|

시장보고서

상품코드

1852103

커패시터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Capacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

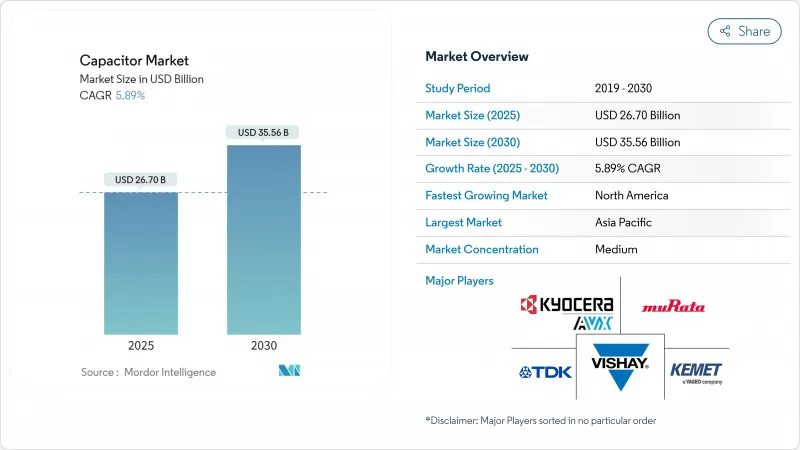

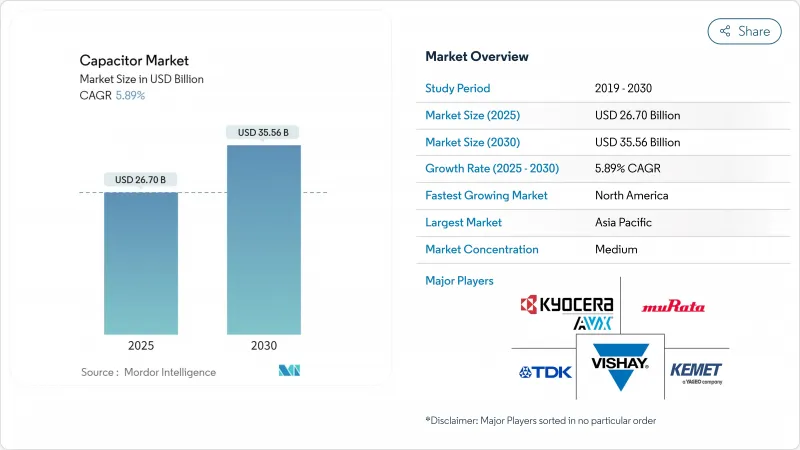

커패시터 시장 규모는 2025년에 267억 달러, 2030년에는 355억 6,000만 달러에 이르고, CAGR 5.89%를 나타낼 것으로 예측됩니다.

쇠약한 전기자동차의 보급, 분산 에너지 자원, 5G의 고밀도화는 업계의 성장 전망을 지원하는 내구성이 뛰어난 3기둥 드라이버 세트를 형성합니다. 세라믹 MLCC는 넓은 온도 범위에 걸친 신뢰성으로 설계 소켓의 이점을 유지하면서 슈퍼커패시터는 전력 회사가 하이브리드 스토리지 토폴로지를 시도하기 때문에 가장 빠른 수익 증가를 기록합니다. 인공지능 데이터센터 노드에 대한 설비투자가 활발해짐으로써 초저ESR·고리플전류 커패시터에 대한 수요가 더욱 높아져 기존 스마트폰의 계절성에서 수량이 효과적으로 분리됩니다. 현지 생산에 대한 병행 투자는 지정학적 리스크를 줄이고, 특히 북미의 전기 이동성 신흥 기업들 사이에서 새로운 가격 탄력적 수요 포켓을 창출합니다. 정책 입안자의 조달 인센티브는 세액 공제와 교환하여 공급망 지역화에 의욕적인 기업의 수익 가시성을 강화합니다.

