Polymeric Foams

- 5.1.4 Natural

- 5.2 By Installation Zone

- 5.2.1 Wall and Partition

- 5.2.2 Floor and Sub-Floor

- 5.2.3 Ceiling and Roof

- 5.2.4 HVAC Duct and Pipe Wrap

- 5.3 By End-User Industry

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Transportation

- 5.3.4 Industrial

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Armacell

- 6.4.3 Aspen Aerogels, Inc.

- 6.4.4 BASF SE

- 6.4.5 Cabot Corporation

- 6.4.6 CSR Pty Limited

- 6.4.7 Fletcher Insulation

- 6.4.8 Huntsman International LLC

- 6.4.9 Hush Acoustics

- 6.4.10 Johns Manville

- 6.4.11 Kingspan Group

- 6.4.12 Knauf Group

- 6.4.13 Owens Corning

- 6.4.14 Recticel Insulation

- 6.4.15 ROCKWOOL A/S

- 6.4.16 Saint-Gobain

- 6.4.17 Siderise Group

- 6.4.18 Sika AG

- 6.4.19 Trelleborg AB

- 6.4.20 Xella International (Etex Group)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Demand for Aesthetic Prospects and Fire-resistant Properties of Acoustic Insulation