|

시장보고서

상품코드

1637795

유전체학 실험실 자동화 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Lab Automation In Genomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

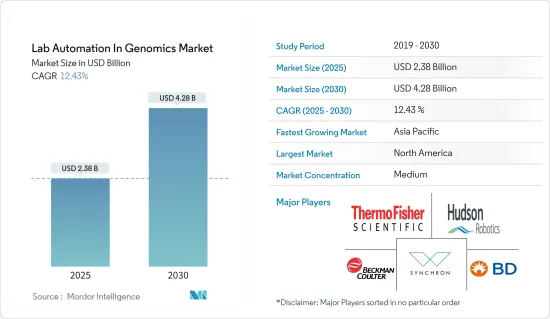

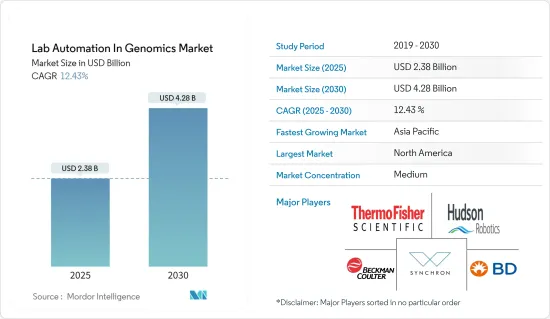

유전체학 실험실 자동화 시장 규모는 2025년 23억 8,000만 달러, 2030년 42억 8,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 12.43%에 달할 것으로 예측됩니다.

알 수 없는 상관관계, 숨겨진 패턴 및 기타 통찰력을 드러내는 데이터 분석의 진보라는 점에서 특히 대규모 데이터 세트를 테스트할 때 유전체 시퀀싱에 대한 이해가 크게 향상되었습니다. 이는 기술의 진보와 계산 능력의 향상이 시장을 견인하고 있기 때문입니다.

주요 하이라이트

- 유기체 전체의 전체 DNA 서열을 이용하는 유전체학의 개발은 몇몇 유전체학 대기업의 혁신적인 성과와 최근 차세대 시퀀싱 기술에 의한 것입니다.

- 차세대 시퀀싱 기술의 개발로 유전체 시퀀싱의 속도, 양 및 가격이 모두 극적으로 향상되었습니다. 게다가 바이오인포매틱스의 진보로 과학적 연구를 촉진하는 수백 개의 생명과학 데이터베이스와 프로그램이 가능하게 되었습니다. 이러한 데이터베이스는 정리되고 저장된 정보를 쉽게 검색, 대조 및 분석할 수 있도록 합니다.

- 게다가, 의학의 현저한 진보가 급속히 일어나고 있으며, 그 주된 이유는 최근의 유전체 분석의 진보에 있습니다. DNA 염기서열 분석은 유전자의 다양성이 어떻게 질병을 일으키는지를 보여주고 결국 새로운 치료로 이어집니다. 또한, 실험실 자동화는 혁신적인 유연성, 처리량 향상, 비용 효율적인 솔루션을위한 공간을 열었습니다. 신속한 처리가 가능하므로 정확성과 신뢰성에 대해 걱정하지 않고도 프로세스를 가속화할 수 있습니다. 제노타이핑과 DNA 시퀀싱 비용이 낮기 때문에 사업 확대율이 높습니다.

- DNA 시퀀싱 기술의 향상에 의해 보다 저렴한 가격으로 널리 이용할 수 있게 되었기 때문에 유전자 검사의 신흥 기업이 히나단처럼 탄생하고 있습니다. 그러나 모든 유전체에 대한 지식은 특히 다양한 상황에서 유전자 발현 패턴에 관심이 있는 기능적 유전체학를 실행할 수 있게 하여 유전체 시퀀싱 프로그램의 폭과 속도를 빠르게 증가시킬 수 있게 했습니다. 이 경우 가장 중요한 도구는 마이크로어레이와 바이오인포매틱스입니다.

