|

시장보고서

상품코드

1640665

발효 화학제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Fermentation Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

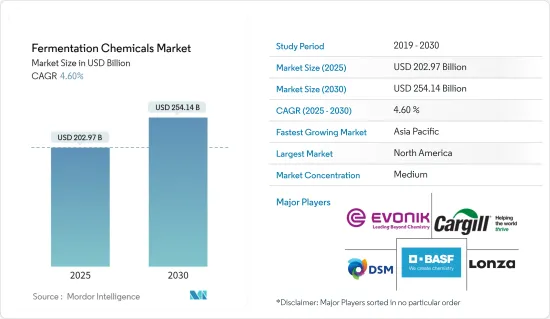

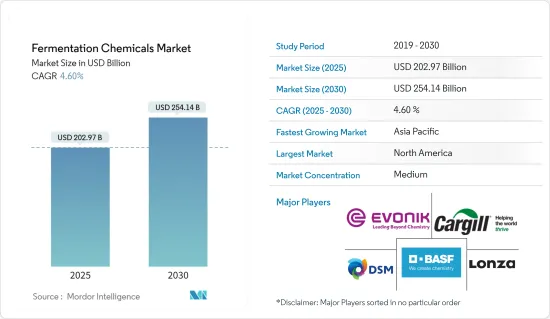

발효 화학제품 시장 규모는 2025년에 2,029억 7,000만 달러로 추정되고, 예측기간(2025-2030년)의 CAGR은 4.6%로 전망되며, 2030년에는 2,541억 4,000만 달러에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 발효 화학제품 시장에 부정적인 영향을 미쳤습니다. 그러나 2021년에는 시장이 크게 회복되었습니다.

주요 하이라이트

- 단기적으로는 메탄올과 에탄올 산업 수요 증가와 제약 산업 수요 증가가 조사 대상 시장의 성장을 가속하는 주요 요인입니다.

- 그러나 제조 공정의 복잡성으로 인한 비용 상승은 시장 성장을 억제할 가능성이 높습니다.

- 그린 케미스트리의 기회가 늘어나면 세계 시장에 유리한 성장 기회가 곧 방문할 것으로 예상됩니다.

- 북미는 발효 화학제품 시장을 독점하고 있으며, 미국, 캐나다, 멕시코 등의 국가에 의한 소비가 최대입니다.

발효 화학제품 시장 동향

시장을 독점하는 식음료 부문

- 발효는 일반적으로 미생물의 작용이 바람직하다는 것을 의미합니다. 발효는 와인, 맥주, 사이다 등의 알코올 음료를 생산합니다. 발효는 유제품 생산과 빵 팽창에도 사용됩니다.

- 발효 화학제품은 인류가 보다 안전하고 안정적이고 더 나은 식품을 생산하기 위해 사용하는 가장 오래된 생명공학이기 때문에 식품 및 식품 산업에서 높은 수요가 있습니다.

- 아시아태평양에서는 라이프 스타일 변화, 사람들의 가처분 소득, 사회인, 패스트 푸드 선호도 증가로 가공 식품에 대한 수요가 증가하고 있습니다. 소비자는 요리에 필요한 시간이 상당히 짧고 신선하고 매력적이며 견고한 포장을 포함한 조리 된 식품을 선호합니다.

- 또한 중국은 아시아 최대의 식품 시장이 될 것으로 예상되며, 인도와 동남아시아에서는 식품 지출이 가장 크게 증가하고 있습니다.

- 북미의 식품 가공 시장은 사람들의 포장 식품에 대한 과도한 의존과 식품 가공 기업의 강력한 골격에 의해 견조합니다. PepsiCo, Tyson Foods, Nestle은 이 지역에서 사업을 전개하는 주요 식품 가공 기업입니다.

- 독일은 유럽 최대의 식음료 시장으로 세계에서 가장 부유한 소비자 8,300만명 이상이 살고 있습니다. 2023년 독일 식품 시장은 2,455억 달러의 매출을 창출할 것으로 예상됩니다. 이 시장은 2023년부터 2027년까지 매년 3.64%의 성장이 전망되고 있습니다.

- OIV(국제포도 와인기구)에 따르면, 2022년 세계의 와인 생산량은 약 2억 5,800만 헥토리터였습니다.

- 또한 2022년 이탈리아는 세계 최고의 와인 생산국이었으며, 가장 많은 와인을 수출했으며, 그 양은 2,190만 헥토리터였습니다. 수출량 톱은 다른 2대 와인 생산국이었습니다. 프랑스는 1,400만 헥터, 스페인은 2,120만 헥터를 수출하고 있습니다.

- 이러한 요인이 음식 부문의 조사 시장 수요를 뒷받침하는 것으로 간주됩니다.

시장을 독점하는 북미

- 북미는 현재 세계 발효 화학제품 시장에서 가장 높은 점유율을 차지하고 있습니다.

- 미국에서는 제약 산업이 북미 시장을 크게 견인하고 있으며, 녹색 산업으로의 전환에 힘을 쏟고 있습니다.

- 북미에서는 미국이 세계 의약품 판매에 따른 수익의 최대 점유율을 차지하고 있습니다. AstraZeneca에 따르면 2024년 미국은 의약품에 6,050억-6,350억 달러를 소비할 것으로 예측되고 있습니다.

- 캐나다 의약품 시장은 세계 9위로 세계 시장 매출의 2.1%를 차지합니다. 캐나다의 의약품 부서는 정부의 직접적인 지원하에 진행되고 있습니다. 예를 들어, 2021년 8월 캐나다 정부는 당뇨병 연구에 대한 새로운 투자를 발표했습니다.

- 최근 식음료 산업은 미국에서 큰 성장을 이루고 시장 조사를 추진할 가능성이 높습니다.

- 2022년 3월 Nestle은 미국 애리조나 주 메트로피닉스에 6억 7,500만 달러를 투자하고 오토밀크 커피 크리머를 포함한 음료를 생산할 계획을 발표했습니다. 공장은 2024년에 가동될 예정입니다.

- 또한 캐나다와 멕시코에서는 제약 및 식품 및 식품 산업에서 사용되는 발효 화학제품에 대한 수요가 증가하고 있습니다.

- 따라서, 상기 요인은 예측기간 동안 북미에서 발효 화학제품 시장 수요 증가에 기여합니다.

발효 화학제품 산업 개요

세계의 발효 화학제품 시장은 부분적으로 통합되어 있습니다. 주요 진입기업은 BASF SE, Cargill, Incorporated, Evonik Industries AG, DSM, Lonza 등입니다(순부동).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 메탄올과 에탄올 산업에서의 수요 증가

- 제약산업에서의 수요 증가

- 기타 촉진요인

- 억제요인

- 제조 공정의 복잡성으로 인한 비용 상승

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

- 제품 유형별

- 알코올

- 유기산

- 효소

- 기타

- 용도별

- 공업용

- 음식

- 의약품 및 영양

- 플라스틱 및 섬유

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율(%)** 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- AB Enzymes

- Ajinomoto Co., Inc.

- ADM

- BASF SE

- Biocon

- BioVectra

- Cargill, Incorporated.

- Chr. Hansen Holding A/S

- DSM

- Evonik Industries AG

- Lonza

- MicroBiopharm Japan Co., Ltd.

- Novasep

- Novozymes

- Teva Pharmaceutical Industries Ltd.

제7장 시장 기회 및 향후 동향

- 그린 케미스트리의 성장 기회

- 기타 기회

The Fermentation Chemicals Market size is estimated at USD 202.97 billion in 2025, and is expected to reach USD 254.14 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the fermentation chemicals market. However, the market recovered significantly in 2021.

Key Highlights

- Over the short term, the growing demand from the methanol and ethanol industry and increasing demand from the pharmaceutical industry are major factors driving the studied market's growth.

- However, high costs due to the complexity involved in the manufacturing process are likely to restrain the growth of the studied market.

- Nevertheless, growing green chemistry opportunities will likely create lucrative growth opportunities for the global market soon.

- The North American region dominates the fermentation chemicals market, with the largest consumption coming from countries like the United States, Canada, and Mexico.

Fermentation Chemicals Market Trends

Food and Beverage Sector to Dominate the Market

- Fermentation usually signifies that the action of microorganisms is desirable. Fermentation produces alcoholic beverages such as wine, beer, and cider. Fermentation is also used to produce dairy products and leavening bread.

- Fermentation chemicals are highly demanded by the food and beverages industry as it is the oldest biotechnology used by human beings to produce safer, more stable, and better foodstuff.

- In the Asia-Pacific region, the demand for processed food is growing due to increasing lifestyle changes, disposable income of people, working professionals, and preferences for fast food. Consumers prefer ready-to-eat foods as these require considerably lesser time for cooking, are fresh, and include attractive and sturdy packaging.

- Also, China is expected to continue to be Asia's largest food market, and India and Southeast Asia will witness the most significant increases in food spending.

- The market for food processing in North America is robust due to the excessive dependence of people on packaged food products and the strong foothold of the food processing companies. PepsiCo, Tyson Foods, and Nestle are large food processing companies operating in the region.

- Germany is by far Europe's largest market for foods and beverages, home to more than 83 million of the world's wealthiest consumers. In 2023, the German food market is expected to generate USD 245.50 billion in revenue. The market is expected to grow annually by 3.64% between 2023 to 2027.

- According to OIV (International Organisation of Vine and Wine), global wine production in 2022 amounted to about 258 million hectoliters.

- Additionally, in 2022, Italy was the world's top wine producer and exported the most wine, amounting to 21.9 million hectoliters. The top exporters were the other two top wine producers. France exported 14 million hectoliters, while Spain exported 21.2 million.

- Such factors likely support the demand for the studied market from the food and beverages segment.

North America to Dominate the Market

- North America currently accounts for the highest global fermentation chemicals market share.

- The pharmaceutical industry highly drives the market for North America in the United States and its growing focus to turn itself into a green industry.

- In North America, the United States accounts for the largest share of the revenue generated by global pharmaceutical sales. In 2024, the United States is projected to spend between USD 605 and 635 billion on medicines, according to AstraZeneca. It will make the country achieve the highest pharmaceutical spending by far.

- Canada's pharmaceuticals market is the ninth-largest globally, with a 2.1% share of global market sales. The pharmaceutical sector in Canada is progressing under direct support from the government. For instance, in August 2021, the government of Canada announced new investments in diabetes research.

- Recently, the food & beverage industry witnessed major growth in the United States, likely to drive the market studied.

- In March 2022, Nestle announced its plans to invest USD 675 million in a new plant in Metro Phoenix, Arizona, the United States, to produce beverages, including oat milk coffee creamers, as consumer demand for plant-based products increases. The plant is expected to be operational in 2024.

- Additionally, there is an increasing demand for fermentation chemicals from Canada and Mexico for use in the pharmaceutical, food & beverage industries.

- Therefore, the abovementioned factors contribute to the increasing demand for the fermentation chemicals market in North America during the forecast period.

Fermentation Chemicals Industry Overview

The global fermentation chemicals market is partially consolidated in nature. The major players include BASF SE, Cargill, Incorporated., Evonik Industries AG, DSM, and Lonza, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Methanol and Ethanol Industry

- 4.1.2 Increasing Demand from the Pharmaceutical Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost Due to the Complexity Involved in the Manufacturing Process

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Alcohols

- 5.1.2 Organic Acids

- 5.1.3 Enzymes

- 5.1.4 Other Product Types

- 5.2 Application

- 5.2.1 Industrial

- 5.2.2 Food and Beverage

- 5.2.3 Pharmaceutical and Nutritional

- 5.2.4 Plastics and Fibers

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AB Enzymes

- 6.4.2 Ajinomoto Co., Inc.

- 6.4.3 ADM

- 6.4.4 BASF SE

- 6.4.5 Biocon

- 6.4.6 BioVectra

- 6.4.7 Cargill, Incorporated.

- 6.4.8 Chr. Hansen Holding A/S

- 6.4.9 DSM

- 6.4.10 Evonik Industries AG

- 6.4.11 Lonza

- 6.4.12 MicroBiopharm Japan Co., Ltd.

- 6.4.13 Novasep

- 6.4.14 Novozymes

- 6.4.15 Teva Pharmaceutical Industries Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Opportunities for Green Chemistry

- 7.2 Other Opportunities