|

시장보고서

상품코드

1641895

방화 재료 : 시장 점유율 분석, 산업 동향,통계, 성장 예측(2025-2030년)Fire Protection Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

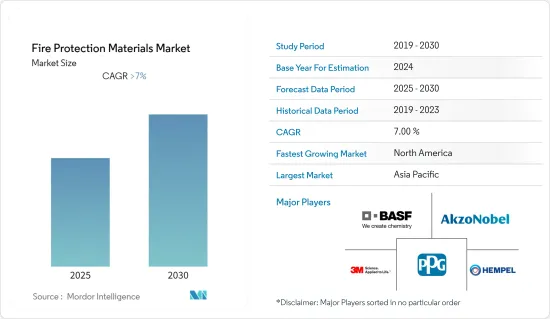

방화재료 시장은 예측기간 중에 7% 이상의 CAGR를 기록할 것으로 예상됩니다.

전 세계적으로 생산이 중단되고 대규모 건설 프로젝트가 연기됨에 따라 COVID-19는 방화재 시장에 심각한 영향을 미쳤습니다. 유행 후 건축 시장의 확대로 산업의 방화 페인트 수요가 증가할 것으로 예상됩니다.

주요 하이라이트

- 산업화의 진전과 시멘트계 도료와 발연성 도료의 사용이 시장의 성장을 가속할 것으로 예상됩니다.

- 반면에 수동적 방화제품의 기술적 과제는 조사 대상 시장의 성장을 방해할 것으로 예상됩니다.

- 예측 기간 동안 건축물이나 전기자동차에 관계없이 전기 제품의 사용 확대가 시장 성장의 기회가 될 것으로 예상됩니다.

- 방화 제품은 아시아태평양이 시장을 독점하고 있습니다. 그러나 예측기간 동안 북미가 최대 CAGR을 나타낼 것으로 예측되고 있습니다.

방화재료 시장 동향

상업용도가 시장을 독점

- 많은 사업용 건물은 안전상의 이유로 방화재료의 혜택을 누릴 수 있습니다. 상업용 건물에서는 방화 부재를 사용하여 '구획'을 확보하여 한 구역에서 발생한 화재가 다른 구역으로 퍼지지 않도록 합니다. 수동 방화재를 바닥, 천장, 지붕, 벽에 적용하여 최고의 안전 수준을 제공할 수 있습니다.

- 유럽 공공 부동산 협회에 따르면 독일, 영국, 프랑스는 최대 상업용 부동산 시장을 형성하고 있으며, 2022년 12월 현재 시장 규모는 약 4조 8,000억 달러입니다. 2022년 유럽의 상업용 부동산 점유율은 독일이 약 1조 8,000억 달러로 엄청난 비중을 차지했으며, 영국, 프랑스가 그 뒤를 이었습니다.

- 아시아태평양은 장기간 상업 부문에 대한 큰 투자를 해왔습니다. 중국국가통계국에 따르면 중국 부동산 개발업체는 2021년 연간 5,974억 위안(약 930억 달러)을 사무실 건물에 투자했지만 전년 대비 약 520억 위안(약 80억 달러) 감소했습니다. 또한 India Brand Equity Foundation(IBEF)도 이 보고서에서 2022년 2분기에 인도 부동산 부문에 총 7억 400만 달러가 투자되었다고 말했습니다.

- 또한 몇몇 중요한 기업들이 상업 건설 부문에 대한 투자를 활발하게 했습니다. 예를 들어 2025년 만국박람회는 오사카에서 개최될 예정입니다. 자연재해로부터의 부흥과 재개발이 건설의 주요 힘이 되고 있습니다. 37층 높이 230m의 오피스 초고층 빌딩과 61층 높이 390m의 오피스 타워는 각각 2021년과 2027년에 완성이 예정되어 있는 도쿄역의 고층 타워입니다.

- 또한 2021년 4분기에 착공해 2025년 4분기에 완성할 예정인 영국 런던의 토브라론 믹스 유스 타워 프로젝트입니다. 이 6억 6,200만 달러의 프로젝트는 1993년에 건설된 보건부 사무실, 노숙자를 위한 키워스 스트리트 호스텔, 런던 사우스뱅크 대학의 페리 도서관, 스킵턴 하우스를 변화시킬 것으로 예상됩니다.

- 중동에서는 사우디아라비아 비전 2030과 아부다비 경제 비전 2030 등 상업 부문 개발을 강화하기 위한 몇 가지 정부 이니셔티브가 있으며 방화재료 소비 촉진에 크게 기여할 것으로 보입니다.

- 전세계 여러 상업용 부동산 건설 프로젝트가 진행 중이며, 그 결과 안전성을 목적으로 하는 방화재료 시장 수요가 증가할 것으로 예상됩니다.

