|

시장보고서

상품코드

1637773

지르코늄 시장 - 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Zirconium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

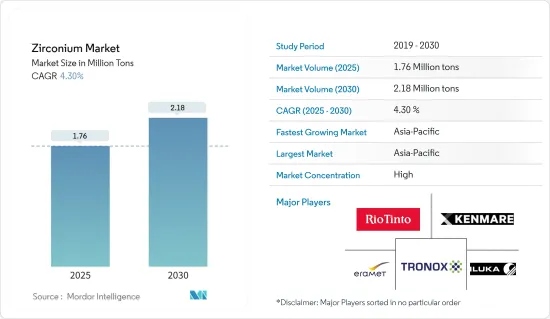

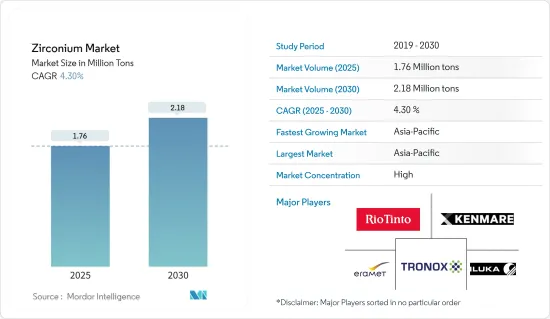

지르코늄 시장 규모는 2025년에 176만톤으로 추정되며, 2030년에는 218만톤에 이를 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 4.3%로 예상됩니다.

COVID-19의 감염자 수가 급증함에 따라 많은 국가들이 폐쇄 조치에 착수하여 세계 경제에 큰 영향을 미쳤습니다. 경제·산업 활동이 일시적으로 중단되었기 때문에 지르코늄 시장은 철강, 시멘트, 에너지·화학, 세라믹 등의 최종 사용자 산업으로부터의 생산과 수요의 양면에서 영향을 받았습니다. 그러나 원자력자원 개발에 대한 주목이 높아지고 있기 때문에 예측기간 동안 시장은 플러스 성장을 이룰 것으로 기대됩니다.

주요 하이라이트

- 중기적으로는 주조와 내화물의 성장, 아시아태평양의 원자력 발전소 증가, 표면 코팅의 사용 가속이 시장 성장의 주요 요인입니다.

- 반면 지르콘에 대한 의존도가 떨어지는 것은 시장 성장을 크게 방해할 가능성이 높습니다.

- 정형외과용 의료 부문의 지르코늄 수요 증가와 자동차 산업에 대한 엄격한 배출 기준이 조사한 시장에 기회를 가져올 것으로 예상됩니다.

- 중국은 전체 시장 수익의 대부분을 차지하고 있으며 예측 기간 동안 가장 빠른 CAGR을 나타낼 것으로 기대됩니다.

지르코늄 시장 동향

지르콘 분말/모래로부터 수요 증가

- 지르콘은 모든 유기와 무기 모래 결합제와 결합하는 능력, 저산성, 저열팽창계수, 고온에서의 높은 공간안정성, 고온에서의 화학적 안정성, 양호한 재활용성 등의 다양한 특성으로 주 모래와 분말(분쇄 모래)의 형태로 세라믹과 주조에 널리 사용됩니다.

- 세라믹에서 지르콘 모래는 불투명화에 대한 높은 굴절률과 같은 매우 가치있는 특성에 사용됩니다. 세라믹 본체 및 유리 모재에 높은 기계적 강도, 인성, 내구성을 부여하는 능력과 같은 부수적인 이점은 확립된 특성이며, 세라믹 산업의 특정 부문에서 용도를 찾을 수 있게 해줍니다. 이에 따라 이러한 특성을 선호하는 시장에 대응하고 있습니다.

- 주조 용도에서는 모래 주조, 인베스트먼트 주조, 코스워스 주조(알루미늄)용 성형 모재로 널리 사용됩니다. 또한, 다른 주물 모래의 젖음성을 저하시키기 위해 다이캐스트나 내화물의 도료나 세정의 금형 코팅으로서도 사용됩니다.

- 지르콘 모래는 금형과 중자의 제조에 사용되며 내화성, 저팽창성, 용강에 의한 습윤성 저감, 고열 전도성으로 규사보다 큰 이점이 있습니다.

- 지르콘 주조 모래는 더 나은 금속 마감, "번온" 가능성 감소, 금속 응고 개선을 제공합니다. 금속의 침투에 대한 저항력을 높이고 주물에 균일한 마무리를 줍니다.

- 앞서 언급한 요인들로부터, 지르콘 분말/모래 수요는 예측 기간 동안 성장할 것으로 예상됩니다.

시장을 독점하는 중국

- 중국은 지르코늄 세계 시장 점유율을 독점하고 있으며 현재 시나리오에서 가장 빠르게 성장하는 원자력 에너지 소비국으로 인기를 끌고 있습니다. 원자력자원 개발에 대한 관심이 높아지면서 지르코늄 수요가 증가할 것으로 예상됩니다.

- 중국은 세계 최대의 철강 생산국입니다. 세계철강협회가 발표한 보고서에 따르면 중국은 세계 철강 생산량 전체의 53%(1950.5톤)를 차지하고 있습니다. 또한 2021년 중국 정부는 총 조강 생산 능력 2,933만 톤/년의 43개의 새로운 EAF 건설을 승인했습니다. 따라서 새로운 철강 공장의 건설은 내화물 시장을 견인하여 국내 지르코늄 소비를 증가시킬 가능성이 높습니다.

- 인프라 정비의 속도가 빨라짐에 따라 중국에서는 주택과 상업용 건물이 증가하고 있습니다. 이 때문에 시멘트산업과 철강산업에서의 내화물 수요가 증가하여 시장 연구가 진행될 것으로 예상됩니다.

- 중국은 현재 가장 빠르게 성장하는 원자력 에너지 소비국으로 인기를 끌고 있습니다. 이 나라에는 50개의 운전가능한 원자로가 있으며 총 용량은 47,518MW입니다. 원자력자원 개발에 대한 주목이 높아짐에 따라 지르코늄 수요도 증가할 것으로 예상됩니다.

- 중국의 원자력 연구 이니셔티브에 따르면 2035년까지 원자력발전소의 가동은 약 180GW에 이를 것입니다. 그러므로 원자력발전의 생산능력 증가는 이 나라의 지르코늄 소비를 증가시킬 가능성이 높습니다.

- 내화물 및 세라믹과 같은 산업의 성장은 예측 기간 동안 시장 조사를 촉진할 것으로 예상됩니다.

지르코늄 산업 개요

세계 지르코늄 시장은 통합되어 있으며 상위 5개 기업이 세계 소비의 주요 점유율을 차지하고 있습니다. 지르코늄 소비의 대부분은 아시아태평양과 유럽입니다. 시장의 주요 진출기업은 Iluka Resources Limited, Rio Tinto, Tronox Holdings PLC, Kenmare Resources PLC, Eramet 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 아시아태평양의 원자력 발전소 성장

- 주조와 내화물에 있어서의 안정된 성장

- 표면 코팅에 사용 가속

- 억제요인

- 지르콘에의 의존도의 저하

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

- 수출입

- 무역규제 시책 분석

- 가격 동향

제5장 시장 세분화(시장 규모(수량 기준))

- 산출 유형

- 지르콘

- 지르코니아

- 기타

- 용도

- 지르콘 분말/분쇄 모래

- 지르콘 불투명체

- 내화물(지르코니아)

- 지르콘 화학제품

- 지르콘 금속

- 지역

- 생산

- 호주

- 브라질

- 중국

- 인도

- 인도네시아

- 남아프리카

- 우크라이나

- 기타

- 소비

- 중국

- 미국

- 일본

- 유럽연합

- 인도

- 러시아

- 기타

- 생산

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%) 분석

- 주요 기업의 전략

- 기업 프로파일

- Australian Strategic Materials Ltd

- Base Resources Limited

- Binh Dinh Minerals Company

- Doral Mineral Sands Pty Ltd

- Eramet

- Iluka Resources Limited

- INB

- Kenmare Resources PLC

- Lanka Mineral Sands Limited

- MZI Resources Ltd

- Rio Tinto

- Tronox Holdings PLC

제7장 시장 기회와 앞으로의 동향

- 의료 부문, 특히 정형외과 임플란트에서의 용도 확대

- 자동차에 관한 엄격한 배출 기준

The Zirconium Market size is estimated at 1.76 million tons in 2025, and is expected to reach 2.18 million tons by 2030, at a CAGR of 4.3% during the forecast period (2025-2030).

A sharp increase in the number of COVID-19 cases led to numerous countries resorting to lockdowns, which significantly affected the global economy. The economic and industrial activities came to a temporary halt, which led the zirconium market to witness repercussions in terms of both production and demand from end-user industries, such as iron and steel, cement, energy and chemicals, and ceramics. However, the increasing focus on developing nuclear power resources is expected to help the market achieve positive growth during the forecast period.

Key Highlights

- Over the medium term, the major factors driving the market's growth are the growth in foundries and refractories, the increasing number of nuclear power stations in Asia-Pacific, and the accelerating usage of surface coatings.

- On the other hand, the reducing dependence on zircon is likely to hinder the growth of market significantly.

- The rising demand for zirconium in the healthcare sector for orthopedics and stringent emission standards pertaining to the automotive industry are expected to create the opportunities for the market studied.

- China dominated the market studied, accounting for a major share of the total revenue, and it is expected to witness the fastest CAGR over the forecast period.

