|

시장보고서

상품코드

1851311

튜브 포장 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Tube Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

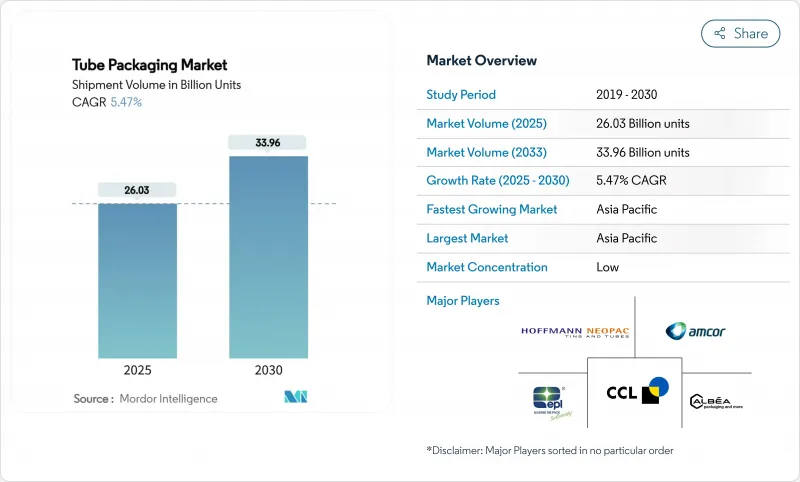

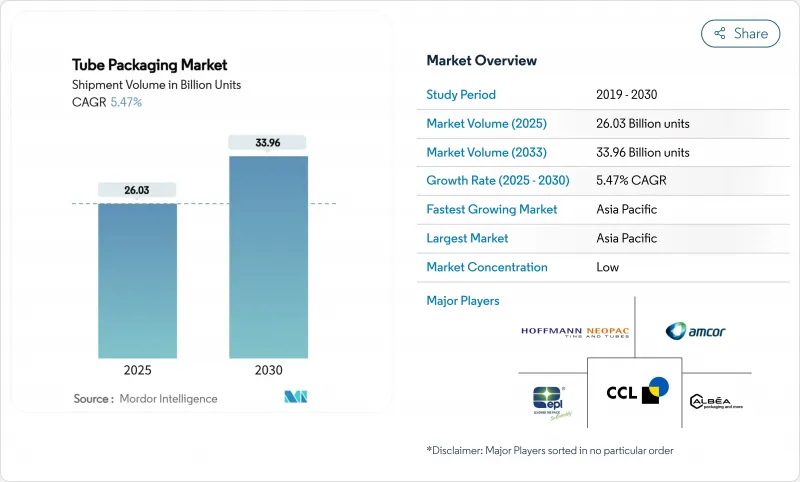

튜브 포장 시장 규모는 2025년에 260억 3,000만 유닛에 이를 것으로 추정되고, 2030년에는 339억 6,000만 유닛에 이를 것으로 예측되며, CAGR 5.47%로 성장할 전망입니다.

2030년까지 재활용 가능 의무화 규제 및 지속 가능한 솔루션에 대한 소비자 수요가 증가함에 따라 제조업체는 단일 소재와 재활용 컨텐츠 형식에 대한 투자를 강요합니다. 판지와 바이오 튜브는 CAGR 8.53%로 가장 빠른 성장을 기록하고 있지만, 플라스틱 형식은 가공 인프라가 확립되어 있기 때문에 수량의 리더를 유지하고 있습니다. 브랜드는 편의성과 정확한 용량을 선호하기 때문에 최종 용도가 조리된 식품과 일반용 의약품으로 다양화되어 수익원이 넓어지고 있습니다. Amcor와 Berry Global의 84억 달러의 합병으로 대표되는 지속적인 합병 활동은 경쟁 역학을 재구성하고 다층 플라스틱에 대한 의존을 제한하는 장벽 기술의 혁신을 가속화하고 있습니다.

세계의 튜브 포장 시장 동향 및 인사이트

퍼스널케어 및 화장품 수요 증가

미용 브랜드는 제품 라인의 프리미엄화를 계속하고 있으며, 섬세한 처방을 보호하고 제어된 디스펜서를 가능하게 하는 튜브가 선호됩니다. Albea는 컨셉부터 출시까지의 사이클을 단축하는 한편, 리사이클 소재를 채용해, 2030년까지 46%의 이산화탄소 삭감 목표를 추구하고 있습니다. 콜게이트의 투명 PET 엘릭서 튜브는 에브리드롭 코팅으로 제품의 배출성을 향상시키고 브랜드 충성도를 강화하는 사용자 경험의 향상을 강조하고 있습니다. 소재의 출처나 탄소발자국의 가시성도 향상하고 있어 환경 의식이 높은 쇼핑객에게 울림을 주는 마케팅 나라티브를 지지하고 있습니다.

지속 가능한 패키지에 대한 소비자 선호도 증가

가정용 구강 관리 브랜드는 복합 라미네이트에서 영국에서 주류가 되는 커브사이드 흐름으로 들어갈 수 있는 완전히 재활용 가능한 고밀도 폴리에틸렌 형식으로 이동합니다. Neopac은 유럽의 튜브 제조 업체로서 처음으로 RecyClass EN 15343 인증을 받았으며 추적 가능한 재활용 함량을 입증하고 경쟁력을 강화했습니다. 이러한 이정표는 지속가능성 컴플라이언스를 시장 차별화로 바꾸어 튜브 포장 시장을 보다 가치 있는 혁신으로 끌어올립니다.

대체품의 가용성

경량, 개봉의 용이함, 재료 사용량의 삭감을 겸비한 스탠드 업 파우치는 2029년까지 470억 달러에 이를 것으로 예측되어, 소스나 조미료의 브랜드를 튜브로부터 떼어내고 있습니다. 마스터 푸즈의 재활용 가능한 종이 1회 팩은 대체 형식이 지속가능성과 물약 제어 우선순위를 충족시킬 수 있는 방법을 보여줍니다. 이러한 기술 혁신에 의해 튜브 제조업체 각사는 정확한 도징이나 높은 산소 배리어성과 같은 기능적인 강점을 강조해, 용적의 감소를 방지하려고 하고 있습니다.

부문 분석

플라스틱 형식은 2024년 튜브 포장 시장 점유율의 68.14%를 차지했으며, 비용 효율적인 압출 라인과 보편적인 브랜드 지명도에 의해 지원됩니다. 플라스틱 중에서는 고밀도 폴리에틸렌과 폴리프로필렌이 크림에서 젤까지 다양한 점도에 대응하여 업계를 가로지르는 범용성을 확보하고 있습니다. 폴리머층과 알루미늄층을 적층한 라미네이트는 풍미 유지가 불가결한 구강 케어용 제제를 계속 보호하고 있습니다. 알루미늄 튜브는 틈새 시장이지만 휘발성 약제 활성 물질과 산소에 민감한 식품을 저장하고 프리미엄 가격의 발판을 굳히고 있습니다.

그러나 판지와 바이오 솔루션은 PPWR이 재생 가능한 기판으로의 이동을 가속화하기 때문에 CAGR 8.53%로 더 넓은 튜브 포장 시장을 능가하고 있습니다. Huhtamaki의 OmniLock Ultra 배리어 종이는 재활용이 가능하지만 알루미늄과 같은 보호 기능을 제공합니다. Amcor사가 특허를 받은 AmFiber Performance Paper도 마찬가지로 식품 및 헬스케어 분야를 목표로 하고 있으며 섬유 기반 구조가 엄격한 수분 제한을 충족시킬 수 있음을 증명하고 있습니다. 채택이 확대됨에 따라 플라스틱이 규모면에서 우위를 유지하더라도 절대량에서는 플라스틱 리드가 줄어들 것으로 예측됩니다.

스퀴즈 튜브 및 접이식 튜브는 2024년 출하량의 65.34%를 차지했으며, CAGR 7.43%로 증가할 것으로 예측됩니다. 충격 압출 알루미늄 버전은 피부과 크림의 공기 침입을 0으로 하고, 공압출 플라스틱 버전은 무게를 줄이며 그래픽 호소를 강화합니다. 라미네이트 가공된 스퀴즈 튜브는 향료 배리어성이 우수하므로 오랄 케어의 표준으로 계속되고 있습니다.

트위스트 식 및 정밀 도포식 디자인은 복용량의 정확성이 가장 중요한 처방 피부과 및 고급 화장품에서 특별한 역할을 수행합니다. 인몰드 라벨, 폴리프로필렌 튜브 등의 혁신은 장식과 구조를 원스텝으로 통합하여 라인 효율 및 재활용성을 향상시킵니다. 밀폐 및 장식 옵션의 폭이 넓기 때문에 스퀴즈 형식은 항상 적응할 수 있으며 튜브 포장 시장에서의 리드를 확고하게 만듭니다.