세계의 커패시터 시장 동향과 인사이트

EV 파워 일렉트로닉스 채용 확대

2024년 전기차 생산 대수는 전년 대비 25% 증가한 1,730만대에 달했고, 트랙션 인버터용 고전압 필름 커패시터 수요 증가에 직결합니다. 각 배터리 전기자동차에는 기존의 연소 모델의 4배인 1만 5,000개 이상의 MLCC가 탑재되어 있으며, 800V 프리미엄 드라이브 트레인에는 정격 전압과 열 안정성이 강화된 디바이스가 필요합니다. AEC-Q200 규격에 합격한 커패시터 공급자는 소비자용 일렉트로닉스의 난고하로부터 몸을 지키기 위해, 다년간에 걸친 설계의 성공을 거두고 있습니다. TDK의 3225 케이스 크기 100V, 10µF MLCC는 제품 로드맵이 실적를 확장하지 않고 성능 엔벨로프를 확장하는 방법을 보여줍니다. 그 결과 자동차 1대당 평균 판매가격이 구조적으로 상승하여 전동화와 커패시터 시장 사이의 양의 플라이휠이 강화됩니다.

급속한 5G/FTTx 전개가 고주파 MLCC 수요를 견인

애널리스트는 2029년까지 전 세계 모바일 데이터의 75%가 5G 인프라를 통과할 것으로 예측됩니다. Massive-MIMO 안테나 어레이는 6GHz 이상의 주파수에서 초저유전 손실을 가진 커패시터를 필요로 하는데, 이는 종래의 세라믹 블렌딩에서 충족하기 어려운 사양입니다. 삼성전기는 원래 통신기지국용으로 개발된 노하우를 커넥티드 차량 플랫폼용으로 활용해 차량용 MLCC 매출 1조원을 목표로 하고 있습니다. 무라타 제작소의 006003인치 MLCC는 기존 제품보다 75% 소형화되어 전기적 성능 지표를 유지하면서 지속적인 소형화 경쟁을 구현하고 있습니다. 각 기지국의 무선 보드에는 수만 개의 커패시터가 탑재되어 있으며, 5G의 전개가 증가 경향이 있기 때문에 커패시터 시장은 세계의 대역폭 소비 동향과 긴밀하게 연동하고 있습니다.

고용량 세라믹 MLCC 공급망 불안정성

티타네이트 바륨의 부족으로 차재 등급 MLCC의 리드 타임은 2024년 6개월을 넘어 중국이 전구체 가공을 독점했기 때문에 지리적 집중 위험이 부각되었습니다. AEC-Q200 규격에 적합한 커패시터의 수율은 여전히 70%를 밑돌고 있으며, 공급이 박박할 때마다 자동차용과 전기통신용 고객간에 배분쟁쟁이 발생합니다. 유전체 층의 박막화를 가능하게 하는 장치의 업그레이드는 층 두께가 물리적 한계에 가까워짐에 따라 초고순도 원료를 필요로 하므로 제약을 악화시킵니다. 구미 제조업체는 생산 능력 확대를 발표하고 있지만, 새로운 공장이 인정을 받기 위해서는 최대 2년이 걸리므로 당분간 공급 불균형이 장기화됩니다.

부문 분석

세라믹 커패시터는 2024년 커패시터 시장 점유율의 42.3%를 차지하고 체적 효율과 견고한 온도 내성의 균형으로 대체 유전체가 틈새 발판을 얻는 가운데 수익의 주도권을 유지했습니다. 이 부문의 기세는 무라타 제작소가 풋 프린트를 75% 삭감했음에도 불구하고 정전 용량을 유지하는 006003인치 MLCC를 릴리스 한 것으로 실증된 바와 같이, 끊임없는 층수 증가와 세밀도 제어로부터 발생하고 있습니다. 향후 성장은 고온에서의 마이그레이션을 방지하면서 은 팔라듐의 비용 노출을 줄이는 니켈 장벽 종단의 채용에 달려 있습니다.

슈퍼/울트라 커패시터는 고전압 리튬 팩과 탄소 기반 파워 버퍼를 결합한 하이브리드 버스 라인에 밀어 넣어 모든 유형에서 가장 빠른 CAGR 7.5%를 나타낼 전망입니다. 탄탈 부품은 체적 효율성과 비용 절감을 상쇄하는 의료용 임플란트 및 아비오닉스 모듈에서 관련성을 유지하지만, 광석 조달로 인해 가격 변동이 커집니다. 알루미늄 전해 커패시터는 서지 전류 능력이 내구성 우려를 능가하는 고전압 전원 소켓을 유지합니다. 폴리프로필렌 필름은 신재생에너지 컨버터로 늘어나지만 PTFE 기반은 PFAS 관련 단계적 감소 의무에 직면합니다.

저전압 장비(<=100 V) delivered 49.1% of 2024 revenue, anchored by smartphones, wearables, and infotainment consoles. 6.4%로 가속될 것으로 예측되며, 이들과 함께 송전 컨디셔닝에 특화된 커패시터 시장 규모를 확대하고 있습니다. 중전압 부품(100V-1kV)은 로봇 공학과 공장 자동화의 개수가 효율 향상을 위해 DC 버스 레벨이 높은 것으로 이행하고 있기 때문에 꾸준히 성장하고 있습니다.

설계자들은 와이드 밴드갭 반도체 스위치의 링잉을 억제하기 위해 세라믹과 필름 기술을 결합한 임피던스 제어의 고전압 스택을 점점 더 요구하고 있습니다. 하이브리드 모듈을 지원하는 공급업체는 프리미엄 가격을 획득하여 높은 리플 전류와 부분 방전 저항을 모두 수용할 수 있는 솔루션에 가치가 있음을 보여줍니다. 그 결과 제품 차별화가 진행되고 수량이 증가해도 가격 하락은 완만합니다.

지역 분석

아시아태평양은 중국, 일본, 한국의 수직 통합형 공급망으로 2024년 세계 매출의 46.7%를 차지했습니다. 성숙한 세라믹 분말 소성, 자동화된 MLCC 소결, 전자 OEM 클러스터에 대한 근접성은 스케일 이점을 제공하여 이 지역의 기준선 생산에 대한 지배력을 강화하고 있습니다. 일본의 벤더는 미세화 특허를 활용해 인건비 할증에도 불구하고 높은 평균 판매 가격을 확보하고, 한국의 벤더는 AEC-Q200의 열충격 제한을 충족하는 차재 등급의 로트에 특화하고 있습니다.

북미는 2030년까지 연평균 복합 성장률(CAGR)이 7.4%를 나타낼 것으로 예측되며, 이는 주요 지역에서 가장 빠릅니다. CHIPS 및 과학법에 근거한 연방 정부의 우대 조치는 웨이퍼 팹 투자에 인접한 수동 부품의 리쇼어링을 장려하고, 새로운 EV 조립 공장은 클린 자동차 세액 공제를 해제하기 위해 현지 조달을 이용합니다. 또한 데이터센터 사업자는 AI 가속기가 보드 레벨 용량 예산을 약 25% 증가시키고 고신뢰성 세라믹 및 폴리머 알루미늄 디바이스의 수년에 걸쳐 급등을 유지하기 위해 수요를 높이고 있습니다.

유럽에서는 견조한 산업 자동화 수요와 재료 선택을 바꾸는 규제의 역풍과의 균형이 잡혀 있습니다. PFAS의 단계적 폐지로 인해 폴리프로필렌과 폴리에틸렌 나프탈레이트 필름에 대한 대체가 급속히 진행되고 있는 반면, 배터리 규칙 2023/1542는 폐쇄 루프 재활용을 문서화할 수 있는 공급업체를 우월하게 하는 확대 생산자 책임 규칙을 도입하고 있습니다. 남미와 중동 및 아프리카의 신흥 시장은 신재생에너지 경매와 통신망의 확장으로 일시적인 상승을 보이지만 인프라 격차로 절대량은 적습니다. 전반적으로 지리적 다양화는 단일 지역의 충격을 완화하고 커패시터 시장의 장기적인 확장을 촉진합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EV 파워 일렉트로닉스의 채용 확대

- 급속한 5G/FTTx 전개가 고주파 MLCC 수요를 견인

- 그리드 규모의 축전지 도입

- 자동차 존 E/E 아키텍처

- 초저 ESR 캡이 필요한 에너지 수확 IoT 노드

- 시장 성장 억제요인

- 고용량 세라믹 MLCC 공급 체인의 변동성

- 고체 울트라커패시터에 관한 기술적 노하우의 갭

- PTFE 필름에 대한 PFAS 단계적 폐지 압력 커패시터 시장

- 탄탈 광석의 원료비 상승

- 거시경제 요인의 영향

- 업계 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 분석

제5장 시장 규모와 성장 예측

- 유형별

- 세라믹 커패시터

- 탄탈 커패시터

- 알루미늄 전해 커패시터

- 필름 커패시터

- 슈퍼/울트라 커패시터

- 전압 범위별

- 저전압(100V 이하)

- 중전압(100V-1kV)

- 고전압(1kV 이상)

- 장착 방식별

- 표면 실장

- 관통 홀

- 최종 사용자 업계별

- 자동차

- 산업

- 에너지 및 전력

- 통신/서버/데이터 저장

- 소비자 가전

- 항공우주 및 방위

- 의료기기

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- KYOCERA AVX Components Corporation

- KEMET(Yageo Group)

- Vishay Intertechnology, Inc.

- Panasonic Holdings Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Walsin Technology Corporation

- Nippon Chemi-Con Corporation

- Rubycon Corporation

- Nichicon Corporation

- Cornell Dubilier Electronics, Inc.

- EPCOS AG(Infineon Technologies)

- Eaton Corporation plc(xEV capacitors)

- Maxwell Technologies, Inc.(UCAP)

- Skeleton Technologies Group OU

- LS Materials Co., Ltd.

- WIMA GmbH & Co KG

- Wurth Elektronik eiSos GmbH & Co KG

- Illinois Capacitor(Cornell Dubilier)

- Cap-XX Limited

- Lelon Electronics Corporation

- Samwha Electric Co., Ltd.

- Faratronic Co., Ltd.

- Elna Co., Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.25The capacitor market size stands at USD 26.7 billion in 2025 and is forecast to achieve USD 35.56 billion in 2030, advancing at a 5.89% CAGR.

Unabated electric-vehicle adoption, distributed-energy resources, and 5G densification form a durable three-pronged driver set that underpins the industry's growth outlook. Ceramic MLCCs retain design-socket dominance because of reliability across wide temperature ranges, whereas supercapacitors post the fastest revenue gains as utilities trial hybrid storage topologies. Heightened capital expenditure in artificial-intelligence data-center nodes further amplifies demand for ultra-low-ESR and high-ripple-current capacitors, effectively decoupling volumes from legacy smartphone seasonality. Parallel investments in localized production mitigate geopolitical risk and create new price-elastic demand pockets, especially among North American electric-mobility startups. Policymakers' procurement incentives strengthen the revenue visibility of companies willing to regionalize supply chains in exchange for tax credits.

Global Capacitor Market Trends and Insights

Growing Adoption of EV Power-Electronics

Electric-vehicle output rose to 17.3 million units in 2024, a 25% year-on-year surge that translates directly into higher demand for high-voltage film capacitors in traction inverters. Each battery-electric car now integrates more than 15,000 MLCCs, quadrupling the baseline content found in traditional combustion models, while premium 800 V drivetrains require devices with enhanced voltage ratings and thermal stability. Capacitor suppliers able to pass AEC-Q200 qualifications enjoy multi-year design wins that shield them from consumer-electronics volatility. TDK's 100 V, 10 µF MLCC in the 3225 case size exemplifies how product roadmaps stretch performance envelopes without enlarging footprint. The result is a structural uplift in average selling price per vehicle, reinforcing the positive flywheel between electrification and the capacitor market.

Rapid 5G/FTTx Roll-Outs Driving High-Frequency MLCC Demand

More than 300 network operators will activate commercial 5G service by late 2024, and analysts forecast that 75% of global mobile data will traverse 5G infrastructure by 2029.Massive-MIMO antenna arrays require capacitors with ultra-low dielectric loss at frequencies above 6 GHz, a specification that legacy ceramic formulations struggle to meet. Samsung Electro-Mechanics, therefore, targets KRW 1 trillion in automotive MLCC revenue, leveraging know-how originally developed for telecommunication base stations to serve connected-vehicle platforms. Murata's 006003-inch MLCC, 75% smaller than its predecessor, embodies the perpetual miniaturization race while safeguarding electrical performance metrics. With each base-station radio board hosting tens of thousands of capacitors, the upward trajectory of 5G deployments ensures that the capacitor market remains tightly coupled to global bandwidth-consumption trends.

Volatility in MLCC Supply Chain for High-Capacitance Ceramics

Barium titanate shortages pushed lead times for automotive-grade MLCCs beyond six months in 2024, underlining geographic concentration risks because China dominates precursor processing. Yield rates for capacitors that meet AEC-Q200 standards remain below 70%, creating allocation battles between automotive and telecom customers whenever supply tightens. Equipment upgrades that enable thinner dielectric layers exacerbate constraints by requiring ultrapure raw materials as layer thickness nears physical limits. Western manufacturers have announced capacity expansions, yet fresh factories need up to two years to qualify, prolonging near-term supply imbalances.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Scale Battery Storage Deployment

- Automotive Zonal E/E Architectures

- Technical Know-How Gap for Solid-State Ultracapacitors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceramic capacitors captured 42.3% of the capacitor market share in 2024 by balancing volumetric efficiency with rugged temperature tolerance, maintaining revenue leadership even as alternative dielectrics gain niche footholds. The segment's momentum stems from relentless layer-count increases and finer-grain control, as demonstrated by Murata's release of a 006003-inch MLCC that maintains capacitance despite a 75% footprint reduction. Future growth hinges on incorporating nickel-barrier terminations that reduce silver-palladium cost exposure while preventing migration at high temperatures.

Super-/ultracapacitors register a 7.5% CAGR, the fastest across all types, propelled by hybrid bus lines that pair high-voltage lithium packs with carbon-based power buffers. Tantalum parts sustain relevance in medical implants and avionics modules where volumetric efficiency offsets cost premiums, though ore sourcing adds price volatility. Aluminum electrolytics retain high-voltage power-supply sockets where surge current capability trumps endurance concerns. Film capacitors experience bifurcated demand: polypropylene films grow in renewable-energy converters, whereas PTFE-based variants face PFAS-related phase-down mandates.

Low-voltage devices (<=100 V) delivered 49.1% of 2024 revenue, anchored by smartphones, wearables, and infotainment consoles. Yet the high-voltage class (>1 kV) is projected to accelerate at a 6.4% CAGR as 800 V battery-electric vehicles and series-capacitor banks proliferate; together they are expanding the capacitor market size devoted to power-transmission conditioning. Medium-voltage parts (100 V-1 kV) grow steadily because robotics and factory-automation retrofits migrate to higher DC-bus levels for efficiency gains.

Designers increasingly demand impedance-controlled, high-voltage stacks that combine ceramic and film technologies to tame ringing in wide-band-gap semiconductor switches. Suppliers responding with hybrid modules capture premium pricing, demonstrating that value accrues to solutions able to handle both high ripple current and partial-discharge endurance. The resulting product differentiation keeps price erosion modest even as unit volumes rise.

The Capacitor Market Report is Segmented by Type (Ceramic, Tantalum, and More), Voltage Range (Low <=100 V, Medium 100 V-1 KV, High - Above 1 KV), Mounting Style (Surface-Mount, and Through-Hole), End-User Industry (Automotive, Industrial, Energy and Power, Consumer Electronics, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 46.7% of 2024 worldwide revenue thanks to vertically integrated supply chains in China, Japan, and South Korea. Mature ceramic-powder calcination, automated MLCC sintering, and proximity to electronics OEM clusters provide scale economies that reinforce the region's grip on baseline production. Japanese vendors leverage miniaturization patents to secure higher average selling prices despite labor-cost premiums, while South Korean lines specialize in automotive-grade lots that satisfy AEC-Q200 thermal-shock limits.

North America is forecast to record a 7.4% CAGR through 2030, the fastest across major regions. Federal incentives under the CHIPS and Science Act encourage passive-component reshoring adjacent to wafer-fab investments, and new EV assembly plants use localized sourcing to unlock clean-vehicle tax credits. Data-center operators also raise demand as AI accelerators inflate board-level capacitance budgets by about 25%, sustaining a multi-year uplift for high-reliability ceramic and polymer-aluminum devices.

Europe balances steady industrial-automation demand with regulatory headwinds that reshape material choices. PFAS phase-outs compel rapid substitution toward polypropylene and polyethylene naphthalate films, while Battery Regulation 2023/1542 introduces extended-producer-responsibility rules that favor suppliers able to document closed-loop recycling. Emerging markets in South America and the Middle East & Africa add episodic upside via renewable-energy auctions and telecom network expansions, yet infrastructure gaps keep absolute volumes small. Altogether, geographic diversification mitigates single-region shocks and reinforces long-run expansion for the capacitor market.

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- KYOCERA AVX Components Corporation

- KEMET (Yageo Group)

- Vishay Intertechnology, Inc.

- Panasonic Holdings Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Walsin Technology Corporation

- Nippon Chemi-Con Corporation

- Rubycon Corporation

- Nichicon Corporation

- Cornell Dubilier Electronics, Inc.

- EPCOS AG (Infineon Technologies)

- Eaton Corporation plc (xEV capacitors)

- Maxwell Technologies, Inc. (UCAP)

- Skeleton Technologies Group OU

- LS Materials Co., Ltd.

- WIMA GmbH & Co KG

- Wurth Elektronik eiSos GmbH & Co KG

- Illinois Capacitor (Cornell Dubilier)

- Cap-XX Limited

- Lelon Electronics Corporation

- Samwha Electric Co., Ltd.

- Faratronic Co., Ltd.

- Elna Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of EV power-electronics

- 4.2.2 Rapid 5G/FTTx roll-outs driving high-frequency MLCC demand

- 4.2.3 Grid-scale battery storage deployment

- 4.2.4 Automotive zonal E/E architectures

- 4.2.5 Energy harvesting IoT nodes needing ultra-low-ESR caps

- 4.3 Market Restraints

- 4.3.1 Volatility in MLCC supply chain for high-capacitance ceramics

- 4.3.2 Technical know-how gap for solid-state ultracapacitor

- 4.3.3 PFAS phase-out pressure on PTFE film capacitor

- 4.3.4 Rising raw-material cost of tantalum ore

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Ceramic Capacitor

- 5.1.2 Tantalum Capacitor

- 5.1.3 Aluminum Electrolytic Capacitor

- 5.1.4 Film Capacitor

- 5.1.5 Super-/Ultra Capacitor

- 5.2 By Voltage Range

- 5.2.1 Low Voltage (<=100 V)

- 5.2.2 Medium Voltage (100 V-1 kV)

- 5.2.3 High Voltage (Above 1 kV)

- 5.3 By Mounting Style

- 5.3.1 Surface-Mount

- 5.3.2 Through-Hole

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Industrial

- 5.4.3 Energy and Power

- 5.4.4 Communications / Servers / Data Storage

- 5.4.5 Consumer Electronics

- 5.4.6 Aerospace and Defense

- 5.4.7 Medical Devices

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 TDK Corporation

- 6.4.3 KYOCERA AVX Components Corporation

- 6.4.4 KEMET (Yageo Group)

- 6.4.5 Vishay Intertechnology, Inc.

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Samsung Electro-Mechanics Co., Ltd.

- 6.4.8 Taiyo Yuden Co., Ltd.

- 6.4.9 Walsin Technology Corporation

- 6.4.10 Nippon Chemi-Con Corporation

- 6.4.11 Rubycon Corporation

- 6.4.12 Nichicon Corporation

- 6.4.13 Cornell Dubilier Electronics, Inc.

- 6.4.14 EPCOS AG (Infineon Technologies)

- 6.4.15 Eaton Corporation plc (xEV capacitors)

- 6.4.16 Maxwell Technologies, Inc. (UCAP)

- 6.4.17 Skeleton Technologies Group OU

- 6.4.18 LS Materials Co., Ltd.

- 6.4.19 WIMA GmbH & Co KG

- 6.4.20 Wurth Elektronik eiSos GmbH & Co KG

- 6.4.21 Illinois Capacitor (Cornell Dubilier)

- 6.4.22 Cap-XX Limited

- 6.4.23 Lelon Electronics Corporation

- 6.4.24 Samwha Electric Co., Ltd.

- 6.4.25 Faratronic Co., Ltd.

- 6.4.26 Elna Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment