|

시장보고서

상품코드

1641821

포대용 크래프트 종이 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Sack Kraft Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

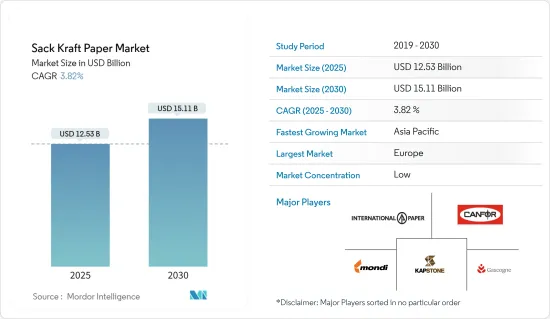

포대용 크래프트 종이 시장 규모는 2025년에 125억 3,000만 달러로 추정됩니다. 예측기간(2025-2030년)의 CAGR은 3.82%로, 2030년에는 151억 1,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 시장 확대의 주요 요인은 건축 및 건설 산업의 현저한 성장입니다. 포대용 크래프트 종이 시장 성장의 다른 주요 촉진요인은 포장 산업의 많은 지역에서 플라스틱 사용에 대한 엄격한 규제 및 금지, 포장 및 포장 용도의 개선입니다.

- 플라스틱 사용의 위험에 관한 환경보호론자와 정부의 의식이 높아짐에 따라 보다 환경친화적인 대체품에 초점을 맞추어야 하며, 포대용 크래프트 종이의 채용을 뒷받침하고 있습니다. 인프라 프로젝트는 건설 산업에 대한 수요를 꾸준히 증가시키고 포대용 크래프트 종이의 사용을 증가시키고 있습니다. 또한, 환경 친화적이고 생물분해성이 있는 포장재에 대한 수요 증가가 성장을 가속합니다. 또한 국제재활용국(BIR)에 따르면 연간 약 4억 2천만 톤의 종이 및 골판지가 생산되고 있으며, 원료의 절반 이상이 회수원에서 나온다고 합니다.

- 게다가, 플라스틱의 대체품으로서 생분해성 포장 수요를 받아들여 시장의 성장이 높아질 것으로 예상됩니다. 예를 들어 캐나다에서는 플라스틱이 강, 호수, 바다를 오염시켜 야생 생물에 해를 끼치고 물에 마이크로 플라스틱을 발생시킵니다. 보덴 라드너 제르베에 따르면 캐나다에서는 매년 300만 톤의 플라스틱 쓰레기가 버려져 있으며, 그중 재활용되고 있는 것은 9%에 불과합니다.

- 석고, 시멘트, 미립자 설탕, 점토 등 고급 종이에 필요한 분말 원료를 담은 가방도 시장 성장을 비약적으로 뒷받침합니다. 또한, 충전 시의 변형이 적기 때문에 가방의 파손이 적고, 건설(시멘트) 산업에서의 채용이 증가하고 있습니다.

- 전자상거래의 보급과 관련 개발로 공예 포장의 고급화가 진행되고 있습니다. 여기에는 짧은 배달 시간에 고품질 그래픽을 인쇄할 수 있는 공예 소재에 대한 수요도 포함됩니다. 몬디와 같은 기업은 이러한 개발에 대응하고 쇼핑백을 포함한 프리미엄으로 크리에이티브한 인쇄 및 포장 용도를 대상으로 한 신제품을 개발해왔습니다. 게다가 포대용 크래프트 종이나 종이봉지의 생산을 개선·가속해, 실시간 계산 및 종이 등급 선택과 함께 제품 보호를 강화하는 많은 혁신을 개시했습니다.

- 그러나 플라스틱 재료, 부드러운 중간 벌크 컨테이너 및 벌크 가방과 같은 대체품의 출현과 색소폰 종이의 가격 상승이 시장 성장을 방해할 수 있습니다.

- COVID-19가 발생한 후 북미, 유럽, 아시아의 많은 지역에서 불필요한 비필수 사업장의 폐쇄 및 운영 중단이 발생하여 세계 수요가 급격히 감소했기 때문에 기업은 재무적 영향을 완화하기 위해 일련의 조치를 취해야 했습니다. 여기에는 대규모 생산 축소, 자본 지출 감소, 규율적 비용 관리 이니셔티브 등이 포함됩니다. 그러나 올해 중반에는 운영 정상화, 재고 감소, 수요 증가로 인해 시장에서 활동하는 주요 업체들이 팬데믹의 영향을 완화하는 데 도움이 되었습니다. 러시아와 우크라이나 전쟁은 전 세계의 포장 생태계 전체에 영향을 받고 있습니다.

