|

시장보고서

상품코드

1637835

탄산칼슘 시장 - 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

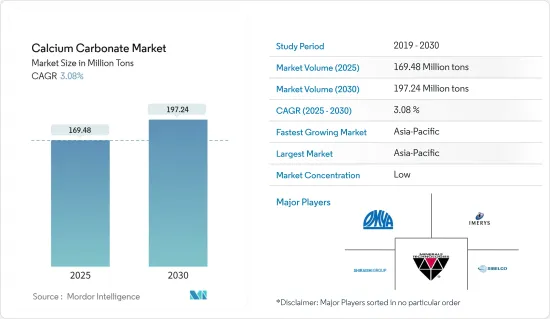

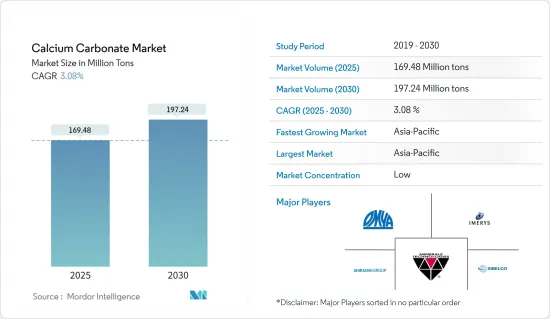

탄산칼슘 시장 규모는 2025년 1억 6,948만 톤, 2030년에는 1억 9,724만 톤으로 추정되며, 예측기간(2025-2030년)의 CAGR은 3.08%에 달할 것으로 예측됩니다.

COVID-19의 발생과 이에 따른 록다운 및 사회적 거리를 두는 규범에 따라 자동차, 건설 및 기타 제조 부문의 다양한 산업이 완전히 운영 중단에 몰렸습니다. 그러나 현재 시장은 대유행 전 수준에 도달한 것으로 추정됩니다.

주요 하이라이트

- 중기적으로 탄산칼슘 세계 시장을 견인하는 주요 요인은 아시아태평양의 건설 활동 확대와 제지 산업의 카올린에서 탄산칼슘으로의 대체입니다.

- 탄산칼슘과 관련된 건강 피해는 예측 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

- 그린 용도의 중요성이 증가하는 것은 조사 대상 시장에 새로운 기회를 제공할 것으로 예상됩니다.

- 중국, 인도, 일본 등 주요 소비국을 포함한 아시아태평양이 세계 시장을 독점하고 있습니다.

탄산칼슘 시장 동향

제지 부문이 시장을 독점

- 탄산칼슘은 충전재나 코팅용으로 사용되기 때문에 제지산업에서의 용도에 고려되는 필수성분 중 하나입니다. 불투명도, 밝기, 부드러움 등 CaCO3의 작업 품질은 필기용, 인쇄용, 포장용 종이 제조에 이상적인 성분이 되고 있습니다.

- 이것은 미네랄 충전제이며 종이 제조 비용을 크게 줄입니다. 광물은 섬유보다 건조하기 쉽기 때문에 기본 원료의 비용도 줄일 수 있습니다. 탄산칼슘은 인쇄 용지의 표면에 밝기와 매끄러움을 제공하기 때문에 종이 코팅에도 사용됩니다.

- 현재, 탄산칼슘은 다른 제지 충전재보다 우세합니다. 탄산칼슘이 선호되는 주요 이유는 더 밝고 부피가 큰 종이에 대한 수요입니다. 알칼리 제지 공정에서 탄산칼슘을 사용하면 큰 이점이 있습니다.

- 제지 산업에서 탄산칼슘은 카올린의 대안으로 사용됩니다. 합성 된 침전 탄산칼슘은 카올린보다 밝고 흰색이므로 많은 제조업체가 종이 채우기 및 코팅 목적으로 사용합니다. 보다 우수한 불투명도, 광택, 고휘도, 표면 마무리를 제공하여 인쇄 적성을 향상시킵니다.

