|

시장보고서

상품코드

1640357

아시아태평양의 의약품 포장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Asia Pacific Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

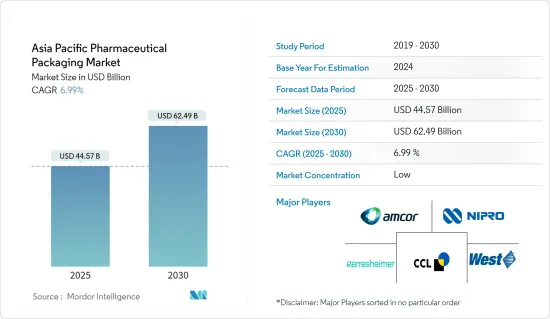

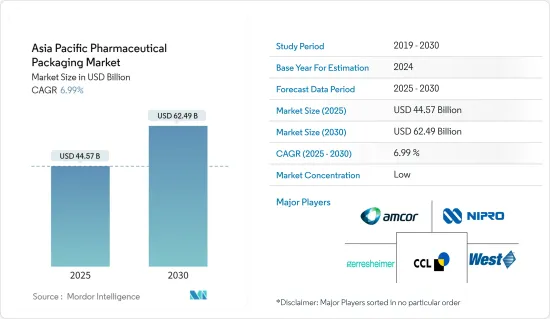

아시아태평양의 의약품 포장 시장 규모는 2025년에 445억 7,000만 달러로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 6.99%로, 2030년에는 624억 9,000만 달러에 달할 것으로 예측되고 있습니다.

주요 하이라이트

- 의약품 포장은 안전하고 효과적인 의약품을 캡슐화, 유지, 보호 및 유통하는 데 필요한 요소의 집합으로, 의약품의 만료일 이전에 언제든지 안전하고 효과적인 투여 형태에 접근할 수 있도록 보장합니다. 적절한 포장 재료는 위조 의약품의 소비를 억제하는 데 도움이 되는 변조를 방지하는 안전성을 제공하는 데 필수적입니다. 또한 고급 포장재는 엄격한 규제 지침을 준수해야 합니다.

- 의약품 포장 제조업체는 의약품 부문에 대한 투자 증가로 아시아태평양에서 큰 비즈니스 기회를 목격할 것으로 예상됩니다. 의약품 수요 증가와 제약 기술의 진보는 유리병, 앰풀 및 기타 유리 포장 솔루션 수요에 직접 기여하고 있습니다. 만성 질환이 계속 증가하고 COVID-19 백신의 생산량이 여전히 많기 때문에 1차 포장, 특히 유리 용기 수요가 급증할 것으로 예상됩니다.

- 이 지역의 의약품 포장 부문에서는 유리 포장이 시장 성장을 이끌 것으로 예상됩니다. 제약회사는 유리 용기를 이용하여 주사약, 경구고형제, 액체제제, 생물제제 등 다양한 의약품을 포장하고 있습니다. 유리 용기 포장의 급성장 배경에는 의약품 제조 사업, 특수 의약품 수요 증가, 의료 인프라 확대 등의 요인이 있습니다. 이 동향은 특히 중국, 인도, 일본, 한국 등 국가에서 두드러지며, 제약산업은 현저한 성장을 이루고 있기 때문에 유리 포장 솔루션 수요가 급증하고 있습니다.

- 플라스틱 병 산업은 향후 몇 년 동안 상당한 성장을 이룰 것으로 예상됩니다. 이 지역에서는 PET의 이용이 꾸준히 증가하고 있으며, 그 결과 유리에 비해 최대 90%의 경량화가 실현되어 보다 비용 효율적인 운송이 가능해집니다. 현재 PET로 만든 플라스틱 병은 의약품 부문에서 부피가 큰 섬세한 유리 병을 대체하는 다양한 액체의 재사용 가능한 포장을 제공합니다. 제약 산업에서 플라스틱 PET 기술의 진보는 시장 전망을 밀어 올릴 것으로 예상됩니다.

- 또한 이 지역의 제약 부문을 강화하기 위한 정부의 이니셔티브가 시장 확대를 촉진할 것으로 예상됩니다. 예를 들어, 국가의 의료 시스템의 현대화를 촉진하기 위해 중국 정부가 시행한 조치는 의약품 포장 산업의 진보를 자극할 것으로 예상됩니다. 또한 중국은 의약품 포장의 인프라와 자원을 적극적으로 개선하는 한편, 의약품 유형을 늘리고 있으며, 의약품 포장 기업에 새로운 길을 열 수 있습니다.

- 세계의 의약품 시장에서의 중국의 존재감은 꾸준히 높아지고 있으며, 주요 소비국인 동시에 세계의 의약품 산업과 공급망의 중요한 구성 요소로서의 역할을 하고 있습니다. 과학기술의 진보에 견인된 최근의 의약품 부문의 급성장은 앞으로도 계속될 것으로 예측되고 있습니다. 2023년 12월 덴마크 제약회사인 노보 노르디스크는 2026년 6월까지 이 지역 신설 회사에 4억 위안(5,960만 달러)을 투자할 계획을 밝혔습니다. 이러한 실질적인 개발은 의약품 포장 서비스 수요를 촉진할 것으로 예상됩니다.

- 포장 산업은 COVID-19의 큰 유행에 의해 큰 영향을 받았습니다. 감염증이나 백신에 중점이 옮겨짐으로써, 당뇨병이나 고혈압 등의 치료 영역에서 성공한 임상 검사나 연구 개발 활동은 감소했습니다. 그러나 제약산업은 유행기간 동안 다양한 질병에 대한 의약품 수요의 급증을 목격하여 포장사업에 많은 투자를 하게 되었습니다. 다행히 제약 산업은 유행에 대응하여 안전하고 위생적인 포장의 필요성을 강조함으로써 즉시 회복되었습니다.

아시아태평양 의약품 포장 시장 동향

유리 포장이 큰 성장을 이룰 전망

- 유리 포장은 포장 산업에서 의약품의 주요 옵션으로 널리 간주됩니다. 그 인기의 이유는 지속 가능한 특성, 불활성, 불 침투성, 재활용성, 품질을 손상시키지 않고 재사용 할 수 있는 능력에 있습니다. COVID-19의 유행은 투약의 필요성이 크게 증가했기 때문에 유리 포장 수요를 더욱 부추겼습니다. 각국의 제약 제조업체에 의한 신약이나 백신의 승인과 유통에 따라 유리 포장의 사용은 계속 확대될 것으로 예상됩니다.

- 유리 포장은 주로 의약품의 주요 포장 옵션으로 제공되며 제약 산업에서 최고 수준의 선택이 되었습니다. 주된 이유는 지속가능성, 불활성, 불침투성, 품질 저하 없이 재활용 가능, 재사용 가능 등의 장점이 있기 때문입니다. 유리 용기는 주요 포장 재료 중 하나로 제약 부문에서 널리 사용됩니다. 만성 질환의 유행이 증가하고 COVID-19 백신의 생산량이 계속 증가함에 따라 1차 포장, 특히 유리 용기 수요가 급증할 것으로 예상됩니다.

- 아시아태평양에서 만성 질환의 유병률 증가는 의약품 포장 시장의 확대를 촉진하는 주요 요인입니다. 당뇨병, 심혈관 질환, 암, 호흡기 질환 등의 질환은 지속적인 투약이 필요합니다. 그 결과, 이러한 의약품을 안전하게 보관, 보호하고 최적의 효율로 유통하기 위한 다양한 의약품 포장 솔루션에 대한 요구가 높아지고 있습니다. 세계보건기구(WHO)에 따르면 비전염성 질환 증가는 이 지역, 특히 중동 및 아프리카의 만성질환 부담 증가에 기여하고 있습니다.

- 1차 포장 유리 솔루션 제조업체인 Stoelzle은 2023년 11월에 개최된 CPHI 바르셀로나 무역 박람회에서 환경 친화적인 최신 PharmaCos 라인을 발표했습니다. 이 포장 솔루션의 새로운 라인은 재활용 유리의 비율이 높고(앰버 유리로 73%, 플린트 유리에서 38%) 경량 병 디자인을 자랑합니다. 또한 이 새로운 라인은 의료 산업의 엄격한 기준을 충족하기 위해 의약품 등급 시설에서 생산됩니다. 공급업체의 이러한 중요한 혁신은 시장 성장을 가속할 것으로 예상됩니다.

- Bormioli Pharma에 따르면, 현재 유형 II와 유형 III 유리를 위해 특별히 고안된 다양한 재생 유리 제품이 판매되고 있습니다. 이 제품은 의약품으로 인증된 외부 공급망에서 조달한 재료를 활용합니다. 화학적 및 기계적 처리는 재생 재료를 새로운 생산 사이클의 기초가되는 유리 분말로 변환합니다. 동시에 볼미 올리파마는 저배출 가스로 개발 프로젝트에도 적극적으로 노력하고 있습니다. 이 퍼니스는 환경 실적를 최소화하는 혁신적인 기술과 산업 공정을 통합합니다.

- 또한 일본과 같은 국가에서 유리 포장 기술 시장은 의약품 공급업체가 의약품 생산을 강화하기 위해 수행하는 투자 증가로 인한 것으로 간주됩니다. 2023년 3월에 Takeda가 발표한 오사카에 혈장 유래 치료(PDT)의 새로운 제조 시설을 건설하기 위해 약 1,000억 엔(7억 5,000만 달러)을 투자할 계획이 있습니다. 이번 투자는 Takeda에게 일본에서 과거 최대 규모의 생산 능력 증강이 됩니다. 2030년까지의 가동을 예정하고 있는 이 최신 시설은 이 유형의 시설로서는 국내 최대가 되어, Takeda의 혈장 제조 능력을 대폭 증강하게 됩니다.

현저한 성장이 기대되는 인도

- 인도는 의약품 포장 시장에서 가장 빠르게 성장하는 지역 중 하나가 될 것으로 예상됩니다. 의약품 포장 부문은 기술 혁신과 새로운 치료의 상승으로 최근 몇 년간 현저한 성장을 이루고 있습니다. COVID-19 팬데믹의 발생은 효율적인 제품 포장과 유통의 중요성을 부각시켰습니다. 그 결과, 포장을 포함한 제조와 유통의 양 공정을 가속시키는 것이 중시되고 있습니다. 그 결과, 포장 기업은 신속한 기술 혁신을 강요당하게 되어, 보다 신속한 오퍼레이션을 요구하는 목소리가 높아지고 있다

- 인도는 특히 제네릭 의약품과 비용 효율적인 의약품의 생산에 있어서 의약품 섹터의 주요 기업으로 부상할 것으로 예상됩니다. 이 나라는 많은 선진국들에게 제네릭 의약품의 주요 공급국으로서 중요한 역할을 하고 있습니다. 제네릭 의약품 생산량 증가와 국제 유통은 인도의 의약품 포장 산업의 확대를 촉진하는 중요한 요소입니다. 게다가 만성질환의 급증과 의약품 제조 사업에 대한 투자 증가는 시장 내 수요의 대폭적인 증가로 이어집니다.

- 이 지역에서는 플라스틱 포장 유형 수요가 현저하게 증가할 것으로 예상됩니다. 의료용품과 의약품에 대한 요구의 급증이 인도에서 플라스틱 의약품 포장의 확대를 뒷받침하고 있습니다. 이 지역 시장 잠재력을 높이기 위해 수많은 기업들이 이 기술에 많은 투자를 하고 있습니다. 예를 들어, 2023년 3월 스페인 포장 회사인 인덴 파르마는 의약품용 플라스틱 포장을 전문으로 하는 오스트리아의 ALPLApharma와의 제휴를 통해 인도에서의 사업 확대를 의도하고 있습니다. 이러한 주목할만한 진보가 시장의 성장을 가속할 것으로 예측되고 있습니다.

- InvestIndia의 보고서에 따르면 인도는 세계 최대의 제네릭 의약품 공급국이며 세계 공급량의 20%를 차지합니다. 또한 인도는 세계 최대의 백신 생산국이기도 합니다. 미국 이외에서는 미국 식품의약국(US FDA)이 정하는 기준에 준거한 제약공장의 수가 가장 많은 것도 인도입니다. 3,000개가 넘는 제약회사와 10,500개가 넘는 제조시설을 보유한 인도는 제약산업에서 견고한 네트워크와 첨단기능을 가진 노동력을 가지고 있습니다. 또한 인도는 세계 백신 수요의 약 60%를 충족하며 DPT, BCG, 홍역 백신의 주요 공급국이기도 합니다. 의약품 제조에서 이러한 광범위한 능력은 확실히이 지역의 포장 비즈니스 시장을 자극하는 것으로 예상됩니다.

- 게다가 InvestIndia에 따르면 인도 제약산업은 주로 수출 증가와 국내 시장 성장으로 2018년부터 22년까지 평균 성장률 9.47%를 기록하며 423억 4,000만 달러에 달했습니다. 예측에 따르면 의약 부문은 2024년에 650억 달러, 2030년에는 1,200억 달러에 이를 전망입니다. 지속적인 성장을 보장하기 위해 정부는 연구와 기술 혁신을 촉진하는 다양한 이니셔티브를 실시했습니다. 2047년을 향한 비전의 일환으로, 정부는 Vasudhaiva Kutumbakam의 원칙에 따라 인도를 저렴한 가격으로 혁신적이고 고품질의 의약품 및 의료기기 생산의 세계 리더로 확립하는 것을 목표로 하고 있습니다. 이러한 중요한 개발은 포장 부문에 시장 개척의 기회를 가져올 것으로 예상됩니다.

아시아태평양 의약품 포장 산업 개요

아시아태평양의 의약품 포장 시장은 경쟁이 치열하고 많은 지역과 세계 진출 기업이 존재합니다. 주요 진출기업으로는 Amcor Ltd., West Pharmaceutical Services Inc., CCL Industries Inc., NIPRO Corporation 등이 있습니다. 각 회사는 신제품을 출시하고 생산 부문을 확대하여 시장 점유율을 늘리고 있습니다. 최근 몇 가지 동향을 발표합니다.

- 2024년 1월, 100% 재활용 폴리에틸렌 테레프탈레이트("PET") 플라스틱과 폴리에스테르 섬유를 제조하여 순환 플라스틱 경제를 가속화하는 것을 사명으로 하는 청정 기술 기업 루프 인더스트리(Loop Industries Inc.)와 제약 포장 및 의료 기기 분야의 세계적인 기업인 보르미올리 파마(Bormioli Pharma)가 100% 재활용 버진 품질의 루프 PET 수지로 제조한 혁신적인 제약 포장 병을 출시했습니다.

- 2023년 6월, CIncorporated는 SGD Pharma와 제휴하여 테랑가나 주에 의약품 포장용 유리를 제조하는 최신 시설을 설립했습니다. 이 시설의 설립에는 양사에서 50억 루피 이상을 투자하는 것으로 보고되었습니다. 이번 코닝사와의 제휴는 제약산업에 있어서의 컨버팅 기술의 향상과, 견고한 공급 체인의 확보를 향한 중요한 한 걸음입니다. 양사가 협력함으로써 제약 제조업체가 생산 능력과 품질에 관한 증대하는 과제를 해결하고, 필수적인 의약품에 대한 세계 수요 증가에 대응할 수 있도록 지원하는 것을 목표로 하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 상정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장 성장 촉진요인

- 신흥국의 의약품 포장 도입 증가

- 시장 성장 억제요인

- 원료 비용의 변동

제5장 시장 세분화

- 재료별

- 플라스틱

- 종이 및 판지

- 유리

- 알루미늄 호일

- 유형별

- 앰풀

- 블리스터 팩

- 플라스틱 병

- 주사기

- 바이알

- 주입

- 기타

- 약물전달 형태별

- 경구약 포장

- 주사제 포장

- 폐 약물 포장

- 기타

- 국가별

- 인도

- 일본

- 중국

- 호주

- 기타 아시아태평양

제6장 경쟁 구도

- 기업 프로파일

- Amcor Ltd

- CCL Industries Inc.

- West Pharmaceutical Services Inc.

- Gerresheimer AG

- Schott AG

- NIPRO Corporation

- Wihuri Group

- Klockner Pentaplast Group

- Catalent Pharma Solutions Inc.

- Berry Global Group Inc.

제7장 투자 분석

제8장 시장의 미래

KTH 25.02.11The Asia Pacific Pharmaceutical Packaging Market size is estimated at USD 44.57 billion in 2025, and is expected to reach USD 62.49 billion by 2030, at a CAGR of 6.99% during the forecast period (2025-2030).

Key Highlights

- Pharmaceutical packaging involves the assembly of elements required to enclose, maintain, safeguard, and distribute a secure and effective medicinal product, ensuring that a secure and effective dosage form is accessible at any given time prior to the drug product's expiration date. Appropriate packaging materials are essential for offering tamper-evident security, which aids in deterring the consumption of counterfeit medications. Furthermore, premium packaging materials must comply with rigorous regulatory guidelines.

- The pharmaceutical packaging manufacturers are anticipated to witness significant opportunities in Asia-Pacific, thanks to the increasing investments in the pharmaceutical sector. The rising demand for pharmaceutical drugs and advancements in pharmaceutical technology are directly contributing to the demand for glass bottles, ampules, and other glass packaging solutions. As chronic illnesses continue to rise and the production of COVID-19 vaccine doses remains substantial, the demand for primary packaging is expected to surge, specifically for glass containers.

- Glass packaging is expected to drive the market's growth in the region's pharma packaging sector. Pharmaceutical companies utilize glass containers to package a diverse array of pharmaceutical products, including injectable medications, solid oral pills, liquid formulations, and biologics. The rapid growth of glass packaging is driven by factors such as pharmaceutical manufacturing operations, the rising demand for specialty pharmaceuticals, and the expansion of healthcare infrastructure. This trend is particularly evident in countries like China, India, Japan, and South Korea, where pharmaceutical industries are experiencing significant growth, leading to a surge in demand for glass packaging solutions.

- The plastic bottles industry is projected to experience substantial growth in the coming years. The utilization of PET is steadily increasing in the region, resulting in a weight reduction of up to 90% compared to glass, thus enabling a more cost-effective transportation procedure. Presently, plastic bottles crafted from PET are extensively substituting bulky and delicate glass bottles in the pharmaceutical sector, providing reusable packaging for different liquids. The rising advancements in plastic PET technology for the pharmaceutical industry are anticipated to boost market prospects.

- Additionally, the government's initiatives to enhance the pharmaceutical sector in the area are anticipated to propel the market's expansion. For example, the measures implemented by the Chinese government to expedite the modernization of the nation's healthcare system are projected to stimulate the advancement of the pharmaceutical packaging industry. Moreover, China is proactively improving its pharmaceutical packaging infrastructure and resources while broadening its range of pharmaceutical products, potentially opening up new avenues for pharmaceutical packaging companies.

- China's presence in the global pharmaceutical market has been steadily growing, serving as both a major consumer and a vital component in the global pharmaceutical industry and supply chains. The rapid expansion of the pharmaceutical sector in recent years, driven by scientific and technological advancements, is projected to continue in the future. In December 2023, Danish pharmaceutical firm Novo Nordisk revealed its plan to invest CNY 400 million (USD 59.6 million) in a newly established company in the region by June 2026. These substantial developments are anticipated to drive the demand for pharmaceutical packaging services.

- The packaging industry experienced significant effects due to the COVID-19 pandemic. With a shift in focus toward infectious diseases and vaccines, there was a decrease in successful clinical trials and research and development activities in therapeutic areas like diabetes and hypertension. However, the pharmaceutical industry witnessed a surge in drug demand for various diseases during the pandemic, leading to substantial investments in the packaging business. Fortunately, the pharmaceutical industry quickly recovered by emphasizing the need for safe and hygienic packaging in response to the pandemic.

Asia Pacific Pharmaceutical Packaging Market Trends

Glass Packaging is Expected to Witness Significant Growth

- Glass packaging is widely considered the leading choice for pharmaceutical products in the packaging industry. Its popularity stems from its sustainable nature, inertness, impermeability, recyclability, and ability to be reused without compromising quality. The COVID-19 pandemic further fueled the demand for glass packaging as the need for medication significantly increased. With the approval and distribution of new drugs and vaccines by pharmaceutical manufacturers in various countries, the use of glass packaging is expected to continue expanding.

- Glass packaging is primarily provided as the main packaging option for pharmaceutical products and is one of the top choices in the pharmaceutical industry. This is mainly because it offers several advantages, including sustainability, inertness, impermeability, recyclability without any compromise in quality, and reusability. Glass containers have become widely utilized in the pharmaceutical sector as one of the primary packaging materials. As the prevalence of chronic diseases increases and the production of COVID-19 vaccine doses continues to rise, there is an anticipated surge in the demand for primary packaging, specifically glass containers.

- The increasing prevalence of chronic diseases in the APAC region is a major factor driving the expansion of the pharmaceutical packaging market. Conditions such as diabetes, cardiovascular diseases, cancer, and respiratory ailments necessitate continuous medication. As a result, there is a rising need for diverse pharmaceutical packaging solutions to securely store, safeguard, and distribute these medications with optimal efficiency. As per the World Health Organization (WHO), the rise in noncommunicable diseases is contributing to the escalating burden of chronic illnesses in the region, especially in the SEA region.

- The primary packaging glass solutions manufacturer, Stoelzle, unveiled their latest eco-friendly PharmaCos line at the CPHI Barcelona trade show in November 2023. This new line of packaging solutions boasts a high percentage of recycled glass (73% in amber glass and 38% in flint glass) and lightweight bottle design. Additionally, the new line is produced in a pharmaceutical-grade facility to meet the strict standards of the healthcare industry. Such significant innovations by the vendors are expected to drive the market's growth.

- Bormioli Pharma states that currently, various recycled glass products are available specifically designed for type II and type III glass. These products utilize materials sourced from an external supply chain that is certified for pharmaceutical use. Through chemical and mechanical processing, the recycled materials can be transformed into glass powder, which serves as the foundation for the new production cycle. Simultaneously, Bormioli Pharma is actively involved in projects aimed at developing low-emission furnaces. These furnaces incorporate innovative technologies and industrial processes that minimize their environmental footprint.

- Moreover, the market for glass packaging techniques in countries like Japan will be driven by the increasing investments made by pharmaceutical vendors to enhance pharmaceutical production. A notable example is Takeda's announcement in March 2023, stating its plan to invest approximately JPY 100 billion (USD 0.75 billion) in constructing a new manufacturing facility for plasma-derived therapies (PDTs) in Osaka, Japan. This investment represents Takeda's largest-ever expansion of manufacturing capacity in Japan. The upcoming state-of-the-art facility, expected to be operational by 2030, will be the largest of its kind in the country and will significantly increase Takeda's plasma manufacturing capacity.

India is Expected to Witness Significant Growth

- India is expected to be one of the fastest-growing regions in the pharmaceutical packaging market. The pharmaceutical packaging sector has witnessed significant growth in recent years, driven by innovations and the rise of new treatments. The onset of the COVID-19 pandemic underscored the importance of efficient product packaging and distribution. As a result, there's a growing emphasis on accelerating both manufacturing and distribution processes, including packaging. Consequently, packaging firms are under mounting pressure to innovate swiftly, meeting the demand for faster operations.

- India is anticipated to emerge as a key player in the pharmaceutical sector, especially in the production of generic drugs and cost-effective medication. The country plays a vital role as a primary provider of generic medicines to numerous advanced nations. The rising output and international distribution of generic drugs are significant factors driving the expansion of the Indian pharmaceutical packaging industry. Additionally, the surge in chronic illnesses and the rise in investments in drug manufacturing operations will lead to a substantial increase in demand within the market.

- The region is anticipated to experience a notable increase in demand for plastic packaging types. The surge in the need for medical supplies and medications has propelled the expansion of plastic pharma packaging in India. Numerous companies are making substantial investments in this technology to enhance the region's market potential. For instance, in March 2023, Spanish packaging company Inden Pharma intended to broaden its operations in India through a partnership with Austria-based ALPLApharma, which specializes in plastic packaging for pharmaceuticals. These noteworthy advancements are projected to stimulate growth in the market.

- InvestIndia reports that India is the largest global provider of generic medicines, making up 20% of the global supply by volume. Additionally, India is the top producer of vaccines worldwide. Outside of the United States, India has the highest number of pharmaceutical plants that comply with the standards set by the US Food and Drug Administration (US FDA). With over 3,000 pharmaceutical companies and more than 10,500 manufacturing facilities, India possesses a robust network and a highly skilled workforce in the pharmaceutical industry. Moreover, India fulfills approximately 60% of the global demand for vaccines and is a major supplier of DPT, BCG, and Measles vaccines. These extensive capabilities in pharmaceutical manufacturing will undoubtedly stimulate the packaging business market in the region.

- Moreover, InvestIndia states that the Indian pharmaceutical industry experienced an average growth rate of 9.47% from FY18 to FY22, reaching USD 42.34 Billion, mainly due to increased exports and a growing domestic market. Forecasts suggest that the pharma sector is expected to reach a value of USD 65 billion in 2024 and USD 120 billion in 2030. To ensure sustained growth, the government has implemented various initiatives to promote research and innovation. As part of its vision for 2047, the government aims to establish India as a global leader in producing affordable, innovative, and high-quality pharmaceuticals and medical devices, in line with the principle of Vasudhaiva Kutumbakam. Such significant developments will provide market opportunities in the packaging sector.

Asia Pacific Pharmaceutical Packaging Industry Overview

The Asia-Pacific pharmaceutical packaging market is competitive, with many regional and global players. Some major players are Amcor Ltd, West Pharmaceutical Services Inc., West Pharmaceutical Services Inc., CCL Industries Inc., and NIPRO Corporation. Companies are increasing their market share by launching new products and expanding production units. Some of the recent developments are:

- January 2024: Loop Industries Inc., a clean technology company whose mission is to accelerate a circular plastics economy by manufacturing 100% recycled polyethylene terephthalate ("PET") plastic and polyester fiber, and Bormioli Pharma, an international player in pharmaceutical packaging and medical devices, launched an innovative pharmaceutical packaging bottle manufactured with 100% recycled virgin quality Loop PET resin.

- June 2023: CIncorporated partnered with SGD Pharma to establish a state-of-the-art facility for producing pharmaceutical packaging glass in Telangana. It was reported that the two companies would collectively invest more than INR 500 crore in setting up this facility. This collaboration with Corning is a significant move in advancing converting technology within the pharmaceutical sector and ensuring a robust supply chain. By working together, these companies aim to assist pharmaceutical manufacturers in addressing the growing challenges related to capacity and quality, as well as meeting the rising global demand for essential medications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Supplier

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Increasing Adoption of Pharmaceutical Packaging in Emerging Economies

- 4.5 Market Restraints

- 4.5.1 Fluctuations in Raw Material Cost

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Paper and Paper Board

- 5.1.3 Glass

- 5.1.4 Aluminum Foil

- 5.2 By Type

- 5.2.1 Ampoules

- 5.2.2 Blister Packs

- 5.2.3 Plastic Bottles

- 5.2.4 Syringes

- 5.2.5 Vials

- 5.2.6 IV fluids

- 5.2.7 Other Types

- 5.3 By Drug Delivery Mode

- 5.3.1 Oral Drug packaging

- 5.3.2 Injectable Drug packaging

- 5.3.3 Pulmonary Drug Packaging

- 5.3.4 Other Drug Delivery Modes

- 5.4 By Country

- 5.4.1 India

- 5.4.2 Japan

- 5.4.3 China

- 5.4.4 Australia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor Ltd

- 6.1.2 CCL Industries Inc.

- 6.1.3 West Pharmaceutical Services Inc.

- 6.1.4 Gerresheimer AG

- 6.1.5 Schott AG

- 6.1.6 NIPRO Corporation

- 6.1.7 Wihuri Group

- 6.1.8 Klockner Pentaplast Group

- 6.1.9 Catalent Pharma Solutions Inc.

- 6.1.10 Berry Global Group Inc.