|

시장보고서

상품코드

1651059

북미의 우편 서비스 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Postal Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

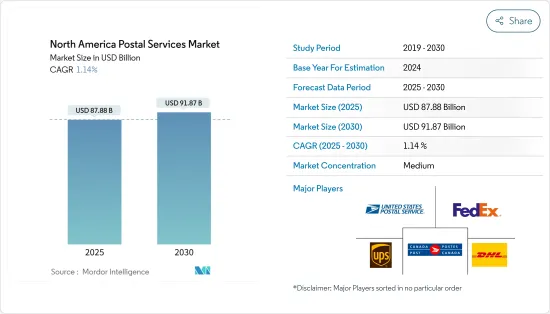

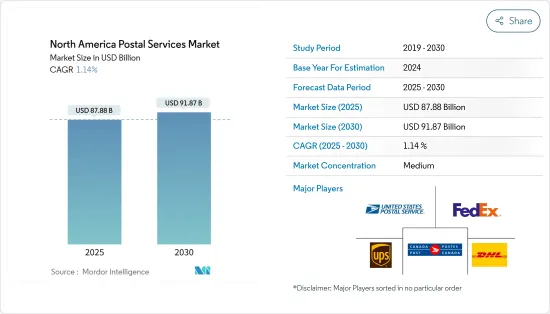

북미의 우편 서비스 시장 규모는 2025년 878억 8,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 1.14%로 2030년에는 918억 7,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 북미에서는 디지털 통신의 부상으로 인해 전통적인 우편물의 양이 감소하고 있습니다. 동시에 E-Commerce의 번영은 택배 및 라스트 마일 물류에 대한 수요 증가를 촉진하고 있습니다. 이러한 상호 연관된 추세는 우편 업계에 변화를 가져오고 있으며, 우편 사업자들에게 서비스 확대와 업무 현대화를 촉구하고 있습니다. 미국 우정공사(USPS)는 미국의 공식적인 우편 사업체이며, USPS의 특급 우편과 직접 경쟁하는 페덱스와 UPS는 긴급한 편지나 소포의 전국 배송 서비스를 제공하고 있습니다.

- 미국 우체국은 독점적 지위를 이용하여 다른 택배업체가 긴급하지 않은 편지를 배달하는 것을 제한하고, 주택이나 사업체의 미국 우편함에 발송하는 것을 금지하고 있습니다. 몇 가지 예외를 제외하고, USPS는 사적 우편물 배달원에게 벌금과 투옥의 가능성을 부과하는 사적 특송 법령에 의해 우편물 배달의 법적 독점권을 유지하고 있습니다. 캐나다에서는 캐나다 우체국이 지배적인 위치를 차지하고 있으며, 소포와 일반 우편물의 대부분을 취급하고 있습니다. 정부가 운영하는 이 서비스는 많은 캐나다인들의 신뢰를 받고 있으며, 소포 3통 중 2통은 캐나다 우체국에서 발송하고 있습니다.

- 2023년 미국의 소포 수입은 7년 만에 감소하여 2022년 1,984억 달러에서 1,979억 달러로 감소했습니다. 이러한 감소는 총 소포 운송량이 2022년 215억 개에서 2023년 217억 개로 0.5% 소폭 증가했음에도 불구하고 발생한 것입니다. 연례 미국 택배 배송 지수에 따르면, 4개 주요 운송업체(미국 우정공사, 아마존 물류, UPS, 페덱스) 중 아마존 물류만 전년 대비 15.7% 증가하며 큰 폭의 성장세를 기록했습니다. 또한 아마존 물류는 택배 취급량에서 페덱스와 UPS를 앞지르며 시장 선두인 USPS에 바짝 다가서고 있습니다. 소식통에 따르면 소규모 운송업체를 포함한 '기타' 카테고리는 매출과 취급량 모두 크게 증가하여 2023년 시장 점유율이 28.5% 증가하여 약 3%(약 6억 개의 소포)에 달했습니다. 소식통에 따르면 2023년 USPS가 66억 개(전년 대비 약 1% 감소)로 1위, 아마존 물류가 59억 개(15.7% 증가), UPS가 46억 개(10.3% 감소), 페덱스가 39억 개(6.1% 감소)를 기록했습니다.

- 최근 몇 년 동안 북미의 우편 서비스 업계는 디지털화의 발전으로 인해 혼란스러운 상황에 직면해 있습니다. 커뮤니케이션의 온라인화가 진행됨에 따라 전통적인 우편 배달 사업은 쇠퇴의 길을 걷고 있습니다. 동시에, 업계는 확대되는 E-Commerce 소포 시장에서 치열한 경쟁에 직면해 있습니다. 그 결과, 우편 및 메일링 사업체는 국영 독점 기업에서 다양한 포트폴리오를 가진 영리 기업으로 진화하고 있습니다.

북미의 우편 서비스 시장 동향

미국이 시장에서 뚜렷한 우위를 점하고 있다

팬데믹 이후 미국의 E-Commerce는 전례 없는 성장을 이루며 다른 많은 국가들의 추세를 반영하게 되었습니다. 인구 3억 3,200만 명의 미국은 인도와 중국에 이어 세계에서 세 번째로 인구가 많은 나라입니다. 주목할 만한 점은 미국 인터넷 사용자의 80%가 온라인 쇼핑을 이용하고 있다는 점입니다. 이러한 E-Commerce의 급격한 증가는 우정사업에 큰 기회가 될 수 있습니다. 소비자들이 신흥 E-Commerce 플랫폼과 기존 오프라인 매장의 온라인화를 점점 더 많이 이용함에 따라 효율적인 배송 및 픽업 채널에 대한 수요가 증가하고 있습니다. 우체국은 전국적인 네트워크와 라스트 마일 배송에 대한 전문성을 바탕으로 이러한 변화하는 환경에서 가치 있는 파트너로 자리매김하고 있으며, 2024년 2분기까지 미국 E-Commerce 매출은 2,916억 4,000만 달러에 달했으며, 전체 소매 매출의 15.9%를 차지합니다. 올해 상반기 미국 E-Commerce 매출은 5,794억 5,000만 달러로 급증했고, 연말에는 1조 2,200억 달러에 달할 것이라는 전망도 있습니다. E-Commerce의 지속적인 성장은 디지털 경제를 뒷받침하는 우정 서비스의 중요한 역할을 강조하고 있습니다.

서신량 감소 추세

미국 우정공사(USPS)는 미국의 공식적인 우정기관으로 2006년 약 2,130억 통을 정점으로 매년 지속적으로 우편물량이 감소하고 있으며, 2023년에는 1,161억 5,000만 통으로 급감할 것으로 예상하고 있습니다. 이러한 감소는 주로 전통적인 우편물, 마케팅 자료, 정기 간행물의 수량 감소에 기인합니다. 이와는 대조적으로, 소포 배송의 수입은 급증하고 있습니다. 이러한 변화의 주요 원인은 기술입니다. 많은 미국인들이 이메일을 사용하게 되면서 전통적인 우편물에 대한 수요가 감소하고 있습니다. 또한 미국의 온라인 소매 판매는 지난 10년 동안 두 배로 증가하여 소포 배송에 대한 수요가 증가하고 있습니다. 캐나다의 공식 우편 서비스인 캐나다 포스트도 이러한 추세를 반영하고 있습니다.

북미의 우편 서비스 산업 개요

업계는 현재 세분화되어 있습니다. 대기업은 광범위한 인프라와 서비스 다양성으로 우위를 점하고 있습니다. 소규모 기업은 전문화를 통해 경쟁하고 있습니다. 정부 소유의 우체국은 일반적으로 우편 배달을 독점하고 있지만, 민간 택배 회사와의 치열한 경쟁에 직면해 있습니다. 경쟁하는 사업체는 서로의 강점을 살리기 위해 제휴를 맺는다. 예를 들어, 대형 특송업체 페덱스(FedEx)와 유나이티드 소포 서비스(UPS)는 특정 주택 배달을 미국 우정공사(USPS)에 위탁하고, USPS는 항공 운송을 페덱스와 UPS에 위탁하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학과 인사이트

- 현재 시장 시나리오

- 시장 성장 촉진요인

- E-Commerce 증가

- 당일·다음날 배송 확대

- 시장 성장 억제요인

- 인건비 상승

- 사이버 보안과 메일 보안

- 시장 기회

- 자동화와 기술 향상

- 밸류체인/공급망 분석

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참여업체의 위협

- 구매자/소비자의 협상력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 유형별

- 특송 우편 서비스

- 정형 우편 서비스

- 품목별

- 레터

- 소포

- 행선지별

- 국내

- 국제

- 지역별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 집중도 개요

- 기업 개요

- USPS

- Canada Post Corporation

- UPS

- DHL

- FedEX

- Purolator

- Correos de Mexico

- Estafeta

- GLS

- APC Postal Logistics

- Santa Lucia Post

- Grenada Postal Corporation

- Paquetexpress

제7장 시장 전망

제8장 부록

- 거시경제 지표

- 운송·보관 GDP 기여도

The North America Postal Services Market size is estimated at USD 87.88 billion in 2025, and is expected to reach USD 91.87 billion by 2030, at a CAGR of 1.14% during the forecast period (2025-2030).

Key Highlights

- In North America, the rise of digital communication has diminished the volume of traditional mail. At the same time, the flourishing e-commerce sector has spurred greater demand for parcel delivery and last-mile logistics. These interconnected trends are transforming the industry, prompting postal operators to expand their services and modernize their operations. The United States Postal Service (USPS) is the official postal entity in the USA. FedEx and UPS, in direct competition with USPS's Express Mail, provide nationwide delivery services for urgent letters and packages.

- Leveraging its monopoly, USPS restricts other U.S. couriers from delivering non-urgent letters and prohibits them from shipping to U.S. mailboxes at residential and business locations. With few exceptions, USPS maintains a legal monopoly on letter delivery, backed by the Private Express Statutes, which impose fines and potential imprisonment on private letter carriers. In Canada, Canada Post is the dominant player, overseeing the majority of both package and traditional mail shipments. This government-run service enjoys the trust of many Canadians, managing the shipment of two out of every three parcels.

- In 2023, US parcel revenue saw its first dip in seven years, falling from USD198.4bn in 2022 to USD197.9bn. This decline came despite a modest 0.5% uptick in total parcel volume, which rose from 21.5 billion in 2022 to 21.7 billion in 2023. The annual US Parcel Shipping Index reveals that among the four primary carriers (USPS, Amazon Logistics, UPS, and FedEx), only Amazon Logistics registered a significant year-over-year (YoY) volume surge of 15.7%. Moreover, Amazon Logistics has surpassed both FedEx and UPS in parcel volumes and is rapidly approaching the market leader, USPS. Sources indicate that the 'others' category, which includes smaller carriers, saw a substantial uptick in both revenue and volume, enhancing their market share by 28.5% in 2023, bringing it to nearly 3%, or about 0.6 billion parcels. According to the sources, in 2023, USPS led in parcel volume with 6.6 billion parcels (a nearly 1% YoY decline), followed by Amazon Logistics at 5.9 billion parcels (a 15.7% increase), UPS with 4.6 billion parcels (a 10.3% decrease), and FedEx at 3.9 billion parcels (down 6.1%).

- In recent years, North America's postal service industry has faced disruptions from the digital landscape. As communication increasingly migrates online, the traditional mail delivery business is witnessing a decline. Concurrently, the industry is grappling with fierce competition in the expanding e-commerce parcel market. As a result, postal and mailing entities are evolving from state-owned monopolies to commercial firms with diversified portfolios.

North America Postal Services Market Trends

United States exhibits a clear dominance in the market

In the wake of the pandemic, e-commerce in the United States has experienced unprecedented growth, mirroring trends seen in many other countries. With a population of 332 million, the U.S. ranks as the world's third most populous nation, trailing only India and China. Notably, nearly 80% of American internet users engage in online shopping. This surge in e-commerce presents a significant opportunity for postal services. As consumers increasingly turn to both emerging e-commerce platforms and traditional brick-and-mortar stores transitioning online, the demand for efficient delivery and collection channels has intensified. Leveraging their established national networks and expertise in last-mile delivery, postal services are positioning themselves as valuable partners in this evolving landscape. By Q2 2024, e-commerce sales in the U.S. reached USD 291.64 billion, constituting 15.9% of the nation's total retail sales. In the first half of the year, U.S. e-commerce sales soared to USD 579.45 billion, with projections suggesting a climb to USD 1.22 trillion by year's end. The continued growth of e-commerce underscores the critical role of postal services in supporting the digital economy.

Letter Volume is on Decline

The U.S. Postal Service (USPS) stands as the official postal authority in the United States. After peaking at approximately 213 billion units in 2006, USPS has witnessed a consistent annual decline in mail volume. By 2023, deliveries had plummeted to a mere 116.15 billion units. This decline is primarily due to reduced volumes in traditional mail, marketing materials, and periodicals. In contrast, revenue from package shipping has surged. Technology is the primary catalyst for this transformation. An increasing number of Americans are turning to email, leading to a reduced appetite for traditional mail. Additionally, U.S. online retail sales have doubled in the last decade, heightening the demand for package deliveries. Canada Post, Canada's official postal service, mirrors this trend.

North America Postal Services Industry Overview

The industry is currently fragmented. Large companies have advantages in widespread infrastructure and diversity of services. Small companies compete by specializing. Government-owned postal agencies typically have a monopoly on mail delivery but face heavy competition from private package delivery companies. The competing entities form partnerships to capitalize on each other's strengths. For instance, major express delivery companies Federal Express (FedEx) and United Parcel Service (UPS) contract certain residential deliveries to the US Postal Service (USPS), while the USPS contracts air transportation out to FedEx and UPS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Drivers

- 4.2.1 Rise In Ecommerce

- 4.2.2 Expansion of Same Day and Next- Day Delivery

- 4.3 Market Restraints

- 4.3.1 Rising Labor Costs

- 4.3.2 Cybersecurity and Mail Security

- 4.4 Market Opportunities

- 4.4.1 Increased Automation and Technology

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Express Postal Services

- 5.1.2 Standard Postal Services

- 5.2 By Item

- 5.2.1 Letter

- 5.2.2 Parcel

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Geography

- 5.4.1 US

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 USPS

- 6.2.2 Canada Post Corporation

- 6.2.3 UPS

- 6.2.4 DHL

- 6.2.5 FedEX

- 6.2.6 Purolator

- 6.2.7 Correos de Mexico

- 6.2.8 Estafeta

- 6.2.9 GLS

- 6.2.10 APC Postal Logistics

- 6.2.11 Santa Lucia Post

- 6.2.12 Grenada Postal Corporation

- 6.2.13 Paquetexpress*

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators

- 8.2 Contribution of Transportation and Storage to GDP