|

시장보고서

상품코드

1639455

포화 폴리에스테르 수지 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Saturated Polyester Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

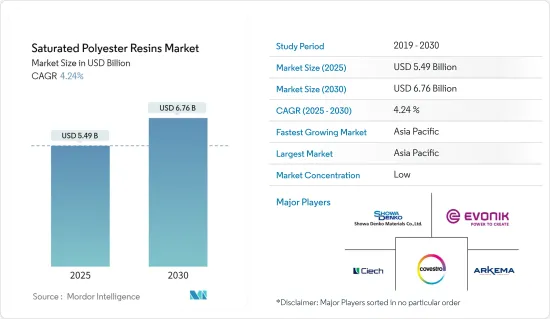

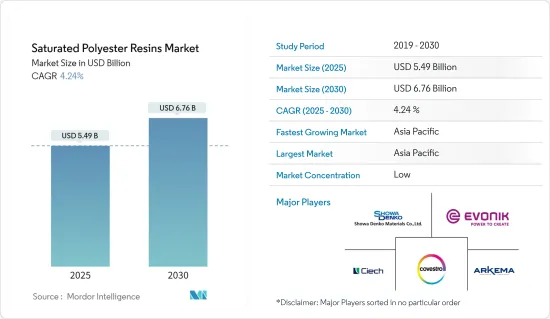

포화 폴리에스테르 수지 시장 규모는 2025년에 54억 9,000만 달러로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 4.24%로, 2030년에는 67억 6,000만 달러에 달할 것으로 예상됩니다.

COVID-19의 대유행 중 포화 폴리에스테르 수지 시장은 세계 각국에서의 조업과 공급 체인의 제한에 의해 침체를 경험했습니다. 이러한 요인은 페인트 및 코팅 산업과 같은 주요 최종 사용자 수요에 부정적인 영향을 미쳤습니다. 그러나 2021년 규제가 완화되면서 폴리에스테르 수지 수요는 팬데믹 전 수준까지 상승했습니다.

주요 하이라이트

- 중기적으로 시장 성장을 견인하는 주요 요인은 기계적 특성이 우수하기 때문에 대체품에 비해 성능이 우수하다는 것입니다.

- 그 반면, 포화 폴리에스테르 수지의 가공·제조 비용이 높은 것이 시장 성장의 방해가 될 것으로 예상됩니다.

- 비 BPA 캔 코팅의 동향은 포화 폴리에스테르 수지에 새로운 성장 기회를 가져옵니다.

- 아시아태평양은 시장을 독점하고 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

포화 폴리에스테르 수지 시장 동향

분말 코팅 수요 증가

- 포화 폴리에스테르 수지는 주로 무용제 분말 코팅 및 코팅제의 제조에 사용됩니다. 뛰어난 내후성, 우수한 충격 강도, 금속에 대한 접착성(습도가 높은 조건 하에서도) 등의 우수한 특성을 가지는 포화 폴리에스테르 수지는 외장이나 내장의 건축 용도, 기계, 소비자용 전자 기기, 스틸 가구, 원예 도구의 도장에 선호됩니다.

- 전 세계적으로 전자 산업에서의 기술 발전과 R&D 활동의 급속한 혁신 속도가 보다 새롭고 빠르며 신뢰성이 높은 전자 제품에 대한 수요를 이끌어 가고 있기 때문에 코팅 부품의 요구가 높아지고 있습니다.

- 일본전자정보기술산업협회(JEITA)에 따르면 세계 일렉트로닉스·IT산업의 생산액은 2021년 3조 3,600억 달러에 대해 2022년에는 전년대비 1%의 성장률을 기록해 3조 4,400억 달러에 달할 것으로 추정됩니다. 게다가 2023년에는 전년 대비 3%의 성장이 전망되고 있습니다. 소비자 기술 협회에 따르면 미국의 소비자 전자 장치 또는 기술 판매 소매 매출은 2021년 4,610억 달러에 비해 2022년에는 5,050억 달러에 달할 것으로 추정됩니다.