- 핵산 분리, RNAi 스크리닝, CRISPR 분석, PCR 및 유전자 발현 분석은 자동화를 이용한 유전체학 용도의 일부입니다. 실험실 자동화 기업/벤더는 이러한 용도 요구 사항을 충족하는 도구를 개발합니다. 예를 들어, Tecan Group의 새로운 "Fluent Automation Workstation" 플랫폼은 일상적인 실험실 자동화를 단순화하고 워크 플로우의 생산성을 향상시키는 다양한 기능을 통합합니다. 실행하는 동안, 시스템은 동적으로 반응하고 지속적으로 최적의 처리량을 유지하기 위해 실제 시간을 기준으로 조정되며, 그 모든 것을 알기 쉬운 Gantt 차트를 통해 실시간으로 볼 수 있습니다.

- 양사는 고객의 요구에 부응하기 위해 신제품 개발과 기존 제품에 새로운 기능을 탑재하고 있습니다. 예를 들어, 2023년 5월, 실험실 자동화 솔루션 제공업체인 Opentrons 는 액체 처리 실험실 로봇인 Opentrons Flex robot의 출시를 발표했습니다. Flex robot은 인공지능 툴에 대응하고 있습니다.

- 유전체학 시장에서 실험실 자동화는 비용이 큰 우려 사항입니다. 초기 설정 비용이 높기 때문에 일부 신흥 국가들은 재생 실험실 자동화와 같은 비용 효율적인 실험실 자동화 시스템의 채택에 주력하고 있습니다. 또한 금리 상승과 경기침체로 인해 새롭고 비싼 장비를 구입하기 위한 개인 소비가 줄어들어 시장 성장을 제한하고 있습니다.

유전체학의 실험실 자동화 시장 동향

자동 액체 처리기가 고성장을 이룹니다.

- 유전체학 실험실에서는 교차 오염이 심각한 문제이지만 시약과 반응 혼합물을 관리하는 자동화 시스템을 채택하여 예방할 수 있습니다. 인위적인 개입을 제거함으로써 더욱 일관성이 높아질 것으로 예상됩니다. 플라스틱 성형 산업에서 수많은 기술 개발로 필요한 화학 물질의 수가 줄어들고 소량의 액체 취급이 용이 해졌습니다. 이러한 개발에 의해 자동 액체 취급 기계에 대응하는 마이크로리터나 나노리터의 플레이트의 작성이 용이하게 되었습니다.

- 업계의 혁신자들은 자동 액체 처리기를 만드는 기준을 수립했습니다. 공정 생산성을 높이기 위해 이러한 기업들은 지속적으로 고품질의 제품 설계에 투자하고 있습니다. 예를 들어, Agilent의 적응성이 높고 공간 절약형 자동 액체 처리 시스템은 항상 높은 정밀도로 합리적인 샘플 준비를 가능하게 합니다. 반복성을 유지하면서 자동화함으로써 실험실은 더 많은 샘플을 처리하고 수작업에서 해제됩니다.

- 또한 미국을 중심으로 세계에서 임상시험과 전임상시험이 급속히 확대되고 있기 때문에 시료분석에 속도가 요구되고 있습니다. 기계는 임상 연구에서 논스톱으로 가동하고 적절한 가동을 유지하기 위해서는 상당한 인력이 필요합니다. 게다가 새로운 질병이 발견되고 오래된 질병이 급속히 확산됨에 따라 조기 치료와 진단에 대한 수요가 증가하고 있습니다. 이로 인해 임상진단에 대한 응용률이 높아지고 자동 액체 핸들러의 채용이 가속될 것으로 예상됩니다.

- 자동 액체 취급 로봇은 종종 튜브와 웰에서 액체를 분산하거나 샘플링하며 액체 크로마토그래피 시스템의 프론트엔드로서 기계식 주입 모듈로 통합되는 경우가 많습니다. 이러한 유형의 장치에는 자동 분배 시스템과 마이크로플레이트 워셔도 포함됩니다. 이러한 필수 절약 도구는 다양한 바이오 분석, 액체 또는 분말 계량, 샘플 준비, 높은 처리량 스크리닝/시퀀싱(HTC)에 대한 정확한 샘플 준비를 제공합니다.

- 로봇산업협회에 따르면 생명과학산업은 자동 액체 핸들러, 자동판 핸들러, 로봇 암 등의 측면에서 수요를 충족하는 산업용 로봇의 성장률이 세 번째로 높다고 합니다.

북미가 가장 큰 시장 점유율을 차지

- 북미는 수년간 임상 연구의 선구자입니다. 이 지역에는 Pfizer, Novartis, GlaxoSmithKline, J&J 등 주요 제약 회사가 있습니다. 이 지역은 또한 개발 업무 위탁 기관(CRO)이 가장 집중하는 지역이기도 합니다. 중요한 CRO로는 Laboratory Corp. of America Holdings, IQVIA, Syneos Health, Parexel International Corp. 등이 있습니다.

- 업계를 선도하는 회사의 존재와 FDA의 엄격한 규제로 인해 이 지역 시장 경쟁은 치열합니다. 경쟁사보다 우위를 차지하기 위해 이 지역의 유전체 연구 기관은 실험실에 로봇 공학과 자동화를 채택하는 경향을 강화하고 있습니다.

- 유전체 산업, 특히 미국은 여전히 성장 단계에 있으며 앞으로 몇 년동안 빠른 속도로 성장할 것으로 예상됩니다. 새로운 유전체 시퀀싱 기술의 가용성, 확립된 건강 관리 인프라 및 노인 인구 증가는 시장 수익 성장에 크게 기여하고 있습니다.

- 미국에서는 성장에 대한 대응과 효율화의 필요성 때문에 혈액센터가 전자동 워크웨이 시스템을 도입하여 형검사나 스크리닝, 또는 감염증검사와 둘 다 실시했습니다.

- 미국의 유전체 산업은 앞으로 몇 년동안 빠른 속도로 성장할 것으로 예상됩니다. 새로운 유전체 시퀀싱 기술의 가용성, 확립된 건강 관리 인프라, 노인 인구 증가는 시장의 수익 성장에 크게 기여하는 요인입니다. 또한 국내에서는 정밀 의약품에 대한 수요가 높아지고 있습니다.

유전체학의 실험실 자동화 산업 개요

유전체학의 실험실 자동화 시장은 많은 크고 작은 기업들이 많은 국가에 제품을 수출하고 있기 때문에 경쟁은 중간 정도입니다. 대기업이 채택하는 주요 전략은 개발의 기술 진보, 파트너십, M&A입니다. 시장의 주요 기업으로는 Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd., Siemens Healthineers, Danaher Corporation, PerkinElmer 등이 있습니다.

2023년 1월, Becton, Dickinson, and Company(BD)는 새로운 실험실 자동화 솔루션인 미생물 실험실을 위한 3세대 BD Kiestra Total Lab Automation System을 발표했습니다. 이 새로운 자동 로보틱 트랙 시스템은 워크플로우의 간소화와 실험실 공간 최적화를 지원합니다. 이것은 실험실의 시료 처리를 자동화하는 BD Kiestra 미생물 실험실 솔루션과 함께 사용됩니다.

2023년 2월, 실험실 자동화 솔루션 제공업체인 Automata는 미국에서 사업 확장을 발표했습니다. Automata의 기술을 통해 미국의 생명과학 산업은 생산량을 늘리고 워크플로우 시간을 최대 50% 줄이고 기존 실험실 공간을 늘리고 과학자들이 혁신적인 연구를 수행하는 시간을 절약할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 공급망 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- COVID-19의 업계에 대한 영향 평가

제5장 시장 역학

- 시장 성장 억제요인

- IoT에 의한 검사실의 디지털 전환의 동향의 고조

- 방대한 데이터의 효율적 관리

- 시장의 과제

- 고액의 초기 설정 비용

제6장 시장 세분화

- 장치별

- 자동 액체 처리기

- 자동 플레이트 처리기

- 로봇 암

- 자동 보관 및 검색 시스템(AS/RS)

- 비전 시스템

- 지역별

- 북미

- 유럽

- 아시아

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Danaher Corporation/Beckman Coulter

- Hudson Robotics Inc.

- Becton, Dickinson and Company

- Synchron Lab Automation

- Agilent Technologies Inc.

- Siemens Healthineers AG

- Tecan Group Ltd.

- Perkinelmer Inc.

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd.

제8장 투자 분석

제9장 향후의 동향

JHS 25.02.12The Lab Automation In Genomics Market size is estimated at USD 2.38 billion in 2025, and is expected to reach USD 4.28 billion by 2030, at a CAGR of 12.43% during the forecast period (2025-2030).

There has been a significant improvement in understanding genome sequencing in terms of data analytics advances that reveal unknown correlations, hidden patterns, and other insights, especially when testing data sets on a large scale. This is due to technological advancements and increasing computational capacities driving the market.

Key Highlights

- The development of genomics, which uses the availability of whole DNA sequences for entire organisms, is due to the innovative work of a few genomics giants and the more recent next-generation sequencing technology.

- The speed, volume, and price of genome sequencing have all dramatically increased because of the development of next-generation sequence technologies. Additionally, hundreds of life science databases and programs that promote scientific study have been made possible because of advancements in bioinformatics. These databases make it simple to search, contrast, and analyze the information that is organized and kept there.

- Furthermore, significant medical advancements are occurring quickly, mostly due to recent improvements in genomic analysis. DNA sequence analysis clarifies how genetic diversity causes disease and ultimately results in novel treatments. Additionally, laboratory automation has opened space for innovative flexibility, increased throughput, and cost-effective solutions. It allows for quick handling and enables the process to be sped up without worrying about accuracy and dependability. Due to the low cost of genotyping and DNA sequencing, the expansion rate is strong.

- Genetic testing start-ups have been springing up like daisies due to improvements in DNA sequencing technology that have made it more affordable and widely available. However, the knowledge of whole genomes has made functional genomics viable, particularly interested in gene expression patterns under various situations, making it possible for genome sequencing programs to increase rapidly in breadth and speed. The most important tools, in this case, are microarrays and bioinformatics.

- Nucleic acid isolation, RNAi screening, CRISPR analysis, PCR, and gene expression analysis are just a few of the genomics applications that use automation. Laboratory automation players/vendors are developing tools to meet these application requirements. For example, Tecan Group's new "Fluent Automation Workstation" platform incorporates a variety of capabilities to simplify day-to-day laboratory automation and increase workflow productivity. During a run, the system reacts dynamically, adjusting based on actual times to maintain continuous optimal throughput, all of which are visible in real-time via an easy-to-understand Gantt chart.

- The companies are developing new products or incorporating new features in the existing products to meet the needs of the customer. For instance, in May 2023, opentrons, a lab automation solution provider, announced the launch of an Opentrons Flex robot, a liquid-handling lab robot. Flex Robot is compatible with artificial intelligence tools.

- The cost is the major concern in lab automation in the genomics market. The initial setup cost is high, so several developing countries focus on the adoption of cost-effective lab automation systems such as refurbished lab automation. Also, declining consumer spending on buying new and costly equipment due to increasing interest rates and economic downturns restrict market growth.

Lab Automation in Genomics Market Trends

Automated Liquid Handlers to Witness High Growth

- In the genomics lab, cross-contamination is a significant issue that can be prevented by employing automated systems to manage the reagents and reaction mixtures. It is thought that eliminating human intervention leads to more consistency. Numerous technological developments in the plastics molding industry have decreased the number of chemicals needed and made it easy to handle smaller volumes of liquid. These developments have made it easier to create micro- and nanoliter plates that can work with automated liquid-handling machinery.

- Industry innovators have established the standard to create automated liquid handlers. To boost process productivity, these businesses consistently invest in designing quality products. As an illustration, Agilent's adaptable and space-saving automated liquid handling systems allow for streamlined sample preparation with consistently high accuracy. While retaining repeatability, automation enables labs to run more samples and free up manual labor.

- Additionally, the quick expansion of several clinical and pre-clinical trials across the globe, mostly in the US, has made the requirement for speed in sample analysis essential. The machines operate nonstop in clinical research and require sizable personnel to maintain proper operation. Additionally, the demand for early treatments and diagnostics grows as new diseases are discovered and old ones spread quickly. This is anticipated to accelerate the adoption of automated liquid handlers by raising the rate at which clinical diagnostic applications are made.

- Automated liquid handling robots disperse and sample liquids in tubes or wells and are frequently integrated as mechanical injection modules as the front end of liquid chromatographic systems. This kind of equipment can also include automated pipetting systems and microplate washers. These essential labor-saving tools provide accurate sample preparation for various bioassays, liquid or powder weighing, sample preparation, and high throughput screening/sequencing (HTC).

- The life science industry, in terms of automated liquid handlers, automated plate handlers, and robotic arms, among others, has had the third-highest growth in industrial robots, according to the Robotic Industries Association, to fulfill the demand.

North America Occupies the Largest Market Share

- North America has been a pioneer in clinical research for years. This region is home to some of the major pharmaceutical companies, like Pfizer, Novartis, GlaxoSmithKline, J&J, and Novartis. The region also has the highest concentration of contract research organizations (CROs). Some of the significant CROs are Laboratory Corp. of America Holdings, IQVIA, Syneos Health, and Parexel International Corp.

- Owing to the presence of all the major players in the industry and stringent FDA regulations, the market is very competitive in the region. To gain an advantage over competitors, the genomics research organizations in the region are increasingly adopting robotics and automation in labs.

- The genomic industry, especially in the United States, is still in its growing phase and is expected to grow at a fast pace over the coming years. The availability of new genome sequencing technologies, well-established healthcare infrastructure, and the increasing geriatric population are significant contributing factors toward the revenue growth of the market.

- In the United States, the need to accommodate growth and the drive to boost efficiency are priming blood centers to acquire fully automated walkaway systems, either to perform types and screens or to test specimens for infectious diseases or both.

- The US genomic industry is expected to grow at a fast pace over the coming years. The availability of new genome sequencing technologies, well-established healthcare infrastructure, and the increasing geriatric population are significant contributing factors toward revenue growth of the market. Additionally, the demand for precision medicines is rising in the country.

Lab Automation in Genomics Industry Overview

Lab automation in the genomics market is moderately competitive, owing to many small and big players exporting products to many countries. The key strategies adopted by the major players are technological advancement in development, partnerships, and mergers and acquisitions. Some of the major players in the market are Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, Siemens Healthineers, Danaher Corporation, PerkinElmer, and others.

In January 2023, Becton, Dickinson, and Company (BD) introduced a new lab automation solution - 'the third-generation BD Kiestra Total Lab Automation System' for microbiology laboratories. The new automated robotic track system will assist in streamlining workflow and optimizing lab space. It is used with the BD Kiestra microbiology laboratory solution that automates lab specimen processing.

In February 2023, Automata, a laboratory automation solution provider, announced a business expansion in the United States as it will likely help the United States life science industry to save lab spaces with automation. With Automata's technology, the United States life sciences industry will increase output and cut workflow times by up to 50%, increase existing lab space, and save scientists time to work on innovative research.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Restraints

- 5.1.1 Growing Trend of Digital Transformation for Laboratories with IoT

- 5.1.2 Effective Management of the Huge Amount of Data Generated

- 5.2 Market Challenges

- 5.2.1 Expensive Initial Setup

6 MARKET SEGMENTATION

- 6.1 By Equipment

- 6.1.1 Automated Liquid Handlers

- 6.1.2 Automated Plate Handlers

- 6.1.3 Robotic Arms

- 6.1.4 Automated Storage and Retrieval Systems (AS/RS)

- 6.1.5 Vision Systems

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thermo Fisher Scientific Inc.

- 7.1.2 Danaher Corporation / Beckman Coulter

- 7.1.3 Hudson Robotics Inc.

- 7.1.4 Becton, Dickinson and Company

- 7.1.5 Synchron Lab Automation

- 7.1.6 Agilent Technologies Inc.

- 7.1.7 Siemens Healthineers AG

- 7.1.8 Tecan Group Ltd.

- 7.1.9 Perkinelmer Inc.

- 7.1.10 Eli Lilly and Company

- 7.1.11 F. Hoffmann-La Roche Ltd.