|

시장보고서

상품코드

1851402

클라우드 스토리지 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cloud Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

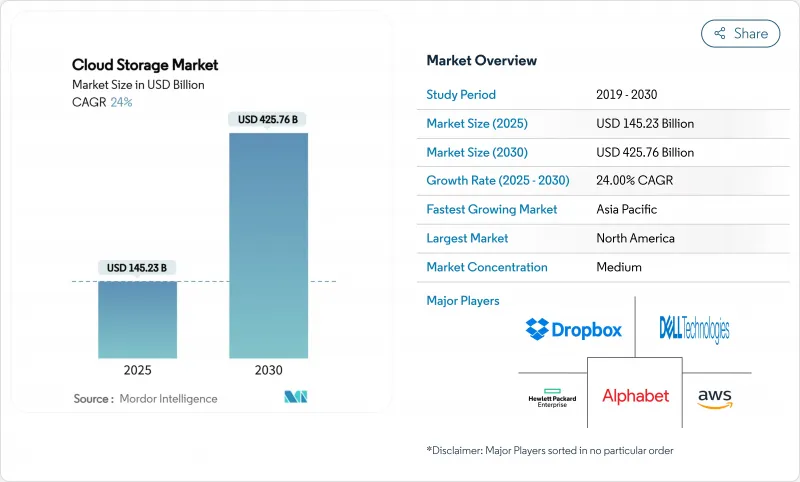

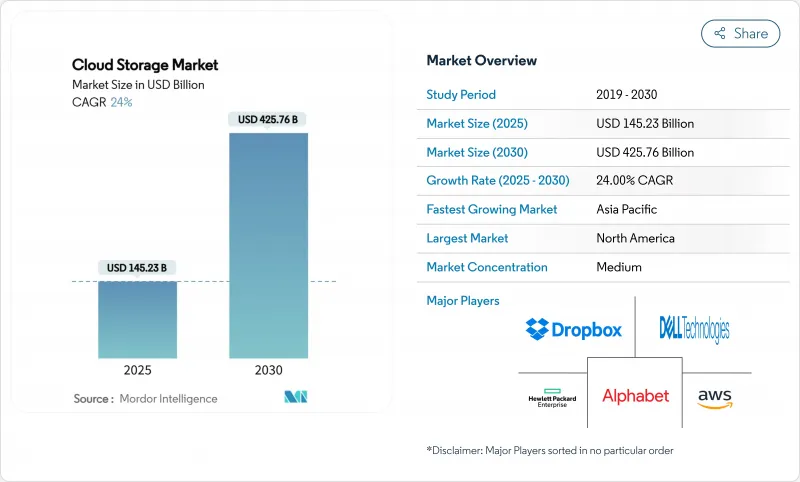

세계의 클라우드 스토리지 시장 규모는 2025년 1,452억 3,000만 달러에 이르고, 2030년까지 CAGR 24.0%로 4,257억 6,000만 달러에 이를 것으로 예측됩니다.

발전 AI 채택, 데이터 주권 의무화, 최신 에너지 효율성이 뛰어난 인프라의 필요성으로 기업의 전환이 가속화되고 세계 스토리지 아키텍처가 재구성되었습니다. 하이퍼스케일러 투자 활성화, 아시아태평양의 소버린 클라우드 지출 증가, 중소기업의 꾸준한 도입으로 세계의 대응가능 기반이 확대되는 한편, 인플레이션에 연동하는 건설 비용이 저전력 기술 혁신에 박차를 가하고 있습니다. 객체 스토리지는 AI 워크로드를 지배하고, 하이브리드 도입이 가장 빠르게 확대되고, 아시아태평양이 지역 확대를 선도하고 있습니다. AI에 최적화된 용량, 소버린 클라우드 존, 카본 어웨어 서비스를 추구하는 프로바이더의 경쟁 기업간 경쟁 관계는 여전히 높습니다.

세계 클라우드 스토리지 시장 동향과 통찰

지식 근로자용 앱의 생성형 AI 주도 데이터 폭발(2025년 이후)

일반 인공지능 워크로드는 기업 데이터의 양이 크게 증가하는 것을 보여주고 있습니다. AI 트레이닝 환경에 대한 SSD 수요는 회전 디스크가 대기 시간 목표를 충족시키는 데 어려움을 겪는 동안 연간 35% 증가하고 있습니다. 단일 트레이닝 실행을 위한 스토리지 실적는 2025년 30TB에서 2030년까지 100TB로 확장되며, 추론 노드는 신제품이 AI 기능을 통합함에 따라 더욱 빠르게 증가합니다. 비용 모델에서는 데이터 처리 비용이 모델 개발 비용을 초과하는 것으로 밝혀졌으며 공급업체는 계층화 및 압축을 최적화해야 합니다. 하이퍼스케일러는 스토리지 계층을 재설계하고 높은 처리량 NVM 기반 클러스터와 병렬 액세스를 위해 조정된 객체 스토리지 버킷을 채택합니다.

