|

시장보고서

상품코드

1907238

리그닌 제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Lignin Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

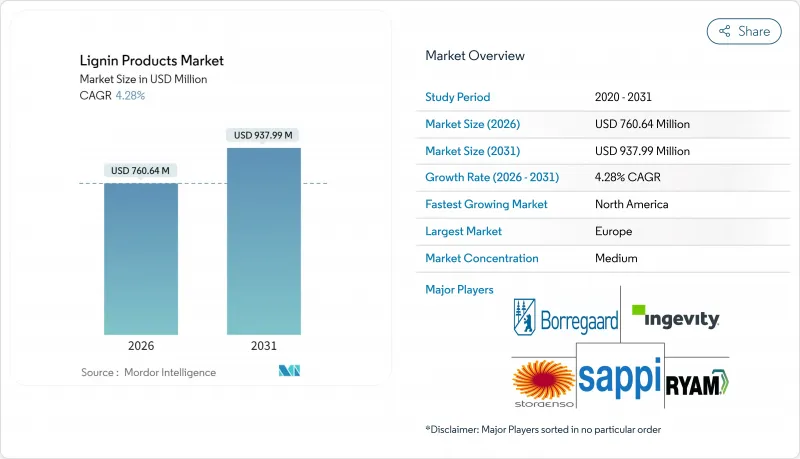

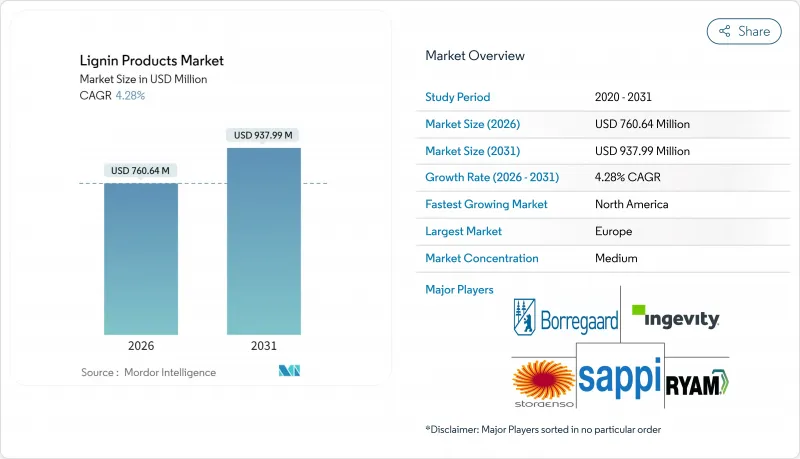

리그닌 제품 시장은 2025년 7억 2,942만 달러로 평가되었고, 2026년에는 7억 6,064만 달러로 성장할 것으로 전망되며, 2026-2031년 CAGR 4.28%로 성장을 지속하여, 2031년까지 9억 3,799만 달러에 달할 것으로 예측되고 있습니다.

이 성장은 저탄소 건설 화학에 대한 수요 증가, 성숙 경제권의 지속가능성 규제 강화, 리그닌 계 방향족 화합물의 고 부가가치 용도를 개척하는 바이오 변환 경로의 지속적인 기술 혁신에 기인합니다. 폐기물 처리에서 부가가치형 바이오리파이너리 통합으로의 전환은 특히 의약품 및 전자기기 밸류체인용 고순도 등급에서 가격 결정력을 강화하고 있습니다. 유럽은 오랜 세월에 걸쳐 펄프 공장 인프라로 선구자 우위성을 유지하는 한편, 북미는 셀룰로오스계 에탄올 의무화 정책 및 자동차 경량화 프로그램을 배경으로 가장 빠른 성장을 기록하고 있습니다. 경쟁 격도는 중간 정도를 유지하고 통합 펄프 생산자는 규모의 경제를 활용하고 소규모 특수 가공업자에 대한 마진 보호를 도모하고 있습니다.

세계의 리그닌 제품 시장 동향 및 인사이트

고성능 콘크리트 혼화제 수요 증가

아시아태평양 및 라틴아메리카의 인프라 확장에 따라 유동성을 향상시키면서 시멘트 소비량을 삭감하는 고성능 감수제 수요가 높아지고 있습니다. 리그닌계 혼화제는 물 시멘트비를 저감해, 압축 강도를 15-20% 향상시키는 것과 동시에, 시멘트 사용량을 8-12% 삭감합니다. LEED 인증 취득을 목표로 하는 건설 회사는 고층 빌딩 및 교통 프로젝트에서 매장 탄소를 줄이는 이러한 바이오 솔루션을 선호합니다. 중국과 인도의 그린 빌딩 기준은 현재 천연 혼화제를 추천하고 있으며, 상업화를 가속시키는 규제면에서의 뒷받침이 되고 있습니다. 제조업체는 고성능 콘크리트를 지정하는 대규모 도시 및 고속도로 계약에 대응하기 위해 생산 능력을 확대하고 있습니다. 스마트 시티 투자의 꾸준한 증가로 인해 중기적으로 리그닌 슈퍼 플라스틱에 대한 지속적인 수요가 예상됩니다.

동물 영양 분야에서 리그닌 기반 사료 결합제 도입

항생제 성장 촉진제를 규제하는 유럽의 법령에 의해 사료 배합업자는 리그노술폰산염 결합제로의 이행을 진행하고 있습니다. 연구에 의하면, 당밀계 시스템에 비해 펠릿 내구성이 25-30% 향상되어 사료 분진의 저감과 수송 손실의 삭감으로 이어집니다. 특정 리그닌 분획은 프리바이오틱 활성을 나타내며 반추동물의 장내 미생물총을 개선하기 때문에 사료 제조업체는 프리미엄 가격으로 판매가 가능해집니다. 덴마크 및 네덜란드 제조업체는 지역 펄프 공장에서 현지 조달한 리그닌 유도체로 물류 비용을 12-15% 절감했다고 보고했습니다. 북미 생산자는 대규모 통합 기업이 항생제를 사용하지 않는 밸류체인을 추구하는 동안 비슷한 전략을 채택하고 있습니다. 아시아태평양의 축산 사업자가 고부가가치 단백질로 이행하여 배합 사료의 효율화를 요구하는 가운데 장기적인 전망은 계속 견조합니다.

추출 프로세스로 인한 품질 편차

크래프트리그닌, 설파이트리그닌, 소다리그닌 간의 황 함량과 분자량의 차이는 일관된 사양이 필요한 사용자에게 조달을 복잡하게 합니다. 설파이트계는 황 함유량이 20-30% 높고, 수지 경화 속도에 영향을 주기 때문에 전용의 가공 프로토콜이 요구됩니다. 하류 기업은 병행 재고 및 이중 인증 프로그램을 유지하고 있으며 공급망 지출을 8-12% 증가시키고 있습니다. 소규모 공장에서는 각 배치를 인증하는 분석 랩을 보유하고 있는 경우가 드물고, 저마진의 판로에 대한 시장 액세스가 제한되어 있습니다. 공통 테스트 기준이 수립되고 클라우드 기반 추적성 플랫폼이 성숙될 때까지 단기적으로 불확실성이 남아 있습니다. 따라서 품질의 조화는 특수 분야에서 광범위한 채용에 매우 중요합니다.

부문 분석

황산염 펄프 제조와 관련된 리그닌 제품 시장 규모는 풍부한 공급량과 분산제로서의 확립된 성능을 배경으로 2025년에 세계 가치의 76.62%를 차지해 전체의 대부분을 차지했습니다. 셀룰로오스계 에탄올 플랜트는 규모가 작은 것 고이익률 공급원이며, 4.95%의 연평균 복합 성장률(CAGR)에 의해 2031년까지에서 가장 성장이 현저한 공급원 카테고리가 되고 있습니다. 미국 재생 가능 연료 기준(RFS) 및 EU 재생에너지 지침 II(RED-II)에 근거한 생산 인센티브는 바이오리파이너리가 리그닌 분리 유닛을 통합하는 것을 촉진하여 에탄올 매출의 12-15%에 해당하는 수익을 추가하고 있습니다. 주로 유럽과 중국에 거점을 두고 있는 황산염 펄프 사업자는 회수율의 최적화와 콘크리트 및 사료용 특주 등급의 투입에 의해 지위를 지키고 있습니다. 소다 펄프는 인도와 동남아시아에서 틈새 시장의 중요성을 유지하고 농업 잔류물을 저회분 리그닌으로 가공하여 지역의 섬유화학에 공급하고 있습니다.

