|

시장보고서

상품코드

1640427

니트로벤젠 - 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Nitrobenzene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

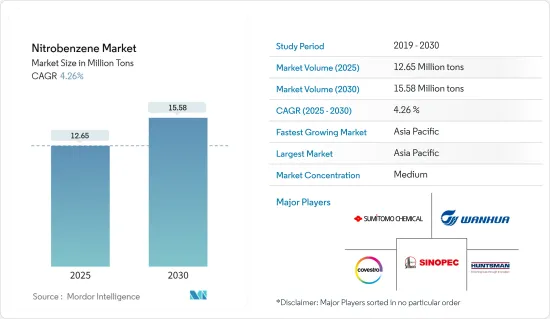

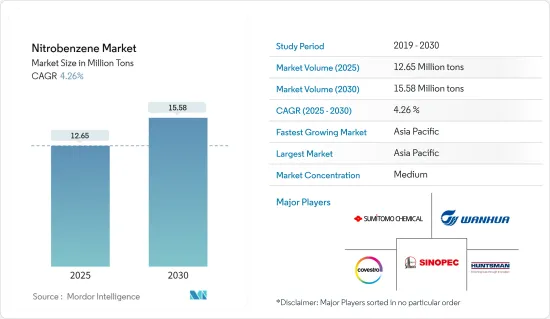

니트로벤젠 시장 규모는 2025년에 1,265만 톤으로 추정됩니다. 예측기간(2025-2030년)의 CAGR은 4.26%로, 2030년에는 1,558만 톤에 달할 것으로 예상됩니다.

니트로벤젠 시장은 2020년에 COVID-19의 악영향을 받았습니다. 팬데믹의 시나리오를 고려하면, 다양한 니트로벤젠 유도체 기반 제품에 대한 수요 감소는 시장 수요에 부정적인 영향을 미쳤습니다. 그러나, 니트로벤젠 유도체의 아닐린으로부터 유도되는 파라세타몰 수요가 증가하여, 니트로벤젠 시장 수요를 자극했습니다. 그럼에도 불구하고, 시장은 팬데믹 후에 페이스를 올리기 시작하고 앞으로도 같은 궤도를 따라갈 것으로 예상됩니다.

주요 하이라이트

- 중기적으로는 아닐린 생산을 위한 니트로벤젠 수요 증가, 생산에 사용되는 원료의 용이한 입수, 아시아태평양의 건설 활동 활성화 등 큰 수요에 기여하는 요인이 시장 성장을 견인할 것으로 예상됩니다.

- 반대로 바이오 화학물질에 대한 수요 증가는 시장 성장을 방해할 가능성이 높습니다.

- 세계 건설 산업의 다양한 투자는 조사한 시장에 기회가 될 가능성이 높습니다.

- 아시아태평양이 세계 시장을 독점하고 중국, 인도 등 국가에서 소비가 가장 많습니다.

니트로벤젠 시장 동향

아닐린 생산 수요 증가

- 아닐린 제조 용도가 니트로벤젠 용도 중에서 가장 큰 점유율을 차지하고 있으며, 그 점유율은 90%를 초과하고 있습니다. 니트로벤젠의 촉매 수소 첨가가 주요 생산입니다.

- 인도는 최대의 아닐린 제조·수출국의 하나입니다. 인도 화학비료성에 따르면 2022-2023년도의 국내 아닐린 생산량은 3만 9,660톤으로 2021-2022년도에 비해 약 18.28% 증가했습니다.

- 아닐린 유래의 메틸렌디페닐디이소시아네이트(MDI)는 건축 및 자동차 부문을 포함한 다양한 최종 이용 산업에서 중합체의 중요한 전구체입니다.

- 국제자동차건설기구(OICA)에 따르면 2022년 세계 자동차 생산량은 약 6% 증가하여 85.01대가 되었습니다. 이로 인해 스티어링 부품, 에어백 커버, 방수 바닥재, 범퍼 등 다양한 자동차 부품 제조에 사용되는 MDI 기반 엘라스토머 및 폴리우레탄과 같은 폴리머 수요가 줄어듭니다.

- 또한 MDI는 폴리우레탄 폼의 제조에도 사용되며 주로 건축물의 단열재로 사용됩니다.

- 토목학회(Institution of Civil Engineers)의 추정에 의하면, 2025년까지 세계 건설 산업의 성장의 60% 가까이를 중국, 인도, 미국의 상위 3개국이 차지하게 됩니다.

- 미국 인구조사국에 따르면 2023년 미국의 건설업 연간 총액은 1조 9,787억 달러로 2022년에 비해 약 7.03% 증가했습니다.

- 의약품 부문은 특히 미국, 인도, 독일에서 가장 높은 성장을 이루는 세계 시장 중 하나입니다. 아세트 아미노펜(파라세타몰)은 아닐린에서 생산되는 인기 진통제입니다. 세계에서 가장 인기있는 제네릭 의약품은 파라세타몰입니다. 모든 연령대를 위해 정제, 정제, 시럽으로 시판됩니다.

- 중국, 인도, 미국, 독일은 세계 최대의 제약 산업입니다. 중국 제조업체는 세계에서 사용되는 약의 약 40%를 차지하는 것으로 추정됩니다. 게다가 중국과 인도는 미국에 수입되는 약의 75%에서 80%를 조달하고 있습니다. 비용 절감과 덜 엄격한 환경 규제에 대한 요구는 중국과 인도의 제약 산업을 견인하고 있습니다.

- IQVIA에 따르면 2023년 세계 의약품 시장 규모는 1조 6,070억 달러로 약 8.34% 증가했습니다.

- 그러므로 위의 모든 요인은 향후 몇 년 동안 시장 성장에 큰 영향을 줄 것으로 예상됩니다.

시장을 독점하는 아시아태평양

- 아시아태평양은 소비 및 생산 측면에서 니트로벤젠의 최대 시장으로, 조사한 시장에서도 예측 기간 동안 가장 높은 성장이 예상됩니다. 이 지역의 인프라와 인건비가 불충분하기 때문에 다양한 외자계 기업이 이 지역에 제조 시설을 이전하고 있습니다. 니트로벤젠의 생산과 소비는 또한 주요 아닐린과 메틸렌디페닐디이소시아네이트(MDI) 제조 기업이 생산 능력을 확대함으로써 큰 영향을 받고 있습니다.

- 접착제, 실란트, 엘라스토머, 폴리우레탄 등 다양한 MDI 기반 제품에 대한 요구가 커지고 있기 때문에 건설 부문은 니트로벤젠의 가장 중요한 최종 사용자 시장이 되었습니다. 또한 목재와 가구의 바인더로도 사용됩니다. 이러한 용도로 건설 산업은 세계에서 생산되는 니트로 벤젠의 48% 이상을 소비하고 있으며, 대부분은 아시아태평양에서 발생하고 있습니다.

- 중국, 인도, 베트남과 같은 아시아태평양 국가들은 건설 활동에서 강력한 성장을 기록하고 있으며 예측 기간 동안이 지역에서 아닐린 기반 유도체의 소비를 촉진할 것으로 예상됩니다.

- 미국 국제무역국에 따르면 중국은 세계 최대의 건설시장으로 2030년까지 연평균 8.6%의 성장이 전망되고 있습니다. 국가개발개혁위원회(NDRC)에 따르면 중국은 2025년까지 중요한 건설 프로젝트에 1조 4,300억 달러를 투자하고 있습니다.

- 중국국가통계국에 따르면 2023년 중국 건설산업의 총 생산액은 1.99% 증가했으며 71조 2,847억 2,000만 위안(10조 867억 8,000만 달러)이었습니다.

- 주택·도시 농촌개발성의 예측에 따르면 중국의 건설 부문은 2025년에도 GDP의 6%를 유지할 것으로 예측되고 있습니다. 이러한 예측을 바탕으로 중국 정부는 2022년 1월 품질과 주도적 개발을 통해 건설산업의 지속가능성을 향상시키는 5개년 계획을 발표했습니다.

- 또한 인도에서는 주택 부문이 성장하고 있으며 정부의 지원과 노력이 수요를 더욱 밀어 올리고 있습니다. 2022년부터 2023년까지의 예산에서 주택도시개발부(MoHUA)는 주택건설과 정지중의 프로젝트를 완료하기 위한 자금 만들기에 약 98억 5,000만 달러를 할당했습니다.

- 그러므로 위의 모든 요인은 앞으로 수년간 시장 성장에 큰 영향을 미칠 것으로 예상됩니다.

니트로벤젠 산업 개요

니트로벤젠 시장은 부분적으로 통합됩니다. 주요 진출기업으로는 Covestro AG, Huntsman International LLC, Sumitomo Chemical, Wanhua, China Petrochemical Corporation(Sinopec) 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 아닐린 수요 증가

- 원료 입수의 용이성

- 아시아태평양의 건설 활동 성장

- 성장 억제요인

- 바이오 베이스 화학제품 수요 증가

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 규제 시책 분석

제5장 시장 세분화(규모별)

- 용도

- 아닐린 제조

- 염료 및 안료

- 살충제

- 의약 중간체

- 기타 용도(용제, 화약 등)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 노르딕

- 터키

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 인수합병, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Aarti Industries Ltd.

- Aromsyn Co.,Ltd.

- Bann Quimica Ltda.

- Chemieorganics Chemical India Pvt.Ltd.

- China Petrochemical Corporation(Sinopec)

- Covestro AG

- Huntsman International LLC.

- Sadhana Nitro Chem Ltd.

- SP Chemicals Pte Ltd.

- Sumitomo Chemical Co., Ltd.

- Wanhua

제7장 시장 기회와 앞으로의 동향

- 건설 산업에 대한 다양한 투자

- 기타 기회

The Nitrobenzene Market size is estimated at 12.65 million tons in 2025, and is expected to reach 15.58 million tons by 2030, at a CAGR of 4.26% during the forecast period (2025-2030).

The nitrobenzene market was negatively impacted by COVID-19 in 2020. Considering the pandemic scenario, the decrease in demand for various nitrobenzene derivative-based products negatively impacted the market demand. However, the demand for paracetamol derived from the nitrobenzene derivative aniline increased, stimulating the demand for the nitrobenzene market. Nevertheless, the market started to gain pace in the post-pandemic era and was expected to continue the same trajectory.

Key Highlights

- Over the medium term, factors such as the increasing demand for nitrobenzene to produce aniline, the easy availability of raw materials used for production, and the growing construction activities in the Asia-Pacific region, which are contributing to significant demand, are expected to drive the market's growth.

- On the contrary, the growing demand for bio-based chemicals will likely hinder the market's growth.

- Various investments in the construction industry across the globe are likely to act as opportunities for the market studied.

- Asia-Pacific dominated the global market, with the largest consumption from countries such as China, India, etc.

Nitrobenzene Market Trends

Increasing Demand for Aniline Production

- Aniline production applications account for the largest share of nitrobenzene applications, with a share of more than 90%. The catalytic hydrogenation of nitrobenzene majorly produces it.

- India is one of the largest manufacturers and exporters of aniline. According to the Ministry of Chemicals and Fertilizers of India, In FY 2022-2023, aniline production in the country was valued at 39.66 thousand metric tons, which is an increase of about 18.28% as compared to FY 2021-2022.

- The aniline-derived methylene diphenyl diisocyanate (MDI) is a crucial precursor for polymers in various end-use industries, including the building and automotive sectors.

- According to the Organization Internationale des Constructeurs d'Automobiles (OICA), global automotive production in 2022 increased by about 6% and was valued at 85.01 units. This will result in a decline in the demand for MDI-based elastomers and polymers like polyurethane, which are used to make various automotive parts, including steering components, airbag covers, waterproof floor materials, bumpers, and others.

- Furthermore, MDI is used for the production of polyurethane foams, mainly used in various building insulation applications, and acts as one of the significant components in construction, both in their flexible and rigid form.

- As per the estimates of the Institution of Civil Engineers, the top three countries, i.e., China, India, and the United States, will account for almost 60% of all growth in the global construction industry by 2025.

- According to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which is an increase of about 7.03% compared to that of 2022.

- The pharmaceutical sector is one of the global markets with the highest growth, particularly in the United States, India, and Germany. Acetaminophen, or paracetamol, is a popular painkiller produced from aniline. The most popular generic medicine worldwide is paracetamol. For people of all ages, it is commercially offered in tablet, pill, and syrup formulations.

- China, India, the United States, and Germany are the largest pharmaceutical industries in the world. Chinese manufacturers are estimated to make up around 40% of all the APIs used worldwide. Additionally, China and India source 75% to 80% of the APIs imported to the United States. The desire for cost savings and less stringent environmental regulations has driven the pharmaceutical industries in China and India.

- According to IQVIA, the global pharmaceutical market in 2023 was valued at USD 1,607 billion, which is an increase of about 8.34%.

- Therefore, all the abovementioned factors are expected to impact the market's growth significantly in the coming years.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is the largest market for nitrobenzene in terms of consumption and production and is also expected to have the highest growth during the forecast period in the market studied. Various foreign corporations have relocated their manufacturing facilities in the area due to the region's inadequate infrastructure and labor expenses. Production and consumption of nitrobenzene have also been significantly influenced by major aniline and methylene diphenyl diisocyanate (MDI) manufacturing companies expanding their production capacities.

- Due to the increased need for various MDI-based products such as adhesives, sealants, elastomers, and polyurethanes, the construction sector is the most important end-user market for nitrobenzene. Moreover, it is used as a binding agent for wood and furniture. Due to these uses, the construction industry consumes over 48% of the nitrobenzene produced globally, with a significant portion of this consumption occurring in the Asia-Pacific area.

- Asia-Pacific countries, such as China, India, and Vietnam, are registering strong growth in construction activities, which will drive the consumption of these aniline-based derivatives in the region over the forecast period.

- As per the U.S. International Trade Administration, China is the largest market for construction globally and is expected to grow at an annual average rate of 8.6% till 2030. According to the National Development and Reform Commission (NDRC), China is investing USD 1.43 trillion in significant construction projects till 2025.

- According to the National Bureau of Statistics of China, the gross output value of the construction industry in China in 2023 increased by 1.99% and was CNY 71,284.72 billion (USD 10,086.78 billion).

- According to the Ministry of Housing and Urban Rural Development's forecast, China's construction sector is projected to remain at 6 % of its GDP in 2025. In view of these forecasts, in January 202, the Chinese government announced a five-year plan to improve sustainability in the construction industry through quality and driven development.

- In addition, the residential sector in India is growing, and government support and initiatives are further boosting demand. In the budget of 2022-2023, the Ministry of Housing and Urban Development (MoHUA) allocated about USD 9.85 billion to construct houses and create funds to complete the halted projects.

- Therefore, all the abovementioned factors are expected to impact the growth of the market in the coming years significantly.

Nitrobenzene Industry Overview

The Nitrobenzene Market is partially consolidated in nature. Some major players include (not in any particular order) Covestro AG, Huntsman International LLC., Sumitomo Chemical Co., Ltd., Wanhua, and China Petrochemical Corporation (Sinopec), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Aniline

- 4.1.2 Easy Availability of Raw Materials

- 4.1.3 Growing Construction Activities in the Asia-Pacific Region

- 4.2 Restraints

- 4.2.1 Growing Demand for Bio-based Chemicals

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Aniline Production

- 5.1.2 Dyes and Pigments

- 5.1.3 Pesticides

- 5.1.4 Intermediate in Pharmaceuticals

- 5.1.5 Other Applications (including Solvent, Explosives, etc.)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Malaysia

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 NORDIC

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Nigeria

- 5.2.5.4 Qatar

- 5.2.5.5 Egypt

- 5.2.5.6 United Arab Emirates

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aarti Industries Ltd.

- 6.4.2 Aromsyn Co.,Ltd.

- 6.4.3 Bann Quimica Ltda.

- 6.4.4 Chemieorganics Chemical India Pvt.Ltd.

- 6.4.5 China Petrochemical Corporation (Sinopec)

- 6.4.6 Covestro AG

- 6.4.7 Huntsman International LLC.

- 6.4.8 Sadhana Nitro Chem Ltd.

- 6.4.9 SP Chemicals Pte Ltd.

- 6.4.10 Sumitomo Chemical Co., Ltd.

- 6.4.11 Wanhua

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Various Investments in Construction Industry

- 7.2 Other Opportunities