|

시장보고서

상품코드

1851537

열가소성 엘라스토머 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Thermoplastic Elastomer (TPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

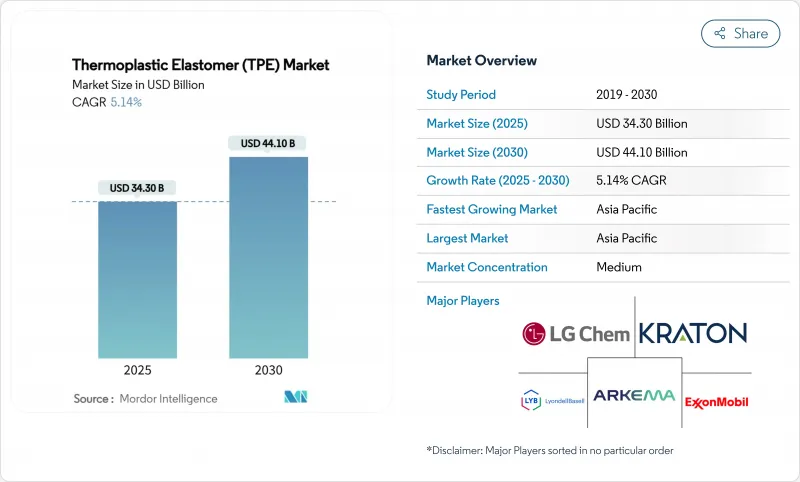

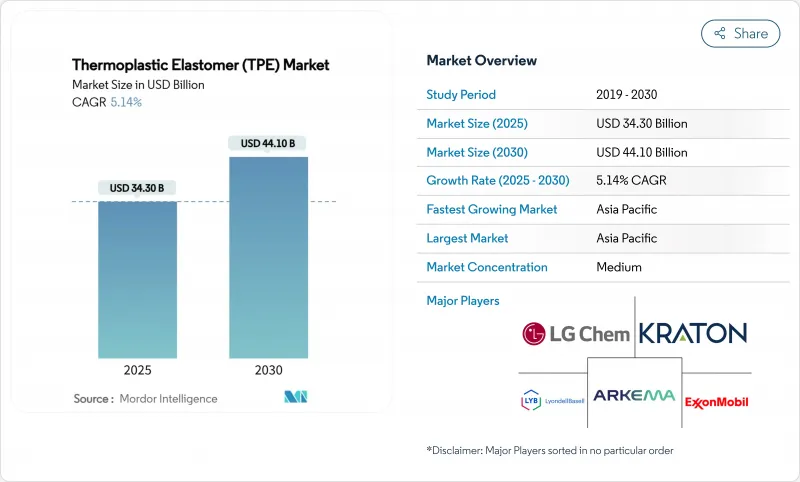

열가소성 엘라스토머 시장 규모는 2025년에 343억 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.14%로, 2030년에는 441억 달러에 이를 것으로 예상됩니다.

이 진보는 고무와 같은 유연성과 열가소성 수지의 가공 효율을 겸비한 이 소재의 능력을 부각하고 있으며, 이 조합은 현재 자동차의 전동화, 차세대 의료기기, 순환형 제조의 의무화에 필수적입니다. 생산자는 지역의 생산 능력을 확대하고 지속가능성에 대한 규제와 기업의 넷 제로 목표를 충족시키기 위해 저탄소에서 재활용 함량이 높은 등급을 도입하고 있습니다. 아시아태평양은 광범위한 자동차 및 전자 제품 공급망, 건강 관리 투자, 전기자동차 정책 지원을 통해 생산 및 소비의 중심이 되고 있습니다. 헬스케어의 현대화와 PVC와 라텍스를 생체적합성이 높은 대체품으로 대체하는 움직임이 더욱 기세를 늘리고, 배터리 전기자동차에서는 와이어 하네스와 충전용 하드웨어의 경량화가 이익률이 높은 제형에 대한 수요를 더욱 끌고 있습니다. 열가소성 엘라스토머 시장은 아디프산의 변동성과 기계 비용의 상승이 브레이크가 되고 있는 것, 산업계가 보다 경량으로 리사이클할 수 있는 설계의 자유도가 높은 재료를 요구하고 있기 때문에 바닥 견고한 성장을 유지하고 있습니다.

세계의 열가소성 엘라스토머 시장 동향과 인사이트

자동차용 와이어 케이블의 EV 경량화 추진

전기자동차 혁명은 와이어 및 케이블의 사양을 근본적으로 바꾸고 있으며, 열가소성 엘라스토머가 경량화와 성능 최적화의 중요한 실현 요인으로 부상하고 있습니다. 세라니즈의 하이트렐 TPC-LCF는 -40°C에서 130°C의 내열성을 가지면서 탄소 실적의 50% 삭감을 실현해, 폴리머 재킷이 전기자동차의 하네스 경량화에 도움이 되고 있음을 나타내고 있습니다. 가교 폴리올레핀은 현재 고전압 라인에서 실리콘을 대체하고 내마모성을 제공하여 배선 경로를 단축하고 구리 사용을 줄입니다. 중국의 OEM이 견인하는 아시아태평양은 전기자동차 생산 대수의 대부분을 차지하고 있기 때문에 현지 컴파운더가 우선 대수의 성장을 확보하고 있습니다. TPE 재킷은 자동차 충전 패드와 냉각수 튜브에도 사용되며, 자동차당 평균 폴리머 함량이 증가하고 열가소성 엘라스토머 시장의 수익이 확대되고 있습니다.

난방·환기·공조(HVAC) 산업에서의 용도 확대

히트펌프의 채용과 새로운 냉매의 채용에 의해 실링과 진동의 요건이 엄격해지고 있습니다. TE 커넥티비티는 가스켓과 호스 라이너의 EPDM에서 고온 TPE로의 교체를 촉진하는 수명 신뢰성을 조달 기준으로 꼽았습니다. DSM의 Arnitel HT는 일체형 열풍 덕트를 가능하게 하여 무게를 40%, 부품 비용을 50% 절감합니다. 디지털 제어 컴프레서에는 센서를 탑재하면서 소음을 감쇠시키는 유연한 마운트도 필요하며, 열가소성 엘라스토머 시장의 특수 TPE 컴파운드가 그 역할을 충분히 완수하고 있습니다.

아디프산 공급에 의한 열가소성 폴리우레탄(TPU)의 가격 변동

원재료 비용 인플레이션은 열가소성 폴리우레탄(TPU)의 밸류체인 전반에 큰 마진 압력을 제공하며, 아디프산 공급 제약이 가격 안정성과 생산 계획에 영향을 미치는 중요한 병목 현상이 되었습니다. BASF는 부탄디올 유도체의 가격을 인상하고 TPU 제조업체의 비용 변동을 증폭시켰습니다. 클레이톤 폴리머는 SIS에서 330톤의 인상을 실시하여 전체 블록 코폴리머의 병렬 인플레이션을 보였습니다. 석유 원료가 급등하고 물류가 느려지면 컨버터는 스프레드 축소에 직면하고 일부 상대방 상표 제품 제조업체(OEM)는 열가소성 엘라스토머 시장에서 TPU에 의존하는 중요하지 않은 프로젝트를 연기하게 됩니다.

부문 분석

열가소성 올레핀은 2024년의 수익 25.59%로 최상위에 달했고, 2030년까지의 CAGR은 7.39%로 예측되어, 부문 레벨에서 열가소성 엘라스토머 시장 규모의 최대 슬라이스를 유지합니다. TPE-O는 폴리프로필렌 기재와 쉽게 접착되어 내후성이 뛰어나므로 자동차 제조업체는 범퍼 페이시아, 에어댐 실, 언더바디 패널에 TPE-O를 사용하고 있습니다. 건설 프로파일과 소비재는 특히 비용면에서 PP 기반 합금이 유리하기 때문에 수량이 증가하고 있습니다.

TPU는 스포츠 신발, 컨베이어 벨트, 카테터 자켓 등의 마모가 중요한 용도로 선호되어 금액 기준으로 2위를 차지하고 있습니다. 성장의 기세는 아디프산 가격의 불안정성에 의해 억제되었지만, 높은 부가가치 틈새 시장은 이익을 유지하고 있습니다. TPV는 140℃의 피크를 견뎌야 하는 보닛 아래의 공기 관리 부품에서 약간의 차이로 계속됩니다. 스티렌계 블록 공중합체는 접착제와 일회용 면도기로 점유율을 유지하고, TPC와 TPA는 드라이브 벨트, 공압 튜브, 차지 에어 덕트에 그 밑단을 펼치고 있습니다. Teknor Apex의 EV 배터리 씰용 Sarlink TPV와 같은 특수 화합물은 혼합 노하우가 열가소성 엘라스토머 시장에서 프리미엄 가격을 어떻게 실현하는지 보여줍니다.

지역 분석

아시아태평양은 2024년 판매액의 46.84%를 차지했고, 열가소성 엘라스토머 시장의 지역별 점유율에서 가장 높으며, 2030년까지의 CAGR은 6.45%를 나타낼 전망입니다. 중국은 세계 자동차의 거의 3대에 1대를 생산해 스마트폰이나 가전제품의 대규모 클러스터를 안고 있는 지점이 되고 있습니다. 상하이에서 나일론 66의 생산 능력을 연산 40만 톤으로 두배로 하는 인비스타의 움직임은 컴파운더의 성장을 지지하는 원재료의 자급자족을 명확하게 보여줍니다. 한국은 디스플레이와 배터리 부품을 공급하고 인도는 신재생에너지용 와이어 앤 케이블의 제조를 확대하고 역내 무역을 유지하고 있습니다.

북미는 여전히 기술 혁신이 활발합니다. 디트로이트 OEM은 바이오 TPV 윈도우 씰을 지정하고 보스턴 지역의 의료기기 신흥 기업은 새로운 카테터 코팅을 시험적으로 사용하여 수익성이 높은 틈새 시장을 고정시킵니다. 세라니즈의 하이트렐 TPC-LCF는 Chinaplas에서 발표되었지만, 텍사스에서 개발된 것으로 미국의 인플레이션 삭감법의 인센티브에 맞추어 이산화탄소 배출량의 50% 삭감을 달성했습니다. 2025년부터 실시되는 석유화학제품의 수입관세는 수지비용에 12-20% 상승할 수 있으며, 컴파운드 제조업체는 중간체 생산을 재보유하고 국내 TPU 라인의 생산능력을 확대할 가능성이 있습니다.

유럽 환경 지침은 애비언트의 재사용 REC GP 7820과 같은 재활용 원료를 60% 포함하는 TPE의 보급을 가속화합니다. 독일 Tier 1은 유로 7 콜드 스타트 요구 사항을 충족하는 TPV 라디에이터 호스를 테스트합니다. 한편, 스페인과 이탈리아에서는 탈탄소 목표를 달성하기 위해 Arnitel HT 덕트를 이용한 히트펌프의 개조를 전개하고 있습니다. 남미와 중동 및 아프리카는 현재 규모가 작지만 인프라가 확대됨에 따라 장기적인 상승 여지가 있습니다. 멕시코는 현재 세계 4위의 폴리우레탄 시장이 되고 있는데, 이는 미국의 자동차 공급망이 니어 쇼어링화되어 TPU 사출 성형 제조업체가 OEM에 가까워지고 있음을 반영하고 있습니다. 걸프 협력 회의 국가는 원유 수출에서 다각화하기 위해 특수 엘라스토머 허브에 투자하고 있으며, 이는 열가소성 엘라스토머 시장의 강하 수요 지역화를 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차용 와이어·케이블에 있어서 EV 경량화의 추진

- 난방·환기·공조(HVAC) 산업에 있어서 용도의 성장

- 가전제품에서의 이용 확대

- 헬스케어 산업에서의 수요 증가

- 신발와 스포츠 용품 수요

- 시장 성장 억제요인

- 아디프산 공급에 의한 TPU(열가소성 폴리우레탄) 가격 변동

- 높은 제조 비용과 장비 비용

- 연질 열가소성 수지에 의한 3D 프린팅의 과제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 유형별

- 스티렌계 블록 공중합체(TPE-S)

- 열가소성 올레핀(TPE-O)

- 열가소성 가황체(TPV)

- 열가소성 폴리우레탄(TPU)

- 열가소성 공중합에스터(TPC)

- 열가소성 폴리아미드(TPA)

- 용도별

- 자동차 및 운송

- 건축 및 건설

- 신발

- 전기 및 전자

- 의료

- 기타 용도(가정용품, 접착제 및 실란트, HVAC)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Arkema

- Asahi Kasei Corporation.

- Avient Corporation

- BASF

- Celanese

- Covestro AG

- Group Dynasol

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- Huntsman International LLC

- Kraton Corporation

- Lanxess

- LCY

- LG Chem

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Group Corporation.

- SABIC

- Teknor Apex

- Sumitomo Chemical Co., Ltd.

- APAR Industries Ltd.

- The Lubrizol Corporation

제7장 시장 기회와 향후 전망

KTH 25.11.21The Thermoplastic Elastomer Market size is estimated at USD 34.30 billion in 2025, and is expected to reach USD 44.10 billion by 2030, at a CAGR of 5.14% during the forecast period (2025-2030).

This advance highlights the material's ability to combine rubber-like flexibility with thermoplastic processing efficiency, a combination now integral to vehicle electrification, next-generation medical devices, and circular manufacturing mandates. Producers are expanding regional capacity and introducing low-carbon, recycled-content grades to satisfy sustainability regulations and corporate net-zero targets. Asia-Pacific continues to anchor production and consumption thanks to its extensive automotive and electronics supply chains, healthcare investment, and policy support for electric vehicles. Healthcare modernization and the ongoing replacement of PVC and latex with biocompatible alternatives add another layer of momentum, while lighter wire harnesses and charging hardware in battery-electric cars further pull demand into high-margin formulations. Despite adipic-acid volatility and elevated machinery costs acting as brakes, the thermoplastic elastomers market retains a resilient growth profile as industries seek lighter, recyclable, and more design-flexible materials.

Global Thermoplastic Elastomer (TPE) Market Trends and Insights

EV Light Weighting Push in Automotive Wire and Cable

The electric vehicle revolution is fundamentally reshaping wire and cable specifications, with thermoplastic elastomers emerging as critical enablers of weight reduction and performance optimization. Celanese's Hytrel TPC-LCF delivers a 50% carbon-footprint cut while enduring -40 °C to 130 °C, illustrating how polymeric jacketing helps reduce harness weight in electric vehicles. Cross-linked polyolefins now displace silicone in high-voltage lines, providing abrasion resistance that shortens routing paths and trims copper usage. Asia-Pacific, led by Chinese OEMs, dominates EV output, so local compounders secure volume growth first. TPE jacketing is also moving into onboard charging pads and coolant tubes, lifting average polymer content per vehicle and magnifying revenue inside the thermoplastic elastomers market.

Growing Application in the Heating, Ventilation, and Air Conditioning (HVAC) Industry

Heat-pump adoption and new refrigerants intensify sealing and vibration requirements. TE Connectivity cites lifetime reliability as a procurement benchmark, spurring substitution of EPDM with higher-temperature TPEs in gaskets and hose liners. DSM's Arnitel HT permits single-piece hot-air ducts, cutting weight 40% and part cost 50%, a direct gain for installers targeting energy-efficient retrofits. Digitally controlled compressors also need flexible mounts that dampen noise while hosting sensors, a niche well served by specialty TPE compounds in the thermoplastic elastomers market.

Thermoplastic Polyurethane (TPU) Price Volatility Due to Adipic Acid Supply

Raw material cost inflation is creating significant margin pressure across the Thermoplastic Polyurethane (TPU) value chain, with adipic acid supply constraints representing a critical bottleneck that affects pricing stability and production planning. BASF raised butanediol derivative prices, amplifying cost swings for TPU makers . Kraton implemented a USD 330 t increase on SIS, signifying parallel inflation across block copolymers. When petroleum feedstocks spike and logistics falter, converters face slimmer spreads, prompting some Original Equipment Manufacturers (OEMs) to defer non-critical projects that rely on TPU inside the thermoplastic elastomers market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Utilization in Consumer Electronics

- Increasing Demand from Healthcare Industry

- High Manufacturing and Equipment Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoplastic olefins led with 25.59% 2024 revenue and are forecast to post the segment-best 7.39% CAGR through 2030, sustaining the largest slice of the thermoplastic elastomers market size at segment level. Automakers rely on TPE-O for bumper fascia, air-dam seals, and under-body panels because the blends bond readily with polypropylene substrates and resist weathering. Construction profiles and consumer goods add volume, especially where cost targets favor PP-based alloys.

TPU holds the number-two spot by value, favored for abrasion-critical uses in athletic shoes, conveyor belts, and catheter jacketing. Growth momentum remains tempered by adipic-acid price instability, yet high value-added niches preserve margins. TPV follows closely in under-hood air-management parts that must tolerate 140 °C peaks. Styrenic block copolymers keep share in adhesives and disposable razors, while TPC and TPA extend reach into drive belts, pneumatic tubing, and charge-air ducts. Specialty compounding, such as Teknor Apex's Sarlink TPV for EV battery seals, demonstrates how formulation know-how unlocks premium pricing within the thermoplastic elastomers market.

The Thermoplastic Elastomers Market Report is Segmented by Product Type (Styrenic Block Copolymers (TPE-S), Thermoplastic Olefins (TPE-O), Thermoplastic Vulcanizates (TPV), and More), Application (Automotive and Transportation, Building and Construction, Footwear, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific claimed 46.84% of 2024 value, the highest thermoplastic elastomers market share among regions, and is on course for a 6.45% CAGR to 2030. China represents the fulcrum, producing nearly one in three vehicles globally and hosting expansive smartphone and appliance clusters. INVISTA's move to double Nylon 6,6 capacity to 400,000 t/y in Shanghai underscores raw-material self-sufficiency that underpins compounder growth. South Korea supplies display and battery components, while India escalates wire-and-cable builds for renewable energy, sustaining intra-regional trade.

North America remains innovation-heavy. Detroit OEMs specify bio-based TPV window seals, and Boston-area medical device startups pilot new catheter coatings, locking in profitable niches. Celanese's Hytrel TPC-LCF, launched at Chinaplas yet developed in Texas, achieves a 50% carbon-footprint cut, aligning with US Inflation Reduction Act incentives. Tariffs on petrochemical imports, effective 2025, could add 12-20% to resin costs, nudging compounders to reshore intermediate production and potentially opening capacity for domestic TPU lines.

Europe's environmental directives accelerate uptake of recycled-content TPEs such as Avient's reSound REC GP 7820, which contains 60% post-consumer feedstock . German Tier 1s test TPV radiator hoses that meet Euro 7 cold-start requirements. Meanwhile, Spain and Italy deploy heat-pump retrofits that use Arnitel HT ducting to meet decarbonization targets. South America and the Middle East & Africa are smaller today yet offer long-run upside as infrastructure expands. Mexico is now the world's fourth-largest polyurethane market, reflecting near-shoring of US automotive supply chains and drawing TPU injection molders closer to OEMs. Gulf Cooperation Council countries invest in specialty elastomer hubs to diversify away from crude exports, hinting at localized downstream demand within the thermoplastic elastomers market.

- Arkema

- Asahi Kasei Corporation.

- Avient Corporation

- BASF

- Celanese

- Covestro AG

- Group Dynasol

- dsm-firmenich

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- Huntsman International LLC

- Kraton Corporation

- Lanxess

- LCY

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Group Corporation.

- SABIC

- Teknor Apex

- Sumitomo Chemical Co., Ltd.

- APAR Industries Ltd.

- The Lubrizol Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Light Weighting Push in Automotive Wire and Cable

- 4.2.2 Growing Application in the Heating, Ventilation, and Air Conditioning (HVAC) Industry

- 4.2.3 Increasing Utilization in Consumer Electronics

- 4.2.4 Increasing Demand from Healthcare Industry

- 4.2.5 Subtantial Demand from Footwear and Sports Equipment

- 4.3 Market Restraints

- 4.3.1 TPU (Thermoplastic Polyurethane) Price Volatility Due to Adipic Acid Supply

- 4.3.2 High Manufacturing and Equipment Cost

- 4.3.3 Challenges of 3D Printing with Soft Thermoplastics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Styrenic Block Copolymers (TPE-S)

- 5.1.2 Thermoplastic Olefins (TPE-O)

- 5.1.3 Thermoplastic Vulcanizates (TPV)

- 5.1.4 Thermoplastic Polyurethane (TPU)

- 5.1.5 Thermoplastic Copolyester (TPC)

- 5.1.6 Thermoplastic Polyamide (TPA)

- 5.2 By Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Building and Construction

- 5.2.3 Footwear

- 5.2.4 Electrical and Electronics

- 5.2.5 Medical

- 5.2.6 Other Applications (Household Goods, Adhesive and Sealants, HVAC)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corporation.

- 6.4.3 Avient Corporation

- 6.4.4 BASF

- 6.4.5 Celanese

- 6.4.6 Covestro AG

- 6.4.7 Group Dynasol

- 6.4.8 dsm-firmenich

- 6.4.9 DuPont

- 6.4.10 Evonik Industries AG

- 6.4.11 Exxon Mobil Corporation

- 6.4.12 Huntsman International LLC

- 6.4.13 Kraton Corporation

- 6.4.14 Lanxess

- 6.4.15 LCY

- 6.4.16 LG Chem

- 6.4.17 LyondellBasell Industries Holdings B.V.

- 6.4.18 Mitsubishi Chemical Group Corporation.

- 6.4.19 SABIC

- 6.4.20 Teknor Apex

- 6.4.21 Sumitomo Chemical Co., Ltd.

- 6.4.22 APAR Industries Ltd.

- 6.4.23 The Lubrizol Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Bio-Based Thermoplastic Elastomers