포대용 크래프트 종이 시장 동향

식품은 시장에서 큰 점유율을 차지하는 것으로 추정

- 식품 분야는 많은 최종 사용자 수직에서 석공예 종이의 대규모 사용자이며 식품 산업의 추가 요구에 동기 부여됩니다. 이는 포장식품산업이 환경친화적인 포장으로 이행하여 그 결과 포대용 크래프트 종이에 대한 수요가 증가했음을 알 수 있습니다. 예를 들어 노동통계국에 따르면 미국 가구 가정에서의 평균 식품 지출은 2021년 5,259달러에 달했습니다.

- 밀가루, 설탕, 전분, 식품 첨가물, 가공 및 건조 과일, 계란, 우유 등의 식품을 운반하려면 일반적으로 포대용 크래프트 종이를 사용합니다. 이러한 모든 요인이 입가방에 대한 수요를 높입니다. 청소년의 퀵 서비스 음식점에 대한 선호도는 포대용 크래프트 종이 수요를 충족하고 있습니다. 미국 인구조사국에 따르면 이 나라의 퀵서비스 레스토랑의 연간 매출은 2020년 3,284억 달러에서 2021년에는 3,895억 달러로 증가합니다. 매출 성장은 포대용 크래프트 종이의 확대를 지원하는 것으로 예상됩니다.

- 또한 백화점과 슈퍼마켓에서는 크래프트 종이 가방이 자주 사용됩니다. 미국 인구조사국에 따르면 슈퍼마켓 및 기타 백화점 및 식료품점의 총 매출은 2020년 7,415억 7,000만 달러에서 2021년에는 7,659억 8,000만 달러로 증가했습니다. 미국 식품 소매업을 지배하는 것은 체인 슈퍼마켓입니다. 전미에 여러 소규모 슈퍼마켓을 소유·경영하는 Walmart와 Kroger Company가 미국의 식료품 기업의 톱 2사입니다.

- 또한, 소비자의 선호도는 각 지역의 FDA에 의한 녹색 규제와 함께 식품 산업에서 포대용 크래프트 종이 포장을 촉진하고 있습니다. 유럽 종이 봉지 및 공예 종이 산업은 종이 봉지를 식품에 가장 적합한 포장으로 만드는 많은 개발에 기여해 왔습니다. PSSMA(Paper Shipping Sack Manufacturers'Association)에 따르면, 식품산업에서 사용되는 종이수송용 삭과 소비자용 가방은 연간 30억 가방 이상을 출하하는 10억 달러 규모의 산업으로 성장했습니다.

유럽이 시장에서 큰 점유율을 차지

- 포대용 크래프트 종이 수요는 총 포장비를 줄이기 위해 다양한 제품을 대량으로 운송하는 주요 포장 형태로이 지역을 견인하고 있습니다. 포대용 크래프트 종이는 주로 반려동물 식품의 대량 포장에 사용되며 반려동물 식품 수요 증가를 지원합니다.

- 게다가 영국 지역에는 생산 설비를 갖춘 석공예 종이를 제공하는 다양한 주요 세계 기업들이 존재합니다. Mondi Group과 같은 유럽 전역에서 사업을 전개하고 영국에 본사를두고 있는 기업은 밸브와 입을 열고 있는 산업용 가방에 사용되는 포대용 크래프트 종이의 갈색, 백색, PE 코트지 등급을 제공합니다. 이 지역 시장 진출 기업은 다른 부문에서 발자국의 확대에도 주력하고 있습니다. 예를 들어, 2022년 4월, Mondi Paper Bags는 이집트의 주요 시멘트 제조업체인 Lafarge Cement Egypt의 자회사인 National Bag와 Egypt Sack에서 종이봉투 라인을 인수했습니다. 인수한 생산 라인을 통해 Mondi의 생산 능력은 연간 약 1억 5,000만-1억 8,000만 봉투로 증가하고, 이집트의 종이 봉투 시장에서의 Mondi의 지위는 강화됩니다.

- 또한 제지산업연맹(CPI)에 따르면 영국 지역에는 잉글랜드, 스코틀랜드, 웨일즈, 북아일랜드 전역에서 운영하는 47개 공장이 있으며, 400만 톤의 종이를 생산하고 100만 톤을 수출하고 있습니다. 게다가 이 나라의 소비량은 1,000만톤에 육박하는 기세이며, 그 결과, 수출량도 많습니다.

- 게다가 유럽 종이봉투 사업은 예측된 시간 프레임 내에서 식품 부문의 고객 수요에 헌신적임을 보여줄 것으로 예상됩니다. 이 지역의 업자는 낙농과 코코아 산업의 문제로 이 플랫폼에 견인하고 있습니다. 주요 세계 기업은 맞춤형 포장 솔루션 수요 증가에 대응하기 위해 포대용 크래프트 종이의 R&D 사업에 폭넓게 투자하고 새로운 창고를 설치하고 있습니다.

- 게다가 지역 기업들은 사업 기회를 전략적으로 향상시키기 위해 생산 능력을 확대하기 위해 노력하고 있습니다. 다른 종이 제품을 포함한 색종이의 러시아 최고공급업체인 Mariinsky Pulp and Paper Mill은 기존의 정제 공정(2단계, 낮은 일관성)의 현대화에 투자하고 있습니다. Segezha Group도 마찬가지로 현대화에 투자하고 있으며, 2021년까지 석공예 종이 생산량을 연간 45만 톤으로 늘리고 있습니다.

포대용 크래프트 종이 산업 개요

포대용 크래프트 종이 시장은 비교적 세분화되어 있으며, 몬디, 노르딕 페이퍼, 세게자 등 시장에서 공동 패커를 버릴 수 있는 진출기업이 대량으로 존재하고 있습니다. 또한 진입기업의 유통채널과 원료가 지역시장 경쟁에 영향을 미치고 있습니다. 컨버터/포장 기업이 원료 공급업체를 인수하는 수직 통합은 지난 몇 년간의 동향입니다.

2022년 8월 : 프랑스 제지·가방 제조업체인 Gascogne은 2022-2026년까지의 설비 투자 프로그램의 자금 조달을 위해 은행 풀과 1억 2,680만 유로(1억 2,640만 달러) 상당의 신디케이트론 계약을 유럽 투자 은행(EIB)과 5,000

이 투자 프로그램은 주로 남프랑스의 미미잔 공장에 새로운 초지기를 설치하는 것을 포함합니다. Gascogne은 초지기 제조업체와 연내 매매 계약 체결을 위해 독점 협상에 들어갔다고 발표했습니다. 이 회사는 2022-2026년에 걸쳐 총액 3억 유로(2억 9,910만 달러)를 투자할 의향입니다. 투자계획의 자금을 조달하기 위해 위의 투자대출과 미래에 최소 1,000만 유로(990만 달러)의 증자 등을 포함한 자금조달 계획을 세우고 있습니다.

Gascogne에 따르면 건물과 기술 환경을 포함한 초지 기계의 설치에는 2억 2,000만 유로(2억 1,940만 달러)가 소요됩니다. 또한 기존 산업자산의 보강을 8,000만 유로(7,970만 달러)로 실시했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자/소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- COVID-19가 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 환경 친화적인 생물 분해가 가능한 포장 재료에 대한 수요 증가

- 건설산업의 급성장

- 시장의 과제

- 플라스틱 재료나 연질인 중간 벌크 용기·벌크 백 등 대체품의 출현

제6장 시장 세분화

- 포장 유형별

- 밸브 포대

- 개봉 포대

- 기타

- 등급별

- 크래프트

- 반신축성

- 신축성

- 기타

- 산업별

- 건축자재 및 시멘트

- 식품

- 화학

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 독일

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- BillerudKorsnas AB

- Mondi PLC

- Segezha Group

- Natron-Hayat doo

- Nordic Paper AS

- Gascogne Group

- KapStone Paper and Packaging Corporation(Westrock)

- Horizon Pulp & Paper Ltd.

- International Paper Company

- Canfor Corporation

제8장 투자 분석

제9장 시장의 미래

KTH 25.02.17The Sack Kraft Paper Market size is estimated at USD 12.53 billion in 2025, and is expected to reach USD 15.11 billion by 2030, at a CAGR of 3.82% during the forecast period (2025-2030).

Key Highlights

- The main factor driving the market's expansion is the building and construction industry's significant growth. Other major drivers of the sack kraft paper market growth are strict regulations and bans on plastic use in numerous regions of the packaging industry and improvements in packaging and wrapping applications.

- The growing awareness among environmentalists and governments about the hazards of using plastic is forcing them to focus on greener alternatives, favoring the adoption of sack kraft paper. Due to infrastructure projects, a steady rise in demand in the construction industry has increased the use of sack kraft paper. Also, increasing demand for eco-friendly and bio-degradable packaging material will promote growth. Additionally, according to the Bureau of International Recycling (BIR), around 420 million tonnes of paper and cardboard are produced yearly, with well over half of the raw material coming from recovered sources.

- Further, accepting the demand for biodegradable packaging as an alternative to plastic will increase market growth. For instance, in Canada, Plastic is polluting rivers, lakes, and oceans, harming wildlife, and generating microplastics in the water. Every year, Canadians throw away 3 million tons of plastic waste, only 9% of which is recycled, meaning the vast majority of plastic ends up in landfills, and about 29,000 tons find their way into the natural environment, according to Borden Ladner Gervais.

- Sacks filled with powdered materials, such as gypsum, cement, fine-grained sugar, clays, etc., which are necessary for high-quality papers, also exponentially aid market growth. The sack is also exposed to less strain during filling, leading to a lower sack breakage and increasing its adoption in the construction (cement) industry.

- The increasing popularity of e-commerce and related developments have led to the premiumization of kraft packaging. It includes the demand for kraft material that can take high-quality graphics on short print runs. Companies like Mondi have kept up with such developments and developed new products targeting premium creative print and packaging applications, including shopping bags. Moreover, players initiated many innovations that have improved and accelerated the production of sack kraft paper and paper sacks and enhanced product protection along with real-time calculations and selection of paper grade.

- However, the emergence of alternatives, such as plastic materials and flexible intermediate bulk containers and bulk bags, and the rise in the prices of sack kraft paper may hinder the market's growth.

- After the onset of COVID-19, global demand declined sharply in the wake of closures of non-essential businesses and lockdowns in many parts of North America, Europe, and Asia which pushed the companies to take a series of measures to mitigate the financial impacts. It includes extensive production curtailment, reduced capital spending, and disciplined cost management initiatives. However, by mid-year, a return to more normalized operation, lean inventories, and increased demand helped the major player operating in the market mitigate the impact of the pandemic. The overall packaging ecosystem across the globe has been impacted owing to the Russia-Ukraine war.

Sack Kraft Paper Market Trends

Food is Estimated to Have Significant Share in the Market

- The food sector is a large user of sack kraft paper among the many end-user verticals and is motivated by the additional need of the food industry. It is seen from the packaged food industry's transition to environmentally friendly packaging, which subsequently increased demand for sack kraft paper. For instance, according to the Bureau of Labor Statistics, a US household's average food at-home expenditure amounted to USD 5,259 in 2021.

- Transporting food items like flour, sugar, starch, food additives, processed or dried fruit, eggs, or milk typically involves using sack kraft paper. All of these factors are increasing the demand for open-mouth bags. Youth's preference for quick-service eateries is also meeting sack kraft paper demand. The US Census Bureau reports that from USD 328.4 billion in 2020, the country's yearly quick-service restaurant sales increased to USD 389.5 billion in 2021. Sales growth will support the expansion of sack kraft paper.

- Furthermore, department stores and supermarket stores frequently use kraft paper bags. According to the US Census Bureau, supermarkets and other departmental and grocery stores achieved total sales of USD 765.98 billion in 2021, up from USD 741.57 billion in 2020. Chain supermarkets dominate the US food retail sector. Walmart and Kroger Company, which own and run several smaller supermarkets around the country, are two top American grocery companies.

- Moreover, the consumer's preference, along with the green regulations from the FDA across the regions, also promotes sack kraft packaging in the food industry. The European paper sack and sack kraft paper industry have contributed many developments that make paper sacks the perfect packaging for food. According to Paper Shipping Sack Manufacturers' Association (PSSMA), paper shipping sacks and consumer bags used in the food industry have emerged into a billion-dollar industry with shipments of over three billion sacks annually.

Europe has Significant Share in the Market

- The demand for sack kraft paper drives the region as a primary packaging format for transporting various products in bulk to lower the total packaging expenditure. Sack kraft paper is used mainly for large quantities of pet food packaging in the region and supports the growing demand for pet food.

- Additionally, the UK region is marked by various major global key players offering sack kraft paper with production units. Companies like Mondi Group, operating throughout Europe with a significant presence and headquartered in the UK, offer brown, white, and PE-coated paper grades for sack kraft papers used in valve and open-mouth industrial bags. The market players in the region are also focusing on expanding their footprint in other areas. For instance, in April 2022, Mondi Paper Bags acquired the paper bag converting lines from National Bag and Egypt Sack, two subsidiaries of Lafarge Cement Egypt, a major cement producer in the country. The acquired production lines will increase Mondi's capacity by around 150-180 million bags annually and strengthen Mondi's position in the Egyptian paper bag market.

- Also, according to the Confederation of Paper Industries (CPI), the UK region has 47 mills operating throughout England, Scotland, Wales, and Northern Ireland, which produce 4 million tons of paper, with exports of 1 million tons. Furthermore, the country has a consumption nearing 10 million tons, which results in heavy exports of the material.

- Additionally, the European paper sack business will demonstrate its dedication to client demands in the food sector in the forecast timeframe. The regional merchants are driven to this platform by problems in the dairy and cocoa industries. Major global corporations are extensively investing in sack paper kraft R&D operations and setting up new warehouses to meet the rising demand for customized packaging solutions.

- Moreover, regional companies are involved in capacity expansion to improve their business opportunity strategically. Mariinsky Pulp and Paper Mill, a prominent Russian supplier of sack paper, including other paper products, is investing in modernizing the existing refining process (two-stage, low-consistency). Segezha Group similarly invests in modernization and has increased sack kraft paper production to 450,000 tons annually by 2021.

Sack Kraft Paper Industry Overview

The sack kraft paper market is relatively fragmented, with a large volume of players, including Mondi, Nordic Paper, and Segezha, among others, which can cut out co-packers in the market. Further, the players' distribution channels and raw materials impact the regional market competition. Vertical integration, which means raw material suppliers acquired by converters/packaging companies, has been a trend for the past couple of years.

August 2022: French paper and sacks manufacturer Gascogne signed a syndicated loan contract worth EUR 126.8 million (USD 126.4 million) with a banking pool and an agreement worth EUR 50 million (USD 49.8 million) with the European Investment Bank (EIB) to finance its Capital Expenditure program for the 2022-2026 period.

The investment program mainly includes the installation of a new paper machine at the company's Mimizan mill in Southern France. Gascogne said that it entered into exclusive negotiations with a paper machine manufacturer to finalize the purchase agreement before the end of the year. The company intends to invest a total of EUR 300 million (USD 299.1 million) in 2022-2026. To finance the investment program, it has set up a financing plan which includes the investment loans mentioned above and a future increase in capital of at least EUR 10 million (USD 9.9 million), amongst others.

According to Gascogne, the installation of the paper machine, including the building and the technical environment, will cost EUR 220 million (USD 219.4 million). In addition, the reinforcement of the existing industrial assets will be pursued for EUR 80 million (USD 79.7 million).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Eco-Friendly and Bio-degradable Packaging Material

- 5.1.2 Rapid Growth of Construction Industry

- 5.2 Market Challenges

- 5.2.1 Emergence of Alternatives such as Plastic Materials and Flexible Intermediate Bulk Containers and Bulk Bags

6 MARKET SEGMENTATION

- 6.1 By Packaging Type

- 6.1.1 Valve Sacks

- 6.1.2 Open Mouth Sacks

- 6.1.3 Other Packaging Types

- 6.2 By Grade

- 6.2.1 Kraft

- 6.2.2 Semi-extensible

- 6.2.3 Extensible

- 6.2.4 Other Grades

- 6.3 By End-user Vertical

- 6.3.1 Building Material and Cement

- 6.3.2 Food

- 6.3.3 Chemical

- 6.3.4 Other End-user Verticals

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 France

- 6.4.2.3 Germany

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.2.6 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.5 Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 BillerudKorsnas AB

- 7.1.2 Mondi PLC

- 7.1.3 Segezha Group

- 7.1.4 Natron-Hayat d.o.o

- 7.1.5 Nordic Paper AS

- 7.1.6 Gascogne Group

- 7.1.7 KapStone Paper and Packaging Corporation (Westrock)

- 7.1.8 Horizon Pulp & Paper Ltd.

- 7.1.9 International Paper Company

- 7.1.10 Canfor Corporation