|

시장보고서

상품코드

1641947

원심 펌프 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Centrifugal Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

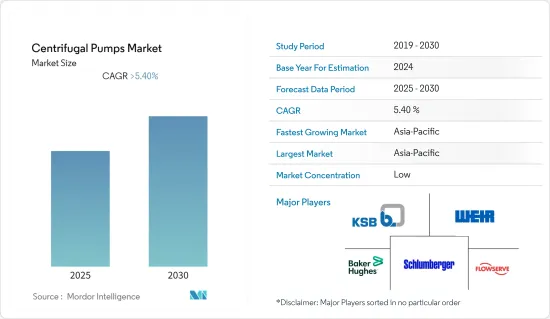

원심 펌프 시장은 예측 기간 동안 5.4% 이상의 연평균 성장률을 기록할 것으로 예상됩니다.

COVID-19는 공급망에 문제를 일으켜 원심 펌프 시장에 타격을 주었지만 시장은 2022년에 회복되었습니다.

주요 하이라이트

- 원심 펌프 수요는 북미나 아프리카 등에 있어서의 해양 심해유,가스전의 탐사·생산 증가 등에 의해 견인될 가능성이 높습니다.

- 그러나 원유,가스 가격의 변동은 E&P 기업의 비용 절감과 프로젝트 지연으로 원심 펌프 시장에 영향을 미칠 것으로 보입니다.

- 예측 기간 동안 심해와 초심해 탐사를 가능하게 하는 신기술은 석유 생산을 증가시키고 시장 성장 기회를 창출할 것으로 예상됩니다.

- 예측 기간 동안 아시아태평양이 가장 큰 급성장 지역이 될 것으로 예상됩니다. 이는 이 지역의 산업 인프라 성장으로 이어진 거대한 경제 성장 때문입니다.

원심 펌프 시장 동향

석유 및 가스 부문이 시장을 독점

- 원심 펌프는 석유 및 가스 부문에서 석유 및 석유 제품, 액화 가스 및 기타 유체를 이송하는 데 사용됩니다. 석유 및 가스 인프라 개발의 급증은 예측 기간 동안 원심 펌프 시장에 큰 추진력을 줄 것으로 예상됩니다.

- BP Statistical Review of World Energy 2022에 따르면 세계 천연가스 생산량은 2021년에 약 4조369억 입방미터(bcm)에 달하고, 2020년 3,861.5bcm에서 4.5% 증가했으며 2015년보다는 약 15% 증가했습니다. 마찬가지로 세계 천연가스 수요는 2021년 약 4,037.5bcm로 2019년 3,845.6bcm에서 5% 증가했으며 2015년부터 약 16% 증가했습니다. 천연가스 생산 및 소비 증가는 원심 펌프의 세계 수요를 촉진할 것으로 예상됩니다.

- 2023년 1월, Ebara Pumps는 인라인 3E 원심 펌프의 새로운 모델을 출시했습니다. 이 펌프는 주철 케이스를 갖추고 있으며 2극 또는 4극 모터와 통합형 E-SPD 주파수 컨버터를 사용할 수 있습니다. 또한, 3E형은 임펠러를 모터 샤프트에 직접 스플라인 접속한 클로즈 커플링 구조, 3ES형은 임펠러를 모터에 리지드 커플링으로 스플라인 접속한 클로즈 커플링 구조의 펌프와 표준 모터의 접속을 기재하고 있습니다.

- 2023년 2월 CPC Pumps International은 새로운 BB5 펌프를 발표하고 제품 범위를 확대했습니다. CPC 원심 펌프의 용도는 전통적으로 널리 정제 및 석유 화학 산업입니다. BB5는 CO2 배출량 저감의 중심이 되는 탄소 회수·이용·저장(CCUS) 프로세스에 사용됩니다.

- 2020년 1월에 시행되는 국제 해양기구(IMO)의 2020년 규제는 저황 연료 수요를 증가 시켰으며, 주요 정유소는 저황 연료를 생산하기 위해 기존 인프라를 업그레이드할 필요가 있다고 예상되었습니다. 정유소의 리노베이션이 예상됨에 따라 원심 펌프 수요는 향후 몇 년동안 증가 할 가능성이 높습니다.

