|

시장보고서

상품코드

1639397

아시아태평양의 카본블랙 - 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Asia-Pacific Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

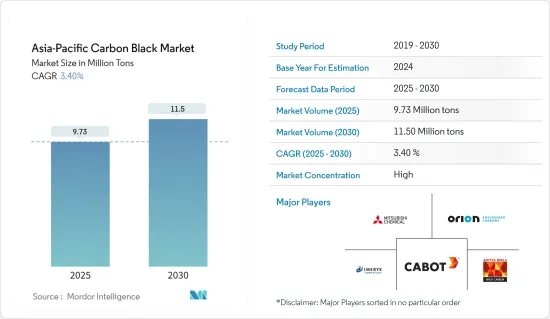

아시아태평양의 카본블랙 시장 규모는 2025년 973만 톤으로 추정되며, 2030년에는 1,150만 톤에 이를 것으로 예상됩니다. 예측 기간(2025-2030년)의 CAGR은 3.4%입니다.

시장은 COVID-19에 의해 부정적인 영향을 받았습니다. 팬데믹(세계적 유행) 시나리오로 인해 아시아태평양의 일부 국가들은 바이러스의 확산을 억제하기 위해 폐쇄 상태로 들어갔습니다. 다수의 기업과 공장이 가동 중지되어 세계 공급망이 혼란스러워 생산, 납기, 제품 판매에 타격을 주었습니다. 현재 시장은 COVID-19 팬데믹에서 회복되어 크게 증가하고 있습니다.

주요 하이라이트

- 섬유 산업에서의 용도 확대, 스페셜티 블랙 시장 침투 확대, 타이어 산업에서의 수요 급증이 시장을 견인하는 주요 요인입니다.

- 불안정한 원료 가격과 녹색 타이어의 상승이 시장 성장을 방해할 것으로 예상됩니다.

- 전기자동차 및 자율주행 차량의 보급과 인쇄 용도에서의 카본블랙 수요의 급증은 향후 수년간 시장에 기회를 가져올 것으로 예상됩니다.

아시아태평양 카본블랙 시장 동향

타이어 및 산업용 고무 제품 수요 증가

- 카본블랙은 고무 컴파운드에 첨가하여 방열 성능과 조종성, 트레드 마모, 연비를 향상시키고 있습니다. 또한 내마모성도 향상시키고 있습니다. 카본블랙은 주로 탄성률이나 인장 강도를 변화시키는 등의 보강 효과를 낳는 고무 분야 충전제로 사용됩니다. 제품의 분자간 힘 또는 응집력을 향상시키고 고무계 접착제, 실란트, 코팅제에 전도성을 부여하는 데 사용됩니다.

- 자동차 산업의 성과는 카본블랙 수요를 나타내는 중요한 지표입니다. 국제자동차공업회(OICA)에 따르면 아시아태평양의 자동차 생산대수는 2021년 기록된 4,600만대에 비해 2022년에는 7% 증가한 5,000만대에 달했습니다.

- 아시아태평양의 고무 타이어 산업을 지배하는 것은 중국과 인도입니다. 중국은 이 지역에서 가장 큰 고무 타이어 생산국이자 소비국이기도 합니다. 원료의 충분한 가용성과 정부의 지원책이 이들 국가의 타이어 고무 산업에 적극적으로 공헌하고 있습니다.

- 중국교교공업협회(CRIA)가 정식으로 발표한 고무산업 '제14차 5개년' 개발계획의 지도요강에 따르면 중국은 2025년까지 연간 7억 400만 그루의 타이어를 생산할 것으로 예측된다. 그 내역은 승용차용 레이디얼 타이어가 5억 2,700만개, 트럭·버스용 레이디얼 타이어가 1억 4,800만개, 바이어스트럭용 타이어가 2,900만개, 초대형 공업용 타이어가 2만개, 농업용 타이어 1,200만개, 항공기 타이어가 5만 4,000개입니다. 이 확대는 중국의 타이어 제품에 대한 국제 시장 수요 증가를 시사하고 있으며, 중국의 타이어 산업은 세계 시장에서 주요 진출기업으로 자리매김하고 있습니다.

- 또한 인도에서 자동차 제조가 지속적으로 증가함에 따라 다양한 타이어 제조업체들이 이 나라에 새로운 생산 시설을 투자하고 있습니다. 예를 들어, 요코하마 고무는 2022년 4월 안도라 프라데시주 비샤 카파트남에서 오프로드 타이어 생산을 시작했으며, 일일 생산 능력은 고무 무게로 69톤이 되었습니다. 이 회사는 또한 2024년까지 시작될 예정인 2기 확대 공사를 진행하고 있으며, Nissan 능력을 132톤으로 끌어올릴 예정입니다.

- 따라서, 상기 요인을 고려하면, 카본블랙 수요는 예측 기간 동안 타이어 및 산업용 고무 제품 부문으로부터 증가할 것으로 예상됩니다.

시장을 독점하는 중국

- 중국은 아시아태평양 시장에서 카본블랙의 최대 소비국입니다. 이는 자동차 부문의 카본블랙 수요 증가로 인한 것입니다. 중국의 카본블랙 시장에서 가장 큰 점유율을 차지하는 것은 타이어 용도입니다.

- 중국은 아시아태평양에서 가장 큰 타이어 생산국입니다. 그러나 국가 통계국 통계에 따르면 2022년 타이어 생산량은 8억 5,600만개로 전년 대비 5% 감소했습니다. 이 감소는 에너지·비용의 상승과 구미 국가의 교통량의 감소에 의해 2022년 후반에 수출 수요가 감소한 결과라고 생각되고 있습니다.

- 긍정적인 측면에서 중국의 자동차 생산은 현저한 성장을 보였으며 이 나라의 타이어 수요를 증가시켰습니다. OICA에 따르면 2022년 중국의 자동차 생산 대수는 2021년 대비 3% 증가했습니다.

- 페인트 시장은 하류 수요가 증가함에 따라 중국에서 급성장하고 있습니다. 건설, 자동차, 산업 섹터의 활황은 페인트 및 코팅 시장을 뒷받침할 것으로 예상됩니다. 그 결과 예측 기간 동안 카본블랙 수요를 끌어올릴 것으로 예상됩니다.

- European Coatings에 따르면 중국에는 10,000곳에 가까운 페인트 제조업체가 있습니다. Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BAF SE, Axalta Coatings 등 세계의 주요 페인트 제조업체 중 대부분이 중국에 제조 기지를 두고 있습니다. 페인트 및 코팅 회사는 중국에 대한 투자를 점점 늘리고 있습니다.

- 예를 들어 BASF SE는 2022년 7월 자회사인 BASF Coatings(Guangdong)(BCG)를 통해 중국 남부의 광동성 장문시에 있는 이 회사의 도료 거점에서 자동차용 재도장 도료의 제조 능력을 확대했습니다. 이 회사는 이 확장 프로젝트를 통해 생산 능력을 연간 30킬로톤으로 강화했습니다.

- 다양한 최종사용자 산업에서의 수요가 증가하고 있기 때문에 카본블랙 제조업체는 새로운 생산 시설을 설립하거나 기존의 생산 시설을 확대하고 있습니다. 그러므로 이러한 추세는 향후 몇 년동안 중국의 카본블랙 수요를 증가시킬 것으로 예상됩니다.

아시아태평양 카본블랙 산업 개요

아시아태평양 카본블랙 시장은 통합된 특성을 가지고 있습니다. 주요 기업에는 Cabot Corporation, Mitsubishi Chemical Group Corporation, Orion Engineered Carbons, Imerys, Birla Carbon 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 섬유 산업에서의 용도 확대

- 스페셜티 블랙 시장 침투 증가

- 타이어 산업에서의 수요 급증

- 억제요인

- 불안정한 원료 가격

- 친환경 타이어의 상승

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(규모별)

- 프로세스 유형

- 퍼니스 블랙

- 가스 블랙

- 램프 블랙

- 서멀 블랙

- 용도

- 타이어 및 산업용 고무 제품

- 플라스틱

- 토너와 인쇄 잉크

- 코팅

- 섬유

- 기타 용도(전력, 절연, 건축 등)

- 지역

- 중국

- 인도

- 일본

- 한국

- 아세안 국가

- 기타 아시아태평양

제6장 경쟁 구도

- 인수합병, 합작사업, 제휴, 협정

- 시장 점유율 분석**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Birla Carbon

- Bridgestone Corporation

- Cabot Corporation

- Cancarb Limited

- Continental Carbon Company

- Epsilon Carbon Private Limited

- Himadri Specialty Chemical Ltd

- Imerys

- Longxing Chemical Stock Co. Ltd

- Mitsubishi Chemical Group Corporation

- OCI COMPANY Ltd

- Orion Engineered Carbons

- PCBL(Phillips Carbon Black Limited)

- Shandong Huadong Rubber Materials Co., Ltd.

- Tokai Carbon Co. Ltd

제7장 시장 기회와 앞으로의 동향

- 전기차와 자율주행차의 보급 확대

- 인쇄 잉크 용도의 수요 급증

The Asia-Pacific Carbon Black Market size is estimated at 9.73 million tons in 2025, and is expected to reach 11.50 million tons by 2030, at a CAGR of 3.4% during the forecast period (2025-2030).

The market was negatively impacted due to COVID-19. Owing to the pandemic scenario, several countries in Asia-Pacific went into lockdown to curb the spread of the virus. The shutdown of numerous companies and factories disrupted worldwide supply networks and harmed production, delivery schedules, and product sales. Currently, the market recovered from the COVID-19 pandemic and is increasing significantly.

Key Highlights

- Major factors driving the market studied are growing application in fiber and textile industries, increasing market penetration of specialty black, and surge in demand from the tire industry.

- Volatile raw material prices and the rising prominence of green tires are expected to hinder the studied market's growth.

- Growth in the adoption of electric and self-driving cars and the surge in demand for carbon black in printing applications will likely create opportunities for the market in the coming years.

Asia-Pacific Carbon Black Market Trends

Increasing Demand for Tires and Industrial Rubber Products

- Carbon black improves heat-dissipation capabilities and handling, tread wear, and fuel mileage when added to rubber compounds. It also provides abrasion resistance. Carbon black is mostly used as a rubber sector filler to generate reinforcing effects, such as changing the modulus or tensile strength. It is used to improve the intermolecular or cohesive forces of the product and to provide conductivity to rubber-based adhesives, sealants, and coatings.

- The automotive industry's performance is an important indicator of the demand for carbon black. According to the International Organization of Motor Vehicle Manufacturers (OICA), automotive production in the Asia-Pacific region increased by 7% to 50 million units in 2022, compared to 46 million units recorded in 2021.

- China and India dominate the rubber and tire industry in the Asia-Pacific region. China is the largest producer and consumer of rubber tires in the region. Sufficient availability of raw materials and supporting government initiatives positively contribute to these countries' tire and rubber industries.

- As per the officially released guiding outline for the "14th Five-Year" Development Plan for the Rubber Industry by China Rubber Industry Association (CRIA), China is projected to produce 704 million tires annually by 2025. It includes 527 million passenger radial tires, 148 million truck/bus radial tires, 29 million bias truck tires, 20 thousand extra-large industrial tires, 12 million agricultural tires, and 54 thousand aircraft tires. This expansion suggests the international market's growing demand for China's tire products, positioning China's tire industry as a major player in the global market.

- Furthermore, due to the continuous increase in automotive manufacturing in India, various tire manufacturers are investing in new production facilities in the country. For instance, Yokohama Rubber Co. commenced production of off-road tires in Vishakhapatnam, Andhra Pradesh, in April 2022, with a daily manufacturing capacity of 69 tonnes in rubber weight. The company is also working on the second phase of expansion, expected to begin by 2024, increasing the daily capacity to 132 tonnes.

- Therefore, considering the factors above, the demand for carbon black is expected to rise from the tires and industrial rubber products segment during the forecast period.

China to Dominate the Market

- China is the largest consumer of carbon black in the Asia-Pacific market. It is due to the increasing demand for carbon black from the automotive sector. The tire application accounts for the largest share of the carbon black market in China.

- China is the largest producer of tires in the Asia-Pacific region. However, according to the statistics reported by the National Bureau of Statistics, the production of tires stood at 856 million units in 2022, showcasing a decline of 5% from the previous year. The decline is perceived as a consequence of the reduction in export demand in the second half of 2022 due to the rising energy cost and decline in traffic in Europe and American countries.

- On the positive front, automotive production in China witnessed a prominent rise which aided the demand for tires in the country. According to the OICA, automotive production in China in 2022 increased by 3% compared to 2021.

- The coatings market is growing rapidly in China, with increasing downstream demand. The booming construction, automotive, and industrial sectors will likely propel the paint and coatings market. It, in turn, is expected to boost the demand for carbon black during the forecast period.

- According to European Coatings, nearly 10,000 coatings manufacturers are located in China. Most leading global coating manufacturers, such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BAF SE, and Axalta Coatings, contain their manufacturing bases in China. Paints and coatings companies are increasingly growing investments in the country.

- For instance, in July 2022, BASF SE, through its subsidiary BASF Coatings (Guangdong) Co., Ltd. (BCG), expanded its manufacturing capabilities for automotive refinish coatings at its coatings site in Jiangmen, Guangdong Province in South China. The company increased its production capacity to 30 kilotons annually through this expansion project.

- Due to the increasing demand of various end-user industries, carbon black manufacturers are setting up new production facilities and expanding existing manufacturing facilities. Hence, such trends are expected to increase the demand for carbon black in China in the upcoming years.

Asia-Pacific Carbon Black Industry Overview

The Asia-Pacific carbon black market is consolidated in nature. The major companies (in noy any particular order) include Cabot Corporation, Mitsubishi Chemical Group Corporation, Orion Engineered Carbons, Imerys, and Birla Carbon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Application in Fiber and Textile Industries

- 4.1.2 Increasing Market Penetration of Specialty Black

- 4.1.3 Surge in Demand from Tire Industry

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Rising Prominence of Green Tires

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Process Type

- 5.1.1 Furnace Black

- 5.1.2 Gas Black

- 5.1.3 Lamp Black

- 5.1.4 Thermal Black

- 5.2 Application

- 5.2.1 Tires and Industrial Rubber Products

- 5.2.2 Plastics

- 5.2.3 Toners and Printing Inks

- 5.2.4 Coatings

- 5.2.5 Textile Fibers

- 5.2.6 Other Applications (Power, Insulation, Construction, etc.)

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 ASEAN Countries

- 5.3.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Birla Carbon

- 6.4.2 Bridgestone Corporation

- 6.4.3 Cabot Corporation

- 6.4.4 Cancarb Limited

- 6.4.5 Continental Carbon Company

- 6.4.6 Epsilon Carbon Private Limited

- 6.4.7 Himadri Specialty Chemical Ltd

- 6.4.8 Imerys

- 6.4.9 Longxing Chemical Stock Co. Ltd

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 OCI COMPANY Ltd

- 6.4.12 Orion Engineered Carbons

- 6.4.13 PCBL (Phillips Carbon Black Limited)

- 6.4.14 Shandong Huadong Rubber Materials Co., Ltd.

- 6.4.15 Tokai Carbon Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth in the Adoption of Electric Cars and Self-driving Cars

- 7.2 Surge in Demand for Printing Inks Application