|

시장보고서

상품코드

1851101

컨테이너 보안 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Container Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

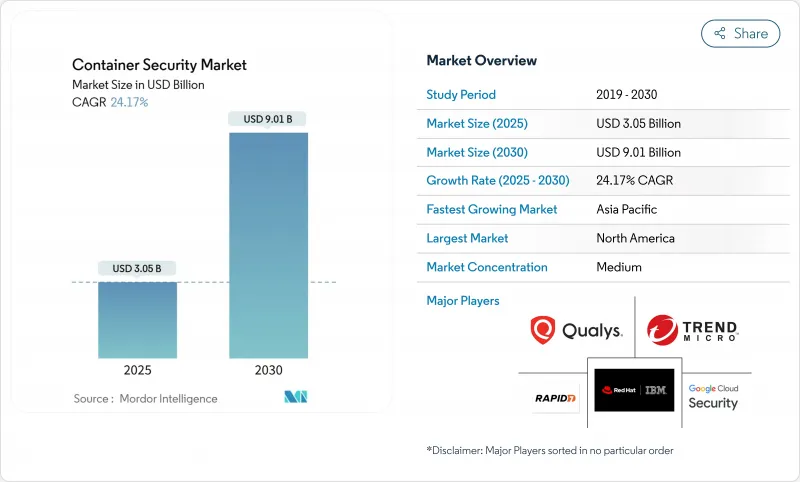

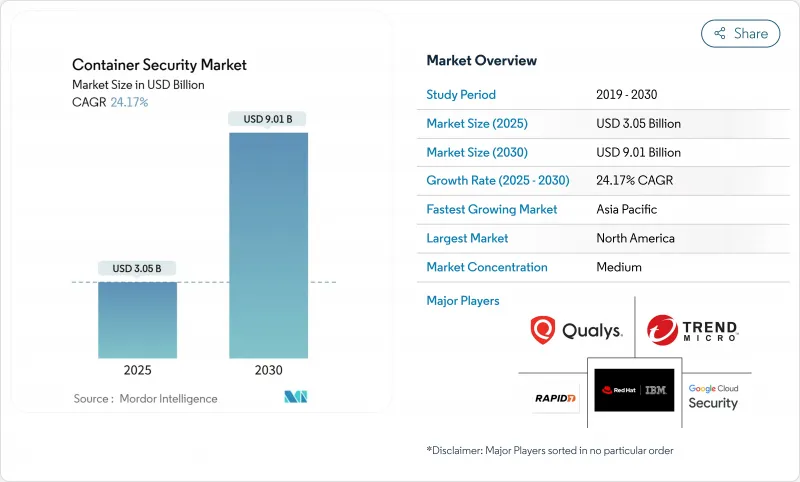

컨테이너 보안 시장 규모는 2025년에 30억 5,000만 달러로 추정되고, 2030년에는 90억 1,000만 달러로 확대될 것으로 예측됩니다.

끊임없는 성장은 모놀리식 소프트웨어에서 여러 클라우드 및 엣지 사이트에 걸쳐 클라우드 네이티브 컨테이너화 아키텍처로의 전환을 반영합니다. 조직은 현재 전통적인 경계 방어가 아니라 애플리케이션과 함께 이동하는 제로 트러스트, 워크로드 중심의 제어를 선호하고 있습니다. 아시아태평양 기업의 53%는 이미 컨테이너를 운영하고 있으며 클라우드 간에 일관성 없는 보안 태세가 중요한 워크로드를 노출하고 있음을 인식하고 있기 때문에 수요가 더욱 가속화되고 있습니다. 또한 PCI-DSS 4.0, NIS2, 소프트웨어 부품표(SBOM) 공개 등 법규에 대한 관심이 높아짐에 따라 컨테이너 보안은 재량적 투자에서 컴플라이언스의 필수 조건으로 변화하고 있습니다. 이와 병행하여 5G나 엣지 플랫폼의 급속한 전개는 컨테이너화된 네트워크 기능을 도입하여 새로운 공격 대상을 만들어 특별한 런타임 세이프 가드가 필요합니다. 지속적인 벤처 기업의 자금 조달과 기록적인 규모 인수는 2025년 3월 구글이 320억 달러로 Wiz를 인수한 것으로 대표되는 클라우드 네이티브 보호의 전략적 역할을 강조합니다.

세계의 컨테이너 보안 시장 동향 및 인사이트

하이브리드 및 멀티 클라우드 컨테이너 워크로드 채택 증가

기업은 비용과 내결함성을 최적화하기 위해 둘 이상의 퍼블릭 클라우드에서 워크로드를 동시에 운영하고 있지만 보안 관리, API 및 규정 준수 의무에 일관성이 없기 때문에 가시성 격차가 위험을 증가시키고 있습니다. ABN AMRO와 같은 금융기관은 여러 클라우드에 걸친 HashiCorp Vault에서 비밀을 중앙 집중화하고 플랫폼에 맞지 않는 제어가 전개 옵션을 유지하면서 정책을 통일한다는 것을 입증합니다. 보안 공급업체는 현재 모든 클러스터를 검색하고 정책을 표준화하며 규정 준수 증거 수집을 자동화하는 오케스트레이션 계층을 제공합니다. 멀티클라우드의 복잡성이 격리된 도구의 장점을 뛰어넘기 때문에 통합 대시보드 및 에이전트 없는 검색에 대한 수요가 계속 증가하고 있습니다.

마이크로서비스 및 DevSecOps 파이프라인으로의 빠른 이동

대규모 애플리케이션을 수백 개의 느슨하게 결합된 서비스로 분할하면 릴리스 속도가 향상되지만 지속적인 통합 및 지속적인 전개 흐름 전체에 보안 검사가 삽입됩니다. 소매업체인 Target은 Unimatrix 플랫폼을 통해 매주 수백 개의 업데이트를 전개하면서 자동 스캔 및 정책 게이트를 통합하여 취약한 이미지가 프로덕션 환경에 도달하는 것을 방지합니다. 보안 플랫폼은 일반적인 CI/CD 도구의 네이티브 플러그인을 게시하고, 정책 애즈코드 템플릿을 활성화하며, 실행하기 전에 구성 오류를 자동 수정하도록 되어 있습니다.

DevOps 팀에서 컨테이너 보안 기술 세트 부족

Kubernetes에 익숙한 보안 엔지니어 수요는 공급을 능가하고 있으며, 특히 신흥국에서는 대학이 아직 전문 커리큘럼을 전개하고 있지 않습니다. 회사는 직원의 학습 곡선이 프로젝트를 지연시키기 때문에 전개 사이클이 길어질 것이라고 보고합니다. 공급업체는 현재 처방 정책 템플릿, AI 채팅 도우미 및 관리형 검색 서비스를 번들로 전문 지식의 격차를 줄이고 있지만 인력 부족은 계속 전개 속도를 낮추고 있습니다.

부문 분석

2024년 매출의 72.1%를 소프트웨어가 차지하고, 오케스트레이션 레이어에 직접 내장된 자동 스캔, 정책 엔진, 런타임 감지에 대한 수요가 부각되었습니다. 그러나 많은 기업들이 아키텍처 설계, 파이프라인 통합, 24시간 365일 모니터링을 수행하기 위해 외부 전문가를 필요로 하기 때문에 전문 서비스 및 관리 서비스 CAGR은 24.7%로 성장하고 있습니다. 컨설팅 계약은 일반적으로 전체 하이브리드 에스테이트의 비밀 관리, 네트워크 마이크로 세분화 및 컴플라이언스 매핑을 지원합니다.

서비스의 물결은 고객이 사내에 직원을 배치할 수 없는 관리 업무를 전문가 파트너에게 맡겨 플랫폼의 소비를 증폭시킵니다. Kubernetes, 컨테이너 레지스트리 및 서비스 메쉬를 다루는 관리형 검색 서비스는 리소스 제한 팀을 완화하고 컨테이너 보안 시장으로의 침투를 촉진합니다. 또한 이 동향은 프로덕션 워크로드를 투입하기 전에 문서화된 운용 런북을 요구하는 규제 산업에서의 대응 가능한 저변을 넓혀줍니다.

