|

시장보고서

상품코드

1640499

아시아태평양의 유전용 화학제품 - 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Asia-Pacific Oilfield Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

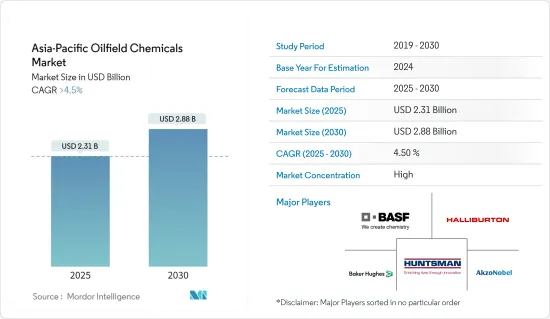

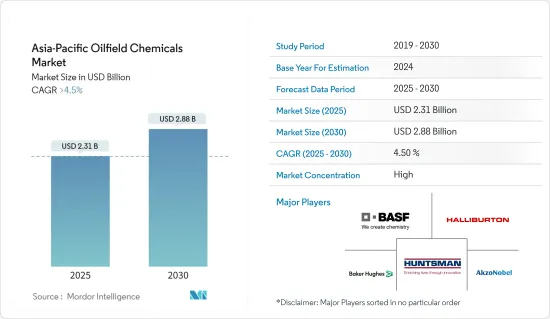

아시아태평양의 유전용 화학제품 시장 규모는 2025년에는 23억 1,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR은 4.5%를 초과하여, 2030년에는 28억 8,000만 달러에 달할 것으로 예측됩니다.

COVID-19의 대유행은 석유 및 가스 산업에 악영향을 미치고, 아시아태평양의 유전용 화학제품 시장에도 영향을 끼쳤습니다. 그러나 COVID-19 이후에는 석유 및 가스산업의 수요가 증가하고 있어 이 지역의 유전용 화학제품 시장은 부활할 것으로 예상됩니다.

주요 하이라이트

- 시장 성장을 가속하는 주요 요인 중 하나는 아시아태평양의 가스 탐사 및 생산 점유율 확대입니다. 수송산업의 석유계 연료 수요 증가가 예측기간 중 시장 수요를 견인할 것으로 보입니다.

- 바이오연료 산업의 상승은 시장 성장을 방해할 가능성이 높습니다. 지속가능성과 환경문제에 대한 관심이 증가함에 따라 유전 화학산업은 규제 압력과 투자자들의 관심 저하에도 직면할 수 있습니다.

- 셰일 오일 가스와 같은 심해 자원과 비재래형 자원에 대한 관심 증가는 시추 오일, 윤활유 및 완성 오일의 새로운 시장을 개척합니다. 이러한 까다로운 환경에 대응하는 고성능, 친환경 화학제품의 개발은 큰 비즈니스 기회입니다.

- 아시아태평양 전체에서는 중국이 시장을 독점하고 있으며, 이 지역에서 가장 많은 유전용 화학제품 소비를 보이고 있습니다.

아시아태평양 유전 화학제품 시장 동향

부식 및 스케일 억제제 부문이 시장을 독점

- 부식 방지제는 유정 금속 파이프의 부식을 억제하는 데 사용됩니다. 탄소강 파이프나 용기는 부식 억제 처치를 필요로 합니다. 억제제의 장점은 공정이 계속되는 경우에도 대부분의 경우 사용할 수 있다는 점입니다.

- 부식은 산소가 금속 부분과 반응하여 산화물을 형성함으로써 발생합니다. 부식 방지제는 노출된 부품 위에 얇은 장벽 층을 형성하여 작용합니다. 유전에서는 여러 유형의 부식 방지제가 사용됩니다.

- DEHA-디에틸하이드록실아민, 폴리아민, 모르폴린, 시클로헥실아민, 이산화탄소 부식방지제 등이 존재하며 필름용 아민 혼합물은 복수 라인 부식 방지제 제조에 사용됩니다. 이 혼합물은 고증기압 및 저증기압 액체 모두 이용가능하기 때문에 모든 공정을 보호할 수 있습니다.

- 스케일은 온도가 상승함에 따라 불용성이 되는 가용성 고체가 침전되어 유전 설비의 표면에 형성되는 잔류물입니다. 스케일은 금속 부식을 일으키고 장비의 기능과 유지 보수에 영향을 미칩니다. 침전은 부식 속도를 높이고 생산 손실을 유발하며 흐름을 제한합니다.

- 그러므로 유전 설비를 보호하고 효율을 유지하기 위해서는 스케일 방지제 역할을 하는 과학적으로 설계된 화학물질을 첨가하여 올바른 상태를 유지해야 합니다. 유기인산염, 무기인산염, 폴리머(폴리아크릴산염), 포스폰산염, 유기킬레이트제인 에틸렌디아민테트라아세트산(EDTA) 등의 화학제품이 스케일 방지제의 일부입니다. 부식 방지제는 유정 금속 파이프의 부식을 억제하는 데 사용됩니다. 탄소강 파이프나 용기는 부식 억제 처치를 필요로 합니다.

- Rystad에 따르면, 해상 프로젝트는 그린 필드 투자 회복을 촉진하고 석유 및 가스 산업에서 해저 인프라와 시추 서비스에 대한 수요를 상승시킬 것으로 발표했습니다.

- 예를 들어, 페트로나스의 카사와리는 말레이시아 최초의 탄소 회수 및 저류(CCS) 투자 승인을 발표하고, 이어 태국의 PTT Exploration and Productions(PTTEP)의 Lang Lebah가 말레이시아에서 2023년 FID를 목표로 하고 있습니다.

- 에너지산업협의회에 따르면 쉘은 최근 괌스토 카캅 게론 자그스 이스트(GKGJE) 심해 프로젝트(2024년 가동 예정인 해저 타이백 개발)에 대한 투자를 승인했습니다.

- S&P Global Inc.에 따르면 뉴질랜드의 Refining NZ는 2022년 전반에 마스덴 포인트 정유소를 수입 터미널로 전환할 수 있도록 10월 중 고객과의 터미널 서비스 계약을 정리할 예정이라고 합니다.

- S&P Global Inc.에 따르면 호주 Viva Energy는 연방 정부의 연료 확보 패키지 발표를 환영하며, 그 일환으로 2027년 6월까지 질롱에서의 정제 조업을 유지하고 3년간의 옵션으로 2030년 6월까지 연장할 것을 6년간 약속했습니다.

- 태국의 시라차 정유소에서는 40억 달러의 청정 연료 프로젝트가 진행되고 있습니다. 이 업그레이드는 2023년에 완료될 예정이며, 정유소의 생산 능력을 27만 5,000b/d에서 40만b/d로 증강하여 보다 깨끗한 제품의 생산성을 높일 예정입니다.

- 또한 아시아태평양의 유지 보수 신규 계약은 예측 기간 동안 부식 및 스케일 방지제에 대한 투자 증가를 보여줍니다.

시장을 독점하는 중국

- 석유 및 가스 산업은 중국 경제의 주요 지표 중 하나입니다. 석유 및 가스 산업은 고온 환경하의 조업을 포함하고 있습니다.

- 유전 화학제품은 시추, 생산, 주입 및 회수 작업 향상에 사용됩니다. 셰일층으로부터 석유 및 가스 매장량을 개발하는데는 수압파쇄 등의 작업이 필요한데 이 때 유전용 화학제품이 사용되고 있습니다. 중국은 셰일 가스 탐사 능력과 시추 기술에서 많은 이정표를 달성했고 따라서 세계 최대 셰일 가스 공급국이 되었습니다.

- BP Statistical Review 2023에 의하면 2022년 중국 전체의 석유 생산량은 2억 470만 톤에 이르렀으며 2021년 생산량 1억 9,890만 톤에 비해 2.9%의 성장률이었습니다.

- 마찬가지로 중국의 전체 석유 소비량도 지난 10년간 증가하는 경향에 있습니다. 예를 들어, 2022년 중국의 석유 소비량(1,000 배럴/일)은 1,429만 5,000 배럴/일로 2021년에는 1,489만 3,000 배럴/일이었습니다. 또한 2012년부터 22년까지 10년간 소비량 증가율은 연률 3.6%였습니다.

- 게다가, 위 보고서는 중국이 천연가스 생산 분야에서 긍정적인 성장을 이룩했다는 것을 보여줍니다. 예를 들어, 2021년 천연가스 생산량은 2,092억 입방미터였지만, 2022년에는 2,218억 입방미터로 증가하였으며, 이는 약 6.0%의 성장입니다. 또한 지난 10년간 생산량은 연평균 7.1% 증가했습니다.

- 중국 내 석유 및 가스 생산 능력 증가는 중국 유전용 화학제품 시장을 견인할 것으로 예상됩니다.

아시아태평양 유전 화학제품 산업 개요

아시아태평양의 유전 화학 시장은 그 특성상 부분적으로 통합되어 있습니다. 주요 기업(순서부동)에는 AkzoNobel NV, Haliburton, Huntsman International LLC, Baker Hughes Company, BASF SE 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 성과

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 촉진요인

- 운수 산업 내 석유계 연료 수요 증가

- 아시아태평양의 셰일 가스 탐사 및 생산 증가

- 기타 촉진요인

- 억제요인

- 바이오연료 산업의 상승

- 청정 에너지 이니셔티브

- 산업 가치사슬 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

- 화학 유형

- 살생물제

- 부식 및 스케일 방지제

- 유화제

- 폴리머

- 계면활성제

- 기타 화학제품(유기산, 분쇄액 등)

- 용도

- 시추와 시멘팅

- 석유 회수 향상

- 생산

- 갱정 주입

- 개수 및 완공

- 지역

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 필리핀

- 호주 및 뉴질랜드

- 기타 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- AkzoNobel NV

- Albemarle Corporation

- Ashland

- Baker Hughes Company

- BASF SE

- CLARIANT

- Chevron Phillips Chemical Company LLC

- Dow

- Ecolab

- Elementis PLC

- Haliburton

- Huntsman International LLC

- Innospec

- Kemira

- Newpark Resources Inc.

- SLB

- Solvay

제7장 시장 기회와 앞으로의 동향

- 심해 시추 사업이 여는 새로운 지평

- 신흥국가가 가져오는 생산 기회

The Asia-Pacific Oilfield Chemicals Market size is estimated at USD 2.31 billion in 2025, and is expected to reach USD 2.88 billion by 2030, at a CAGR of greater than 4.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the oil and gas industry, which in turn affected the oilfield chemicals market in the Asia-Pacific region. However, post-COVID-19, the rising demand from the oil and gas industry is expected to revive the market for oilfield chemicals in the region.

Key Highlights

- One of the major factors driving the market's growth is the increased share of gas exploration and production in the Asia-Pacific region. Rising demand for petroleum-based fuel from the transportation industry is expected to drive the market demand during the forecast period.

- The rising biofuel industry is likely to hinder the market growth. With the increasing focus on sustainability and environmental concerns, the oilfield chemicals industry may face regulatory pressures and a decline in investor interest as well.

- The increasing focus on deepwater and unconventional resources like shale oil and gas opens up new markets for drilling fluids, lubricants, and completion fluids. Developing high-performance, environmentally friendly chemicals for these challenging environments is a lucrative opportunity.

- China dominated the market across the Asia-Pacific Region, with the most significant consumption of oilfield chemicals in this region.

Asia-Pacific Oilfield Chemicals Market Trends

Corrosion and Scale Inhibitors segment to dominate the market

- Corrosion inhibitors are used to reduce corrosion in the metallic pipes of the oil well. Inhibition is the preferred treatment for carbon steel pipes and vessels. The advantage of inhibition is that it can be used in most cases even when the process is continuing.

- Corrosion occurs due to the reaction of oxygen with metallic parts to form oxides. Corrosion inhibitors act by forming a thin barrier layer over the exposed parts. Several types of corrosion inhibitors are used in oilfields.

- These include Deha - Diethyl Hydroxyl Amine, Polyamine, Morpholine, Cyclohexylamine, and Carbon Dioxide Corrosion Inhibitors. A mixture of filming amines is used to prepare condensate line corrosion inhibitors. This can protect every stage due to the presence of both high and low vapor/liquids.

- Scale is a residue that forms on the surface of oilfield equipment as a result of the precipitation of soluble solids that become insoluble as temperature increases. This, in turn, causes metallic corrosion that affects the functioning and maintenance of equipment. This deposition increases corrosion rates, causes loss of production, and restricts flow.

- Hence, to safeguard oilfield equipment and to maintain their efficiency, it is necessary to maintain accurate conditions by adding scientifically designed chemicals that act as scale inhibitors. Chemicals, such as organic phosphates, inorganic phosphates, polymers (polyacrylates), phosphonates, and ethylenediaminetetraacetic acid (EDTA), an organic chelating agent, are some of the scaling inhibitors. Corrosion inhibitors are used to reduce corrosion in metallic pipes of oil wells. Inhibition is the preferred treatment for carbon steel pipes and vessels.

- As per Rystad, offshore projects will drive the recovery in greenfield investment, with significant demand for subsea infrastructure and drilling services in the oil and gas industry.

- For example, Petronas's Kasawari announced investment approval for the first carbon capture and storage (CCS) in Malaysia, which was followed by Thai company PTT Exploration and Productions's (PTTEP's) Lang Lebah, targeting FID in 2023 in Malaysia.

- Shell's recent investment approval for the Gumusut-Kakap-Geronggong-Jagus East (GKGJE) deep-water project - a subsea tieback development planned to start up in 2024, according to the Energy Industries Council.

- As per S&P Global Inc., New Zealand's Refining NZ said it was working to finalize terminal services agreements with customers in October to enable the conversion of its Marsden Point refinery into an import terminal in the first half of 2022.

- As per S&P Global Inc, Australia's Viva Energy welcomed the federal government's announcement of a fuel security package and, as part of this, would make a six-year commitment to maintain refining operations at Geelong through to June 2027 with a further three-year option to extend until June 2030.

- A USD 4 billion clean fuel project is being undertaken at Thailand's Sriracha refinery. The upgrade is slated to be completed in 2023 and will increase the refinery's capacity from 275,000 b/d to 400,000 b/d, boosting the yield of cleaner products. as per S&P Global Inc.

- Furthermore, new contracts for maintenance in Asia-Pacific exhibit increased investment in corrosion and scale inhibitors during the forecast period.

China to Dominate the Market

- The oil and gas industry is one of the key contributors to the Chinese economy. The oil and gas industry operates in high-temperature environments.

- Oilfield chemicals are used in drilling, production, stimulation, and enhanced oil recovery activities. Developing oil and gas reserves from shale formations requires activities such as hydraulic drilling, which encourages the use of oilfield chemicals. China has achieved many milestones in capacity and drilling techniques in shale gas exploration. This makes it one of the top shale gas suppliers around the globe.

- According to BP Statistical Review 2023, the overall oil production in the country reached 204.7 million metric tons in 2022 at a growth rate of 2.9% compared to 198.9 million metric tons produced in 2021.

- Similarly, the country's overall oil consumption has been on the rise over the past decade. For instance, in 2022, the country's oil consumption in thousands of barrels per day was 14,295 thousand barrels per day, whereas in 2021, the consumption stood at 14,893 thousand barrels per day. In addition, the consumption growth rate has been 3.6% yearly over the decade between 2012 and 22.

- Moreover, the same source cited that the country witnessed positive growth in natural gas production. For instance, in 2021, the natural gas produced was 209.2 billion cubic meters, whereas in 2022, the production increased to 221.8 billion cubic meters, which is around 6.0% growth. In addition, over the decade, production has been growing by an average of 7.1% yearly.

- The increase in the production capacities of oil and gas in the country is likely to drive the market for oilfield chemicals in the country.

Asia-Pacific Oilfield Chemicals Industry Overview

The Asia-Pacific oilfield chemicals market is partially consolidated in nature. The major players (not in a particular order) include AkzoNobel N.V., Haliburton, Huntsman International LLC, Baker Hughes Company, and BASF SE, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Petroleum-based Fuel from the Transportation Industry

- 4.1.2 Increased Shale Gas Exploration and Production in Asia-Pacific

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Rising Biofuel Industry

- 4.2.2 Clean Energy Initiatives

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemical Type

- 5.1.1 Biocide

- 5.1.2 Corrosion and Scale Inhibitor

- 5.1.3 Demulsifier

- 5.1.4 Polymer

- 5.1.5 Surfactant

- 5.1.6 Other Chemical Types (Organic Acids, Fracturing Fluids, etc.)

- 5.2 Application

- 5.2.1 Drilling and Cementing

- 5.2.2 Enhanced Oil Recovery

- 5.2.3 Production

- 5.2.4 Well Stimulation

- 5.2.5 Workover and Completion

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Malaysia

- 5.3.6 Thailand

- 5.3.7 Indonesia

- 5.3.8 Vietnam

- 5.3.9 Philippines

- 5.3.10 Australia & New Zealand

- 5.3.11 Rest of Asia-pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Albemarle Corporation

- 6.4.3 Ashland

- 6.4.4 Baker Hughes Company

- 6.4.5 BASF SE

- 6.4.6 CLARIANT

- 6.4.7 Chevron Phillips Chemical Company LLC

- 6.4.8 Dow

- 6.4.9 Ecolab

- 6.4.10 Elementis PLC

- 6.4.11 Haliburton

- 6.4.12 Huntsman International LLC

- 6.4.13 Innospec

- 6.4.14 Kemira

- 6.4.15 Newpark Resources Inc.

- 6.4.16 SLB

- 6.4.17 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Horizons Opened Up due to Deep-water Drilling Operations

- 7.2 Production Opportunities Provided by Developing Countries