Zirconium Market Trends

Increasing Demand from Zircon Flour/Sand

- Zircon is widely used in ceramics and foundry, mostly in the form of sand and flour (milled sand), due to its various properties, such as the ability to bind with all organic and inorganic sand binders, low acidity, low thermal expansion coefficient, and high spatial stability at increased temperatures, chemical stability at high temperatures, and good recyclability.

- In ceramics, zircon sand is used for its highly valuable properties, such as its high refractive index for opacification. Its ancillary benefits, including its ability to impart greater mechanical strength, toughness, and durability to ceramic bodies and glass matrices, are established attributes and enable it to find applications in specific segments of the ceramic industry, thereby catering to markets with a preference for these attributes.

- In foundry applications, it is used widely as a molding base material for sand casting, investment casting, and Cosworth casting (aluminum). It is also used as a mold coating in die casting and refractory paints and washes, as it reduces the wettability of other foundry sands.

- Zircon sand is used for mold and core manufacturing, where its refractoriness, low expansion, reduced wettability by molten steel, and high thermal conductivity offer significant advantages over silica sand.

- Zircon foundry sands produce a better metal finish, a lesser likelihood of 'burn-on,' and improved metal solidification. It increases the resistance to metal penetration and imparts a uniform finish to the casting.

- Owing to the aforementioned factors, the demand for zircon flour/sand is expected to grow over the forecast period.

China to Dominate the Market

- China dominated the global market share for zirconium, and it is gaining popularity as the fastest-growing consumer of nuclear energy in the present scenario. The increasing focus on developing nuclear power resources is expected to increase the demand for zirconium.

- China is the largest steel producer in the world. According to the report published by World Steel Association, China accounted for 53% of the overall production of steel in the world, which is 1950.5 metric tons. Additionally, in 2021, the Chinese government approved the construction of 43 new EAFs with a total crude steel capacity of 29.33 million mt/year. Thus, the construction of new steel plants is likely to drive the market for refractories, thereby increasing the consumption of zirconium in the country.

- The increased pace of infrastructural activities has led to an increase in residential and commercial buildings in China. This is expected to drive the demand for refractories in the cement and iron steel industries, thereby driving the market studied.

- China is currently gaining popularity as the fastest-growing consumer of nuclear energy. The country has 50 operable nuclear reactors, with a combined net capacity of 47,518 MW. The increasing focus on the development of nuclear power resources is expected to increase the demand for zirconium.

- According to China's Atomic Energy Research Initiative, by 2035, nuclear plants operation should reach around 180 GW. Thus, increasing nuclear power production capacities is likely to increase the consumption of zirconium in the country.

- The growth in industries, such as refractories and ceramics, is expected to drive the market studied in the forecast period.

Zirconium Industry Overview

The global zirconium market is consolidated, with the top five companies accounting for major shares of global consumption. Most of the consumption of zirconium is in the Asia-Pacific region and Europe. The major players in the market include Iluka Resources Limited, Rio Tinto, Tronox Holdings PLC, Kenmare Resources PLC, and Eramet.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth of Nuclear Power Stations in the Asia-Pacific

- 4.1.2 Consistent Growth in Foundries and Refractories

- 4.1.3 Accelerating Usage in Surface Coatings

- 4.2 Restraints

- 4.2.1 Reducing Dependence on Zircon

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import and Export

- 4.5.1 Trade Regulatory Policy Analysis

- 4.5.2 Price Trends

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Occurrence Type

- 5.1.1 Zircon

- 5.1.2 Zirconia

- 5.1.3 Other Occurrence Types

- 5.2 Applications

- 5.2.1 Zircon Flour/Milled Sand

- 5.2.2 Zircon Opacifier

- 5.2.3 Refractories (Zirconia)

- 5.2.4 Zircon Chemicals

- 5.2.5 Zircon Metal

- 5.3 Geography

- 5.3.1 Production

- 5.3.1.1 Australia

- 5.3.1.2 Brazil

- 5.3.1.3 China

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 South Africa

- 5.3.1.7 Ukraine

- 5.3.1.8 Rest of the World

- 5.3.2 Consumption

- 5.3.2.1 China

- 5.3.2.2 United States

- 5.3.2.3 Japan

- 5.3.2.4 European Union

- 5.3.2.5 India

- 5.3.2.6 Russia

- 5.3.2.7 Rest of the World

- 5.3.1 Production

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Australian Strategic Materials Ltd

- 6.4.2 Base Resources Limited

- 6.4.3 Binh Dinh Minerals Company

- 6.4.4 Doral Mineral Sands Pty Ltd

- 6.4.5 Eramet

- 6.4.6 Iluka Resources Limited

- 6.4.7 INB

- 6.4.8 Kenmare Resources PLC

- 6.4.9 Lanka Mineral Sands Limited

- 6.4.10 MZI Resources Ltd

- 6.4.11 Rio Tinto

- 6.4.12 Tronox Holdings PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Usage in the Healthcare Sector, Especially Orthopedic Implants

- 7.2 Stringent Emission Standards Pertaining to Automotive