|

시장보고서

상품코드

1640654

북미의 전문 클라우드 서비스 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Professional Cloud Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

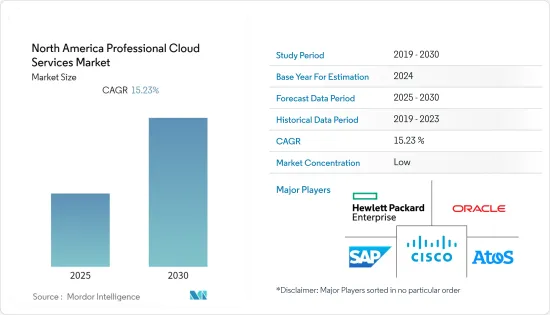

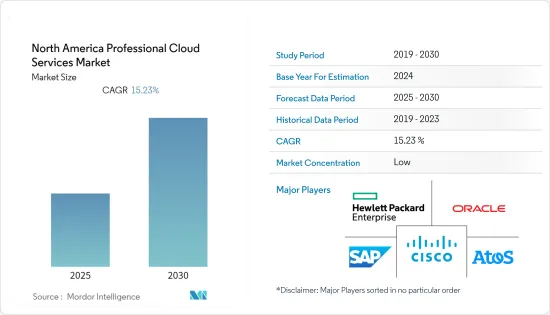

북미의 전문 클라우드 서비스 시장은 예측 기간 동안 CAGR 15.23%를 나타낼 전망입니다.

주요 하이라이트

- 전문 클라우드 서비스를 통해 소비자는 다양한 유형의 클라우드 서비스를 배포할 수 있습니다. 클라우드는 IT 혁신의 촉매 역할을 하며 선호하는 클라우드와 기존 온프레미스 인프라를 워크로드에 최적의 비율로 결합할 수 있는 유연성을 제공합니다.

- COVID-19 동안 직원의 안전을 유지하기 위해 많은 기업들이 규제와 정책을 변경해야 했습니다. 앞서 언급했듯이 업무 혼란의 가장 큰 원인은 노동력의 움직임과 인사를 조정할 수 없다는 것입니다. 출장이나 해외 입국이 어렵고 사회적인 거리도 멀어졌기 때문에 기업은 현재의 기능방법을 변경하고 업무상의 선택을 재고할 필요가 있었습니다.

- 클라우드 구축의 주요 요인은 자본 지출 감소, IT 관리의 복잡성, 새로운 용도을 신속하게 배포할 수 있다는 것입니다. 이러한 요인은 기업의 클라우드 기반 플랫폼 채택을 뒷받침하고 있습니다. 최신 멀티테넌트 클라우드 플랫폼 서비스를 통해 수천 명의 고객이 동일한 리소스를 활용할 수 있습니다. 그 결과 노동력과 그에 따른 비용을 크게 절약할 수 있습니다.

- 가장 성공적인 클라우드 사업자인 Google의 존재는 클라우드에서 제공하는 대규모 웹 기반 용도의 실행 가능성을 입증합니다. Microsoft는 현재 클라우드 기반 플랫폼에서 서비스를 제공하고 있으며, 북미에서 이 시장의 핵심 촉진요인 중 하나가 되고 있습니다.

- 성능 관련 문제와 데이터 보안에 대한 우려는 업계가 직면한 주요 과제입니다. 그러나 최근 기술의 진보는 이러한 문제를 해결하고 기업이 핵심 역량에 집중할 수 있도록 노력하고 있습니다.

북미의 전문 클라우드 서비스 시장 동향

하이브리드 클라우드가 시장에서 높은 성장을 기대

- 하이브리드 클라우드는 Google Cloud 및 Amazon Web Services와 같은 퍼블릭 클라우드 제공업체와 프라이빗 클라우드를 결합한 것입니다. 컴퓨팅 요구와 비용 변화에 따라 워크로드를 퍼블릭 클라우드와 프라이빗 클라우드 간에 이동할 수 있게 함으로써 하이브리드 클라우드는 기업의 유연성을 높이고 데이터 배포 옵션을 늘릴 수 있습니다.

- 이 지역의 기업은 경쟁 우위를 얻기 위해 신제품과 새로운 서비스를 투입하고 있습니다. 예를 들어 Hewlett Packard Enterprise는 고객이 온프레미스 및 오프프레미스 클라우드를 관리하고 최적화할 수 있도록 설계된 HPE GreenLake Hybrid Cloud를 발표했습니다. HPE GreenLake Hybrid Cloud는 Microsoft Azure, AWS, Azure Stack과 같은 주요 클라우드 솔루션에서 고객 환경의 지속적인 관리 및 최적화를 제공합니다.

- 또한 다양한 규모의 조직이 전통적인 비즈니스 형태에서 디지털 비즈니스 형태로 변화하고 있습니다. 이러한 변화는 총 소유 비용(TCO) 감소, 높은 보안, 유연성, 민첩성 등의 이점을 제공하여 하이브리드 클라우드 시장을 창출하고 있습니다. IBM은 IT 리더의 89%가 비즈니스 크리티컬 워크로드를 클라우드로 마이그레이션할 것으로 기대하고 있으며 디지털화의 진전이 모든 것을 뒷받침하고 있다고 말합니다.

- 이 지역에서는 온프레미스 및 오프프레미스 하이브리드 클라우드 사용이 증가하고 있습니다. 2021년 연방 정부 IT 관리자의 92%가 하이브리드 클라우드가 탄력 있는 정부를 위한 최적의 운영 환경임에 동의했습니다. 또한 3분의 2 이상(67%)이 COVID-19에 의해 조직에 있어서의 하이브리드 클라우드의 도입이 1년 이상 가속했다고 응답하고 있습니다.

- 게다가 시스코는 2021년까지 클라우드 워크로드와 컴퓨팅 인스턴스의 73%가 퍼블릭 클라우드 데이터센터에 놓여 2016년 58%에서 증가할 것으로 예측했다(5년 CAGR은 27.5%).

- 게다가 지난해 버지니아주 북부는 미국의 주요 데이터센터 시장에서 가장 데이터센터의 순흡수량이 많아 303.3메가와트에 달했습니다. 이러한 데이터센터 도입 동향은 전문 클라우드 서비스 시장의 성장을 가속화할 것으로 예상됩니다.

미국이 최대 시장을 차지할 것으로 예측

- 클라우드 서비스 시장을 독점하는 것은 미국입니다. 이 지역은 클라우드 컴퓨팅 서비스를 일찍부터 도입해 왔습니다. 또한 이 지역은 모든 분야에서 클라우드 서비스 기술을 적극적으로 도입하는 자세를 보이고 있습니다.

- Stormforgein이 2021년 4월에 발표한 보고서에 따르면 북미 응답자의 18%가 회사 조직의 클라우드 이용 금액이 월10만 달러에서 25만 달러라고 답했습니다. 또한 응답자의 44%는 향후 1년 동안 클라우드 지출이 다소 증가할 것으로 예상하고, 다른 32%는 향후 1년간 조직 클라우드에 대한 지출이 크게 증가할 것으로 예상하고 있습니다.

- IT 부서는 이미 이 기술을 채택하고 있습니다. 북미에서 클라우드 컴퓨팅 서비스의 새로운 분야는 건강 관리 분야입니다. 이 기술은 데이터 스토리지 서비스의 범위를 벗어나 현재 비용을 절감하면서 환자 관리를 개선하고 개인화하기 위해 이 기술이 어떻게 사용되는지에 초점을 맞추었습니다.

- 대규모 배포의 주요 요인은 SaaS 기반 서비스에 대한 조직 기울기 및 디지털 비즈니스 전략의 채택입니다. 또한 데이터 무결성과 프라이버시 기반 클라우드 서비스에 대한 수요의 지속적인 증가는 조사 기간 동안 더욱 증가하고 주요 공급업체가 시장에서 성장할 기회를 늘릴 수 있을 것으로 예상됩니다.

북미의 전문 클라우드 서비스 산업 개요

시장 경쟁 구도는 세분화되어 있으며 다음과 같은 주요 기업이 존재합니다. Cisco Systems Inc., Oracle Corporation, Atos SE, SAP SE, and Hewlett Packard Enterprise Company 등이 있습니다. 개인 및 조직에서 온프레미스 및 프라이빗 클라우드 사용이 증가함에 따라 시장에는 여러 제품이 출시되고 있습니다.

2022년 8월 IBM은 하이브리드 클라우드 솔루션을 제공하기 위해 VMware와의 제휴를 발표했습니다. 이 제휴는 금융 서비스, 헬스케어, 공공 부문과 같은 업계 기업들이 하이브리드 환경에 미션 크리티컬 워크로드를 배치하는 비용과 위험을 줄이는 데 도움이 되는 공동 엔지니어링 클라우드 솔루션을 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 세분화

- 전개 유형별

- 퍼블릭

- 프라이빗

- 하이브리드

- 서비스 모델별

- Platform-as-a-Service

- Software-as-a-Service

- Infrastructure-as-a-Service

- 최종 사용자 업계별

- 헬스케어

- 소매

- 엔터테인먼트 및 미디어

- 정부 및 공공기관

- BFSI

- 정보통신기술

- 기타 최종 사용자 업계

- 국가별

- 미국

- 캐나다

제6장 경쟁 구도

- 기업 프로파일

- Cisco Systems Inc.

- Hewlett Packard Enterprise Company

- Cognizant

- Accenture PLC

- Dell EMC

- Microsoft Corporation

- Fujitsu Limited

- Capgemini SE

- Infosys Limited

- Nippon Data Systems Ltd

- HCL Technologies Limited

- Oracle Corporation

- NTT Data

- Atos SE

- SAP SE

제7장 투자 분석

제8장 시장 기회와 앞으로의 동향

KTH 25.02.19The North America Professional Cloud Services Market is expected to register a CAGR of 15.23% during the forecast period.

Key Highlights

- Professional cloud services allow consumers to deploy various types of cloud services. Cloud acts as a catalyst for IT transformation, delivering the flexibility to combine the preferred clouds and existing on-premises infrastructure in the ratio best suited for the workload.

- Maintaining employees' safety during COVID-19 forced many corporations to change their regulations and policies. As stated earlier, the foremost cause of the business disruption was the inability to move the workforce and coordinate HR. The inability to travel and cross borders and social distancing forced businesses to change their current ways of functioning and reconsider operational choices.

- The primary drivers for cloud adoption are reducing capital expenditure spending, IT management complexity, and the ability to deploy new applications faster. These factors are helping companies adopt cloud-based platforms. Modern, multi-tenant cloud platform services enable thousands of customers to use the same resources. This results in saving a lot of the workforce and the expenses involved.

- The presence of Google, the most successful cloud operator, has proven the viability of large-scale, web-based applications provided from the cloud. Microsoft, currently moving to offer its services on a cloud-based platform, is one of the core drivers of this market in North America.

- Performance-related issues and data security concerns are the significant challenges faced by the industry. However, recent technological advancements are striving to rectify these problems and ensure that companies can concentrate on their core competencies.

North America Professional Cloud Services Market Trends

Hybrid Cloud is Expected to Have High Growth in the Market

- A hybrid cloud combines a public cloud provider, such as Google Cloud and Amazon Web Services, with a private cloud, i.e., designed to be used by a single organization. By allowing workloads to move between public and private clouds as computing needs and costs change, the hybrid cloud has led businesses to achieve greater flexibility and more data deployment options.

- Companies in the region are launching new products or services to gain a competitive advantage. For instance, Hewlett Packard Enterprise launched HPE GreenLake Hybrid Cloud, designed to help customers manage and optimize their on- and off-premise clouds. HPE GreenLake Hybrid Cloud provides ongoing management and optimization of customers' environments in leading cloud solutions like Microsoft Azure, AWS, and Azure Stack.

- Moreover, many organizations of different sizes are transforming from traditional to digital modes of business. This transformation creates a hybrid cloud market because of the benefits, like reduced total cost of ownership (TCO), high security, flexibility, and agility. IBM stated that 89% of IT leaders expect to move business-critical workloads to the cloud, and the growth in digitization drives all.

- The region is witnessing an upswing in hybrid on and off-premises cloud use. According to MeriTalk, research from a government news analysis organization, in 2021, 92% of federal IT managers agreed that a hybrid cloud is the best operating environment for a resilient government. In addition, more than two-thirds (67%) said that COVID-19 accelerated hybrid cloud adoption in their organizations by a year or more.

- Moreover, Cisco had predicted that by 2021, 73% of the cloud workloads and compute instances would be in public cloud data centers, up from 58% in 2016 (CAGR of 27.5% in five years).

- Furthermore, in last year, Northern Virginia had the highest data center net absorption among the leading data center markets in the United States, amounting to 303.3 megawatts. Such trends in the adoption of data centers are expected to accelerate the growth of the professional cloud services market.

United States is Anticipated to Hold the Largest Market

- The United States dominates the cloud services market. The region has been the early adaptor of cloud computing services. In addition, this region has shown its willingness to embrace cloud services technology in every sector.

- According to a report published by Stormforgein in April 2021, 18% of respondents from North America stated that their organization has a monthly cloud spend of between USD 100,000 and USD 250,000. Furthermore, 44% of respondents expected cloud spending to increase somewhat over the next 12 months, while another 32% indicated that they expected their organization's cloud spending to increase significantly over the next 12 months.

- The IT sector has already adopted this technology. The emerging sector for cloud computing services in the North American region is the healthcare sector. The technology has moved beyond data storage service, and the focus is currently on how this technology is being used to improve and personalize patient care while lowering costs.

- The primary factors for large-scale adoption are the inclination of organizations toward SaaS-based offerings and the adoption of digital business strategies. Moreover, the ongoing increase in demand for cloud services based on data integrity and privacy is further expected to increase in the study period and enable leading vendors with more opportunities to grow in the market.

North America Professional Cloud Services Industry Overview

The competitive landscape of the market is fragmented, with major players such as Cisco Systems Inc., Oracle Corporation, Atos SE, SAP SE, and Hewlett Packard Enterprise Company. The market has been experiencing several market launches due to the increasing use of on-premises and private cloud for personal and organizational purposes.

In August 2022, IBM announced its partnership with VMware to offer hybrid cloud solutions. The partnership will offer co-engineered cloud solutions aimed at helping companies in industries such as financial services, healthcare, and the public sector to reduce the cost and risk of placing mission-critical workloads in a hybrid environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Market Drivers

- 4.4 Market Restraints

- 4.5 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type of Deployment

- 5.1.1 Public

- 5.1.2 Private

- 5.1.3 Hybrid

- 5.2 By Type of Service Model

- 5.2.1 Platform-as-a-Service

- 5.2.2 Software-as-a-Service

- 5.2.3 Infrastructure-as-a-Service

- 5.3 End-user Industry

- 5.3.1 Healthcare

- 5.3.2 Retail

- 5.3.3 Entertainment and Media

- 5.3.4 Government and Public Sector

- 5.3.5 BFSI

- 5.3.6 Information and Communication Technology

- 5.3.7 Others End-user Industries

- 5.4 Country

- 5.4.1 United States

- 5.4.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Hewlett Packard Enterprise Company

- 6.1.3 Cognizant

- 6.1.4 Accenture PLC

- 6.1.5 Dell EMC

- 6.1.6 Microsoft Corporation

- 6.1.7 Fujitsu Limited

- 6.1.8 Capgemini SE

- 6.1.9 Infosys Limited

- 6.1.10 Nippon Data Systems Ltd

- 6.1.11 HCL Technologies Limited

- 6.1.12 Oracle Corporation

- 6.1.13 NTT Data

- 6.1.14 Atos SE

- 6.1.15 SAP SE