셀룰로오스계 에탄올 유래 리그닌은 통상 크래프트법 원료보다 회분이 낮고 분자량 분포가 좁기 때문에 특수 폴리머 용도로 프리미엄이 붙습니다. 자동차 복합재료의 파일럿 사용자는 연속 섬유 방사를 돕는 예측 가능한 레올로지 특성을 높이 평가합니다. 에탄올 생산자가 생산 능력을 확대함에 따라 이 고품질 리그닌 공급이 증가하고 바이오연료와 특수화학 체인의 통합이 긴밀해지고 있습니다. 아황산염 유래의 생산량이 다른 공급원을 압도하고 있는 것, 경쟁의 발휘는 단순한 생산량이 아니라 톤당 가치에 달려 있어, 특히 탄소 수익이 수익성에 영향을 주는 상황하에서는 더욱더입니다.

지역별 분석

유럽은 2025년 세계 가치의 33.55%를 차지했습니다. 통합된 임업 및 엄격한 기후 정책이 리그닌의 조기 가치화를 촉진하기 때문입니다. 핀란드 및 스웨덴의 펄프 공장에서는 새로운 수익원으로 추출 라인의 개수가 진행되고 있으며, 독일의 콘크리트 자동차 산업에서는 안정적인 수요가 계속되고 있습니다. REACH 화학물질 규제는 배합업체가 바이오 유래 원료로의 전환을 촉진하고 수요 전망을 개선하고 있습니다. 유럽연구조성 프로그램 '호라이즌 및 유럽'은 바닐린 및 탄소섬유 분야에서의 파일럿 전개를 가속시켜, 동지역의 혁신 주도권을 확고하게 하고 있습니다.

북미는 2031년까지 5.08%라는 가장 빠른 CAGR로 추이할 전망입니다. 연방 셀룰로오스계 연료 의무화 정책이 리그닌 공급을 확대하고 자동차 경량화에 대한 노력이 지속 가능한 복합재료 수요를 높이기 위해서입니다. 미국의 콘크리트 혼화제용 리그닌 제품 시장 규모는 교량과 교통의 근대화를 추진하는 초당파 인프라법의 뒷받침에 의해 확대됩니다. 캐나다의 임업 기업은 풍부한 북방림 자원을 활용하여 펄프를 넘은 특수 리그닌의 다각화를 진행하고 있습니다. 이것은 저 배출 물질을 우월한 국가의 탄소 가격 제도에 의해 지원됩니다. 멕시코의 건설 붐도 혼화제 수입의 여지를 만들어 대륙 전체 수요를 보완하는 형태가 되고 있습니다.

아시아태평양은 도입 단계가 비교적 빠른 것, 큰 성장 여지를 가지고 있습니다. 중국의 급속한 도시화가 콘크리트 소비를 밀어 올리고, 국가 기준이 리그닌 슈퍼 플라스틱를 인지하기 시작하고 있습니다. 인도에서는 농업 잔사용 소다 펄프 제조를 확대하여 현지 사료나 염료 분산제용으로 비용 경쟁력이 있는 리그닌을 생산하고 있습니다. 일본에서는 전자수지에 리그닌의 방향족 골격을 활용하고, 한국에서는 리그닌계 화학제품을 그린 조달 리스트에 통합하고 있습니다. ASEAN 국가의 인프라 정비 계획과 육류 생산의 확대가 복합적인 수요를 촉진하고 있지만, 국경을 넘은 거래에는 기준의 조화가 필수적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고성능 콘크리트 혼화제 수요 증가

- 동물 영양 분야에 있어서 리그닌계 사료 결합제의 도입 상황

- 펄프 공장 제품별 가치화에 의한 순환형 수익 창출

- 획기적인 리그닌에서 바닐린으로의 바이오 변환 경로

- 자동차 업계에서 리그닌 유래 바이오 탄소섬유 추진

- 시장 성장 억제요인

- 추출 공정 간의 품질 편차

- 당 유래 바이오 방향족 화합물의 경쟁

- 국제적인 리그닌 제품 기준 부족

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 소스별

- 아황산염 펄프

- 셀룰로오스계 에탄올

- 크래프트 펄프 제조

- 소다 펄프법

- 제품 유형별

- 리그노술폰산염

- 크래프트 리그닌

- 고순도 리그닌

- 소다 리그닌

- 기타 제품 유형

- 용도별

- 분산제

- 콘크리트 첨가제

- 사료

- 수지

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 및 랭킹 분석

- 기업 프로파일

- Borregaard AS

- Burgo Group SpA

- Domsjo Fabriker AB

- Ingevity

- Lignin Industries AB

- MetGen

- Metsa Group

- NIPPON PAPER INDUSTRIES CO., LTD.

- RYAM

- Sappi Ltd

- Stora Enso

- Suzano S/A

- UPM Biochemicals

- Valmet

제7장 시장 기회 및 장래 전망

AJY 26.01.26The Lignin Products market is expected to grow from USD 729.42 million in 2025 to USD 760.64 million in 2026 and is forecast to reach USD 937.99 million by 2031 at 4.28% CAGR over 2026-2031.

Performance gains stem from rising demand for low-carbon construction chemicals, stricter sustainability regulations across mature economies, and continuing breakthroughs in bioconversion pathways that open high-value outlets for lignin-based aromatics. The shift from waste-stream disposal toward value-added biorefinery integration reinforces pricing power, especially for high-purity grades supplied to the pharmaceutical and electronics value chains. Europe preserves first-mover advantage thanks to long-standing pulp-mill infrastructure, while North America records the fastest growth on the back of cellulosic ethanol mandates and automotive lightweighting programs. Competitive intensity remains moderate, with integrated pulp producers leveraging scale to protect margins against smaller specialty processors

Global Lignin Products Market Trends and Insights

Rising Demand for High-Performance Concrete Admixtures

Infrastructure expansion across Asia-Pacific and Latin America raises the need for superplasticizers that improve flow while lowering cement consumption. Lignin-based admixtures reduce water-cement ratios, boosting compressive strength by 15-20% and cutting cement use by 8-12%. Construction firms pursuing LEED certification favor these bio-based solutions because they lower embodied carbon in high-rise and transportation projects. Green-building codes in China and India now endorse natural admixtures, providing a regulatory pull that accelerates commercialization. Producers scale up capacity to keep pace with large metro and highway contracts that specify performance concrete. Steady gains in smart-city investments anticipate durable demand for lignin superplasticizers through the medium term.

Uptake of Lignin-Based Feed Binders in Animal Nutrition

European regulations that restrict antibiotic growth promoters have moved feed formulators toward lignosulfonate binders. Studies show 25-30% better pellet durability versus molasses systems, translating into lower feed dust and reduced transport losses. Specific lignin fractions exhibit prebiotic activity that enhances ruminant gut microbiota, allowing feed companies to price at a premium. Danish and Dutch manufacturers report 12-15% logistics cost savings after sourcing local lignin derivatives from regional pulp mills. North American producers adopt similar strategies as large integrators target antibiotic-free supply chains. The long-term outlook remains strong as Asia-Pacific livestock operators shift toward higher-value protein and require efficiency gains in compound feed.

Quality Variability Across Extraction Processes

Differences in sulfur content and molecular weight between kraft, sulfite, and soda lignin complicate procurement for users that require consistent specifications. Sulfite variants carry 20-30% higher sulfur, impacting resin cure kinetics and demanding tailored processing protocols. Downstream firms maintain parallel inventories and dual qualification programs, inflating supply-chain spending by 8-12%. Smaller mills rarely possess analytical labs to certify each batch, restricting market access to low-margin outlets. Near-term uncertainty remains until shared testing standards emerge and cloud-based traceability platforms mature. Quality harmonization is therefore pivotal for broader adoption in specialty segments.

Other drivers and restraints analyzed in the detailed report include:

- Valorisation of Pulp-Mill Side-Streams for Circular Revenue

- Breakthrough Lignin-to-Vanillin Bioconversion Routes

- Competition from Sugar-Derived Bio-Aromatics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The lignin products market size linked to sulfite pulping totaled the bulk of global value, securing 76.62% in 2025 on the back of abundant volumes and well-known performance in dispersants. Cellulosic ethanol plants offer much smaller but higher-margin flows, and their 4.95% CAGR makes them the most dynamic source category to 2031. Production incentives under the U.S. Renewable Fuel Standard and EU RED-II encourage biorefineries to integrate lignin separation units, adding revenue equal to 12-15% of ethanol sales. Sulfite operators, chiefly in Europe and China, defend position by optimizing recovery yields and launching tailor-made grades for concrete and feed. Soda pulping keeps niche importance in India and Southeast Asia, processing agricultural residues into low-ash lignin for regional textile chemicals.

Cellulosic ethanol lignin typically displays lower ash and narrower molecular-weight distribution than kraft material, granting it a premium in specialty polymers. Pilot users in automotive composites value the predictable rheology that aids continuous fiber spinning. As ethanol producers scale capacity, supply of this high-quality lignin grows, tightening integration between biofuel and specialty chemical chains. Although sulfite volumes dwarf other sources, competitive dynamics hinge on value per ton rather than tonnage alone, especially as carbon revenue streams influence profitability.

The Lignin Products Market Report is Segmented by Source (Sulfite Pulping, Cellulosic Ethanol, Kraft Pulping, and Soda Pulping), Product Type (Lignosulfonate, Kraft Lignin, and Other Product Types), Application (Dispersant, Concrete Additive, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe held 33.55% of global value in 2025 because integrated forest industries and strict climate policies foster early lignin valorization. Pulp mills in Finland and Sweden retrofit extraction lines to capture new revenue, while German concrete and automotive sectors absorb steady volumes. REACH chemicals regulation nudges formulators toward bio-derived inputs, improving demand visibility. Horizon Europe research grants accelerate pilot deployments in vanillin and carbon-fibre, solidifying the region's innovation leadership.

North America posts the fastest 5.08% CAGR through 2031 as federal cellulosic fuel mandates widen lignin supply and automotive lightweighting efforts raise the bar on sustainable composites. The lignin products market size for concrete admixtures climbs in the United States on the back of the Bipartisan Infrastructure Law, which modernizes bridges and transit. Canadian forestry companies leverage abundant boreal resources to diversify beyond pulp into specialty lignin, supported by provincial carbon-pricing mechanisms that favor low-emission materials. Mexico's construction boom also creates room for admixture imports, rounding out continental demand.

Asia-Pacific stands at an earlier adoption curve yet offers vast upside. China's rapid urbanization elevates concrete consumption, and state standards begin to recognize lignin superplasticizers. India scales soda pulping for agri-residue, producing cost-competitive lignin for local feed and dye dispersants. Japan exploits lignin's aromatic backbone in electronics resins, while South Korea includes lignin-based chemicals in green-procurement lists. Ongoing ASEAN infrastructure initiatives and growing meat production foster multipronged demand, though standards harmonization will be critical for cross-border trade.

- Borregaard AS

- Burgo Group S.p.A.

- Domsjo Fabriker AB

- Ingevity

- Lignin Industries AB

- MetGen

- Metsa Group

- NIPPON PAPER INDUSTRIES CO., LTD.

- RYAM

- Sappi Ltd

- Stora Enso

- Suzano S/A

- UPM Biochemicals

- Valmet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High-Performance Concrete Admixtures

- 4.2.2 Uptake of Lignin-Based Feed Binders in Animal Nutrition

- 4.2.3 Valorisation of Pulp-Mill Side-Streams for Circular Revenue

- 4.2.4 Breakthrough Lignin-To-Vanillin Bioconversion Routes

- 4.2.5 Automotive Push for Lignin-Derived Bio-Carbon Fibre

- 4.3 Market Restraints

- 4.3.1 Quality Variability Across Extraction Processes

- 4.3.2 Competition from Sugar-Derived Bio-Aromatics

- 4.3.3 Lack of International Lignin Product Standards

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source

- 5.1.1 Sulfite Pulping

- 5.1.2 Cellulosic Ethanol

- 5.1.3 Kraft Pulping

- 5.1.4 Soda Pulping

- 5.2 By Product Type

- 5.2.1 Lignosulfonate

- 5.2.2 Kraft Lignin

- 5.2.3 High-Purity Lignin

- 5.2.4 Soda Lignin

- 5.2.5 Other Product Types

- 5.3 By Application

- 5.3.1 Dispersant

- 5.3.2 Concrete Additive

- 5.3.3 Animal Feed

- 5.3.4 Resins

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Borregaard AS

- 6.4.2 Burgo Group S.p.A.

- 6.4.3 Domsjo Fabriker AB

- 6.4.4 Ingevity

- 6.4.5 Lignin Industries AB

- 6.4.6 MetGen

- 6.4.7 Metsa Group

- 6.4.8 NIPPON PAPER INDUSTRIES CO., LTD.

- 6.4.9 RYAM

- 6.4.10 Sappi Ltd

- 6.4.11 Stora Enso

- 6.4.12 Suzano S/A

- 6.4.13 UPM Biochemicals

- 6.4.14 Valmet

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment