|

시장보고서

상품코드

1639517

코일 코팅 시장 전망 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Coil Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

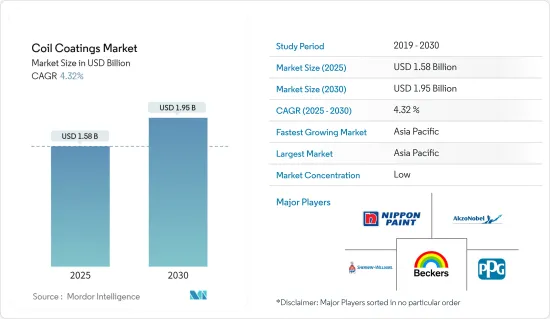

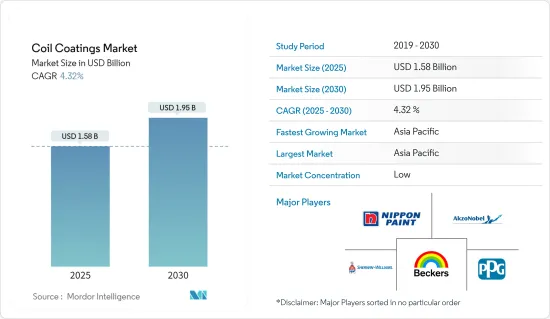

코일 코팅 시장 규모는 2025년에 15억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 4.32%를 나타낼 전망이며, 2030년에는 19억 5,000만 달러에 달할 것으로 예측됩니다.

코로나19 팬데믹은 시장에 부정적인 영향을 미쳤습니다. 팬데믹은 전 세계 건물 건설 및 엔지니어링 프로젝트를 여러 가지 방식으로 위협했고, 많은 프로젝트가 폐쇄되거나 중단되어 팬데믹 위기 동안 코일 코팅 시장의 성장이 둔화되었습니다. 그러나 2021년에는 업계가 회복세를 보이며 연구 대상 시장에 대한 수요가 반등했습니다.

주요 하이라이트

- 단기적으로는 건축 및 건설 산업의 수요 증가와 환경 영향의 증가, 기술 발전이 연구 시장을 이끄는 주요 요인입니다.

- 반대로 자동차 산업에서 경량 재료에 대한 수요 증가는 시장 성장을 방해할 것으로 예상됩니다.

- 그러나, 건축 용도의 불소 수지 코팅에 대한 수요 증가는 기회로 작용할 가능성이 높습니다.

- 아시아태평양은 완제품 철강의 높은 생산량과 최종 사용자 제품의 높은 제조로 인해이 지역의 사전 코팅 된 금속판의 생산 및 수출이 증가하여 소비 측면에서 시장을 지배했습니다.

코일 코팅 시장 동향

건축 및 건설 업계로부터 수요 증가

- 건축 및 건설 산업은 코일 코팅의 가장 큰 소비처입니다. 건축에 광범위하게 사용되는 주요 수지는 폴리에스테르 수지, 실리콘 변성 폴리에스테르, 폴리비닐리덴 플루오르화물(PVDF) 또는 불소 중합체입니다. 에너지 효율적인 구조를 장려하는 건축법이 증가함에 따라 주택 건설업체와 소비자는 장기적으로 성능과 에너지 절감을 제공하는 건축 전략으로 점차 이동하고 있습니다.

- 건설 업계의 수요 증가는 코일 코팅 시장을 이끄는 핵심 요소입니다. 전 세계에서 진행 중인 대형 건물 건설 프로젝트 중에는 2025년 1분기에 완공될 것으로 예상되는 10억 달러 규모의 텍사스 매그놀리아 복합단지 프로젝트가 있습니다. 일본 도쿄의 미나미코이와 6초메 1지구 도시 재개발 프로젝트도 2026년에 완공될 것으로 예상되는 또 다른 프로젝트입니다. 따라서 이러한 건설 프로젝트에는 지붕, 강철 문, 알루미늄 패널, 고무, 금속 라미네이션 본딩, 리노베이션 공사 등에 코일 제품이 사용될 것으로 예상됩니다.

- 또한 코일 코팅은 가단성으로 인해 실내 및 외부 건설 응용 분야에도 널리 사용됩니다. 주택 건설업자와 소비자는 성능과 장기적인 에너지 절약을 제공하는 건축 기술로 점점 더 변화하고 있습니다. 따라서 에너지 효율적인 구조의 개발에 주력하고 있습니다.

- 코일 코팅은 건물의 실내 온도를 낮추는 데 도움이 되는 적외선 반사 안료 기술을 제공합니다. 이 기술은 냉방에 소비되는 에너지를 줄여주기 때문에 코일 코팅은 에너지 효율이 높아 건축 및 건설 작업에 사용되는 코일 제품에 선호되고 있습니다. 또한 방수 설치를 위한 거터와 다운스파우트 건설에도 사용됩니다.

- 북미의 건설 산업은 상업용 부동산 부문의 개선과 공공 건설 및 기관 건물에 대한 연방 및 주정부의 투자 증가로 인해 꾸준히 성장하고 있습니다. 북미의 주요 건물 건설 프로젝트에는 25억 달러 규모의 이스트 리버 복합 용도 개발 프로젝트가 있습니다. 이 프로젝트는 2040년에 완공될 예정인 텍사스에 더 나은 주거 및 사무실 시설을 제공하는 것을 목표로 합니다. 따라서 건축 및 건설 산업의 투자 증가는 코일 코팅에 대한 상승 여력을 창출할 것으로 예상됩니다.

- 프랑스, 독일, 영국, 이탈리아 등 주요 서유럽 국가들이 코일 코팅 시장에 적극적으로 기여하고 있습니다. 이 지역에서 건물 건설 활동이 증가함에 따라 코일 코팅에 대한 수요가 크게 증가했습니다. 예를 들어, Trading Economics에 따르면 프랑스의 건설 생산량은 2022년 7월에 비해 2022년 12월에 3.1% 증가했습니다.

- 게다가 코일 코팅은 고급스러운 미관과 오래 지속되는 가치로 인해 건축 및 건설 산업에서 천장 그리드, 문, 지붕 및 사이딩, 창문 등에 사용됩니다. 현재 진행 중인 건설 프로젝트에는 미국 워싱턴주 벨뷰에 25층 규모의 오피스 타워를 건설하는 4억 7,600만 달러 규모의 에잇 오피스 타워 프로젝트가 있습니다. 이 프로젝트는 2024년에 완공될 예정입니다. 일본 도쿄의 31억 7,000만 달러 규모의 하마마츠초 시바우라 1초메 재개발 프로젝트도 진행 중인 프로젝트입니다.

- 이 프로젝트는 두 개의 건물을 건설하는 것으로 2030년까지 완공될 예정입니다. 호주에서 8억 4,100만 달러 규모의 엘리자베스 키 5부두 및 6부두 복합단지 건설 프로젝트는 2025년에 완공될 것으로 예상되는 또 다른 프로젝트입니다. 이러한 프로젝트는 향후 주거용 및 상업용 건물 건설에서 프리코팅 금속에 대한 수요를 증가시킬 것으로 예상됩니다.

- 이러한 요인으로부터 건축 및 건설 업계의 코일 코팅 시장은 예측 기간 중에 안정된 성장이 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양 지역은 전 세계 시장 점유율에서 압도적인 우위를 점하고 있습니다. 코일 코팅은 고급스러운 미관과 오래 지속되는 가치로 인해 천장 그리드, 문, 지붕 및 사이딩, 창문 등의 건축 및 건설 산업에서 사용됩니다.

- 아시아태평양의 코일 코팅 시장은 예측 기간 동안 크게 성장할 것으로 예상되며, 중국이 건설 확대와 빠른 산업 발전으로 인해 시장을 주도할 것으로 전망됩니다. 이 지역의 건물 건설 및 리노베이션 활동이 증가함에 따라 코일 코팅의 소비가 급증할 것으로 예상됩니다.

- 예를 들어, 아시아태평양지역에서 진행 중인 건물 건설 프로젝트에는 2030년 완공 예정인 31억 7천만 달러 규모의 일본 도쿄 하마마츠초 시바우라 1 초메 재개발 프로젝트가 있습니다. 또 다른 프로젝트는 중국 우한에 포선 번드 센터 T1을 건설하는 우한 포선 번드 센터 T1 프로젝트입니다. 따라서 건물 건설 프로젝트의 증가는 이 지역에서 코일 코팅의 성장을 견인할 것으로 예상됩니다.

- 또한 운송 차량에 대한 수요 증가가 코일 코팅 시장을 견인하고 있습니다. 2023년 인도의 자동차 부문은 강력한 수요와 대중교통보다 개인 차량을 선호하는 소비자들의 선호로 인해 아시아 태평양 지역에서 가장 강력한 시장이 될 것으로 예상됩니다. 예를 들어, OICA에 따르면 2022년 인도의 자동차 생산량은 5,456,857대로 2020년에 비해 24% 증가할 것으로 예상됩니다. 따라서 이 지역의 코일 코팅 산업은 전반적인 자동차 제조의 증가로 인해 확장될 가능성이 높습니다.

- 이러한 모든 요인들이 이 지역의 코일 코팅에 대한 수요를 증가시킬 것으로 예상됩니다.

코일 코팅 산업 개요

코일 코팅 시장은 세분화되어 있습니다. 이 시장의 주요 기업(특정한 순서 없음)에는 Akzo Nobel NV, Beckers Group, PPG Industries, Inc., The Sherwin-Williams Company, 일본 페인트 홀딩스 등이 포함됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 건축 및 건설 업계로부터 높은 수요

- 환경 영향의 확대와 기술의 진보

- 기타 촉진요인

- 억제요인

- 자동차 산업에 있어서의 경량 재료 수요 증가

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

- 수지 유형별

- 폴리에스테르

- 폴리불화비닐리덴(PVDF)

- 폴리우레탄(PU)

- 플라스티졸

- 기타 수지 유형

- 최종 사용자 산업별

- 건축 및 건설

- 산업 및 가정용 가전제품

- 수송

- 가구

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율 분석, 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- 코일 코터

- ArcelorMittal

- Arconic

- BDM Coil Coaters

- CENTRIA

- Chemcoaters

- Dura Coat Products

- Goldin Metals Inc.

- Jupiter Aluminum Corporation

- Norsk Hydro ASA

- Novelis

- Ralco Steels

- Rautaruukki Corporation

- Salzgitter Flachstahl GmbH

- Tata Steel

- Tekno Kroma

- thyssenkrupp AG

- UNICOIL

- United States Steel Corporation

- 페인트 공급업체

- Akzo Nobel NV

- Axalta Coatings System LLC

- Beckers Group

- Brillux GmbH & Co. KG

- Hempel A/S

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd

- NOROO Coil Coatings Co., Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Yung Chi Paint & Varnish Mfg Co. Ltd

- 전처리, 수지, 안료, 기기

- Arkema

- Bayer AG

- Covestro AG

- Evonik Industries AG

- Henkel AG & Co. KgaA

- Solvay

- Wacker Chemie AG

- 코일 코터

제7장 시장 기회와 앞으로의 동향

- 건축 용도에서의 불소 수지 코팅 수요 증가

- 기타 기회

The Coil Coatings Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 1.95 billion by 2030, at a CAGR of 4.32% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. The pandemic jeopardized building construction and engineering projects worldwide in numerous ways, and many projects were closed or halted, decelerating the growth of the coil coatings market during the pandemic crisis. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, rising demand from the building and construction industry and growing environmental influences, and advancing technology are the major factors driving the market studied.