대기업은 대규모 IT 자산과 풀 스택 보호를 요구하는 규제 의무로 2024년 65.6%의 점유율을 유지했습니다. 이러한 고객은 정책 애즈코드, 자동화된 컴플라이언스 증거, 딥 패킷 검사를 마이크로서비스 워크플로우에 직접 통합하여 성숙한 보안 시스템을 반영합니다.

중견 및 중소기업은 소비 기반 가격 설정으로 복잡성을 은폐하고 간소화된 클라우드 제공 제품으로 CAGR 25.3%로 확대하고 있습니다. 공급업체는 현재 스캔, 비밀 회전 및 기본 런타임 가드 레일을 단일 대시보드로 번들로 제공하고 있으며 중소기업은 전담 SOC 직원이 없어도 컨테이너를 도입할 수 있습니다. 카스퍼스키의 컨테이너 보안과 같은 솔루션은 거버넌스를 유지하면서 지리적 확장을 추구하는 분산 팀에 대응하고 자원에 제한이 있는 조직에서 컨테이너 보안 시장의 침투를 확대합니다.

지역 분석

북미는 Kubernetes의 조기 도입, 높은 사이버 성숙도, 연방 정부의 제로 트러스트 지령의 혜택을 받아 2024년 매출이 28.9%를 차지했습니다. Google의 Wiz 인수와 같은 획기적인 거래는 컨테이너 보호를 보다 광범위한 클라우드 플랫폼에 긴밀하게 통합하기 위한 지속적인 통합을 제안합니다. 금융 서비스, 방위 및 기술 업계는 FIPS 호환 암호화 및 다중 클러스터 페더레이션과 같은 기능을 계속 형성하고 있습니다.

아시아태평양은 CAGR 24.3%에서 가장 빠르게 확대되고 있습니다. 디지털 이니셔티브, 정부의 클라우드 정책 지원, 개발자 커뮤니티의 확대로 컨테이너 전개가 가속화되고 있으며, 이 지역 기업의 53%가 이미 프로덕션 가동 중입니다. 통신 사업자는 5G 에지 노드를 활용하고 제조 기업은 스마트 팩토리의 청사진을 채택하는 것이이 지역의 성장에 매우 중요합니다. 사이버 인시던트 증가는 위협 인텔리전스의 자동 피드 및 관리형 감지 서비스에 대한 지출을 뒷받침하고 있습니다.

유럽은 엄격한 데이터 보호법을 배경으로 큰 점유율을 유지하고 있습니다. NIS2 지침은 약 350,000개의 조직에 컨테이너 오케스트레이션 방위를 강화하고, 거버넌스에 중점을 둔 통제 및 지속적인 컴플라이언스 감사 수요를 높이고 있습니다. 금융기관은 다중 클라우드 민첩성과 프라이버시 의무를 조화시키기 위해 HashiCorp Vault와 같은 중앙 집중화된 비밀 관리 도구에 의존합니다. 이러한 역학은 대륙 전체에서 컨테이너 보안 시장의 꾸준한 확장을 보장합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이브리드 및 멀티클라우드 컨테이너 워크로드 채용 증가

- 마이크로서비스 및 DevSecOps 파이프라인으로의 급속한 시프트

- 보안 의무화(PCI-DSS 4.0, NIS2, SBOM 등)

- 컨테이너 이미지에 대한 공급망 공격의 빈도 상승

- 엣지 및 5G 컨테이너 런타임의 보급

- 하드웨어 레벨 컨테이너 격리 혁신

- 시장 성장 억제요인

- DevOps 팀의 컨테이너 보안 기술 세트 부족

- 멀티클라우드, 멀티클러스터 에스테이트의 운영 복잡성

- 경고 피로 및 위양성 과다

- 고급 컨테이너 이스케이프 킬 체인

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 플랫폼 및 소프트웨어

- 서비스

- 기업 규모별

- 대기업

- 중소기업

- 전개별

- 클라우드 기반

- 온프레미스

- 보안 및 컨트롤별

- 이미지 스캔 및 취약성 관리

- 런타임 보호 및 이상 감지

- 컴플라이언스 및 구성 관리

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 소매 및 전자상거래

- 헬스케어 및 생명과학

- 공업 및 제조업

- 기타(미디어, 교육, 정부 기관)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Google Cloud Security

- Red Hat(IBM)

- Trend Micro

- Qualys

- Rapid7

- Suse NeuVector

- Mirantis

- Thales

- Sysdig

- Anchore

- Prisma Cloud by Palo Alto

- Tenable

- AccuKnox

- Tigera

- VMware(NSX-ALB)

- Microsoft Defender for Containers

- Capsule8(Snowflake)

- Fidelis Cybersecurity

제7장 시장 기회 및 향후 전망

AJY 25.11.12The container security market size is estimated at USD 3.05 billion in 2025 and is projected to advance to USD 9.01 billion by 2030, registering a steep 24.17% CAGR.

Unrelenting growth mirrors the migration from monolithic software to cloud-native, containerized architectures that sit across multiple clouds and edge sites . Organizations now favor zero-trust, workload-centric controls that travel with applications rather than traditional perimeter defenses. Demand further accelerates because 53% of Asia-Pacific enterprises already run containers in production and recognize that inconsistent security postures across clouds expose critical workloads . Heightened regulatory attention-covering PCI-DSS 4.0, NIS2 and software bill of materials (SBOM) disclosure-has turned container security from a discretionary investment into a compliance prerequisite cisco.com. In parallel, the rapid rollout of 5G and edge platforms introduces containerized network functions that create new attack surfaces and require specialized run-time safeguards redhat.com. Sustained venture funding and record-size acquisitions underscore the strategic role of cloud-native protection, exemplified by Google's USD 32 billion purchase of Wiz in March 2025.

Global Container Security Market Trends and Insights

Rising adoption of hybrid and multi-cloud container workloads

Enterprises simultaneously operate workloads on two or more public clouds to optimize cost and resilience, yet inconsistent security controls, APIs and compliance obligations create visibility gaps that heighten risk. Financial institutions such as ABN AMRO centralize secrets with HashiCorp Vault across multiple clouds, demonstrating how platform-agnostic controls unify policies while preserving deployment choice. Security vendors now ship orchestration layers that discover every cluster, standardize policy and automate compliance evidence collection. Demand for unified dashboards and agentless discovery continues rising as multi-cloud complexity outweighs the benefits of isolated tools.

Rapid shift toward microservices and DevSecOps pipelines

Breaking large applications into hundreds of loosely coupled services improves release velocity but inserts security checks throughout continuous integration and continuous deployment flows. Forty-two percent of organizations reported advanced DevSecOps adoption in 2024, and another 48% were in early stages.Retailer Target deploys hundreds of updates weekly through its Unimatrix platform while embedding automated scanning and policy gates that prevent vulnerable images from reaching production. Security platforms increasingly expose native plugins for popular CI/CD tools, enable policy-as-code templates and auto-remediate misconfigurations before runtime.

Shortage of container-security skillsets in DevOps teams

Demand for Kubernetes-savvy security engineers exceeds supply, particularly in emerging economies where universities have yet to roll out specialized curricula. Enterprises report longer deployment cycles as staff learning curves delay projects. Vendors now bundle prescriptive policy templates, AI chat assistants and managed detection services to narrow the expertise gap, but talent scarcity continues to dampen roll-out velocity.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory security mandates (PCI-DSS 4.0, NIS2, SBOM)

- Rising frequency of supply-chain attacks on container images

- Operational complexity of multi-cloud and multi-cluster estates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 72.1% of 2024 revenue, underscoring demand for automated scanning, policy engines and run-time detection built directly into orchestration layers. Professional and managed services, however, are growing at 24.7% CAGR because many enterprises need external specialists to design architectures, integrate pipelines and run 24/7 monitoring. Consulting engagements typically address secrets management, network micro-segmentation and compliance mapping across hybrid estates.

The services wave amplifies platform consumption as clients lean on expert partners to operate controls they cannot staff internally. Managed detection offerings covering Kubernetes, container registries and service meshes relieve resource-constrained teams, advancing broader penetration of the container security market. This trend also widens the addressable base among regulated industries that seek documented operational runbooks before committing production workloads.

Large enterprises retained 65.6% share in 2024 by virtue of sizable IT estates and regulatory obligations that demand full-stack protections. These customers embed policy-as-code, automated compliance evidence and deep packet inspection directly into microservice workflows, reflecting mature security postures.

Small and medium enterprises are expanding at 25.3% CAGR thanks to simplified, cloud-delivered offerings that mask complexity behind consumption-based pricing. Vendor bundles now bake scanning, secrets rotation and basic run-time guardrails into single dashboards, allowing SMEs to deploy containers without dedicated SOC staff. Solutions such as Kaspersky Container Security cater to distributed teams pursuing geographic expansion while maintaining governance, a dynamic that broadens container security market penetration among resource-constrained organizations.

Container Security Market Report is Segmented by Component (Platform/Software and Services), Organization Size (Large Enterprise, Small and Medium Enterprises), Deployment (Cloud, On Premise), Security Control (Image Scanning and Vulnerability Management, and More), End User Industry (IT and Telecom, BFSI, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 28.9% revenue in 2024, benefiting from early Kubernetes adoption, high cyber-maturity and federal zero-trust directives. Landmark transactions such as Google's acquisition of Wiz signal ongoing consolidation aimed at integrating container protection tightly into broader cloud platforms. Financial services, defense and technology verticals continue to shape features such as FIPS-compliant cryptography and multi-cluster federation.

Asia-Pacific is the fastest expanding region at a 24.3% CAGR. Digital initiatives, supportive government cloud policies and a swelling developer community place container rollouts on an accelerated curve, with 53% of regional firms already in production. Telecom operators leveraging 5G edge nodes and manufacturing firms adopting smart-factory blueprints are pivotal to regional growth. Rising cyber incidents also fuel spending on automated threat intelligence feeds and managed detection services.

Europe maintains significant share on the back of stringent data protection statutes. The NIS2 directive pushes roughly 350,000 organizations to uplift container orchestration defenses, elevating demand for governance-heavy controls and continuous compliance audits. Financial institutions rely on centralized secrets tools, such as HashiCorp Vault, to reconcile multi-cloud agility with privacy obligations. These dynamics assure steady container security market expansion across the continent.

- Google Cloud Security

- Red Hat (IBM)

- Trend Micro

- Qualys

- Rapid7

- Suse NeuVector

- Mirantis

- Thales

- Sysdig

- Anchore

- Prisma Cloud by Palo Alto

- Tenable

- AccuKnox

- Tigera

- VMware (NSX-ALB)

- Microsoft Defender for Containers

- Capsule8 (Snowflake)

- Fidelis Cybersecurity

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of hybrid and multi-cloud container workloads

- 4.2.2 Rapid shift toward micro-services and DevSecOps pipelines

- 4.2.3 Mandatory security mandates (e.g., PCI-DSS 4.0, NIS2, SBOM)

- 4.2.4 Rising frequency of supply-chain attacks on container images

- 4.2.5 Proliferation of edge and 5G container runtimes

- 4.2.6 Hardware-level container isolation innovations

- 4.3 Market Restraints

- 4.3.1 Shortage of container-security skillsets in DevOps teams

- 4.3.2 Operational complexity of multi-cloud and multi-cluster estates

- 4.3.3 Alert-fatigue and false-positive overload

- 4.3.4 Advanced container-escape kill-chains

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform / Software

- 5.1.2 Services

- 5.2 By Organisation Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Deployment

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.4 By Security Control

- 5.4.1 Image Scanning and Vulnerability Management

- 5.4.2 Runtime Protection and Anomaly Detection

- 5.4.3 Compliance and Configuration Management

- 5.5 By End-user Industry

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Retail and e-Commerce

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Industrial and Manufacturing

- 5.5.6 Others (Media, Education, Gov.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Google Cloud Security

- 6.4.2 Red Hat (IBM)

- 6.4.3 Trend Micro

- 6.4.4 Qualys

- 6.4.5 Rapid7

- 6.4.6 Suse NeuVector

- 6.4.7 Mirantis

- 6.4.8 Thales

- 6.4.9 Sysdig

- 6.4.10 Anchore

- 6.4.11 Prisma Cloud by Palo Alto

- 6.4.12 Tenable

- 6.4.13 AccuKnox

- 6.4.14 Tigera

- 6.4.15 VMware (NSX-ALB)

- 6.4.16 Microsoft Defender for Containers

- 6.4.17 Capsule8 (Snowflake)

- 6.4.18 Fidelis Cybersecurity