지역 분석

2024년 튜브 포장 시장은 아시아태평양이 38.43%의 수량 점유율로 선도하였고, 2030년까지 CAGR 9.21%로 성장이 예상됩니다. 중국과 인도에서 FMCG의 견조한 확대, 가처분 소득 증가, 도시 지역의 라이프 스타일은 여행에 편리한 퍼스널케어 아이템과 1회분 조미료 수요를 뒷받침하고 있습니다. 베트남의 종이 부문은 2026년까지 35억 달러의 매출을 목표로 하고 있으며, 섬유 기반의 패키징을 목표로 하는 지역의 기세를 나타내고 있습니다.

북미와 유럽은 성숙하고 있지만, 보다 엄격한 재활용 목표를 다루고 있으며, 조달 전략과 자본 배분을 재구성하고 있습니다. EU의 PPWR은 컨버터에게 단일 소재 생산을 위한 라인의 개조를 강제하고 있어 수년에 걸친 오버홀에 자금을 공급할 수 있는 종합 대기업에게 유리합니다. 미국과 캐나다에서는 이산화탄소 감소에 대한 브랜드 헌신이 지역 소매점에서 재활용률이 높은 튜브를 테스트하는 파일럿 프로그램을 추진하고 있습니다.

라틴아메리카와 중동은 중산 계급 인구 증가로 패키지 식품 성장에 박차를 가하는 새로운 기회 영역입니다. 브라질의 포장 식품 시장은 2028년까지 1,686억 달러에 달할 수 있으며, 물약 제어 소스와 맛 페이스트 수요에 박차를 가하고 있습니다. 동시에 태국, 아프리카, 걸프 협력 회의에서 ALPLA의 시설 개발은 수입 관세 및 물류가 비용 부담이 되는 시장에서 현지 공급의 전략적 중요성을 강조합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 퍼스널케어 및 화장품 수요 증가

- 지속 가능한 포장에 대한 소비자 선호도 증가

- 리사이클 의무화로 단소재 튜브 증가

- 편의성 및 다양성에 대한 수요 증가

- 하이브리드 배리어 기술에 대한 세계적 FMCG CAPEX 푸시

- 시장 성장 억제요인

- 대체품의 유무

- 원재료 부족 및 비용 변동

- 시장 침투를 막는 한정된 제품 호환성

- 공급망 분석

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 원재료 분석

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 플라스틱 튜브

- 폴리에틸렌(PE) 튜브

- 폴리프로필렌(PP) 튜브

- 기타 플라스틱 튜브

- 알루미늄 튜브

- 라미네이트 튜브

- 판지 및 바이오튜브

- 플라스틱 튜브

- 패키징 유형별

- 스퀴즈 및 압출

- 트위스트

- 최종 이용 산업별

- 화장품 및 퍼스널케어

- 의약품

- 식품

- 기타 최종 이용 산업

- 유통 채널별

- 직접 판매

- 간접 판매

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- EPL Limited

- Albea Group

- Hoffmann Neopac AG

- CCL Industries Corp.

- Tubex Aluminium Tubes

- Huhtamaki Oyj

- Montebello Packaging

- LINHARDT Group GmbH

- CTLpack Group, SLU

- Plastube Inc.

- Unette Corporation

- Scandolara SpA

- Alltub Deutschland GmbH

- TUBETTIFICIO PERFEKTUP Srl

- AptarGroup Inc.

- Witoplast Kisielinscy Joint Stock Company

- Mpack Poland Sp. zoo

- Viva Healthcare Packaging

- Gp Plast Sp. z..oo

- EPL Poland Sp. zoo

- Elpes sp. zoo

- ALPLA WERKE ALWIN LEHNER GMBH and CO KG

제7장 시장 기회 및 향후 전망

AJY 25.11.21The tube packaging market size stands at 26.03 billion units in 2025 and is projected to reach 33.96 billion units by 2030, advancing at a 5.47% CAGR.

Regulatory mandates that require recyclability by 2030, combined with rising consumer demand for sustainable solutions, are compelling manufacturers to invest in mono-material and recycled-content formats. Paperboard and bio-based tubes record the fastest growth at 8.53% CAGR, while plastic formats retain volume leadership because of established processing infrastructure. End-use diversification into ready-to-eat foods and over-the-counter pharmaceuticals broadens revenue streams as brands prioritize convenience and precise dosing. Continued merger activity, led by Amcor's USD 8.4 billion combination with Berry Global, is reshaping competitive dynamics and accelerating innovation in barrier technologies that limit reliance on multi-layer plastics.

Global Tube Packaging Market Trends and Insights

Rising Demand in Personal Care and Cosmetics

Beauty brands continue to premiumize product lines, which favors tubes that protect sensitive formulations and allow controlled dispensing. Albea has trimmed concept-to-launch cycles while integrating recycled content, pursuing a 46% carbon-reduction target for 2030. Colgate's clear PET Elixir tube with EveryDrop coating improves product evacuation, underscoring user experience gains that strengthen brand loyalty. Visibility into material provenance and carbon footprint is also improving, supporting marketing narratives that resonate with eco-conscious shoppers.

Growing Consumer Preferences for Sustainable Packaging

Household-name oral care brands have shifted from composite laminates toward fully recyclable high-density polyethylene formats that can enter mainstream kerbside streams in the United Kingdom. Neopac became the first European tube maker to earn RecyClass EN 15343 certification, validating traceable recycled content and strengthening its competitive edge. Such milestones convert sustainability compliance into market differentiation, pushing the tube packaging market toward higher-value innovations.

Availability of Substitutes

Stand-up pouches, which combine light weight, easy opening, and reduced material use, are projected to hit USD 47 billion by 2029, drawing sauce and condiment brands away from tubes. MasterFoods' recyclable paper single-dose pack further illustrates how alternate formats can satisfy sustainability and portion-control priorities. These innovations pressure tube producers to highlight functional strengths, such as precise dosing and high oxygen barrier, to prevent volume erosion.

Other drivers and restraints analyzed in the detailed report include:

- Recyclability Mandates Boosting Mono-material Tubes

- Rising Demand for Convenience and Versatility

- Raw Material Shortages and Fluctuating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic formats accounted for 68.14% of tube packaging market share in 2024, supported by cost-efficient extrusion lines and universal brand familiarity. Within plastics, high-density polyethylene and polypropylene accommodate diverse viscosities, from creams to gels, ensuring cross-industry versatility. Laminates that stack polymer and aluminum layers continue to protect oral-care formulas where flavor retention is essential. Aluminum tubes, though niche, preserve volatile pharmaceutical actives and oxygen-sensitive foods, reinforcing a premium-priced foothold.

Paperboard and bio-based solutions, however, outpace the broader tube packaging market at an 8.53% CAGR as the PPWR accelerates the shift toward renewable substrates. Huhtamaki's OmniLock Ultra barrier paper delivers aluminum-like protection while remaining curbside-recyclable. Amcor's patented AmFiber Performance Paper similarly targets food and healthcare segments, proving that fiber-based structures can satisfy strict moisture limits. As adoption widens, plastic's volume lead is expected to narrow in absolute terms, even if it retains scale advantages.

Squeeze and collapsible tubes represented 65.34% of 2024 shipments and are projected to rise at a 7.43% CAGR, reflecting strong consumer affinity for one-handed dispensing. Impact-extruded aluminum versions ensure zero air ingress for dermatological creams, whereas co-extruded plastic variants lower weight and enhance graphic appeal. Laminated squeeze tubes remain the oral-care standard because of flavor-barrier proficiency.

Twist and precision-applicator designs fill specialized roles in prescription dermatology and luxury cosmetics where dosage accuracy is paramount. Innovations such as in-mold-label polypropylene tubes merge decoration and structure in a single step, improving line efficiency and recyclability. The breadth of sealing and decoration options keeps squeeze formats adaptable, cementing their lead in the tube packaging market.

The Tube Packaging Market Report is Segmented by Product Type (Plastics Tubes, Aluminum Tubes, Laminated Tubes, Paperboard/Bio-Based Tubes), Packaging Type (Squeeze and Collapsible, Twist), End-Use Industry (Cosmetics and Personal Care, Pharmaceutical, Food, Other End-Use Industry), Distribution Channel (Direct Sales, Indirect Sales), and Geography. The Market Forecasts are Provided in Terms of Volume (Units).

Geography Analysis

Asia-Pacific led the tube packaging market in 2024 with a 38.43% volume share and is expected to advance at 9.21% CAGR through 2030. Robust FMCG expansion in China and India, higher disposable income, and urban lifestyles underpin demand for travel-friendly personal care items and single-serve condiments. Vietnam's paper segment, on course for USD 3.5 billion revenue by 2026, illustrates regional momentum toward fiber-based packaging.

North America and Europe, while mature, are navigating stricter recycling targets that reshape sourcing strategies and capital allocation. The EU PPWR compels converters to retrofit lines for mono-material output, favoring integrated giants able to fund multi-year overhauls. In the United States and Canada, brand commitments to carbon reduction drive pilot programs that test high-recycled-content tubes at regional retailers.

Latin America and the Middle East are emerging opportunity zones as rising middle-class populations fuel packaged food growth. Brazil's packaged-food market could reach USD 168.6 billion by 2028, spurring demand for portion-controlled sauces and flavored pastes. Concurrently, ALPLA's facility roll-outs in Thailand, Africa, and the Gulf Cooperation Council underline the strategic importance of local supply in markets where import duties and logistics add cost layers.

- Amcor plc

- EPL Limited

- Albea Group

- Hoffmann Neopac AG

- CCL Industries Corp.

- Tubex Aluminium Tubes

- Huhtamaki Oyj

- Montebello Packaging

- LINHARDT Group GmbH

- CTLpack Group, S.L.U.

- Plastube Inc.

- Unette Corporation

- Scandolara S.p.A.

- Alltub Deutschland GmbH

- TUBETTIFICIO PERFEKTUP S.r.l.

- AptarGroup Inc.

- Witoplast Kisielinscy Joint Stock Company

- Mpack Poland Sp. z.o.o.

- Viva Healthcare Packaging

- Gp Plast Sp. z..o.o.

- EPL Poland Sp. z.o.o.

- Elpes sp. z.o. o.

- ALPLA WERKE ALWIN LEHNER GMBH and CO KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand in Personal Care and Cosmetics

- 4.2.2 Growing consumer preferences for sustainable Packaging

- 4.2.3 Recyclability mandates boosting mono-material tubes

- 4.2.4 Rising Demand for Convenience and Versatility

- 4.2.5 Global FMCG CAPEX push into hybrid-barrier technologies

- 4.3 Market Restraints

- 4.3.1 Availability of Substitutes

- 4.3.2 Raw Material Shortages and Fluctuating cost

- 4.3.3 Limited Product Compatibility Restricting Market Penetration

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Raw Material Analysis

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Product Type

- 5.1.1 Plastics Tubes

- 5.1.1.1 Polyethylene (PE) Tubes

- 5.1.1.2 Polypropylene (PP) Tubes

- 5.1.1.3 Other Plastic Tubes

- 5.1.2 Aluminum Tubes

- 5.1.3 Laminated tubes

- 5.1.4 Paperboard/Bio- Based tubes

- 5.1.1 Plastics Tubes

- 5.2 By Packaging Type

- 5.2.1 Squeeze and Collapsible

- 5.2.2 Twist

- 5.3 By End-Use Industry

- 5.3.1 Cosmetics and Personal Care

- 5.3.2 Pharmaceutical

- 5.3.3 Food

- 5.3.4 Other End-use Industry

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 EPL Limited

- 6.4.3 Albea Group

- 6.4.4 Hoffmann Neopac AG

- 6.4.5 CCL Industries Corp.

- 6.4.6 Tubex Aluminium Tubes

- 6.4.7 Huhtamaki Oyj

- 6.4.8 Montebello Packaging

- 6.4.9 LINHARDT Group GmbH

- 6.4.10 CTLpack Group, S.L.U.

- 6.4.11 Plastube Inc.

- 6.4.12 Unette Corporation

- 6.4.13 Scandolara S.p.A.

- 6.4.14 Alltub Deutschland GmbH

- 6.4.15 TUBETTIFICIO PERFEKTUP S.r.l.

- 6.4.16 AptarGroup Inc.

- 6.4.17 Witoplast Kisielinscy Joint Stock Company

- 6.4.18 Mpack Poland Sp. z.o.o.

- 6.4.19 Viva Healthcare Packaging

- 6.4.20 Gp Plast Sp. z..o.o.

- 6.4.21 EPL Poland Sp. z.o.o.

- 6.4.22 Elpes sp. z.o. o.

- 6.4.23 ALPLA WERKE ALWIN LEHNER GMBH and CO KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment