|

시장보고서

상품코드

1640369

중동 및 아프리카의 폴리우레탄 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Middle East And Africa Polyurethane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

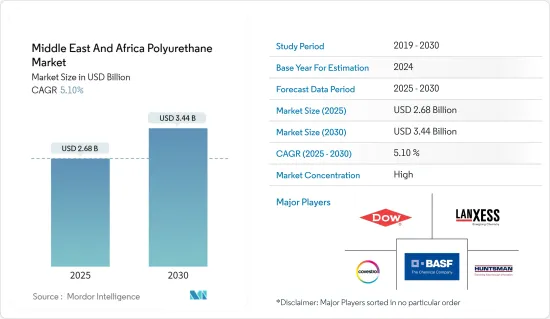

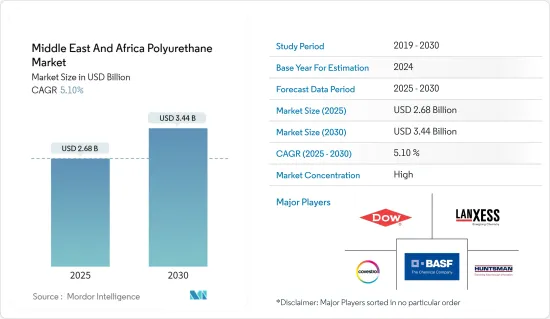

중동 및 아프리카의 폴리우레탄 시장 규모는 2025년에 26억 8,000만 달러로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 5.1%로, 2030년에는 34억 4,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- COVID-19의 발생은 시장에 부정적인 영향을 미쳤습니다. COVID-19의 발생을 막기 위한 프로젝트의 중단이나 지연, 이동 제한, 생산 정지, 노동력 부족 등이 폴리우레탄 시장의 성장 저하를 초래했습니다. 그러나 2021년부터 가구, 인테리어, 자동차 등 다양한 최종 용도의 소비 증가로 크게 회복되었습니다.

- 단기적으로는 건축 및 건설산업에서의 수요 증가와 전자·소비자용 전자기기산업으로부터의 단열재에 대한 요구의 고조가 조사한 시장의 성장을 가속하는 주요 요인이 되고 있습니다.

- 반면 원료 가격 변동과 폴리우레탄 페인트의 독성이 시장 성장을 방해할 것으로 예상됩니다.

- 중동의 건축물에 관한 에너지 효율화 시책에 대한 의식의 높아지는 향후 시장 성장의 기회가 될 것 같습니다.

- 사우디아라비아는 시장을 독점하고 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

중동 및 아프리카의 폴리우레탄 시장 동향

건축 및 건설산업에서의 수요 증가

- 폴리우레탄의 가장 광범위한 용도는 건축 및 건설 산업입니다. 폴리우레탄은 강력하면서도 가볍고 성능이 뛰어나고 내구성과 범용성이 뛰어난 고성능 제품의 제조에 사용됩니다.

- 건축 및 건설 산업은 경질 폴리 우레탄 폼의 가장 큰 소비자입니다. 경질 폴리우레탄 폼 단열재를 사용하면 에너지 효율, 고성능, 다용도, 열적/기계적 성능, 환경 친화적인 특성 등 많은 이점이 있습니다.

- '쿠웨이트 비전 2035'의 '서스테이너블 생활 환경'의 축에는 5개의 기둥이 있으며, 그중 가장 중요한 것은 2029년까지 종료되는 32억 2,000만 KWD(105억 달러) 규모의 5개 프로젝트를 통해 6만 5,500호의 주택을 공급해 시민들에게 주거 서비스를 제공할 게획입니다.

- 이러한 프로젝트가 시행되면 현재 91,000개의 주택 수요의 약 72%를 충족하게 됩니다. 주택 케어 계획의 첫 번째 프로젝트는 자벨 알 아하마드시의 쿠웨이트 2035(신 쿠웨이트) 구상을 중심으로 한 것으로, 완성률은 95%입니다. 두 번째 프로젝트는 알 무트라아 시에서 완성률은 64%로 2023년 말까지 완성을 목표로 계획되었습니다.

- 3번째 프로젝트는 교외 사우스 압둘라 알 무바락시로 완성률은 72%, 2025년 말까지 완성 예정입니다. 네 번째 프로젝트인 남쪽 사바 알 아하마드의 완성률은 아직 준비 단계이기 때문에 약 14%로 2029년에 완성될 것으로 보입니다. 이 남서드 알 압둘라는 아직 준비 단계에서 2029년에 종료되기 때문에 완성률은 13%입니다. 이 때문에 쿠웨이트에서의 주택 건설 증가로 경질 폼이 필요하게 되어 쿠웨이트에서의 폴리우레탄 시장 수요가 더욱 높아질 것으로 보입니다.

- 따라서 앞서 언급한 요인은 예측 기간 동안 폴리우레탄 시장을 밀어올릴 것으로 예상됩니다.

사우디아라비아가 시장을 독점

- 중동 및 아프리카의 폴리우레탄 시장에서는 사우디아라비아가 가장 큰 점유율을 차지하고 있습니다. 이 나라에서는 투자나 건설, 가구, 전자기기의 활동이 활발해지고 있기 때문에 폴리우레탄 수요는 예측기간을 통해 증가할 것으로 보입니다. 인구와 가처분소득 증가로 고품질 주택 개발 수요가 높아졌습니다.

- 사우디아라비아의 건설 시장은 '비전 2030', 'NTP2020', 석유의 다각화를 위한 몇몇 진행 중인 개혁을 통해 큰 성장을 보이고 유리한 잠재력을 제공할 것으로 예상됩니다. 비전 2030, NTP2020, 민간 부문 투자 촉진, 진행 중인 개혁은 예측 기간 동안 사우디아라비아 건설 산업에 의한 폴리우레탄 시장의 성장 촉진요인이 될 것으로 예상됩니다. 사우디아라비아의 '비전 2030'은 지방자치단체의 전국 주택 인프라 개발에 많은 투자를 하면서 건설산업을 활성화하고 증가하는 국제 진출기업에 대한 관심을 창출하고 있습니다.

- 또한 '비전 2030' 아래 2030년까지 사우디아라비아 전역에서 11,000개 이상의 고급스러운 객실을 갖춘 호텔이 새롭게 80개 개업할 예정입니다. 따라서 건설 및 호텔 가구에 대한 투자가 증가하고 연질 형태 수요가 예상됩니다.

- 현재 사우디아라비아 경제는 포스트 석유 시대를 맞이하고 있으며 건설 중인 메가 시티가 미래의 성장을 가져올 것으로 예상됩니다. 산업계에 따르면 사우디아라비아에서는 현재 5,200개 이상의 건설 프로젝트가 진행 중이며, 그 총액은 8,190억 달러에 이릅니다. 이 프로젝트는 걸프 협력 회의(GCC) 전반에 걸쳐 진행 중인 프로젝트 총액의 약 35%를 차지합니다.

- 사우디아라비아의 주요 도시 건설 프로젝트에는 마카의 지자체·농촌 문제성이 개발한 각각 213억 달러의 압도라 국왕 경비 시설(5단계)과 그랜드 모스크(성할람·모스크 확대 공사) 등이 있습니다.

- 사우디아라비아의 상위 건설 프로젝트에는 Neom, 홍해 프로젝트, Qiddiya 엔터테인먼트 시티, Amaala, Al-Ula의 Jean Nouvel's Sharaan 리조트, Makkah Grand Mosque-Third Expansion, Jeddah Tower, 주택성의 Sakani Homes, Jabal Omar, Al 드 메디컬 시티 확대 공사, 킹 압둘라 빈 압둘 아지즈 메디컬 컴플렉스, 킹 살만 에너지 파크(스파크), 사우디 아람코의 베리와 마르장, 하너지 솔라 파크, 두마트 알 잔달 풍력 발전소 등이 있습니다.

- 사우디아라비아의 '아미드 비전 2030'은 국가 인프라 성장을 목표로 한 거대한 프로젝트에 의해 지원되는 중요한 개발 계획입니다. 환경에 대한 노력, 시민의 삶의 질 향상, 강력한 경제 창조에 중점을 두고, 비전 2030은 변화를 가져올 것을 목표로 합니다. 비전 2030과 이에 상응하는 국가 개조 계획(NTP)의 도입으로 의료, 교육, 인프라 등 여러 부문에 대한 투자가 확대되고 있습니다.

- 사우디아라비아에서는 많은 주택·상업 프로젝트가 개시되고 있어, 동국의 건설 활동의 활성화가 기대되고 있습니다. 예를 들어, 사우디아라비아 정부는 관광객을 유치하기 위해 국내 각지에서 여러 메가 프로젝트를 시작하고 순조롭게 진행하고 있습니다. 집합 주택이 있는 메가 프로젝트 중 일부는 Qiddiya입니다. 2025년까지 4,000호, 2030년까지 1만 1,000호의 주택이 건설되어 유명한 문화적 랜드마크가 됩니다. 딜리어 게이트에서는 리야드 프로젝트에서 2027년까지 2만호 주택이 건설됩니다. 뉴 무라바에서는 리야드 시내 프로젝트에서 10만 4,000호 주택이 건설될 예정입니다.

- 사우디아라비아는 개발 도중에 있으며, 눈부신 금액의 투자를 받고 있습니다. 사우디아라비아는 2022년 3월 8,000킬로미터의 새로운 궤도를 놓고 철도망의 규모를 3배 이상으로 확대할 것이라고 선언했습니다. 2021년 7월에는 1,470억 달러가 운송 및 물류 부문에 할당되었습니다. 목표가 달성되는 2030년까지 이러한 산업은 국가 GDP의 10%를 차지하고 현재보다 4% 증가합니다.

- Gulf Council Corporation에 따르면 사우디아라비아는 의료 시설에 664억 9,000만 달러의 투자를 계획하고 있으며, 민간 부문의 협력도 얻어 2030년까지 65% 상승할 전망입니다.

- 이러한 점에서 사우디아라비아의 폴리우레탄 시장은 앞으로 수년간 안정적인 성장이 예상되고 있습니다.

중동 및 아프리카의 폴리우레탄 산업 개요

중동 및 아프리카의 폴리우레탄 시장은 고도로 통합되어 있습니다. 이 시장의 주요 기업으로는 Covestro AG, BASF SE, Dow, LANXESS, Huntsman International LLC 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 전자기기 산업에서 단열재 수요의 증대

- 건축 및 건설 산업에서의 수요 증가

- 기타 촉진요인

- 억제요인

- 불안정한 원료 가격

- 폴리우레탄·코팅의 독성

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(규모별)

- 용도

- 발포체

- 경질 폼

- 연질 폼

- 코팅제

- 접착제 및 실란트

- 엘라스토머

- 기타

- 발포체

- 최종 사용자 산업

- 가구 및 인테리어

- 건축 및 건설

- 전자기기

- 자동차

- 신발

- 포장

- 기타

- 지역

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 쿠웨이트

- 카타르

- 모로코

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 인수합병, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- BASF SE

- BCI Holding SA

- Covestro AG

- Dow

- Huntsman International LLC

- Kuwait Polyurethane Industries WLL

- LANXESS

- Mitsui Chemicals, Inc.

- Perfect Rubber

- Wanhua Chemical Group Co.,Ltd

제7장 시장 기회와 앞으로의 동향

- 중동 지역의 건물 관련 에너지 효율 정책에 대한 인식 증가

- 바이오 기반 폴리우레탄에 대한 수요 증가

The Middle East And Africa Polyurethane Market size is estimated at USD 2.68 billion in 2025, and is expected to reach USD 3.44 billion by 2030, at a CAGR of 5.1% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 outbreak negatively impacted the market. Stoppage or slowdown of projects, movement restrictions, production halts, and labor shortages to contain the COVID-19 outbreak led to a decline in the polyurethane market growth. However, it recovered significantly from 2021, owing to rising consumption from various end-use applications, including furnishing, interiors, and automotive.

- Over the short term, increasing demand from the building and construction industry and growing requirement for thermal insulation from the electronics and appliances industry are some of the major factors driving the growth of the market studied.

- On the flip side, volatile raw material prices and the toxic nature of polyurethane coatings are expected to hinder the growth of the market.

- Growing awareness of the Energy Efficiency Policy related to buildings in the Middle Eastern region is likely to act as an opportunity for market growth in the future.

- Saudi Arabia is expected to dominate the market and will also witness the highest CAGR during the forecast period.

Middle East and Africa Polyurethane Market Trends

Increasing Demand from the Building and Construction Industry

- The most extensive application of polyurethane is in the building and construction industry. Polyurethanes are used to make high-performance products that are strong but lightweight, perform well, and are durable and versatile.

- The building and construction industry is the largest consumer of rigid polyurethane foam. There are many benefits of using rigid polyurethane foam insulation, including its energy efficiency, high performance, versatility, thermal/mechanical performance, and environment-friendly nature.

- The sustainable living environment axis in Kuwait Vision 2035 includes five pillars, the most prominent of which is to provide housing care to citizens through what is planned to ensure the provision of 65.5 thousand housing units through five projects costing about KWD 3.22 billion (USD 10.5 billion), the last of which ends by 2029.

- When these projects are implemented, the state will have met approximately 72% of the current housing requests, which stands at 91,000. The first project of the residential care plan revolves around the vision of Kuwait 2035 (New Kuwait) in the city of Jaber Al-Ahmad, which has a completion rate of 95%. The second project is in the city of Al-Mutla'a, with a completion rate of 64%, to be completed by the end of 2023.

- The third project is in the suburb of South Abdullah Al-Mubarak, which has a completion rate of 72% and will be completed by the end of 2025. The completion rate in the fourth project, which is the South Sabah Al-Ahmad, is about 14%, as it is still in the preparation stage, and it is expected to be completed in 2029. This south of Saad Al-Abdullah has a completion rate of 13% as it is still in its preparatory phase and ends in 2029. Therefore, the growing residential housing construction in Kuwait will demand rigid foams, which will further rise the demand for the polyurethane market in Kuwait.

- Thus, the aforementioned factors are expected to boost the market for polyurethanes during the forecast period.

Saudi Arabia to Dominate the Market

- Saudi Arabia holds the largest share in the Middle East and African polyurethane market. The demand for polyurethane is expected to rise throughout the forecast period due to rising investments and construction, furniture, and electronics activities in the country. The rise in the population and disposable income increased the demand for the development of better-quality residential buildings.

- The Saudi Arabian construction market is expected to witness significant growth and offer lucrative potential due to its Vision 2030, NTP 2020, and several ongoing reforms to diversify away from oil. Vision 2030, NTP 2020, the private sector investment boost, and the ongoing reforms are expected to be the growth drivers for the Saudi polyurethane market from the country's construction industry during the forecasted period. Saudi Arabia's Vision 2030, along with a significant investment in housing and infrastructure development promoted across the country by local authorities, is revitalizing the construction industry and generating interest in a growing number of international players.

- Moreover, under Vision 2030, 80 new hotels with more than 11,000 luxurious rooms will be opened across Saudi Arabia by 2030. Therefore, increasing investments in construction and hotel furniture are expected to create demand for flexible foam.

- Currently, the country's economy is entering a post-oil era in which the kingdom's mega-cities, which are under construction, will provide future growth. According to industry sources, more than 5,200 construction projects are currently ongoing in Saudi Arabia at a value of USD 819 billion. These projects account for approximately 35% of the total value of active projects across the Gulf Cooperation Council (GCC).

- Some of the major urban construction projects in Saudi Arabia include the King Abdullah Security Compounds (Phase 5) and the Grand Mosque (Holy Haram Mosque expansion), each valued at USD 21.3 billion and developed by the Ministry of Municipalities and Rural Affairs in Makkah.

- The top construction projects in Saudi Arabia include Neom, the Red Sea Project, Qiddiya entertainment city, Amaala, Jean Nouvel's Sharaan resort in Al-Ula, Makkah Grand Mosque - Third Expansion, Jeddah Tower, Ministry of Housing's Sakani Homes, Jabal Omar, Al Widyan, Riyadh Metro, Riyadh Rapid Bus Transit System, King Fahd Medical City Expansion, King Abdullah Bin Abdulaziz Medical Complexes, King Salman Energy Park (Spark), Saudi Aramco's Berri and Marjan, Hanergy Solar Park, Dumat Al Jandal Wind Power Plant, Saudi Aramco-Total's PIB factory, and Pan-Asia bottling facility.

- Saudi Arabia's Amid Vision 2030 is a significant development plan supported by megaprojects aimed at the growth of the nation's infrastructure. With an emphasis on environmental commitments, enhancing citizen quality of life, and creating a strong economy, Vision 2030 aspires to bring about change. Investments in several fields, including healthcare, education, and infrastructure, have expanded as a result of the introduction of Vision 2030 and the corresponding National Transformation Plan (NTP).

- Many residential and commercial projects are being launched in Saudi Arabia, which is anticipated to increase the country's construction activity. For instance, the Saudi government has started several mega projects, which are well underway around the country to attract tourists. Some of the mega projects that will have residential complexes are Qiddiya: The project will become a prominent cultural landmark with 4,000 residential units by 2025 and 11,000 units by 2030. Diriyah Gate: The project in Riyadh will include 20,000 residential units by 2027. New Murabba: The Riyadh downtown project is likely to house 104,000 residential units.

- Saudi Arabia is developing, and the nation is receiving impressive amounts of investment. The nation declared in March 2022 that it would more than triple the size of its rail network by installing 8,000 kilometers of new track. In July 2021, USD 147 billion was allocated to the transportation and logistics sectors. By 2030, when the targets have been met, these industries will contribute 10% of the nation's GDP, a 4% increase from today.

- According to the Gulf Council Corporation, Saudi Arabia has planned to invest USD 66.49 billion in healthcare facilities, with help from the private sector, whose participation is expected to rise by 65% by 2030.

- With all of these things, the Saudi Arabian polyurethane market is expected to grow steadily over the next few years.

Middle East and Africa Polyurethane Industry Overview

The Middle East and African polyurethane market is highly consolidated in nature. Some of the major players in the market include Covestro AG, BASF SE, Dow, LANXESS, and Huntsman International LLC, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Requirement of Thermal Insulation from the Electronics and Appliances Industry

- 4.1.2 Rising Demand from the Building and Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Toxic Nature of Polyurethane Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Foams

- 5.1.1.1 Rigid Foam

- 5.1.1.2 Flexible Foam

- 5.1.2 Coatings

- 5.1.3 Adhesives and Sealants

- 5.1.4 Elastomers

- 5.1.5 Other Applications

- 5.1.1 Foams

- 5.2 End-user Industry

- 5.2.1 Furniture and Interiors

- 5.2.2 Building and Construction

- 5.2.3 Electronics and Appliances

- 5.2.4 Automotive

- 5.2.5 Footwear

- 5.2.6 Packaging

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 South Africa

- 5.3.4 Egypt

- 5.3.5 Kuwait

- 5.3.6 Qatar

- 5.3.7 Morocco

- 5.3.8 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 BCI Holding SA

- 6.4.3 Covestro AG

- 6.4.4 Dow

- 6.4.5 Huntsman International LLC

- 6.4.6 Kuwait Polyurethane Industries W.L.L

- 6.4.7 LANXESS

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 Perfect Rubber

- 6.4.10 Wanhua Chemical Group Co.,Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Awareness of Energy Efficiency Policy related to Buildings in the Middle Eastern Region

- 7.2 Increasing Demand for Bio-based Polyurethane

샘플 요청 목록