|

시장보고서

상품코드

1640355

인도의 플라스틱 포장 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)India Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

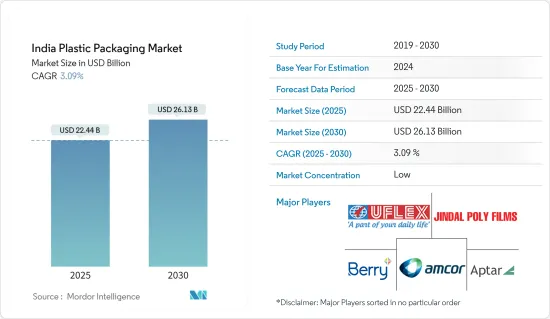

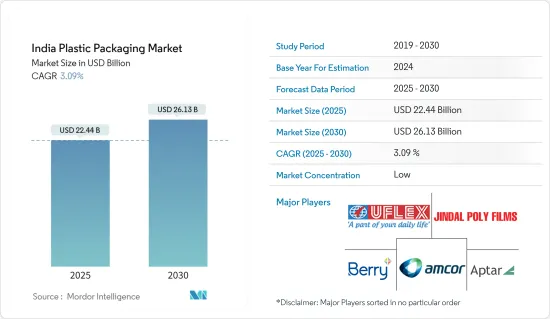

인도의 플라스틱 포장 시장 규모는 2025년 224억 4,000만 달러, 2030년 261억 3,000만 달러로 추정되며, 예측 기간(2025-2030년)중 CAGR은 3.09%에 달할 것으로 예측되고 있습니다.

플라스틱은 가장 유명한 포장 재료 중 하나입니다. 이 재료는 가볍고 저가이므로 모든 최종 사용자 간에 즉시 차별화됩니다.

주요 하이라이트

- 플라스틱 포장은 인도 포장 산업의 새로운 시대의 중심에 있습니다. 다목적 용도는 많은 산업에서 제품 포장의 기초가되고 있습니다. 다른 포장 유형에 비해 플라스틱 포장 용기는 높은 충격 강도, 강성 및 장벽 특성과 같은 독특한 이점을 갖추고 있으며, 이는 최근 플라스틱 포장 시장을 확대하고 있습니다.

- 폴리에틸렌은 주로 폴리백, 플라스틱 필름, 지오멤브레인 등의 포장에 사용됩니다. 경량으로 부분 결정성의 열가소성 수지이며, 고내구성, 저흡습성, 차음성을 가지고 있습니다. 저밀도 폴리에틸렌(LDPE)은 주로 플라스틱 가방의 제조에 사용됩니다. LDPE 폴리에틸렌 가방은 부드럽고 유연하며 천연 색상이 있습니다. 이러한 가방에 대한 수요는 유연성, 투명성, 높은 충격 강도, 물과 알코올 증기를 제외한 약한 장벽 특성과 같은 알려진 특징 때문입니다. 내열성은 약하지만, 우수한 전기 특성과 우수한 내약품성이 있습니다. 환경 응력 균열의 경향이 있습니다.

- 파우치 포장은 매우 편리하고 휴대하기 편리한 솔루션이기 때문에 인기가 높아지고 있습니다. 많은 구매자는 기존의 단단한 포장보다 유연한 스탠드업 파우치를 선호합니다. 소비자는 지난 10년간 스탠드업 파우치(스낵, 음식, 베이비 푸드, 산업용 오일 및 윤활유용)에 대한 수요를 비약적으로 늘렸습니다. 포장 유형 특유의 혁신은 시장의 지속가능성을 더욱 향상시키고 있습니다.

- 인도에서는 최근 몇 년동안 음료 포장 시장이 크게 성장하고 있습니다. 국가 전체의 음료 포장 동향의 급속한 변화는 시장 성장에 매우 중요합니다. 음료 포장의 새로운 추세는 구조 변화 외에도 사후 소비자 재활용과 같은 재활용 재료 개발, 고객 수용성, 안전성 및 새로운 충전 기술에 중점을 둡니다. 내열성 PET 병의 개발로 일부 음료의 보존성이 향상되었습니다.

- 그러나 인도의 플라스틱 포장 시장은 주로 환경 문제 증가로 인한 규제 기준의 역동적인 변화로 인해 큰 문제에 직면할 것으로 예상됩니다. 정부는 플라스틱 포장 폐기물에 대한 국민의 우려에 대응하고 환경 폐기물을 최소화하고 폐기물 관리 프로세스를 개선하기 위한 규제를 실시했습니다.

인도 플라스틱 포장 시장 동향

식품 부문이 큰 점유율을 차지

- 식품 산업에서 플라스틱 포장 수요는 편리하고 컴팩트한 솔루션의 필요성, 특히 조리된 식품의 인기가 높아짐에 의해 견인되고 있습니다. 원형 용기와 샐러드 팩과 같은 다양한 형태의 밀폐 트레이에 포장되는 경우가 많습니다. 이 전략적 움직임은 환경 친화적인 포장 솔루션을 추구하는 소비자의 선호도에 부합하며 산업 내에서 시장 수요에 부응하고 환경에 미치는 영향을 줄이기 위해 노력하고 있음을 보여줍니다.

- 연질 포장에는 파우치, 가방, 필름, 랩 등 다양한 형태가 있으며, 식육, 닭고기, 어류 산업에서 다양한 컷, 물약 크기, 포장 형태에 대응하는 다용도의 포장 솔루션을 가능하게 하고 있습니다. 이를 통해 홀 컷부터 소시지나 필레 같은 가공품에 이르기까지 다양한 제품의 효율적인 포장이 가능합니다.

- 높은 영양가를 실현하기 위해, 치즈, 우유, 요구르트 등, 영양가가 높은 유제품으로의 소비자의 시프트가 진행되고 있는 것도, 성장을 뒷받침할 것으로 추정됩니다. 게다가, 유제품은 비타민, 단백질, 고흡수성 칼슘 등과 오랫동안 관련되어 왔습니다. 이러한 유제품에 포함된 수많은 생물학적으로 기능적인 성분은 예측 기간 동안 유제품 부문을 강화할 것으로 예상됩니다.

- 또한 플라스틱 트레이와 용기는 식당, 레스토랑, 가정, 사무실 등의 식품 용기로 수많은 산업에서 사용됩니다. 레스토랑과 같은 외식 산업은 식품 포장 트레이를 테이크 아웃 및 배달 서비스에 활용하여 식품의 안전과 외관을 보장합니다. 또한 카페 및 베이커리와 같은 다른 부문은 제품 포장 및 진열을 위해 이러한 트레이에 의존하여 고객의 편의성과 매력을 향상시킵니다.

- 트레이는 주로 식품 산업에서는 1차 포장, 2차 포장, 의약품 및 소비재에서는 2차 포장에 사용됩니다. 트레이와 용기는 주로 식품, 음식 및 접객 산업에서 일회용 시장의 일부입니다. 이 제품은 널리 이용 가능하며 가격도 저렴하며 일회용 시장의 대부분을 차지합니다.

- '메이크업 인디아' 개념의 일환으로 인도 정부는 식품 가공 부문에 대한 투자를 선호하고 촉진했습니다. 정부는 식품 가공 공급 체인을 개선하기 위해 134개의 콜드체인 프로젝트와 18개의 메가 푸드 파크를 설립했습니다. 식품가공부문은 산업진흥을 위해 시작된 1,000억 루피(13억 5,000만 달러) 프로그램 등 최근 정부의 조치를 통해 견조한 개발 궤도를 타고 있으며, 결국 국내 연질 플라스틱 포장에 대한 수요를 높이고 있습니다.

- 인도의 전자상거래 성장은 다양한 식품에 대한 수요를 창출하고 있습니다. 이 나라의 온라인 소매 매출은 2022년 8,700만 달러에서 크게 증가했으며, 2027년에는 1억 7,300만 달러에 이를 것으로 예상됩니다. 온라인 소매 판매 증가는 식품 포장 수요가 인도에서 증가하고 있음을 나타냅니다. 게다가 플라스틱 병과 용기는 포장된 식품에 긴 보존 기간을 제공하는 능력으로 식품 산업에서 중요성을 증가시키고 있습니다.

인도에서 강력한 성장을 이루는 병

- 시장에서 병이 널리 사용되는 산업에는 식품, 음식, 화장품, 산업, 의료 등이 있습니다. 음료 부문의 플라스틱 병 시장은 병 음료수와 비알코올 음료 수요 증가로 성장할 것으로 예상됩니다.

- PepsiCo India는 기업의 제품인 펩시 블랙이 탄산 음료 카테고리에서 처음으로 인도에서 제조되는 100% 재활용 PET 플라스틱 병을 도입할 것이라고 발표했습니다. 이 노력에는 완전 재활용 병의 펩시 블랙 라벨과 캡이 포함되어 있지 않습니다.

- 페트병 음료수 시장은 다른 포장 방법보다 비용 효율적이고 유통 기한이 길고 사용하기 쉽기 때문에 소비자들 사이에서 포장 음료수에 대한 수요가 높아지고 있는 것이 배경에 있습니다. 순수한 식수의 필요성에 대한 일반 소비자의 의식이 높아짐에 따라 포장 식수 및 병 음료수의 포장 산업은 급속한 성장을 이루고 있습니다.

- 플라스틱 병은 탄산 음료, 주스 음료, 과일 주스, 스포츠 음료, 에너지 음료 등 다양한 카테고리에서 큰 수요가 있으며, 그 중에서도 물병은 인도에서 잠재적인 점유율을 보여 페트병 시장의 성장을 돕고 있습니다. Indian Railways Catering and Tourism Corporation Limited는 페트병 음료수 브랜드 "Rail Neer"를 출시하여 기차와 역에서 판매합니다. 2021년 생산량은 7,520만개로 2023년에는 3억 5,770만개로 증가하여 이 지역에서 페트병 음료수 수요의 유기적 동향을 보이고 있습니다.

- 플라스틱 병은 모양을 만들기 쉽습니다. 상자의 경우, 청량음료수와 같은 가압상품이 들어있는 강한 내압 하에서는 그 형태를 유지하기가 어렵습니다. 그러나 기술의 진보, 제조 방법, 재료의 개발로 플라스틱은 압력이 가해도 어떤 형태로도 성형할 수 있게 되었습니다. 페트병은 떨어뜨려도 안전성이 높고, 가벼우며 투명하고, 리필 가능합니다. 회수의 필요성은 플라스틱 재활용을 제한할 수도 있습니다. 그러나 새로운 기술을 통해 더 많은 플라스틱을 재활용 할 수 있습니다.

경쟁 구도

인도에서는 플라스틱 포장 수요가 크게 증가하고 있기 때문에 시장이 부문화되고 있습니다. 시장을 독점하는 대기업은 Aptar Group Inc., Uflex Limited, Berry Global, Sealed Air Corporation, Constantia Flexibles 등이 있습니다. 이러한 기업들은 시장 점유율을 유지하기 위해 기술 혁신을 계속하고 전략적 파트너십을 맺고 있습니다. 예를 들면

- 2024년 4월 Manjushree Technopack Limited는 Oricon Enterprises Ltd.의 플라스틱 포장 사업을 기업 가치 52억 루피(629만 달러)로 인수하는 최종 계약을 체결했습니다. 인수된 기업에는 주로 음료에 사용되는 플라스틱 용기와 클로저 제조 업체인 Oriental Containers가 포함됩니다. 연간 150억 가까이의 설비 능력을 가진 이 인수는 캡 클로저 부문에서 MTL의 현재 시장 점유율을 두배로 합니다.

- 2023년 12월, 미국의 Aptar Corporation의 완전 자회사인 Aptar Pharma는 동남아 시장을 위한 생산 능력을 강화하기 위해 인도 뭄바이에 새로운 제조 시설을 설립했습니다. 생산 능력은 동남아의 의약품 고객의 제조 능력을 향상시키고 혁신적인 제품 솔루션을 제공하기 위해 더욱 강화되었습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 역학

- 시장 성장 촉진요인

- 경량 포장의 채용 증가

- 친환경 포장 및 재생 플라스틱 증가

- E-Commerce 산업의 성장이 성장을 견인할 전망

- 시장 성장 억제요인

- 원료(플라스틱 수지) 가격의 상승

- 정부의 규제와 환경 문제

- 플라스틱 포장 세계 시장 개요

제6장 시장 세분화

- 포장 유형별

- 연질 플라스틱 포장

- 경질 플라스틱 포장

- 최종 사용자별

- 식품

- 음료

- 의료

- 퍼스널케어 및 가정용품

- 기타

- 제품 유형별

- 병과 항아리

- 트레이 및 용기

- 파우치

- 가방

- 필름 및 랩

- 기타

제7장 경쟁 구도

- 기업 프로파일

- Hitech Plast(Hitech Group)

- Mondi Group

- Sealed Air Corporation

- Berry Global Inc.

- Polyplex Corporation Limited

- TCPL Packaging Ltd

- Manjushree Tecnopack Ltd

- Aptar Group Inc.

- Amcor PLC

- Jindal Poly Films Limited

- Cosmo Films Ltd(Cosmo First Limited)

- Constantia Flexibles

제8장 투자 분석

제9장 시장의 미래

JHS 25.02.10The India Plastic Packaging Market size is estimated at USD 22.44 billion in 2025, and is expected to reach USD 26.13 billion by 2030, at a CAGR of 3.09% during the forecast period (2025-2030).

Plastic is one of the most prominent packaging materials. The material's lightweight and low-cost nature instantly distinguished it among all the end-users.

Key Highlights

- Plastic packaging is at the center of a new era in the Indian packaging industry. Its versatile usage is becoming the foundation for many industries for product packaging. Compared to other packaging types, plastic packaging containers provide unique benefits, such as high impact strength, stiffness, and barrier properties, which have expanded the market for plastic packaging in recent years.

- Polyethylene is primarily used for packaging plastic bags, plastic films, geomembranes, etc. It is a lightweight, partially crystalline, thermoplastic resin with high resistance, low moisture absorption, and sound-insulating properties. Low-density polyethylene (LDPE) is mainly used to manufacture plastic bags. LDPE polyethylene bags are soft and flexible and are available in natural colors. The demand for these bags is due to their known features, such as flexibility, transparency, high impact strength, and weak barrier, except for water and alcohol vapor. These bags have weak temperature resistance but outstanding electrical properties and excellent chemical resistance. They show a tendency for environmental stress cracking.

- Pouch packaging is gaining popularity as it is a highly convenient and portable solution. Many shoppers prefer flexible, stand-up pouches over traditional, rigid packaging. Consumers drove the demand for stand-up pouches (for snacks, beverages, baby food, or industrial oils and lubricants) exponentially over the past decade. Specific innovations in the packaging type further drive the market's sustainability.

- The market for beverage packaging has grown significantly over the last few years in India. Rapid changes in beverage packaging trends across the country are critical for the market's growth. The new trends in the packaging of beverages focus on structural changes, as well as the development of recycled materials like post-consumer recycling, customer acceptance, safety, and new filling technologies. The development of heat-resistant PET bottles improved the preservation of several drinks.

- However, the plastic packaging market in India is expected to be significantly challenged due to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. The government is responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

India Plastic Packaging Market Trends

Food Segment to Hold a Significant Share

- The food industry's demand for plastic packaging is driven by the need for convenient, compact solutions, particularly with the increasing popularity of ready-to-eat meals. These meals, often packaged in sealed trays of various shapes, including round containers and salad packs, are now seeing a notable shift toward using sustainable and environmentally friendly materials. This strategic move aligns with consumer preferences for eco-conscious packaging solutions, indicating a commitment to meeting market demands and reducing environmental impact within the industry.

- Flexible packaging comes in various forms, such as pouches, bags, films, and wraps, allowing for versatile packaging solutions to accommodate different cuts, portion sizes, and packaging formats within the meat, poultry, and fish industries. This enables efficient packaging of a wide range of products, from whole cuts to processed items like sausages and fillets.

- The increasing shift of consumers toward nutrient-dense dairy products such as cheese, milk, yogurt, and more to achieve high nutrition is likely to aid growth. Besides, dairy products have been long associated with vitamins, proteins, highly absorbable calcium, and more. Numerous biologically functional components in these dairy products are expected to strengthen the dairy products segment over the forecast period.

- Furthermore, plastic trays and containers are used in numerous industries as food containers in cafeterias, restaurants, homes, offices, etc. Food services businesses like restaurants utilize food packaging trays for takeout and delivery services, assuring food remains secure and presentable. Besides, other sectors like cafes and bakeries depend on these trays for packaging and displaying their products, improving customer convenience and appeal.

- Trays are mainly used for primary and secondary packaging in the food industry and secondary packaging in pharmaceutical and consumer goods. Trays and containers are part of the disposables market, mainly in the food, beverage, and hospitality industries. These products are widely available, cost less, and are a large part of the disposables market.

- As part of the "Make in India" initiative, the Indian government prioritized and promoted investments in the food processing sector. The government created 134 cold chain projects and 18 mega food parks to improve the food processing supply chain. The food processing sector is also on a solid development trajectory due to recent government measures, such as the INR 10,000 crore (USD 1.35 billion) program launched to promote the industry, eventually enhancing the demand for flexible plastic packaging in the country.

- The growth of e-commerce in India creates the demand for different food products. The rise of online retail sales in the county grew significantly from USD 87 million in 2022, and it is forecasted to reach USD 173 million by 2027. Growing retail online sales show that the demand for food packaging is increasing in India. Moreover, plastic bottles and containers have gained importance in the food industry due to their ability to provide longer shelf life to packaged food items.

Bottles to Witness Strong Growth in the Country

- The industries where bottles are widely used in the market include food, beverage, cosmetics, industrial, healthcare, and more. The beverage sector's plastic bottle market is anticipated to witness growth owing to the increased demand for bottled water and non-alcoholic beverages.

- PepsiCo India announced that its product Pepsi Black will introduce the first 100% recycled PET plastic bottles in the carbonated beverages category to be manufactured in India. The manufacturer does not include the Pepsi Black label and cap for a completely recycled bottle in this initiative.

- The market for bottled water packaging in plastic bottles is driven by the rising demand for packaged drinking water among consumers because they are more cost-effective than other packaging options, have a longer shelf life, and are easier to use. The packaged and bottled water packaging industries are experiencing rapid growth as public awareness of the need for pure drinking water increases.

- Plastic bottles have a significant demand in India in various categories, such as carbonated soft drinks, juice drinks, fruit juices, and sports and energy drinks, out of which water bottles show a potential share in the country, aiding the growth of the plastic bottle market. Indian Railways Catering and Tourism Corporation Limited launched a pet bottled water brand, "Rail Neer," which is sold on trains and railway stations. It produced 75.20 million bottles in 2021, which increased to 357.70 million bottles in 2023, indicating the organic trend in demand for plastic bottled water in the region.

- A plastic bottle is simple to shape. It can be difficult for a box containing pressurized goods like soft drinks to keep its shape under intense internal pressure. However, with technological advancements, manufacturing methods, and material development, plastic can be molded into any shape, even under pressure. If dropped, a plastic bottle has a high safety factor and is lightweight, transparent, and refillable. The need for collection can constrain plastic recycling. However, new technologies are making it possible for more plastic to be recycled.

Competitive Landscape

As the demand for plastic packaging is increasing significantly in India, the market is fragmented. Large, dominant players in the market include Aptar Group Inc., Uflex Limited, Berry Global, Sealed Air Corporation, and Constantia Flexibles. These companies keep innovating and entering into strategic partnerships to retain their market share. For instance,

- In April 2024, Manjushree Technopack Limited entered into definitive agreements to acquire Oricon Enterprises Ltd's plastic packaging business for an enterprise value of INR 520 crores (USD 6.29 million). The acquired company included Oriental Containers, a manufacturer of plastic containers and closures used primarily in beverages. With an installed capacity of nearly 15 billion pieces per year, this transaction will double MTL's current market share in the cap and closure sector.

- In December 2023, Aptar Pharma, a wholly owned subsidiary of the US-based Aptar Corporation, established its new manufacturing facility in Mumbai, India, to increase production capacity for Southeast Asian markets. Its production capabilities have been further enhanced to improve the manufacturing capacity of pharmaceutical customers in Southeast Asia and to offer more innovative product solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight-packaging Methods

- 5.1.2 Increased Eco-friendly Packaging and Recycled Plastic

- 5.1.3 Growing E-commerc Industry is Expected to Drive Growth

- 5.2 Market Restraints

- 5.2.1 High Price of Raw Material (Plastic Resin)

- 5.2.2 Government Regulations and Environmental Concerns

- 5.3 Global Plastic Packaging Market Overview

6 MARKET SEGMENTATION

- 6.1 By Packaging Type

- 6.1.1 Flexible Plastic Packaging

- 6.1.2 Rigid Plastic Pacakaging

- 6.2 By End User

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Personal Care and Household

- 6.2.5 Other End Users

- 6.3 By Product Type

- 6.3.1 Bottles and Jars

- 6.3.2 Trays and Containers

- 6.3.3 Pouches

- 6.3.4 Bags

- 6.3.5 Films and Wraps

- 6.3.6 Other Product Types

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Hitech Plast (Hitech Group)

- 7.1.2 Mondi Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 Berry Global Inc.

- 7.1.5 Polyplex Corporation Limited

- 7.1.6 TCPL Packaging Ltd

- 7.1.7 Manjushree Tecnopack Ltd

- 7.1.8 Aptar Group Inc.

- 7.1.9 Amcor PLC

- 7.1.10 Jindal Poly Films Limited

- 7.1.11 Cosmo Films Ltd (Cosmo First Limited)

- 7.1.12 Constantia Flexibles