미디어 및 게임에서 엣지 투 클라우드 워크 플로우 가속화

미디어 스튜디오와 게임 스튜디오는 클라우드 퍼스트 파이프라인을 채택합니다. 스트리밍과 실시간 렌더링이 확대됨에 따라 97%가 2025년 스토리지 예산을 늘릴 예정입니다. 클라우드 게임의 CAGR은 44%로, 지역 간 대기 시간 50ms 미만을 유지하는 분산 캐시가 필요합니다. 하지만 이러한 기업들은 스토리지 예산의 51%를 API 통화 및 이그짓 트래픽에 소비하고 있으며, 수수료를 피하기 위해 멀티클라우드 배포를 촉구하고 있습니다. 엣지 컴퓨팅에 대한 투자는 2024년에는 2,320억 달러에 이를 것으로 예상되며, 공급자는 On-Premise 게이트웨이와 하이퍼스케일 아카이브를 통합하여 원활한 자산 흐름을 실현하려고 합니다.

근본적인 데이터 주권과 관련된 복잡성

미국의 CLOUD법에서 중국의 크로스보더 플로우 규칙에 이르기까지 다양한 규제가 존재하기 때문에 기업은 단편적인 스토리지 실적를 운영하고 현지 법규에 대응하기 위해 데이터세트를 중복하고 있습니다. 법적 불확실성은 컴플라이언스 비용을 증가시키고 중복 관할권의 주장을 탐색하여 세계 배포를 지연시킵니다.

부문 분석

2024년 이 부문의 매출은 퍼블릭 클라우드가 59.0%로 선도하고 있으며 데이터 거주에 관한 법률이 강화됨에 따라 하이브리드 아키텍처는 2030년까지 연평균 복합 성장률(CAGR)이 26.01%가 될 전망입니다. 엔터프라이즈는 On-Premise 노드와 공용 확장성을 결합하여 대기 시간 및 규정 준수 목표를 달성하려고 합니다. 각국 정부의 소버린 프레임워크는 하이브리드 수요를 더욱 촉진하고, 에지에 대한 투자는 마이크로 리전을 통합 풀에 통합합니다. 하이브리드 환경은 현재 엔터프라이즈 워크로드의 82%를 관리하고 있으며 모든 공공 전략에서의 변화를 입증하고 있습니다.

두 번째 성장 벡터는 처리량을 위해 로컬 GPU 인접성이 필요하지만 스파이크를 위해 클라우드 버스트가 필요한 AI 교육 클러스터에 있습니다. 조직은 컨트롤 플레인 소프트웨어를 채택하고 사이트 간 정책을 오케스트레이션하여 잠금을 완화하고 비용을 최적화합니다. 공급업체는 통합 관측 가능성, 자동화된 데이터 계층화 및 마켓플레이스 생태계를 통해 차별화를 도모합니다. 예산 재분배가 진행됨에 따라 클라우드 스토리지 시장에서는 배포 모델이 코어, 에지 및 소버린 존에 걸쳐 유동적이고 정책 중심의 패브릭으로 수렴할 것으로 예측됩니다.

Object Repository는 2024년 51.2%의 매출을 올리고 비구조화된 데이터가 폭발적으로 증가하는 2030년까지 25.0%로 추이합니다. 오브젝트 플랫폼의 클라우드 스토리지 시장 규모는 본질적인 확장성, 풍부한 메타데이터, 생성형 인공지능(AI) 코퍼스의 요구에 맞는 소거 코딩의 경제성으로부터 혜택을 받습니다. 파일 계층과 블록 계층은 레거시 및 OLTP 작업 부하로 인해 지속되지만 페타바이트 규모의 병렬 액세스를 위해 향상된 객체 계층에 공유를 양도합니다.

혁신의 핵심은 멀티테넌트 네임스페이스 분리, 인라인 암호화 및 스테이징 없이 교육 노드에 공급하는 GPU 직접 파이프라인입니다. 마이크론의 32TB NVMe SSD 배포는 플래시 기반 객체 클러스터로의 마이그레이션을 강조합니다. 특허 출원은 지우기 인코딩 캐싱과 분산 해시 인덱스의 진보를 보여주고 성능과 내구성을 향상시킵니다. AI의 채택이 확대됨에 따라 오브젝트 스토리지는 클라우드 스토리지 시장의 컨텐츠, 모델 체크포인트, 벡터 데이터베이스를 지원할 것으로 보입니다.

클라우드 스토리지 시장 보고서는 배포 모드(프라이빗 클라우드, 퍼블릭 클라우드 등), 스토리지 유형(파일 스토리지, 객체 스토리지 등), 기업 규모(중소기업, 대기업), 용도(백업 및 복구, 용도 관리 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 제조업, 소매업, 전자상거래 등), 지역별로 분류됩니다.

지역 분석

북미는 하이퍼스케일러 본사와 AI의 조기 도입이 수요를 견인해 2024년 매출의 38.0%를 차지했습니다. 데이터센터의 전력 요구는 2028년까지 연률 16%로 추이해, 송전의 병목과 허가의 지연이 스케줄을 압박하고 있습니다. 클라우드 노하우 고객(KYC) 점검과 같은 규제 방안은 국경을 넘어서는 워크플로우를 분리하고 기업을 다중 지역 아키텍처로 향하게 할 수 있습니다. 하드웨어 부족은 간헐적으로 용량을 제한하지만, 지속적인 투자로 혁신과 지출의 리더십을 유지하고 있습니다.

아시아태평양은 성장 엔진으로 정부의 디지털화 프로그램, 주권 클라우드의 의무화, AI 도입 증가로 CAGR 24.98%로 성장을 지속합니다. 중국 지출은 현지 공급업체와 정책 지원에 힘입어 2025년에는 460억 달러에 달할 것으로 보입니다. 인도 서비스 시장은 2024년 상반기에 52억 달러에 이르고 2028년까지 255억 달러를 목표로 합니다. 호주와 일본에서는 지역 독자적인 틀이 진행되는 한편, 지역의 데이터센터용량의 CAGR은 13.3%에 달하고, 거주 준거 존의 구축이 진행되고 있습니다.

유럽은 GDPR(EU 개인정보보호규정) 하에서 꾸준히 성장해 섹터별로 암호화 및 데이터 최소화 기능을 추진하고 있습니다. 브라질, 멕시코, 칠레에서는 하이퍼스케일러에 대한 투자가 진행되고 있으며, 라틴아메리카의 코로케이션 파이프라인은 2029년까지 100억 달러에 달할 가능성이 있습니다. 아프리카 수요는 매년 25-30% 증가하고 있지만 세계 매출은 1% 미만입니다. 현지 공급자는 가격과 통화의 유연성으로 차별화를 도모하고 있습니다. 이러한 역학은 지역 생태계가 세계 연결성과 공존하는 다극화 시장을 뒷받침합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 거시 경제 영향 평가

- 시장 성장 촉진요인

- 조직 전체의 클라우드 도입 증가

- 저비용, 고속 스토리지 액세스에 대한 수요 증가

- 미디어와 게임에 있어서의 엣지 투 클라우드의 워크플로우 고속화

- AI 세대가 주도하는 지식 근로자용 앱의 데이터 폭발(2025년 이후)

- 소버린 클라우드 프레임워크에 대한 정부의 자극책

- ESG 주도의 스토리지 최적화와 카본 어웨어 워크로드

- 시장 성장 억제요인

- 근본적인 데이터 주권의 복잡성

- 에그레스 비용의 반발 격화와 벤더 락인 리스크

- 멀티 클라우드 데이터 스프롤의 보안 갭

- 프론티어 시장에서 라스트 마일 대역폭 제한

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 업계 간 경쟁

- 투자분석

제5장 시장 규모와 성장 예측

- 전개 모드별

- 프라이빗 클라우드

- 퍼블릭 클라우드

- 하이브리드 클라우드

- 스토리지 유형별

- 파일 스토리지

- 오브젝트 스토리지

- 블록 스토리지

- 기업 규모별

- 중소기업

- 대기업

- 용도별

- 백업 및 복구

- 데이터 관리 및 아카이브

- 용도 관리

- 협업 및 컨텐츠 서비스

- 최종 사용자 업계별

- BFSI

- 헬스케어 및 생명과학

- 정부 및 공공기관

- 제조

- 소매 및 전자상거래

- IT 및 통신

- 미디어 및 엔터테인먼트

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 튀르키예

- 아프리카

- 남아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC(Alphabet)

- Alibaba Cloud(Alibaba Group)

- IBM Corporation

- Oracle Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- NetApp Inc.

- Dropbox Inc.

- Box Inc.

- Wasabi Technologies

- Backblaze Inc.

- Tencent Cloud

- OVHcloud

- Rackspace Technology

- Hitachi Vantara

- Fujitsu Limited

- pCloud AG

- Tresorit AG

- Iron Mountain

제7장 시장 기회와 장래의 전망

JHS 25.11.13The cloud storage market size reached USD 145.23 billion in 2025 and is forecast to reach USD 425.76 billion by 2030 at a 24.0% CAGR.

Generative-AI adoption, data-sovereignty mandates, and the need for modern, energy-efficient infrastructure are accelerating enterprise migration and reshaping storage architectures worldwide. Intensifying hyperscaler investment, rising sovereign-cloud spend across Asia Pacific, and steady SME adoption are widening the global addressable base while inflation-linked construction costs spur innovation in low-power technologies. Object storage dominates AI workloads, hybrid deployment grows fastest, and Asia Pacific leads regional expansion. Competitive rivalry remains high as providers pursue AI-optimized capacity, sovereign-cloud zones, and carbon-aware services.

Global Cloud Storage Market Trends and Insights

Gen-AI-led data explosion in knowledge-worker apps (2025+)

Generative-AI workloads are multiplying enterprise data volumes by an order of magnitude. Solid-state drive demand for AI training environments is climbing 35% per year as spinning disks struggle to meet latency targets. Storage footprints for single training runs are set to scale from 30 TB in 2025 to 100 TB by 2030, while inference nodes grow even faster as new products embed AI features. Cost models now reveal that data-handling charges eclipse model-development expenses, pushing vendors to optimize tiering and compression. Hyperscalers are redesigning storage layers to favor high-throughput NVM-based clusters and object storage buckets tuned for parallel access.

Edge-to-cloud workflow acceleration in media and gaming

Media and gaming studios are embracing cloud-first pipelines; 97% plan to raise storage budgets in 2025 as streaming and real-time rendering expand. Cloud gaming's 44% CAGR requires distributed caches that maintain <50 ms latency across regions. Yet, these firms spend 51% of storage budgets on API calls and egress traffic, catalyzing multi-cloud placement to avoid fees. Edge-compute spend is forecast at USD 232 billion in 2024, pushing providers to integrate on-premise gateways with hyperscale archives for seamless asset flows.

Persistent data-sovereignty complexity

Divergent regulations-from the U.S. CLOUD Act to China's cross-border flow rules-force organizations to operate fragmented storage footprints and duplicate datasets to meet local statutes. Legal uncertainty raises compliance spend and slows global rollouts as firms navigate overlapping jurisdictional claims.

Other drivers and restraints analyzed in the detailed report include:

- Government stimulus for sovereign cloud frameworks

- ESG-driven storage optimization and carbon-aware workloads

- Escalating egress-fee backlash and vendor lock-in risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment's revenue in 2024 reflected a 59.0% public-cloud lead, yet hybrid architectures are on track for a 26.01% CAGR to 2030 as data residency laws tighten. Enterprises blend on-premise nodes with public scalability to meet latency and compliance goals. Governments' sovereign frameworks further propel hybrid demand, while edge investments embed micro-regions into unified pools. Hybrid environments now manage 82% of enterprise workloads, validating the shift away from all-public strategies.

A second growth vector lies in AI training clusters that require local GPU adjacency for throughput yet still need cloud bursts for spikes. Organizations adopt control-plane software to orchestrate policies across sites, mitigating lock-in and optimizing cost. Vendors differentiate via integrated observability, automated data-tiering, and marketplace ecosystems. As budgets reallocate, the cloud storage market will see deployment models converge into fluid, policy-driven fabrics spanning core, edge, and sovereign zones.

Object repositories generated 51.2% revenue in 2024 and will compound at 25.0% through 2030 as unstructured data explodes. The cloud storage market size for object platforms benefits from intrinsic scalability, rich metadata, and erasure-coding economics that align with generative-AI corpus needs. File and block tiers persist for legacy and OLTP workloads but cede share to object layers hardened for petabyte-scale parallel access.

Innovation centers on multi-tenant namespace isolation, in-line encryption, and GPU-direct pipelines that feed training nodes without staging. Micron's roll-out of 32 TB NVMe SSDs underscores the migration toward flash-based object clusters. Patent filings reveal advances in erasure-coded caching and distributed-hash indexing, amplifying performance and durability. As AI adoption broadens, object storage will underpin content, model checkpoints, and vector databases within the cloud storage market.

The Cloud Storage Market Report is Segmented by Deployment Mode (Private Cloud, Public Cloud, and More), Storage Type (File Storage, Object Storage, and More), Enterprise Size (SMEs and Large Enterprises), Application (Backup and Recovery, Application Management, and More), End-User Industry (BFSI, Manufacturing, Retail and E-Commerce, and More), and Geography.

Geography Analysis

North America held 38.0% revenue in 2024 as hyperscaler headquarters and early AI adoption drove demand. Data-center power needs are on a 16% annual trajectory to 2028, though transmission bottlenecks and permitting delays pressure timelines. Regulatory proposals such as cloud know-your-customer (KYC) checks may fragment cross-border workflows, nudging enterprises toward multi-region architectures. Hardware shortages intermittently constrain capacity, but continuous investment sustains leadership in innovation and spend.

Asia Pacific is the growth engine, charting a 24.98% CAGR courtesy of government digitization programs, sovereign-cloud mandates, and rising AI adoption. China's spending will hit USD 46 billion in 2025, buoyed by local vendors and policy support. India's services market reached USD 5.2 billion in H1 2024 and targets USD 25.5 billion by 2028. Australia and Japan advance localized frameworks, while a 13.3% CAGR in regional data-center capacity underscores the build-out of residency-compliant zones.

Europe grows steadily under GDPR, with sectoral codes pushing encryption and data-minimization features. Latin America's colocation pipeline could reach USD 10 billion by 2029 as Brazil, Mexico, and Chile court hyperscaler investment. Africa's demand rises 25-30% annually, yet represents <1% global revenue; local providers differentiate on price and currency flexibility. These dynamics confirm a multipolar cloud storage market where regional ecosystems coexist with global connectivity.

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC (Alphabet)

- Alibaba Cloud (Alibaba Group)

- IBM Corporation

- Oracle Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- NetApp Inc.

- Dropbox Inc.

- Box Inc.

- Wasabi Technologies

- Backblaze Inc.

- Tencent Cloud

- OVHcloud

- Rackspace Technology

- Hitachi Vantara

- Fujitsu Limited

- pCloud AG

- Tresorit AG

- Iron Mountain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Macroeconomic Impact Assessment

- 4.3 Market Drivers

- 4.3.1 Increase in cloud adoption across organizations

- 4.3.2 Rising demand for low-cost, high-speed storage access

- 4.3.3 Edge-to-cloud workflow acceleration in media and gaming

- 4.3.4 Gen-AI-led data explosion in knowledge-worker apps (2025+)

- 4.3.5 Government stimulus for sovereign cloud frameworks

- 4.3.6 ESG-driven storage optimization and carbon-aware workloads

- 4.4 Market Restraints

- 4.4.1 Persistent data-sovereignty complexity

- 4.4.2 Escalating egress-fee backlash and vendor lock-in risk

- 4.4.3 Multi-cloud data-sprawl security gaps

- 4.4.4 Limited last-mile bandwidth in frontier markets

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Private Cloud

- 5.1.2 Public Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Storage Type

- 5.2.1 File Storage

- 5.2.2 Object Storage

- 5.2.3 Block Storage

- 5.3 By Enterprise Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By Application

- 5.4.1 Backup and Recovery

- 5.4.2 Data Management and Archiving

- 5.4.3 Application Management

- 5.4.4 Collaboration and Content Services

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Government and Public Sector

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-commerce

- 5.5.6 IT and Telecom

- 5.5.7 Media and Entertainment

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 Turkey

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC (Alphabet)

- 6.4.4 Alibaba Cloud (Alibaba Group)

- 6.4.5 IBM Corporation

- 6.4.6 Oracle Corporation

- 6.4.7 Dell Technologies Inc.

- 6.4.8 Hewlett Packard Enterprise

- 6.4.9 NetApp Inc.

- 6.4.10 Dropbox Inc.

- 6.4.11 Box Inc.

- 6.4.12 Wasabi Technologies

- 6.4.13 Backblaze Inc.

- 6.4.14 Tencent Cloud

- 6.4.15 OVHcloud

- 6.4.16 Rackspace Technology

- 6.4.17 Hitachi Vantara

- 6.4.18 Fujitsu Limited

- 6.4.19 pCloud AG

- 6.4.20 Tresorit AG

- 6.4.21 Iron Mountain

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment