|

시장보고서

상품코드

1640674

유럽의 연료전지 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Fuel Cell - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

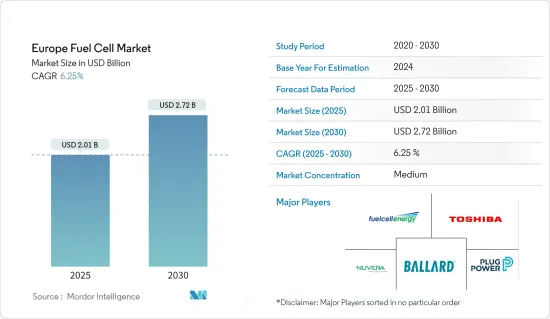

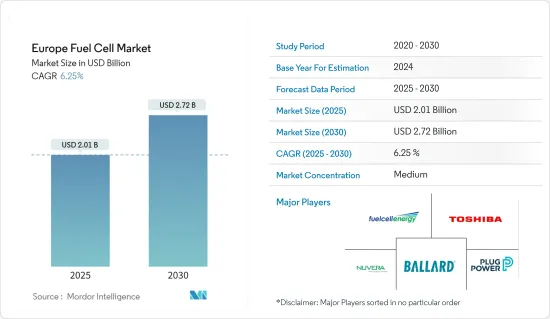

유럽의 연료전지 시장 규모는 2025년에 20억 1,000만 달러로 추정되고, 예측기간(2025-2030년)의 CAGR은 6.25%로 전망되며, 2030년에는 27억 2,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 신재생 에너지원의 적응확대와 정부의 지원시책이 예측기간 중 시장을 견인할 것으로 보입니다.

- 한편, 초기비용이 높은 것이 예측기간 동안 시장성장을 방해할 것으로 예상됩니다.

- 수소 제조와 인프라 개척에 대한 관심 증가는 유럽의 연료전지 시장에 큰 기회를 가져올 것으로 예상됩니다.

- 유럽 연료전지 시장에서는 독일이 큰 역할을 할 것으로 예상됩니다. 독일은 연료전지 기술을 추진하는 선진국이며, 그 채용을 지원하기 위해 다양한 시책과 이니셔티브를 실시했습니다.

유럽 연료전지 시장 동향

수송 산업이 시장을 독점할 것으로 예상

- 연료전지는 특히 버스, 트럭, 기차와 같은 대형 운송 용도 분야에 적합합니다. 이러한 차량은 일반적으로 에너지 수요가 높고 운전 거리가 길기 때문에 순수한 배터리 전기 솔루션으로는 어렵습니다. 연료전지는 제로 방출 운전을 실현하면서 필요한 파워와 항속 거리를 제공할 수 있습니다.

- 운수산업은 온실가스 배출의 주요 요인으로 탈탄소화에 대한 노력이 세계적으로 높아지고 있습니다. 연료전지는 내연 엔진을 대체하는 제로 방출을 제공하고 운송으로 인한 탄소 배출을 줄이는 매력적인 솔루션입니다.

- 유럽에서 연료전지 전기자동차(FCEV) 증가는 제로 방출 운송으로의 광범위한 전환의 일환으로 점차 기세를 늘려왔습니다. 국제에너지기구(IEA)에 따르면 2023년 연료전지 전기차의 총 대수는 2013년 42대에 대해 820대가 됩니다. 지난 10년간 판매량이 크게 증가하고 있으며 운송 산업에서 시장 성장 기회를 보여주고 있습니다.

- 또한 연료전지는 기존 인프라를 활용할 수 있다는 장점이 있습니다. 수소 급유 스테이션은 기존의 주유소에 통합될 수 있기 때문에 전기 충전 인프라가 보급되는 것에 비해 급유 인프라의 전개가 비교적 빠릅니다.

- 게다가 2023년 2월 유럽은 2035년부터 가솔린차와 디젤차의 신차 판매를 금지하기로 공식 결정했습니다. 세계 2위의 자동차 시장인 이 결정은 유럽 의회가 자동차 제조업체에게 새롭게 생산되는 모든 자동차로부터 CO2 배출을 완전히 제로로할 것을 의무화하는 법률을 통과한 것입니다. 이로 인해 예측 기간 동안 연료전지 전기자동차 판매가 증가할 것으로 예상됩니다.

- 따라서 이러한 신흥국 시장의 개척을 고려하면 예측기간 중에는 운수산업이 시장을 독점할 것으로 예상됩니다.

시장을 독점할 것으로 예상되는 독일

- 유럽의 연료전지 시장에서는 독일이 큰 역할을 할 것으로 예상됩니다. 독일은 연료전지 기술의 추진에 있어서 선진국이며, 그 도입을 지원하기 위해 다양한 시책과 이니셔티브를 실시해 왔습니다. 독일 정부는 수소와 연료전지의 보급에 의욕적인 목표를 설정하고, 연료전지 기술의 연구개발과 상업화에 상당한 자금을 할당하고 있습니다.

- 독일은 산업 기반이 발달하고 있으며 제조 능력도 높기 때문에 연료전지 시스템의 생산과 전개를 지원할 수 있습니다. 독일에는 유명한 연료전지 제조업체, 연구 기관 및 산업 단체가 있으며, 기술 발전과 시장 성장에 기여하고 있습니다.

- 게다가 독일의 신재생 에너지와 탈탄소화 노력은 깨끗하고 지속가능한 에너지 솔루션으로서 연료전지의 잠재력과 일치합니다. 신재생 에너지, 특히 풍력과 태양광으로의 전환은 효율적인 에너지 변환과 저장을 위해 연료전지를 통합함으로써 보완될 수 있습니다.

- 또한 독일은 수소 제조 시설과 연료 보급 스테이션을 포함한 종합적인 수소 인프라를 개발할 야심찬 계획을 가지고 있습니다. 이 인프라는 연료전지 자동차 및 기타 수소 기반 용도의 보급에 필수적입니다. 수소 인프라 개발에 대한 노력으로 독일은 연료전지 보급의 리더로서의 지위를 확립하고 있습니다.

- H2 스테이션 조직에 따르면 독일에서는 최근 수소 충전소의 수가 크게 증가하고 있습니다. 2023년에는 이 나라의 수소보급 스테이션의 총수는 2018년 52개소에 대해 91개소입니다.

- 2023년 1월에는 H2 MOBILITY Germany가 운영하는 베를린의 Tempelhofer Weg 102의 수소 충전소이 공식적으로 열렸습니다. 이 스테이션은 연료전지 트럭, 폐기물 수집 차량, 자동차, 소형 상용차 등 수소로 움직이는 자동차의 연료 보급 요구에 부응할 것으로 기대됩니다. 주목해야할 것은 Tempelhofer Weg의 수소 스테이션이 850kg 이상의 수소 저장 능력을 자랑하며 유럽에서 가장 효율적인 수소 스테이션 중 하나라는 것입니다. 이 수소 스테이션의 성공은 수도에서 수소 이동성의 발전과 확대에 매우 중요합니다.

- 따라서 이러한 점에서 예측기간 동안 독일이 시장을 독점할 것으로 예상됩니다.

유럽 연료전지 산업 개요

유럽의 연료전지 시장은 적당히 분할되어 있습니다. 이 시장의 주요 기업(순부동)으로는 Ballard Power System Inc., Toshiba Corp., Fuelcell Energy Inc., Plug Power Inc., Nuvera Fuel Cell LLC 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 서문

- 시장 규모 및 수요 예측(단위 : 달러)(-2029년)

- 최근 동향 및 개발

- 정부의 규제 및 시책

- 시장 역학

- 성장 촉진요인

- 정부의 지원 시책과 인센티브

- 신재생 에너지 통합

- 억제요인

- 높은 초기 비용

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 용도별

- 휴대용

- 거치형

- 수송용

- 연료전지 기술별

- 고체 고분자형 연료전지(PEMFC)

- 고체 산화물형 연료전지(SOFC)

- 기타 연료전지 기술

- 지역별

- 독일

- 프랑스

- 이탈리아

- 영국

- 러시아

- 노르딕

- 스페인

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 주요 기업의 전략

- 기업 프로파일

- Ballard Power System Inc.

- Toshiba Corp.

- Fuelcell Energy Inc.

- Nuvera Fuel Cells LLC

- Plug Power Inc.

- AFC Energy

- Topsoe

- Ceres Power

- SFC Energy

- Cummins Inc.

- 시장 랭킹 분석

제7장 시장 기회 및 향후 동향

- 수소 제조 및 인프라 개발

The Europe Fuel Cell Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.72 billion by 2030, at a CAGR of 6.25% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adaption of renewable energy sources and supportive government policies are expected to drive the market during the forecasted period.

- On the other hand, the high upfront cost is expected to hinder the market's growth during the forecast period.

- Nevertheless, the increasing focus on hydrogen production and infrastructure development is expected to create huge opportunities for the European fuel cell market.

- Germany is expected to play a major role in the fuel cell market in Europe. Germany has been a leading country in promoting fuel cell technology and has implemented various policies and initiatives to support its adoption.

Europe Fuel Cell Market Trends

Transportation Industry Expected to Dominate the Market

- Fuel cells are particularly suitable for heavy-duty transportation applications such as buses, trucks, and trains. These vehicles typically have higher energy demands and longer operating ranges, making them challenging for purely battery-electric solutions. Fuel cells can provide the required power and range while offering zero-emission operation.

- The transportation industry is a significant contributor to greenhouse gas emissions, and there is a growing global commitment to decarbonizing it. Fuel cells offer a zero-emission alternative to internal combustion engines, making them an attractive solution for reducing carbon emissions from transportation.

- The growth in the number of fuel cell electric vehicles (FCEVs) in Europe has gradually gained momentum as part of the broader transition to zero-emission transportation. According to the International Energy Agency, in 2023, the total number of fuel cell electric vehicles accounted for 820 units compared to 42 units in 2013. Over a decade, the sales number has increased significantly, signifying the growth opportunity for the market in the transportation industry.

- Moreover, fuel cells have the advantage of utilizing existing infrastructure. Hydrogen fueling stations can be integrated into existing gas stations, allowing for a relatively faster rollout of refueling infrastructure compared to widespread electric charging infrastructure.

- Additionally, in February 2023, Europe officially confirmed the prohibition on selling new petrol and diesel cars starting in 2035. As the world's second-largest car market, this decision follows the passing of a law by the European Parliament mandating car manufacturers to achieve complete elimination of CO2 emissions from all newly produced vehicles. This is expected to increase the sales of fuel-cell electric vehicles during the forecasted period.

- Therefore, considering such developments, the transportation industry is expected to dominate the market during the forecast period.

Germany Expected to Dominate the Market

- Germany is expected to play a major role in the European fuel cell market. Germany has been a leading country in promoting fuel cell technology and has implemented various policies and initiatives to support its adoption. The German government has set ambitious targets for hydrogen and fuel cell deployment and has allocated significant funding for research, development, and commercialization of fuel cell technologies.

- Germany has a well-developed industrial base and strong manufacturing capabilities, which can support the production and deployment of fuel cell systems. The country is home to several prominent fuel cell manufacturers, research institutions, and industry associations that contribute to technological advancements and market growth.

- Furthermore, Germany's commitment to renewable energy and decarbonization efforts aligns with the potential of fuel cells as a clean and sustainable energy solution. The country's transition to renewable energy sources, particularly wind and solar, can be complemented by integrating fuel cells for efficient energy conversion and storage.

- Additionally, Germany has ambitious plans to develop a comprehensive hydrogen infrastructure, including hydrogen production facilities and refueling stations. This infrastructure is vital for the widespread adoption of fuel-cell vehicles and other hydrogen-based applications. Germany's commitment to hydrogen infrastructure development positions it as a leader in fuel cell deployment.

- According to the H2 stations organization, the number of hydrogen refueling stations has increased significantly in Germany in recent years. In 2023, the country's total number of hydrogen refueling stations was 91 compared to 52 in 2018.

- In January 2023, the hydrogen refueling station at Tempelhofer Weg 102 in Berlin, operated by H2 MOBILITY Germany, officially opened. This station is expected to cater to the refueling needs of hydrogen-powered vehicles, including fuel cell trucks, waste collectors, cars, and light commercial vehicles. Notably, the Tempelhofer Weg station boasts over 850 kg of hydrogen storage capacity, making it one of Europe's most efficient hydrogen stations. This station's successful operation is crucial for advancing and expanding hydrogen-powered mobility in the capital city.

- Therefore, owing to such points, Germany is expected to dominate the market during the forecast period.

Europe Fuel Cell Industry Overview

The European fuel cell market is moderately fragmented. Some key players in this market (not in particular order) include Ballard Power System Inc., Toshiba Corp., Fuelcell Energy Inc., Plug Power Inc., and Nuvera Fuel Cell LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Supportive Policies and Incentives

- 4.5.1.2 Renewable Energy Integration

- 4.5.2 Restraints

- 4.5.2.1 High Initial Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Portable

- 5.1.2 Stationary

- 5.1.3 Transportation

- 5.2 Fuel Cell Technology

- 5.2.1 Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 5.2.2 Solid Oxide Fuel Cell (SOFC)

- 5.2.3 Other Fuel Cell Technologies

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 Italy

- 5.3.4 United Kingdom

- 5.3.5 Russia

- 5.3.6 NORDIC

- 5.3.7 Spain

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Ballard Power System Inc.

- 6.3.2 Toshiba Corp.

- 6.3.3 Fuelcell Energy Inc.

- 6.3.4 Nuvera Fuel Cells LLC

- 6.3.5 Plug Power Inc.

- 6.3.6 AFC Energy

- 6.3.7 Topsoe

- 6.3.8 Ceres Power

- 6.3.9 SFC Energy

- 6.3.10 Cummins Inc.

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Hydrogen Production and Infrastructure Development

샘플 요청 목록