- Conversely, increasing demand for lightweight materials in the automobile industry is expected to hinder the studied market's growth.

- However, increasing demand for fluoropolymer coatings for architectural applications will likely act as an opportunity.

- Asia-Pacific dominated the market in terms of consumption due to the rise in the production and export of pre-coated metal sheets in the region due to the high production of finished steel and the high manufacturing of end-user products.

Coil Coatings Market Trends

Rising Demand from the Building and Construction Industry

- The building and construction industry is by far the largest consumer of coil coatings. The main resins used extensively in construction are polyester resin, silicone-modified polyester, polyvinylidene fluorides (PVDF), or fluoropolymer. With the rising number of building codes that promote energy-efficient structures, home builders and consumers are gradually moving toward building strategies that deliver performance and energy savings in the long run.

- The rising demand from the construction industry is a key factor driving the coil coatings market. Some of the large ongoing building construction projects worldwide include the Magnolia Mixed-Use Complex project worth USD 1 billion in Texas, which is expected to be completed in Q1 2025. The Minamikoiwa 6-Chome District Type One Urban Redevelopment project in Tokyo, Japan, is another project expected to be completed in 2026. Thus, such construction projects are estimated to use coil products for roofing, steel doors, aluminum panels, rubber, metal lamination bonding, renovation work, and others.

- Furthermore, coil coatings are also widely used for interior and exterior construction applications due to their malleability. Home builders and consumers increasingly shift towards building techniques that impart performance and long-term energy savings. Hence, they are focusing on developing energy-efficient structures.

- Coil coatings provide infrared reflective pigment technology that helps in lowering the indoor temperature of the building. This technique reduces the energy consumed for cooling, making coil coatings energy efficient and the preferred choice for coil products used in building and construction work. It is also utilized to construct gutters and downspouts for waterproof installations.

- The construction industry in North America is growing steadily due to the improving commercial real estate sector and increased federal and state investment in public construction and institutional buildings. Some of North America's major building construction projects include the East River Mixed-Use Development project worth USD 2.5 billion. The project aims to provide better residential and office facilities in Texas, which is expected to be completed in 2040. Therefore, increasing building and construction industry investments are expected to create an upside for coil coatings.

- The major Western European countries, including France, Germany, the United Kingdom, and Italy, are actively contributing to the coil coatings market. With growing building construction activities in the region, the demand for coil coatings increased significantly. For instance, according to Trading Economics, construction output in France increased by 3.1% in December 2022 compared to July 2022.

- Moreover, due to its high-end aesthetics and long-lasting value, coil coatings are used in the building and construction industry in ceiling grids, doors, roofing and siding, windows, etc. Some of the ongoing construction projects include the Eight Office Tower project worth USD 476 million, which involves the construction of a 25-story office tower in Bellevue, Washington, United States. It is expected to be completed in 2024. The Hamamatsucho Shibaura 1 Chome Redevelopment Project, worth USD 3.17 billion in Tokyo, Japan, is another ongoing project.

- The project involves the construction of two buildings and is expected to be finished by 2030. The Elizabeth Quay Lot V and Lot VI Mixed-Use Complex construction project worth USD 841 million in Australia is yet another project likely to be completed in 2025. These projects are expected to increase the demand for pre-coated metals in the construction of residential and commercial buildings in the coming years.

- Due to all such factors, the building and construction industry's coil coatings market is expected to grow steadily during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market share. Due to their high-end aesthetics and long-lasting value, coil coatings are used in the building and construction industry in ceiling grids, doors, roofing and siding, windows, etc.

- The Asia-Pacific coil coatings market is anticipated to grow significantly during the forecast period, with China leading the market owing to expanding construction and rapid industrial development. The growing building construction and renovation activities in the region are expected to surge the consumption of coil coatings.