- 이러한 점에서 예측기간 중에는 석유 및 가스 부문이 원심펌프 시장을 독점할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

- 아시아태평양 산업 인프라는 비즈니스 친화적인 조치로 성장을 목표로합니다. 대부분의 아시아태평양 국가들은 성장 단계에 있으며 높은 인구 증가율에 따라 물 공급에 대한 요구가 높아지고 있다

- 2023-2028년에 걸쳐 아시아태평양의 원유 정제는 중국이 큰 성장을 차지할 것으로 예상되고 있습니다. 2021년 현재 중국의 석유 정제 능력은 일량 1,690만 배럴에 이르고 있습니다.

- 이 지역의 원유 소비량은 2011-2021년에 걸쳐 4.8% 성장했으며, 2021년에는 세계 소비량의 약 16.41%를 차지했습니다. 인구 증가와 산업화는 소비 성장을 지원합니다. 원유 운송에 사용되는 원심 펌프 수요는 지난 몇 년동안 크게 증가하고 있습니다.

- 2022년 1월, 케랄라 주 수도국은 알루바에서 하루에 1억 4,200만 리터(MLD)의 처리 능력을 가진 수처리 플랜트를 건설하기 시작했습니다. 이 정수장의 건설비는 18억 루피로 2024년까지 완공될 예정입니다. 따라서 이러한 미래의 수처리 프로젝트는 예측 기간 동안 원심 펌프 수요를 증가시킬 가능성이 높습니다.

- 또한 유엔대학교 물환경보건연구소에 따르면 2021년 싱가포르, 아랍에미리트(UAE), 카타르, 중국 등 고소득국가에서는 발생한 공업폐수와 도시폐수의 약 74%를 처리하고 있으며, 이 비율은 고중소득국가에서는 43%, 저중소득국에서는 약 26%로 떨어졌습니다. 환경에 대한 인식이 높아지고 물 부족이 심각해짐에 따라 아시아태평양의 개발도상국에서는 수처리 플랜트, 그리고 수처리 플랜트용 원심 펌프 수요가 증가할 것으로 예상됩니다.

- 따라서 가솔린, 난방유, 액화석유 및 가스 등의 석유제품에 대한 수요는 인구 증가와 급속한 도시화에 따라 매일 증가하고 있습니다. 그러므로 기존 수요를 충족시키기 위해서는 새로운 정유소를 설립해야 하며, 이는 예측 기간 동안 아시아태평양 원심 펌프 시장을 견인할 것으로 예상됩니다.

원심 펌프 산업 개요

원심 펌프 시장은 분할되어 있습니다. 이 시장의 주요 기업(특정 순서 없음)은 Flowserve Corporation, Schlumberger Ltd, Baker Hughes Company, KSB SE & Co.KGaA, Weir Group PLC 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2028년까지 시장 규모와 수요 예측(단위: 10억 달러)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 억제요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 단

- 단단 펌프

- 다단 펌프

- 최종 사용자

- 석유 및 가스

- 발전

- 기타

- 임펠러 유형

- 개방형

- 부분 개방형

- 밀폐형

- 지역

- 북미

- 유럽

- 아시아태평양

- 남미

- 중동 및 아프리카

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Baker Hughes Company

- Dover Corporation

- Ebara Corporation

- Flowserve Corporation

- ITT Inc.

- KSB SE & Co. KGaA

- Ruhrpumpen Group

- Schlumberger Ltd.

- Sulzer Ltd

- Weir Group PLC

제7장 시장 기회와 앞으로의 동향

SHW 25.02.19The Centrifugal Pumps Market is expected to register a CAGR of greater than 5.4% during the forecast period.

COVID-19 caused problems in the supply chain, which hurt the market for centrifugal pumps.However, the market rebounded in 2022.

Key Highlights

- Demand for centrifugal pumps is likely to be driven by things like increased exploration and production in offshore deep-water oil and gas fields in places like North America and Africa.

- However, volatile crude oil and gas prices are likely to affect the centrifugal pump market due to cost-cutting and delayed projects by the E&P companies.

- During the forecast period, new technologies that make deep-water and ultra-deep-water explorations possible are expected to increase oil production and create opportunities for market growth.

- During the forecast period, Asia-Pacific is expected to be the biggest and fastest-growing region. This is because of the huge economic growth that has led to the growth of industrial infrastructure in the region.

Centrifugal Pumps Market Trends

Oil and Gas Segment to Dominate the Market

- Centrifugal pumps are used in the oil and gas sector to pump oil and petroleum products, liquefied gases, and other fluids during operations. The surge in oil and gas infrastructure development is expected to provide a huge thrust to the centrifugal pump market during the forecast period.

- According to the BP Statistical Review of World Energy 2022, the total global natural production reached around 4,036.9 billion cubic meters (bcm) in 2021, recording a 4.5% rise from the 3,861.5 bcm recorded in 2020 and around a 15% increase from 2015. Similarly, global natural gas demand stood at around 40,37.5 bcm in 2021, witnessing a 5% rise from 3845.6 bcm in 2019 and around a 16% rise from 2015. The increasing production and consumption of natural gas are expected to drive the global demand for centrifugal pumps.

- In January 2023, Ebara Pumps launched a new in-line 3E centrifugal pump model. The pumps are equipped with cast iron casing and are available with two or four-pole motors as well as an integrated E-SPD+ frequency converter. Additionally, the 3E model features close-coupled construction with the impeller directly splined to the motor shaft while the 3ES model offers a close-coupled construction connection of the pump with standard motor with the impeller splined to the motor by a rigid coupling.

- In February 2023, the CPC Pumps International extended its product range by launching its new BB5 pump. Applications for CPC centrifugal pumps are traditionally in the wider refining and petrochemical industries. The BB5 will be used in carbon capture, utilization and storage (CCUS) processes that are central to lowering CO2 emissions.

- With the IMO 2020 International (Maritime Organization) regulation implemented in January 2020, the increasing demand for low sulfur fuel was anticipated to force major refiners to upgrade the existing infrastructure in order to produce low sulfur fuels. With refineries expected to be revamped, the demand for centrifugal pumps is likely to increase over the next few years.

- Owing to the above points, the oil and gas segment is expected to dominate the centrifugal pumps market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region's industrial infrastructure is witnessing growth due to business-friendly policies. Most Asian-Pacific countries are in a growing phase, and the high population growth rate has led to an increased requirement for water supply.

- China is expected to account for the major growth in Asia-Pacific crude oil refining between 2023 and 2028. As of 2021, China's oil refinery capacity amounted to 16.9 million barrels per day.

- Crude oil consumption in the region grew at 4.8% between 2011-2021 and accounted for around 16.41% of global consumption in 2021. Increasing population and industrialization have supported the growth in consumption. Demand for centrifugal pumps, which are used to transport crude oil, has increased significantly in the past few years.

- In January 2022, Kerala Water Authority started the construction of a water treatment plant at Aluva with a treatment capacity of 142 million liters per day (MLD). The plant is likely to cost INR 180 crore and is expected to be completed by 2024. Thus, such upcoming water treatment projects are likely to increase demand for centrifugal pumps during the forecast period.

- Moreover, according to the United Nations University Institute of Water, Environment, and Health, in 2021, high-income countries such as Singapore, UAE, Qatar, and China treated about 74% of the industrial and municipal wastewater they generated, and this ratio dropped to 43% in upper-middle-income countries and about 26% in lower-middle-income countries. With increasing awareness about the environment and growing water shortage, the demand for water treatment plants, and in turn, centrifugal pumps in water treatment plants are expected to increase in the developing countries of Asia-Pacific.

- Hence, the demand for oil products such as gasoline, heating oil, and liquefied petroleum gas is increasing day-to-day with a growing population and rapid urbanization. Therefore, to meet the existing demand, there is a need to set up new refineries, which, in turn, is expected to drive the centrifugal pump market in the Asia-Pacific region during the forecast period.

Centrifugal Pumps Industry Overview

The centrifugal pump market is fragmented. Some key players in this market (not in particular order) are Flowserve Corporation, Schlumberger Ltd, Baker Hughes Company, KSB SE & Co. KGaA, and Weir Group PLC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Stage

- 5.1.1 Single-stage Pumps

- 5.1.2 Multi-stage Pumps

- 5.2 End-User

- 5.2.1 Oil and Gas

- 5.2.2 Power Generation

- 5.2.3 Other End-Users

- 5.3 Impeller Type

- 5.3.1 Open

- 5.3.2 Partially Open

- 5.3.3 Enclosed

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Baker Hughes Company

- 6.3.2 Dover Corporation

- 6.3.3 Ebara Corporation

- 6.3.4 Flowserve Corporation

- 6.3.5 ITT Inc.

- 6.3.6 KSB SE & Co. KGaA

- 6.3.7 Ruhrpumpen Group

- 6.3.8 Schlumberger Ltd.

- 6.3.9 Sulzer Ltd

- 6.3.10 Weir Group PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

샘플 요청 목록