- 유럽에서는 독일의 전자 산업이 지역 최대입니다. ZVEI에 따르면 독일의 전자 디지털 산업 매출은 2022년 11월에 211억 유로(217억 달러)를 차지했으며 2021년 11월에 비해 14.4%의 성장률을 기록했습니다.

- 유사하게, 성장하는 건설 부문은 포화 폴리에스테르 수지를 사용하여 제조된 무용제 분말 도료의 사용을 촉진할 것으로 예상됩니다. 이에 따라 예측기간 동안 조사된 시장의 성장을 뒷받침하고 있습니다.

- 건설 부문은 아시아태평양, 중동 및 아프리카에서 강력한 성장을 이루고 있습니다. 중동 및 아프리카에서는 각국 정부가 비석유 부문 개발에 주력하고 있습니다. 예를 들어 사우디아라비아 정부는 경제 변혁 계획 '비전 2030'하에 수많은 인프라 프로젝트를 시작했습니다. 이 프로젝트는 주로 전력, 물, 탄화수소, 건설, 도로, 철도, 항만, 공항의 각 부문에 관한 것입니다.

- 따라서 다양한 최종사용자 산업으로부터의 분체도료 수요가 견조하게 성장하고 있으며, 포화 폴리에스테르 수지 수요를 견인할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

- 아시아태평양은 중국, 인도, 일본과 같은 경제권에서의 수요가 증가하고 있기 때문에 점유율로 세계 시장을 독점하고 있습니다.

- 아시아태평양은 예측 기간 동안 포화 폴리에스테르 수지 수요가 건전하게 성장할 것으로 기대되고 있습니다. 이는 이 지역의 건설, 자동차, 일렉트로닉스 산업 등에 있어서의 페인트 및 코팅 용도의 현저한 성장이 예상되기 때문입니다.

- 2022년 2월, 국가개발회의(NDC)에 따르면 중국 정부 기관은 1,800억 대만 달러(64억 7,000만 달러)의 인프라 개발 계획을 제안했습니다. 이 계획에는 2023-2024년에 걸쳐 사용되는 '미래를 전망한 인프라 개발 계획'의 4단계 예산안이 포함되어 있습니다.

- 중국에서는 2021년에 완성된 개발 중 주택이 가장 큰 비율을 차지했습니다. 주택용 건축물은 완성 바닥 면적의 67% 이상을 차지했습니다. 경제 성장에 따라 농촌에서 도시로 이동하는 사람들이 늘어나고 주택에 대한 요구가 커지고 있습니다. 또한 중국에는 세계 최대 건설 시장이 있으며 전 세계 건설 투자의 20%를 차지합니다. 중국은 2030년까지 약 13조 달러를 건축물에 투입할 것으로 예상되고 있으며, 세계 포화 폴리에스테르 수지 시장에 있어서 밝은 시장 전망이 되고 있습니다.

- 아시아태평양은 세계에서 가장 가치있는 자동차 제조 업체의 본거지입니다. 중국, 인도, 일본, 한국 등의 신흥 국가들이 그 거점이 되고 있습니다. 포화 폴리에스테르 수지를 베이스로 한 도료나 코팅제는 금속 표면에 높은 접착성을 가지므로 자동차 산업에서의 사용이 증가하고 있습니다.

- 중국 기차공업협회(CAAM)에 따르면 중국은 세계 최대의 자동차 생산 거점으로 2022년 자동차 총 생산 대수는 2,700만대와 지난해 2,600만대에서 3.4% 증가합니다. 게다가 2022년 첫 7개월 동안 중국은 1,457만대의 자동차를 생산해 전년대비 31.5%의 성장률을 기록했습니다. 게다가 2022년 7월 배터리 전기자동차의 대수는 2021년 1-7월에 비해 117.2% 증가했습니다. 2022년 7월 일본의 전기차 판매량은 약 61만 7,000대로 추정됩니다.

- 또한 인도에서는 인도 자동차 공업회(SIAM)에 따르면 2021-22년도(2021년 4월-2022년 3월)의 자동차 생산 대수는 2020년 4월-2021년 3월 2,266만대에 대조적으로 2,203만대였습니다. 또한 인도 경제 모니터링 센터(CMIE)에 따르면 자동차 생산량은 2022년 6월 16만 9,520대에서 2022년 7월 19만 3,630대로 증가했습니다. 이러한 요인이 조사 대상 시장 수요를 증가시킬 것으로 보입니다.

- 위의 요인은 예측 기간 동안이 지역에서 포화 폴리에스테르 수지 수요를 촉진할 것으로 예상됩니다.

포화 폴리에스테르 수지 산업 개요

포화 폴리에스테르 수지 시장은 부분적으로 분할되어 있으며 주요 기업이 차지하는 비율은 적습니다. 이 선도 기업은 Arkema Group, Covestro AG, Showa Denko Materials, Evonik Industries AG, CIECH SA를 포함합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 포장 산업에서의 수요 증가

- 아시아태평양과 중동 유럽의 급속한 산업화

- 기타 촉진요인

- 억제요인

- 높은 가공·제조 비용

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(규모별)

- 유형

- 액상 포화 폴리에스테르 수지

- 고형 포화 수지

- 용도

- 분말 코팅

- 코일 및 캔 도료

- 자동차용 도료

- 포장용 도료

- 공업용 도료

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 인수합병, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- ALLNEX GMBH

- Arkema Group

- CIECH SA

- Covestro AG

- DIC CORPORATION

- Eternal Materials Co. Ltd

- Evonik Industries AG

- Showa Denko Materials Co. Ltd

- Hitech Industries FZE

- Hexion

- Novaresine SRL

- DSM

- Sir Industriale

- Stepan Company

- Nippon Gohsei

제7장 시장 기회와 앞으로의 동향

- 낮은 VOC 배출에 의한 포화 폴리에스테르 수지의 사용 증가

- 기타 기회

The Saturated Polyester Resins Market size is estimated at USD 5.49 billion in 2025, and is expected to reach USD 6.76 billion by 2030, at a CAGR of 4.24% during the forecast period (2025-2030).

During the COVID-19 pandemic, the saturated polyester resin market witnessed a downturn due to operational and supply chain restrictions in various countries across the globe. Factors like these negatively impacted the demand from key end users like Paints and Coatings industry, among others. However, as the restriction eased in 2021, the demand for polyester resin rose to pre-pandemic levels.

Key Highlights

- Over the medium term, the major factor driving the market's growth is their better performance compared to their alternatives because of their superior mechanical properties.

- On the flip side, the high processing and manufacturing cost of saturated polyester resins is expected to hinder the studied market's growth.

- The growing trend of non-BPA can coatings creates new growth opportunities for saturated polyester resins.

- The Asia-Pacific region is expected to dominate the market and will likely witness the highest CAGR during the forecast period.

Saturated Polyester Resins Market Trends

Increasing Demand for Powder Coatings

- Saturated polyester resins are primarily used to manufacture solvent-free powder paints and coatings. Its superior properties, such as good weather resistivity, excellent impact strength, and adhesion to metals (even under humid conditions), saturated polyester resins are favored for exterior and interior architectural applications, coating machinery, domestic appliances, steel furniture, and garden tools.

- Globally the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer, faster, and more reliable electronic products, thus increasing the need for coated components.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3.44 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021. Moreover, the industry is expected to grow by 3% year on year by 2023. According to the Consumer Technology Association, the retail revenue from consumer electronics or technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021.

- In Europe, the German electronics industry is the largest in the region. According to the ZVEI, Germany's electro and digital industry turnover accounted for EUR 21.1 billion (USD 21.7 billion) in November 2022, witnessing a growth rate of 14.4% compared to November 2021.

- Similarly, the growing construction sector is expected to drive the usage of solvent-free powder coatings manufactured using saturated polyester resins. It is thereby boosting the growth of the market studied during the forecast period.

- The construction sector is witnessing robust growth in Asia-Pacific, Middle East & Africa. In the Middle East & Africa region, governments are trying to develop the non-oil sectors. For Instance, Under the Vision 2030 economic transformation plan, the Saudi Arabian government initiated numerous infrastructure projects. These projects majorly cover projects related to the power, water, hydrocarbons, construction, road, rail, seaport, and airport sectors.

- Hence, the robust growth in the demand for powder coatings from various end-user industries is expected to drive the demand for saturated polyester resins.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market in terms of share, owing to the growing demand from economies like China, India, and Japan.

- Asia-Pacific is expected to witness healthy growth in the demand for saturated polyester resins during the forecast period. It is due to the expected noticeable growth of paints and coatings applications in industries like construction, automotive, and electronics industries, among others in the region.

- In February 2022, the Chinese government agencies proposed a TWD 180 billion (USD 6.47 billion) infrastructure development plan, according to the National Development Council (NDC). It includes the proposed budget for the fourth stage of the Forward-looking Infrastructure Development Program would be used from 2023-2024.

- In China, residential buildings comprised the largest portion of finished development in 2021. Construction intended for housing accounted for over 67% of the completed floor space. As the economy grows, more people move from rural to urban regions, increasing the need for residential accommodation. In addition, the country includes the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for the global saturated polyester resins market.

- The Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, South Korea. As paints and coatings based on saturated polyester resins offer high adhesion to metallic surfaces, These are increasingly used in the automotive industry.

- According to the China Association of Automobile Manufacturers (CAAM), China contains the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year. Further, in the first 7 months of 2022, the country produced 14.57 million units of cars, registering a growth rate of 31.5% Year on Year. Furthermore, in July 2022, the number of battery-powered electric vehicles increased by 117.2% compared to January-July in 2021. In July 2022, the country's electric vehicle sales were estimated at around 617 thousand units.

- Moreover, in India, during FY 2021-22 (April 2021 to March 2022), according to the Society of Indian Automobile Manufacturers (SIAM), the country's automotive industry produced a total of 22.03 million vehicles compared to 22.66 million units during April 2020 to March 2021. Further, according to the Centre for Monitoring Indian Economy (CMIE), car production increased to 193.63 thousand units in July 2022 from 169.52 thousand units in June 2022. Such factors are likely to increase the demand for the studied market

- The factors above are expected to drive the demand for saturated polyester resins in the region during the forecast period.

Saturated Polyester Resins Industry Overview

The saturated polyester resins market is partially fragmented, with the top players accounting for a small chunk of the market. These major players include Arkema Group, Covestro AG, Showa Denko Materials Co. Ltd, Evonik Industries AG, and CIECH SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Packaging Industry

- 4.1.2 Rapid Industrialization in Asia-Pacific and Central and Eastern Europe

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Processing and Manufacturing Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Liquid Saturated Polyester Resin

- 5.1.2 Solid Saturated Resin

- 5.2 Application

- 5.2.1 Powder Coatings

- 5.2.2 Coil and Can Coatings

- 5.2.3 Automotive Paints

- 5.2.4 Packaging

- 5.2.5 Industrial Paints

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ALLNEX GMBH

- 6.4.2 Arkema Group

- 6.4.3 CIECH SA

- 6.4.4 Covestro AG

- 6.4.5 DIC CORPORATION

- 6.4.6 Eternal Materials Co. Ltd

- 6.4.7 Evonik Industries AG

- 6.4.8 Showa Denko Materials Co. Ltd

- 6.4.9 Hitech Industries FZE

- 6.4.10 Hexion

- 6.4.11 Novaresine SRL

- 6.4.12 DSM

- 6.4.13 Sir Industriale

- 6.4.14 Stepan Company

- 6.4.15 Nippon Gohsei

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Usage of Saturated Polyester Resins Due to Low VOC Emissions

- 7.2 Other Opportunities