- 탄산칼슘은 카올린의 대안으로뿐만 아니라 목재 펄프와 첨가제에도 사용됩니다. 알칼리 제지 공정에서 탄산칼슘은 충전재로 제지 공장에서 사용됩니다. 탄산칼슘은 제지에 사용되는 충전재와 안료의 총 점유율의 32%를 차지합니다.

- 현재 제지산업에서 탄산칼슘 시장 수요는 중국을 필두로 아시아태평양이 선도하고 있습니다. 종이 포장 및 티슈 제품 수요 증가가 아시아태평양 시장을 견인할 것으로 예상됩니다. 인도 제지 산업 협회(IPMA)에 따르면 인도 제지 산업은 세계 종이 생산량의 약 4%를 차지하고 있습니다. 이 산업의 추정 매출액은 7,000억 루피(84억 7,456만 달러)(국내 시장 규모는 8,000억 루피(96억 8,521만 달러))로, 재정 기여는 약 500억 루피(6억 533만 달러)입니다.

- 포장 수요는 이 지역의 급속한 경기 상승과 식품 소비 확대가 원동력이 되고 있습니다. 티슈 수요는 인구 증가와 위생 수준의 향상이 원동력이 되고 있습니다.

- 앞서 언급한 모든 요인은 예측 기간 동안 탄산칼슘 수요를 높일 것으로 예상됩니다.

아시아태평양이 세계 시장을 독점할 전망

- 아시아태평양은 이 지역의 건설 활동이 증가함에 따라 탄산칼슘 시장을 선도할 것으로 예상됩니다.

- 이 지역에서 건설 산업이 성장함에 따라 탄산칼슘 수요는 중국, 인도, 인도네시아 등 신흥 경제국의 경제 활동 증가와 새로운 투자 기회에 의해 견인 될 것으로 예상됩니다.

- 중국은 국토 면적의 22.5%에 달하는 대규모 삼림 매장량을 가진 세계 최대의 종이 펄프 생산국입니다. 산업은 현대적이고 고도로 기계화되어 있으며 노동력도 저렴합니다. 정부의 조림 이니셔티브로 중국의 지피 식물이 증가하고 있습니다.

- 중국은 플라스틱, 접착제, 실란트, 고무, 페인트 및 코팅제의 세계 최대 제조 및 소비국입니다. 플라스틱, 접착제, 실란트, 페인트 및 코팅제의 대부분은 자동차 산업과 건설 산업에서 소비됩니다. 고무는 자동차 산업이 주요 소비자입니다.

- 인도 정부의 '2022년까지 모든 사람에게 주택을' 계획도 산업에 큰 변화입니다. 또한 연방 내각은 국내 주요 도시에서 약 1,600개의 막힌 주택 프로젝트를 부활시키기 위해 35억 8,000만 달러의 대체 투자 펀드(AIF)의 설립을 승인했습니다.

- 인도제지공업협회(IPMA)에 따르면 인도 종이펄프 시장은 연 6-7%의 성장을 계속하고 있지만 지난 3년간 생산량은 감소하고 있습니다. 이것은 꾸준히 증가하는 소비량과는 대조적입니다.

- 전반적으로 아시아태평양의 다양한 최종 사용자 산업 수요가 증가하고 있으며, 아시아태평양의 탄산칼슘 시장은 세계 시장을 독점할 것으로 예측됩니다.

탄산칼슘 산업 개요

탄산칼슘 시장은 부분적으로 통합됩니다. 시장의 주요 기업으로는 Omya AG, Mineral Technologies Inc., Imerys, Shiraishi Group, Sibelco 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 아시아태평양의 건설 활동 성장

- 포장·제지산업의 급성장

- 제지 산업에서 카올린을 탄산칼슘으로 대체

- 억제요인

- 탄산칼슘에 따른 건강 피해

- 기타 억제요인

- 산업의 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(시장 규모(수량 기준))

- 유형

- 분쇄 탄산칼슘(GCC)

- 침강 탄산칼슘(PCC)

- 용도

- 건축자재 원료

- 영양보조식품

- 열가소성 플라스틱용 첨가제

- 충전제와 안료

- 접착제 성분

- 연료 가스의 탈황

- 토양 중화제

- 기타

- 최종 사용자 산업

- 종이

- 플라스틱

- 접착제 및 실란트

- 건축

- 페인트 및 코팅

- 의약품

- 자동차

- 농업

- 고무

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Chemical & Mineral Industries Pvt. Ltd

- FUJIAN SANMU NANO CALCIUM CARBONATE CO. LTD

- GLC Minerals

- Gulshan Polyols Ltd

- Huber Engineered Materials

- Imerys

- Kemipex

- Lhoist

- Maruo Calcium Co. Ltd

- Minerals Technologies Inc.

- Mississippi Lime Company

- Newpark Resources Inc.

- OKUTAMA KOGYO CO. LTD

- Omya AG

- Provale Holding SA

- SCHAEFER KALK GmbH & Co. KG.

- Shiraishi Kogyo Kaisha Ltd

- Sibelco

제7장 시장 기회와 앞으로의 동향

- 플라스틱·고무 산업으로부터의 나노탄산칼슘 수요 증가

- 그린 용도의 중요성 증가

The Calcium Carbonate Market size is estimated at 169.48 million tons in 2025, and is expected to reach 197.24 million tons by 2030, at a CAGR of 3.08% during the forecast period (2025-2030).

The outbreak of COVID-19 and resultant lockdowns and social distancing norms led to the complete shutdown of various industries in the automotive, construction, and other manufacturing segments. However, the market is currently estimated to have reached pre-pandemic levels.

Key Highlights

- Over the medium term, major factors driving the global calcium carbonate market are growing construction activities in the Asia-Pacific region and the replacement of kaolin with calcium carbonate in the paper industry.

- Health hazards associated with calcium carbonate are expected to hinder the market's growth during the forecast period.

- The emerging importance of green applications is expected to provide new opportunities for the market studied.

- The Asia-Pacific region, which includes the major consumption countries, such as China, India, and Japan, dominates the global market.

Calcium Carbonate Market Trends

Paper Sector to Dominate the Market

- Calcium carbonate is one of the essential ingredients considered for applications in the paper industry, as it is employed as fillers and for coating purposes. The working qualities of CaCO3, like opacity, brightness, and smoothness, make it an ideal component for the manufacturing of writing, printing, and packaging-grade paper.

- It is a mineral filler, which substantially reduces the production cost of paper. As the minerals are easier to be dried than fibers, it also reduces the cost of basic materials. Calcium carbonate is also used in paper coating, as it brings out the brightness and smoothness on the surface of printing paper.

- In the present scenario, CaCO3 is dominant over other papermaking filler materials. The main reason behind the preference for calcium carbonate is the demand for brighter and bulkier paper. There are significant advantages to the use of CaCO3 in the alkaline papermaking process.

- In the paper industry, calcium carbonate is used as a replacement for kaolin. Since the synthesized precipitated calcium carbonate is brighter and whiter than kaolin, many manufacturers have been using it for paper filling and coating purposes. It offers better opacity, gloss, high brightness, surface finishing, and improves printability.

- Calcium carbonate is not only used as a substitute for kaolin but also for wood pulp and additives. In the alkaline papermaking process, calcium carbonate is used in a paper mill as a filler material. Calcium carbonate amounts for 32% of the total share of filler and pigments used in paper production.

- Currently, the Asia-Pacific leads the market demand for calcium carbonate in the paper industry, with China being the leading consumer. Increasing demand for paper packaging and tissue products is expected to drive the market in the Asia-Pacific region. According to the Indian Paper Manufacturers Association (IPMA), the Indian paper industry accounts for about 4% of the world's production of paper. The estimated turnover of the industry is INR 70,000 crore (~USD 8,474.56 million) (domestic market size of INR 80,000 crores (~USD 9,685.21 million)), and its contribution to the exchequer is around INR 5,000 crore (~USD 605.33 million).

- The packaging demand is driven by rapid economic upticks and growing food consumption in the region. The tissue demand is driven by population growth and improving hygiene standards.

- All the aforementioned factors are expected to boost the demand for calcium carbonate during the forecast period.

Asia-Pacific Expected to Dominate the Global Market

- The Asia-Pacific region is projected to lead the market for calcium carbonate owing to increasing construction activities in the region.

- Along with the growing construction industry in the region, the demand for calcium carbonate is expected to be driven by increasing economic activities and new investment opportunities in emerging economies, such as China, India, and Indonesia, among others.

- China is the largest pulp and paper producing country in the world, owing to large forest reserves, which amount to 22.5% of the land area. The industry is modern and highly mechanized, and labor is cheap. Forest cover is increasing in China owing to the government's afforestation initiatives.

- China is globally the largest manufacturer and consumer of plastics, adhesives and sealants, rubber, and paints and coatings. The majority of plastics, adhesives and sealants, and paints and coatings are consumed by the automotive and construction industries. The automotive industry is the major consumer of rubber.

- The Indian government's 'Housing for All by 2022' scheme is also a major game-changer for the industry. Additionally, the Union Cabinet has approved the setting up of a USD 3.58 billion alternative investment fund (AIF) in order to revive around 1,600 stalled housing projects across the top cities in the country.

- According to the Indian Paper Manufacturers Association (IPMA), even though India's pulp and paper market has been growing around 6-7% per annum, the industry witnessed a drop in production over the past three years. This contrasts with the consumption, which is exhibiting a steady rise.

- Overall, with the demand increasing from various end-user industries in the region, the Asia-Pacific market for calcium carbonate is projected to dominate the global market.

Calcium Carbonate Industry Overview

The calcium carbonate market is partially consolidated in nature. Some of the major players in the market include Omya AG, Mineral Technologies Inc., Imerys, Shiraishi Group, and Sibelco, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Construction Activities in the Asia-Pacific Region

- 4.1.2 Rapidly Increasing Packaging and Paper Industry

- 4.1.3 Replacement of Kaolin with Calcium Carbonate in Paper Industry

- 4.2 Restraints

- 4.2.1 Health Hazards Associated with Calcium Carbonate

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Ground Calcium Carbonate (GCC)

- 5.1.2 Precipitated Calcium Carbonate (PCC)

- 5.2 Application

- 5.2.1 Raw Substance for Construction Material

- 5.2.2 Dietary Supplement

- 5.2.3 Additive for Thermoplastics

- 5.2.4 Filler and Pigment

- 5.2.5 Component of Adhesives

- 5.2.6 Desulfurization of Fuel Gas

- 5.2.7 Neutralizing Agent in Soil

- 5.2.8 Other Applications

- 5.3 End-user Industry

- 5.3.1 Paper

- 5.3.2 Plastic

- 5.3.3 Adhesives and Sealants

- 5.3.4 Construction

- 5.3.5 Paints and Coatings

- 5.3.6 Pharmaceutical

- 5.3.7 Automotive

- 5.3.8 Agriculture

- 5.3.9 Rubber

- 5.3.10 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Australia and New Zealand

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chemical & Mineral Industries Pvt. Ltd

- 6.4.2 FUJIAN SANMU NANO CALCIUM CARBONATE CO. LTD

- 6.4.3 GLC Minerals

- 6.4.4 Gulshan Polyols Ltd

- 6.4.5 Huber Engineered Materials

- 6.4.6 Imerys

- 6.4.7 Kemipex

- 6.4.8 Lhoist

- 6.4.9 Maruo Calcium Co. Ltd

- 6.4.10 Minerals Technologies Inc.

- 6.4.11 Mississippi Lime Company

- 6.4.12 Newpark Resources Inc.

- 6.4.13 OKUTAMA KOGYO CO. LTD

- 6.4.14 Omya AG

- 6.4.15 Provale Holding SA

- 6.4.16 SCHAEFER KALK GmbH & Co. KG.

- 6.4.17 Shiraishi Kogyo Kaisha Ltd

- 6.4.18 Sibelco

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand from the Plastic and Rubber Industry for Nano-calcium Carbonate

- 7.2 Emerging Importance of Green Applications