- For instance, some of the ongoing building construction projects in the Asia-Pacific include the Hamamatsucho Shibaura 1 Chome Redevelopment project worth USD 3.17 billion, expected to be completed in 2030 in Tokyo, Japan. Another such project is the Wuhan Fosun Bund Center T1 project, which involves the construction of the Fosun Bund Center T1 in Wuhan, China. Therefore, increasing building construction projects are expected to drive the growth of coil coatings in the region.

- Furthermore, the growing demand for transport vehicles is driving the coil coatings market. In 2023, India's automotive sector is predicted to be the strongest in the Asia-Pacific region, owing to strong demand and consumers' preference for personal vehicles over public transportation. For instance, according to OICA, in 2022, automobile production in the country amounted to 5,456,857 units, which showed an increase of 24% compared to 2020. Therefore, the region's coil coatings industry will likely expand due to the rise in overall automobile manufacturing.

- All such factors are expected to increase the demand for coil coatings in the region.

Coil Coatings Industry Overview

The coil coatings market is fragmented in nature. The major players in this market (not in a particular order) include Akzo Nobel N.V., Beckers Group, PPG Industries, Inc., The Sherwin-Williams Company, and Nippon Paint Holdings Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Building and Construction Industry

- 4.1.2 Growing Environmental Influences and Advancing Technology

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Demand for Lightweight Materials in Automotive Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin Type

- 5.1.1 Polyester

- 5.1.2 Polyvinylidene Fluorides (PVDF)

- 5.1.3 Polyurethane(PU)

- 5.1.4 Plastisols

- 5.1.5 Other Resin Types

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Industrial and Domestic Appliances

- 5.2.3 Transportation

- 5.2.4 Furniture

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Coil Coaters

- 6.4.1.1 ArcelorMittal

- 6.4.1.2 Arconic

- 6.4.1.3 BDM Coil Coaters

- 6.4.1.4 CENTRIA

- 6.4.1.5 Chemcoaters

- 6.4.1.6 Dura Coat Products

- 6.4.1.7 Goldin Metals Inc.

- 6.4.1.8 Jupiter Aluminum Corporation

- 6.4.1.9 Norsk Hydro ASA

- 6.4.1.10 Novelis

- 6.4.1.11 Ralco Steels

- 6.4.1.12 Rautaruukki Corporation

- 6.4.1.13 Salzgitter Flachstahl GmbH

- 6.4.1.14 Tata Steel

- 6.4.1.15 Tekno Kroma

- 6.4.1.16 thyssenkrupp AG

- 6.4.1.17 UNICOIL

- 6.4.1.18 United States Steel Corporation

- 6.4.2 Paint Suppliers

- 6.4.2.1 Akzo Nobel N.V.

- 6.4.2.2 Axalta Coatings System LLC

- 6.4.2.3 Beckers Group

- 6.4.2.4 Brillux GmbH & Co. KG

- 6.4.2.5 Hempel A/S

- 6.4.2.6 Kansai Paint Co.,Ltd.

- 6.4.2.7 Nippon Paint Holdings Co., Ltd

- 6.4.2.8 NOROO Coil Coatings Co., Ltd.

- 6.4.2.9 PPG Industries, Inc.

- 6.4.2.10 The Sherwin-Williams Company

- 6.4.2.11 Yung Chi Paint & Varnish Mfg Co. Ltd

- 6.4.3 Pretreatment, Resins, Pigments, Equipment

- 6.4.3.1 Arkema

- 6.4.3.2 Bayer AG

- 6.4.3.3 Covestro AG

- 6.4.3.4 Evonik Industries AG

- 6.4.3.5 Henkel AG & Co. KgaA

- 6.4.3.6 Solvay

- 6.4.3.7 Wacker Chemie AG

- 6.4.1 Coil Coaters

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Fluoropolymer Coatings for Architectural Applications

- 7.2 Other Opportunities