|

시장보고서

상품코드

1637848

매니지드 인프라 서비스 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Managed Infrastructure Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

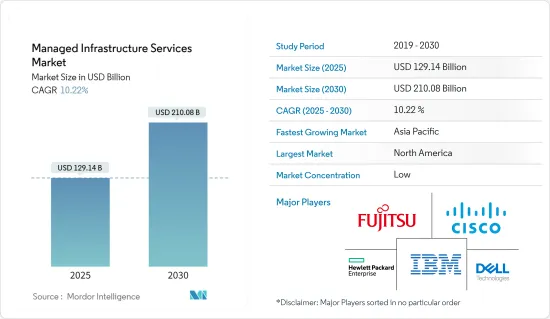

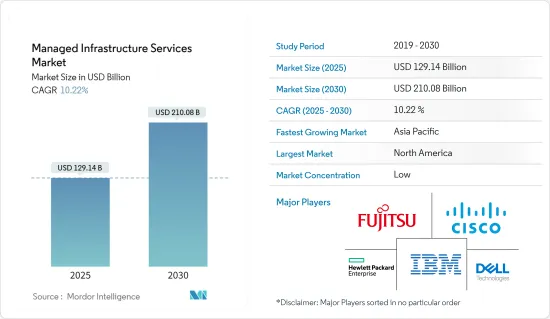

매니지드 인프라 서비스 시장 규모는 2025년에 1,291억 4,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 10.22%로, 2030년에는 2,100억 8,000만 달러에 달할 것으로 예측됩니다.

애널리틱스, 클라우드, IoT, 인지 컴퓨팅과 같은 기술 동향은 새로운 비즈니스의 필요성을 창출하고 있습니다. 기업은 혁신적인 비즈니스 모델 구축, 비즈니스 프로세스 최적화, 직원 능력 향상, 고객 경험을 개인화하기 위해 이러한 디지털 기술을 채택하고 있습니다.

주요 하이라이트

- 용도 테스트, 서비스 카탈로그 생성, 전문 컨설팅 등 전문 부가가치 서비스를 제공하는 관리형 서비스는 중복 가동 중지 시간을 줄여줍니다. 시장 개척은 다양한 모니터링 도구와 개별 팀이 관리하는 수많은 인프라 계층에 의해 지원됩니다. 예를 들어, BMC의 "BMC Helix ITSM"에서 시스템은 중앙 집중화되고 클라우드 네이티브로 관측 가능하게 연결되며 AIOps에 최적화되어 있습니다. 이 솔루션은 IT 인프라, 용도 성능, 네트워크 성능, 클라우드 서비스 모니터링 도구의 데이터를 완벽하게 노출합니다. 또한 팀과 개인 대시보드는 각 사용자의 요구에 맞게 사용자 정의됩니다.

- 클라우드 기반 기술의 보급과 진보가 수요를 끌어올려 시장을 견인하고 있습니다. 지난 몇 년동안 서버 중단 수정 및 문제 해결과 같은 일상 업무는 IT에 대한 주의를 완화하기 위해 아웃소싱되어 IT 서비스 공급업체의 전문 지식을 활용해 왔습니다. 모빌리티와 클라우드를 통한 디지털 전환의 도입이 증가하고 있으며 인프라의 현대화가 진행되고 있습니다. 최신 기술 강화를 위한 필요성으로 인해 조직은 인프라 관리 서비스를 선택하게 되었습니다.

- 비용과 운영 효율성 향상, 오래된 하드웨어 업데이트가 시장을 견인하고 있습니다. 관리 서비스에는 몇 가지 장점이 있으며, 그 중에서도 운영 및 비즈니스 프로세스의 지속적인 개선에 대한 지속적인 주력은 가장 중요합니다. Cisco Systems Inc.에 따르면, 관리형 서비스는 사내 경상 비용을 30-40% 절감하고 효율성을 50-60% 향상시키고 있습니다. 또한, 인프라에 새롭게 확장된 장비가 도입되면 이전 하드웨어가 반드시 호환되는 것은 아닙니다. 데이터센터 운영이 증가함에 따라 하드웨어는 운영을 강화하는 자산이 아니라 운영을 지연시키는 부채가 될 수 있습니다.

- 이익률 감소, 통합성 및 신뢰성에 대한 우려가 시장 성장을 억제합니다. 모빌리티 및 클라우드 컴퓨팅과 같은 새로운 기술은 비즈니스 전망을 빠르게 변화시키고 있습니다. 기업은 고객에게 원하는 이익을 제공하기 위해 이러한 기술과 동기화해야 합니다. 또한 중요한 비즈니스 인프라 호스팅을 통해 파트너에게 요청할 때 신뢰성에 대한 도전도 시장 성장을 방해합니다.

- COVID-19의 유행으로 인해 기업은 원격 근무에 큰 관심을 갖고 있습니다. 코로나바이러스의 만연을 막기 위해 각국 정부가 시행한 폐쇄 조치 중에 기업은 업무 유지에 신경을 쓰게 되어 클라우드 서비스 이용이 크게 늘어났습니다. 기업간에 클라우드 마이그레이션이 널리 퍼지고 어떤 경우에는 견인 역할을 할 것으로 예상되며 대부분의 기업은 이미 관리형 클라우드 서비스 제공업체와의 계약을 업데이트하고 있습니다. 또한 기업과 조직은 디지털 전환을 추진하기 위해 증강현실과 머신러닝과 같은 첨단 기술을 현재 IT 인프라에 통합하는 것을 선호했습니다.

관리형 인프라 서비스 시장 동향

클라우드 부문이 가장 높은 성장을 보여줄 전망

- 클라우드 도입의 등장은 관리형 인프라 서비스 제공업체(MISP)의 영역에 변화를 가져오고 퍼블릭 클라우드 또는 프라이빗 클라우드에서 기술 서비스를 제공하는 딜리버리 모델을 채택했습니다. 클라우드가 제공하는 이점을 고려하여 기업은 적절한 클라우드 공급자 선택, 클라우드로의 마이그레이션, 마이그레이션 후 클라우드 서비스 관리를 수행하기 때문에 클라우드 공급자(Google, AWS, Microsoft 등)와 제휴하는 MISP 요청합니다.

- 기업 수요가 높아지는 가운데, 다양한 기업이 기존의 매니지드 클라우드 인프라 서비스를 진화시키고 있습니다. 예를 들어, 2022년 12월, 스위스 금융 회사인 Klarpay AG는 클라우드 기반 인프라를 구축하기 위해 Amazon Web Services의 사용을 결정했습니다. 이 회사는 데이터센터 운영에 리소스를 소비하는 대신 확장성이 뛰어난 API 지원 트랜잭션 기능과 같은 새로운 기능을 개발하여 뱅킹 상품을 강화하는 등 가치 있는 업무에 집중했습니다.

- 디지털 플랫폼을 이용하는 소비자는 점점 늘어나고 있으며, 대용량 데이터를 저장하기 위해 광범위한 네트워크를 다루는 고속 데이터 전송을 위한 지속적인 디지털화의 진보에 대한 수요가 증가하고 있습니다. IT 비즈니스에서 소비자 기반 성장을 가속화하는 기술의 예시로는 원격 학습, 멀티플레이어 게임, 화상 회의, 라이브 스트리밍 등이 있습니다. IT 조직이 대량의 데이터를 저장하고 더 나은 서비스를 제공하려면 거대한 서버와 데이터 저장 장치가 필요합니다.

- 강화된 클라우드 인프라, IoT 대응 에코시스템 등의 최근 기술 동향은 미국의 IT 부문 전체에 새로운 비즈니스의 필요성을 창출할 수 있는 기회를 제공하고 있으며, 미국에서의 퍼블릭 클라우드의 보급률은 유행시에 높아질 것으로 예측됩니다. 또한 Fujitsu는 Amazon Web Services(AWS)에서 AWS의 공식 관리형 인프라 제공업체 파트너로 인증받아, 클라우드 변환을 가속화하고 디지털 변환을 신속하게 추진하고 기업 및 정부의 혁신을 가속화하는 회사 능력이 인정되었습니다. 이러한 사례는 예측 기간 동안 미국 전체 시장 수요를 촉진할 것으로 예상됩니다.

아시아태평양이 대폭적인 시장 성장을 차지

- 아시아태평양은 중국과 인도 등 다양한 국가에서 IT 및 IT 지원 서비스의 주요 공급원이기 때문에 시장이 크게 성장하고 있습니다. 예를 들어, IT와 BPM 부서는 인도에서 가장 중요한 경제 발생원 중 하나가 되었으며 GDP와 복지에 큰 영향을 미칩니다. IT 부문은 22년도에는 인도의 GDP의 7.4%를 창출했지만, 2025년까지 GDP의 10%를 차지할 것으로 예상되고 있습니다. 전미 소프트웨어 서비스 기업 협회(Nasscom)에 따르면 인도 IT 산업의 수익은 22년도에 2,270억 달러에 달하고, 전년 대비 15.5% 증가했습니다. 인도의 IT 투자액은 2021년 818억 9,000만 달러에서 2023년 1,103억 달러로 증가할 것으로 예측됩니다.

- 아시아태평양의 매니지드 인프라 서비스 성장에 기여하는 주요 요인 중 하나는 다양한 부문에서의 급속한 디지털화와 기술의 발전입니다. 기업은 비즈니스 효율성, 민첩성 및 경쟁을 강화하기 위해 첨단 IT 인프라에 대한 의존도를 높이고 있습니다. 그 결과 이러한 복잡한 IT 환경의 최적의 성능과 보안을 보장할 수 있는 전문적인 관리 서비스의 필요성이 매우 중요해지고 있습니다.

- 아시아태평양의 클라우드 기술 채택은 아시아태평양의 관리형 인프라 서비스 시장에 영향을 미칩니다. 기업이 유연성과 확장성을 높이기 위해 클라우드로 전환함에 따라 관리형 인프라 서비스는 클라우드 기반 인프라 관리로 확장되어 온프레미스 및 클라우드 환경의 원활한 통합을 실현합니다. 이 하이브리드 멀티클라우드 방식을 통해 기업은 변화하는 워크로드 및 수요에 적응하면서 IT 리소스를 최적화할 수 있습니다.

- 게다가 MIT 기술이 발표한 '클라우드 에코시스템 인덱스 2022'에 따르면 싱가포르는 8.48점을 차지하며 세계 클라우드 컴퓨팅 인프라 중 최고 수준이 되었습니다. 한국, 일본, 호주, 뉴질랜드는 2022년 클라우드 서비스에 유리한 생태계를 갖춘 아시아태평양 국가의 최고 점수였습니다. 이 평가는 아시아태평양이 디지털 인프라를 홍보하기 위해 노력하고 있다는 점을 강조하며 클라우드 서비스, 그리고 관리형 인프라 서비스에 매력적인 기지가 되었습니다.

관리형 인프라 서비스 산업 개요

매니지드 인프라 서비스 시장은 기술적으로 확립된 많은 대기업들이 진입하고 있기 때문에 매우 세분화되어 경쟁이 격화될 것으로 예상됩니다. 또한 시장을 유지하고 고객을 유지하기 위해 각 회사는 강력한 경쟁 전략을 채택하고 경쟁 기업간 경쟁 관계가 치열해지고 있습니다. 주요 진출기업은 Fujitsu, Cisco Systems Inc., Dell Technologies Inc. 등이 있습니다.

2023년 9월, 세계적으로 유명한 IT 인프라 서비스 제공업체인 Kyndryl과 풀스택 클라우드 서비스 제공업체의 Expedient가 제휴를 발표했습니다. 이 제휴를 통해 Kyndryl은 Expedient의 신뢰할 수 있는 클라우드 인프라와 데이터센터의 코로케이션을 활용하여 산업을 선도하는 사이버 회복력을 고객에게 향상시키고 있습니다. Expedient의 고도로 상호 연결된 데이터센터의 전국 네트워크는 클라우드 디퍼런스의 멀티클라우드 서비스의 주요 구성 요소인 수상 경력이 있는 인프라를 전문으로 합니다. 인프라는 VMware 기반의 Expedient Enterprise Cloud, 프라이빗 클라우드, 다양한 지역 및 부문 고객 및 잠재 고객 수요에 맞는 맞춤형 구성으로 제공됩니다.

2023년 8월, 전 세계 B2B 구독 상거래 플랫폼인 AppDirect는 ADCom Solutions의 네트워크 운영 센터(NOC)와 VEEUE 플랫폼을 인수했다고 발표했습니다. ADCom Solutions는 복잡한 IT 인프라 설계, 배포 및 종합적인 관리를 전문으로 하는 관리형 서비스의 세계 공급업체입니다. AppDirect는 이번 인수를 통해 기술 어드바이저의 광범위한 네트워크에 대한 액세스를 VEEUE에 제공할 수 있게 되며, AppDirect는 10,000명의 어드바이저 채널을 통해 관리형 네트워크 및 인프라 서비스 세트를 도입할 수 있습니다.

2022년 11월 디지털 변환, 고성능 컴퓨팅, 정보 기술 인프라의 세계 리더인 Atos와 Amazon.com, Inc.의 자회사인 Amazon Web Services(AWS)는 오늘 세계 전략적 변환 계약을 발표했습니다. 이 계약을 통해 대규모 인프라 아웃소싱 계약을 체결한 Atos 고객은 클라우드로의 워크로드 마이그레이션을 가속화하고 디지털 변환을 완료할 수 있습니다. 다년간 산업 최초 계약으로 Atos와 AWS는 전략적 파트너십을 더욱 강화할 수 있습니다. Atos는 AWS를 선호하는 엔터프라이즈 클라우드 제공업체로 선정했으며 AWS는 Atos를 IT 아웃소싱 및 데이터센터 혁신의 전략적 파트너로 인증했습니다. 이 제휴를 통해 Atos 고객은 Atos에서 비즈니스 및 기술 자문, 디지털 엔지니어링 및 관리 서비스를 받음으로써 클라우드로의 마이그레이션을 가속화할 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 시장 정의와 범위

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 이해관계자 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 클라우드 매니지드 인프라 서비스 이용 증가

- 클라우드 기반 기술의 보급과 진보가 수요 촉진

- 비용과 운용 효율의 개선, 노후화한 하드웨어의 갱신

- 시장 성장 억제요인

- 이익률 저하, 통합과 신뢰성에 대한 우려

- COVID-19가 매니지드 인프라 서비스 시장에 미치는 영향

제6장 시장 세분화

- 도입 유형별

- 온프레미스

- 클라우드

- 서비스 유형별

- 데스크톱 프린트 서비스

- 서버

- 재고

- 기타

- 최종 사용자별

- BFSI

- IT 및 텔레콤

- 의료

- 제조업

- 소매

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Fujitsu Ltd

- Cisco Systems Inc.

- Dell Technologies Inc.

- IBM Corporation

- Hewlett Packard Enterprise

- Microsoft Corporation

- TCS Limited

- Canon Inc.

- Alcatel-Lucent SA(Nokia Corporation)

- Toshiba Corporation

- Verizon Communications Inc.

- Citrix Systems Inc.

- Deutsche Telekom AG

- Xerox Corporation

- Ricoh Company Ltd

- Lexmark International Inc.

- Konica Minolta Inc.

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

JHS 25.02.06The Managed Infrastructure Services Market size is estimated at USD 129.14 billion in 2025, and is expected to reach USD 210.08 billion by 2030, at a CAGR of 10.22% during the forecast period (2025-2030).

Technology trends such as analytics, Cloud, IoT, and Cognitive Computing are creating new business imperatives. Companies are adopting these digital technologies to build innovative business models, optimize business processes, empower their workforce, and personalize the customer experience.

Key Highlights

- Redundant downtime is reduced through managed services, which offer specialized value-added services like application testing, service catalog creation, and professional consulting. The market's development is aided by various monitoring tools and numerous layers of infrastructure controlled by separate teams. For instance, in BMC's "BMC Helix ITSM" the system is centralized, cloud-native, connected with observability, and optimized for AIOps. This solution fully exposes data from monitoring tools for IT infrastructure, application performance, network performance, and cloud services. Additionally, team and individual dashboards are customized to each user's needs.

- Technological proliferation and advancement of cloud-based technology boosting the demand is driving the market. Over the past few years, daily operations of break-fix and troubleshooting of servers have been outsourced to reduce their attention over IT, thereby allowing the expertise of IT service vendors. An increase in the adoption of digital transformation with mobility and cloud has led to infrastructure modernization. The need to keep up with the latest technological enhancements has led organizations to opt for infrastructure-managed services.

- Improved cost and operational efficiency and updates of outdated hardware are driving the market. Managed services offer several benefits, relentless focus on continuous improvement of operational and business processes being the most significant one. According to Cisco Systems, managed services reduce recurring in-house costs by 30-40% and increase efficiency by 50-60%. Moreover, as new and enhanced equipment is introduced to the infrastructure, the old hardware might not always be compatible. As data center operations increase, the hardware could become more of a liability which slows down operations, than an asset that enhances them.

- Declining profit margins and integration and reliability concerns are restraining the market to grow. Emerging technologies, such as mobility and cloud computing, are rapidly changing the business landscape. Companies have to be in sync with these technologies to deliver desired benefits to the customers. Reliability concerns are also challenging the market to grow when hiring another partner to host critical business infrastructure.

- Businesses are putting a lot of attention on remote working due to the COVID-19 pandemic. The use of cloud services grew significantly as companies became more concerned with maintaining operations during lockdowns imposed by various governments to stop the spread of the coronavirus. In anticipation of cloud migration becoming more widespread among corporations and, in some cases, even gaining traction, most businesses have already renewed their contracts with managed cloud service providers. Additionally, businesses and organizations prioritized integrating cutting-edge technologies like augmented reality and machine learning into their current IT infrastructure to promote digital transformation.

Managed Infrastructure Services Market Trends

The Cloud Segment is Expected to Exhibit the Highest Growth

- The advent of cloud deployment has brought changes in the managed infrastructure services providers (MISP) space and made them embrace a delivery model for delivering technology services over a public or private cloud. Considering the advantages the cloud offers, businesses are seeking MISPs that have partnerships with cloud providers (such as Google, AWS, Microsoft, etc.) to choose the right cloud providers, migrate to the cloud, and manage cloud services after the transition.

- With the increasing demand from enterprises, various companies have made advancements in their existing managed cloud infrastructure service. For instance, in December 2022, the Swiss finance company Klarpay AG decided to use Amazon Web Services to create its cloud-based infrastructure. Instead of spending its resources to operate a data center, the company concentrated on high-value tasks, such as enhancing its banking product by creating new features like scalable and API-enabled transactional capabilities.

- Increasingly more consumers are using digital platforms, which has increased the demand for ongoing digitalization advancements for high-speed data transport with wide network coverage for large amounts of data storage. Examples of technologies that have accelerated the growth of the consumer base in the IT business include distance learning, multiplayer gaming, videoconferencing, and live streaming. Enormous servers and data storage units are necessary for IT organizations to store large amounts of data and offer improved services.

- Recent technology trends, such as enhanced cloud infrastructure, IoT enabled ecosystems, have provided opportunities in creating new business imperatives across the US IT sector, and the penetration of public cloud in the United States is predicted to be higher during a pandemic. Additionally, Fujitsu has been recognized by Amazon Web Services (AWS) as an official AWS-managed infrastructure provider partner, thereby validating the company's capabilities in accelerating cloud transformation and helping fast-track digital transformation, and accelerating innovation for enterprises and government. Such instances are expected to fuel the demand of the market across the United States during the forecast period.

Asia-Pacific Account for a Significant Market Growth

- Asia-Pacific region accounts for the significant market growth due to dominating sources of IT and IT-enabled services in various countries such as China and India. For instance, the IT & BPM sector has become one of India's most significant economic generators, substantially impacting its GDP and welfare. The IT sector generated 7.4% of India's GDP in FY22; by 2025, it is expected to account for 10% of its GDP. The Indian IT industry's revenue reached USD 227 billion in FY22, a 15.5% YoY growth, according to the National Association of Software and Service Companies (Nasscom). India was predicted to spend USD 110.3 billion on IT in 2023, up from an estimated USD 81.89 billion in 2021.

- One of the key factors contributing to the growth of managed infrastructure services in the Asia-Pacific region is the rapid digitization and technological advancements across various sectors. Enterprises are increasingly relying on advanced IT infrastructure to enhance operational efficiency, agility, and competitiveness. As a result, the need for specialized managed services that can ensure the optimal performance and security of these complex IT environments has become crucial.

- The region's adoption of cloud technologies also influences the Asia-Pacific managed infrastructure services market. As organizations migrate to the cloud for enhanced flexibility and scalability, managed infrastructure services extend to cloud-based infrastructure management, ensuring seamless integration between on-premises and cloud environments. This hybrid and multi-cloud approach allows businesses to optimize their IT resources while adapting to changing workloads and demands.

- Further, according to an MIT Technology publication, Singapore ranked highest on the Cloud Ecosystem Index 2022, with a score of 8.48, for cloud computing infrastructure worldwide. South Korea, Japan, Australia, and New Zealand were top-scoring Asia-Pacific nations with favorable ecosystems for cloud services in 2022. This recognition emphasizes the region's commitment to advancing its digital infrastructure, making it an attractive hub for cloud services and, by extension, managed infrastructure services.

Managed Infrastructure Services Industry Overview

The managed infrastructure services market is highly fragmented as many large, technologically established players are present in the industry, and the rivalry is expected to be on the higher side. Additionally, in order to sustain in the market and retain their clients, companies are employing powerful competitive strategies, thereby intensifying competitive rivalry in the market. Key players are Fujitsu Ltd, Cisco Systems Inc., Dell Technologies Inc., etc.

In September 2023, Kyndryl, a prominent provider of IT infrastructure services globally, and Expedient, a Full-Stack Cloud service provider, announced a partnership. This partnership will improve Kyndryl's industry-leading cyber resilience capabilities to customers by utilizing Expedient's reliable cloud infrastructure and data center colocation. Expedient's highly interconnected nationwide network of data centers is dedicated to its award-winning infrastructure, a key component of its Cloud Different multi-cloud services. Infrastructure is offered in VMware-based Expedient Enterprise Cloud, private cloud, and customized configurations to suit the demands of clients and prospects in various geographies and sectors.

In August 2023, AppDirect, a global B2B subscription commerce platform, announced that it had acquired the Network Operations Center (NOC) and VEEUE platform of ADCom Solutions. ADCom Solutions has been a global provider of managed services, specializing in designing, implementing, and comprehensively administrating complex IT infrastructures. AppDirect will be able to offer VEEUE access to the extensive network of technology advisers through this acquisition, allowing AppDirect to introduce a suite of managed network and infrastructure services through its channel of 10,000 advisors.

In November 2022, Atos, a global leader in digital transformation, high-performance computing, and information technology infrastructure, and Amazon Web Services, Inc. (AWS), a subsidiary of Amazon.com, Inc., today announced a global Strategic Transformation Agreement. This agreement enables Atos customers with large-scale infrastructure outsourcing contracts to accelerate workload migrations to the cloud and complete digital transformation. With the multiyear, first-in-the-industry deal, Atos and AWS can further their strategic partnership. Atos has chosen AWS as its preferred enterprise cloud provider, and AWS has identified Atos as a strategic partner for IT outsourcing and data center transformation. With the help of this arrangement, Atos' clients may hasten their transitions to the cloud by receiving business and technology advisory, digital engineering, and managed services from Atos.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing use of Cloud Managed Infrastructure Services

- 5.1.2 Technological Proliferation and Advancement of Cloud Based Technology Boosting the Demand

- 5.1.3 Improved cost and Operational Efficiency and Update of Outdated Hardware

- 5.2 Market Restraints

- 5.2.1 Declining Profit Margins and Integration and Reliability Concerns

- 5.3 Impact of COVID-19 on Managed Infrastructure Services Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Services Type

- 6.2.1 Desktop and Print Services

- 6.2.2 Servers

- 6.2.3 Inventory

- 6.2.4 Other Types

- 6.3 By End User

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 UK

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia

- 6.4.3.5 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Argentina

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 UAE

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 Dell Technologies Inc.

- 7.1.4 IBM Corporation

- 7.1.5 Hewlett Packard Enterprise

- 7.1.6 Microsoft Corporation

- 7.1.7 TCS Limited

- 7.1.8 Canon Inc.

- 7.1.9 Alcatel-Lucent SA (Nokia Corporation)

- 7.1.10 Toshiba Corporation

- 7.1.11 Verizon Communications Inc.

- 7.1.12 Citrix Systems Inc.

- 7.1.13 Deutsche Telekom AG

- 7.1.14 Xerox Corporation

- 7.1.15 Ricoh Company Ltd

- 7.1.16 Lexmark International Inc.

- 7.1.17 Konica Minolta Inc.