북미가 가장 빠른 성장을 확인

- 북미는 건설 산업의 발판으로 인해 방화재료 시장을 가장 많이 지배하는 지역으로 간주됩니다. 미국은 760만 명 이상의 직원을 보유한 거대한 건설 부문을 자랑합니다. 미국의 건설 부문은 상업, 공업, 시설, 주택, 인프라 건설에 중요한 역할을 하며, 이 나라의 경제에 크게 기여하고 있습니다.

- 미국 인구조사국에 따르면 미국은 2022년 12월 건설 관련 비용으로 1조 8,098억 달러를 지출했습니다. 2022년 12월과 2021년 12월 사이에 건설 부문은 약 7.7% 증가했으며, 총 지출 총액은 1조 6,810억 달러였습니다. 이후 방화재료 시장은 이 혜택을 받게 됩니다.

- 2022년 12월 현재 상업부문의 계절조정 완료 공사 총액은 약 1,290억 달러로 전년 동기 대비 20% 증가했습니다.

- 경제분석국에 따르면 2022년 1-3분기 부동산업 전체의 계절조정이 끝난 연간 부가가치는 6조 달러에 가까웠습니다. 2022년 3분기는 부동산 부문이 창출한 전체 가치에 약 2조 9,000억 달러가 기여했습니다.

- 미국 건축가 협회에 따르면 미국의 비주택 건축물 건설 전체는 2022년 3.1%까지 성장할 것으로 예상됩니다. 호텔 건설은 2022년 8.8%, 사무실 건설은 0.1% 증가할 것으로 전망됩니다.

- 캐나다에서도 캐나다 통계국에 따르면 2022년 8월 건축허가액은 전체적으로 11.9% 증가한 125억 달러에 달했습니다. 주택건설 의향은 12.0% 증가했고 비주택건설 의향은 11.8% 증가했습니다. 그 때문에 방화 재료에 대한 국민의 요구가 높아지고 있다

- 위의 모든 요인은 북미 시장 성장을 가속할 것으로 간주됩니다.

방화 재료 산업 개요

방화재료 시장은 상위 부분이 부분적으로 통합되어 있습니다. 일부 진출기업(특정 순서가 아님)에는 3M, BASF SE, AkzoNobel NV, PPG Industries, Inc, Hempel A/S가 포함됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 산업화의 진전과 시멘트계 도료와 침투성 도료의 사용 증가

- 기타 촉진요인

- 시장 성장 억제요인

- 패시브 방화 제품의 기술적 과제

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

- 특허 분석

제5장 시장 세분화(금액 베이스 시장 규모)

- 재료 유형

- 코팅제

- 실란트와 필러

- 박격포

- 시트/보드

- 스프레이

- 퍼티

- 예비 성형품

- 기타 재료(카본 폼 등)

- 용도

- 상업

- 산업/시설

- 주택용

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 네덜란드

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 중동 및 아프리카의 나머지 지역

- 아시아태평양

제6장 경쟁 구도

- Vendor Tier Analysis

- 주요 기업의 전략

- 기업 프로파일

- 3M

- AkzoNobel NV

- BASF SE

- Contego International Inc.

- Etex Group

- Fire Protection Coatings Ltd

- Hempel A/S

- Hilti Group

- Isolatek International

- Morgan Advanced Materials

- PPG Industries Inc.

- RectorSeal

- Sika AG

- The Sherwin-Williams Company

- Tremco CPG Inc.

- USG Corporation

- WR Grace & Co.-Conn.

제7장 시장 기회와 앞으로의 동향

- 빌딩 및 전기자동차에서 전기 제품의 사용 확대

The Fire Protection Materials Market is expected to register a CAGR of greater than 7% during the forecast period.

Due to the production suspension and large construction project postponement all over the world, COVID-19 had a severe effect on the fire protection material market. Nevertheless, the industry's demand for fire protective coatings is anticipated to increase with the expanding building market following the pandemic.

Key Highlights

- Increased industrialization and the use of cementitious and intumescent coatings are expected to enhance the market growth.

- On the flip side, the technical challenges of passive fire protection products are expected to hinder the studied market's growth.

- During the projected period, it is anticipated that the growing use of electrical products, whether in buildings or electric vehicles, will provide an opportunity for market growth.

- Asia-Pacific region dominated the market for fire protection products. However, North America is anticipated to register the greatest CAGR during the forecast period.

Fire Protection Materials Market Trends

Commercial Application to dominate the market

- Many business structures can benefit from fire protection materials for safety reasons. Commercial buildings use fire protection elements to preserve "compartmentation," ensuring that a fire in one area won't spread to another. Passive fire prevention materials can be applied to floors, ceilings, roofs, and walls to offer the best safety level.

- According to the European Public Real Estate Association, Germany, the United Kingdom, and France includes the largest commercial real estate markets, worth approximately USD 4.8 trillion as of December 2022. Germany had an enormous share value of commercial real estate in Europe in 2022, with a total value of approximately USD 1.8 trillion, followed by the United Kingdom and France.

- The Asia-Pacific region witnessed significant investments in the commercial sector for a long time. According to the National Bureau of Statistics of China, real estate developers in China invested CNY 597.4 billion (~USD 93 billion) in office buildings across the whole year of 2021, a drop of around CNY 52 billion (~USD 8 billion) compared to the previous year. Moreover, the Indian Brand Equity Foundation (IBEF) also stated in its report that a total of USD 704 million had been invested in the real estate sector in India in the second quarter of 2022.

- Several significant businesses also boosted their investments in the commercial construction sector. For instance, the 2025 World Expo will be held in Osaka. Recovery from natural calamities and redevelopment are the main forces behind the construction. A 37-story, 230m-tall office skyscraper and a 61-story, 390m-tall office tower are two high-rise towers for Tokyo Stations expected to be finished in 2021 and 2027, respectively.

- Also starting in the fourth quarter of 2021 and scheduled to be finished in the fourth quarter of 2025 is the Toblerone Mixed-Use Towers project in London, United Kingdom. The USD 662 million projects is anticipated to transform the 1993-built Department of Health offices, Keyworth Street Hostel for the Homeless, Perry Library at London South Bank University, and Skipton House.

- In the Middle East, several government initiatives to bolster commercial sector development, such as Saudi Arabia Vision 2030 and Abu Dhabi Economic Vision 2030, are likely to substantially contribute to driving fire protection material consumption.

- Several other commercial real estate construction projects are underway all across the globe, which would, in turn, increase the demand for fire protection materials in the market for safety purposes.

North America to Witness the Fastest Growth

- North America is considered the most dominating fire protection materials market region, owing to its foothold in the construction industry. The United States boasts a colossal construction sector with over 7.6 million employees. The United States construction sector significantly contributes to the country's economy by playing a prominent role in commercial, industrial, institutional, residential, and infrastructure construction.

- According to the US Census Bureau, the United States spent USD 1,809.8 billion on construction-related costs in December 2022. The construction sector increased by about 7.7% between December 2022 and December 2021, when the total amount spent was USD 1,681.0 billion. The market for fire protection materials would subsequently be benefited from this.

- As of December 2022, the total construction value put in place according to the seasonally adjusted rate in the commercial sector was about USD 129 billion, 20% more than the previous year's value for the same period.

- According to the Bureau of Economic Analysis, the value added at the seasonally adjusted annual rates by the overall real estate industry in the first three quarters of 2022 was close to USD 6 trillion. The third quarter of 2022 contributed around USD 2.9 trillion to the overall value created by the real estate sector.

- According to the American Institute of Architects, overall non-residential building construction in the United States is expected to grow to 3.1% in 2022. The construction of hotels is expected to rise by 8.8% in 2022, and office spaces by 0.1%.

- Even in Canada, the overall value of building permits grew by 11.9% to USD 12.5 billion in August 2022, according to Statistics Canada. Residential construction intentions increased by 12.0%, while non-residential construction intentions increased by 11.8%. It is, hence raising the nation's need for fire protection materials.

- All the abovementioned factors will likely drive market growth in the North American region.

Fire Protection Materials Industry Overview

The fire protection materials market is partially consolidated at the top. Some players (not in any particular order) include 3M, BASF SE, AkzoNobel N.V., PPG Industries, Inc, and Hempel A/S.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increased Industrialization and Increased Use of Cementitious and Intumescent Coatings

- 4.1.2 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Technical Challenges of Passive Fire Protection Products

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Patent Analysis

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Coatings

- 5.1.2 Sealants and Fillers

- 5.1.3 Mortar

- 5.1.4 Sheets/Boards

- 5.1.5 Sprays

- 5.1.6 Putty

- 5.1.7 Preformed Devices

- 5.1.8 Other Material Types (Carbon Foam, etc.)

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Industrial/Institutional

- 5.2.3 Residential

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Netherlands

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Tier Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 3M

- 6.3.2 AkzoNobel N.V.

- 6.3.3 BASF SE

- 6.3.4 Contego International Inc.

- 6.3.5 Etex Group

- 6.3.6 Fire Protection Coatings Ltd

- 6.3.7 Hempel A/S

- 6.3.8 Hilti Group

- 6.3.9 Isolatek International

- 6.3.10 Morgan Advanced Materials

- 6.3.11 PPG Industries Inc.

- 6.3.12 RectorSeal

- 6.3.13 Sika AG

- 6.3.14 The Sherwin-Williams Company

- 6.3.15 Tremco CPG Inc.

- 6.3.16 USG Corporation

- 6.3.17 W. R. Grace & Co.-Conn.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Use of Electric Products in Buildings and Electric Vehicles