|

시장보고서

상품코드

1683111

자동차용 드라이브 샤프트 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Automotive Drive Shaft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

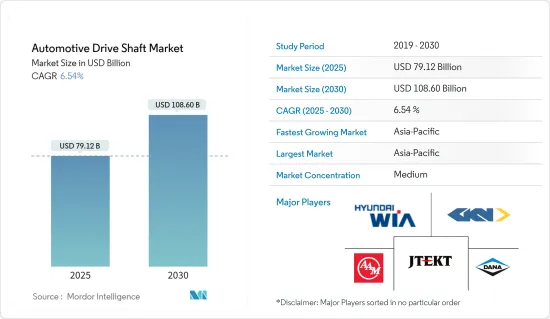

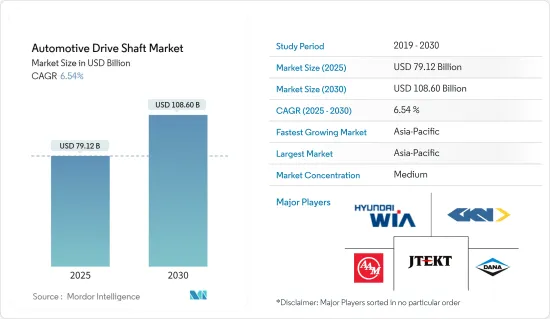

자동차용 드라이브 샤프트 시장 규모는 2025년에 791억 2,000만 달러로 추정되며, 예측 기간 2025년부터 2030년까지 CAGR은 6.54%를 나타낼 전망이며, 2030년에는 1,086억 달러에 달할 것으로 예측됩니다.

중기적으로는 인구와 가처분소득이 증가함에 따라 승용차와 상용차 등 자동차 수요가 세계적으로 확대될 것으로 예상됩니다. 자동차 생산 및 제조 증가는 세계 드라이브 샤프트 수요를 촉진하고 있습니다.

예측기간 중에는 상용차와 버스 수요 증가가 세계 자동차 생산 및 판매의 원동력이 되고, 이 시장이 주목받을 것으로 보입니다. 이 추세는 주로 전기자동차에 대한 수요가 높아지기 때문입니다. 또한 자동차 제조업체는 수요가 증가함에 따라 가장 에너지 효율적인 전기자동차 제조에 최선을 다하고 있습니다. 드라이브 샤프트 제조업체는 지속적으로 변화하는 OEM의 요구를 충족하고 시장 점유율을 확대하기 위해 제품 라인을 업데이트합니다.

전기차의 미래를 고려하여 Volkswagen과 General Motors와 같은 주요 OEM 기업은 신기술에 대한 대규모 투자, 공급망 구축, 전기차 및 부품(배터리 팩 및 모터 등)의 생산 능력을 강화하고 있습니다. 예를 들면

주요 하이라이트

- 2023년 6월, Mercedes-Benz는 유럽 조립 공장에 수십억 달러를 투자하고 10년 후까지 전기자동차로의 전환을 실현할 것이라고 발표했습니다. 이 움직임에는 2025년에 도입된 새로운 전기 플랫폼과 그 부품에 의한 자동차 생산이 포함됩니다.

자동차용 드라이브 샤프트 시장은 경량 부품 수요 증가와 전륜 구동차 판매 증가 등의 동향에 견인되어 향후 수년간 성장할 것으로 예상됩니다. 앞으로 몇 년동안 자동차용 드라이브 샤프트 시장 전체의 성장에 영향을 줄 것으로 예상되는 주목할만한 요인 중 하나는 세계 유틸리티 차량 판매의 급증입니다. 아시아태평양은 신흥 경제권의 존재에 의해 두드러지며 세계 자동차 판매 대수의 약 절반을 차지합니다.

아시아태평양의 자동차용 드라이브 샤프트 시장은 향후 몇 년동안 가장 큰 점유율을 차지하며 가장 높은 성장률을 나타낼 것으로 예상됩니다. 아시아태평양은 신흥 경제국의 존재를 특징으로 하며, 세계 자동차 판매량의 주요 점유율을 차지하며, 이는 예측 기간 동안 계속될 수 있습니다.

중국, 미국, 노르웨이 등 국가에서는 전기자동차에 대한 수요가 계속 증가하고 있습니다. 자동차 제조업체는 향후 몇 년동안 더 많은 EV 모델의 출시를 계획하고 있습니다. 현재 및 향후 EV 모델의 대부분은 전륜 구동(AWD) 또는 후륜구동(FR)이며, 예측 기간 동안 경량 드라이브 샤프트에 대한 수요를 생성할 수 있습니다.

자동차용 드라이브 샤프트 동향

승용차가 시장에서 가장 높은 점유율을 차지합니다.

자동차 시장에서는 세련된 디자인, 크기, 경제성 등의 특징으로 승용차 판매량이 많습니다. 고성능의 고급 SUV에 대한 높은 수요가 이 성장을 뒷받침하고 있습니다. 따라서 많은 기업들이 다양한 신형 승용차의 출시에 주력하고 있습니다. 예 :

- 2023년 5월, Land Rover는 지금까지 가장 강력하고 가장 빠른 시판 SUV의 세부 사항을 발표했습니다. 신형 레인지 로버 스포츠 SV는 슈퍼 충전기를 갖춘 5 리터 V8 엔진으로 635 마력을 발휘합니다.

전기자동차는 자동차산업에 필수적인 존재로 오염물질 및 기타 온실가스의 배출감소와 함께 에너지효율 달성을 위한 길을 제시하고 있습니다. 환경 문제에 대한 관심과 정부의 적극적인 노력이 이러한 성장을 가속하는 주요 요인이 되었습니다.

국제에너지기구(IEA)에 따르면 2024년 1분기 전기차 판매량은 2023년 1분기에 비해 약 25% 증가했으며, 중국이 45%의 최대 점유율을 차지한 다음 유럽이 25%로 나타났습니다.

정부 및 지역 수준의 배기가스 규제는 EV 산업 전반을 추진하는 중요한 요인의 하나가 되고 있습니다. 도로 운송은 일반적으로 유럽에서 유일하게 가장 큰 대기 오염원으로 인식됩니다. 대기오염과 싸우기 위해 EU 이사회는 '환경 대기질 평가 및 관리에 관한 지령 96/62/EC'를 채택하여 대기 중 다양한 유해 화합물의 배출 목표를 정하고 있습니다. 자동차에서 배출되는 가장 중요한 오염물질은 질소산화물(NOx)과 미세먼지(입자상물질-PM)이며, 현재 모두 연간 40g/m3이 상한이 되고 있습니다.

유럽은 2050년까지 기후 중립이 되는 높은 목표를 세우고 있습니다. 유럽 위원회는 이러한 목표를 달성하기 위해 향후 몇 년동안 몇 가지 새로운 법률안을 발표할 예정이며, 그 중 상당수는 모빌리티 개선을 목적으로 하고 있습니다. 이 10년의 끝까지 유럽 위원회는 적어도 3천 만 대의 전기자동차를 보급하는 것을 목표로 하고 있습니다. 이 목표를 달성하기 위해서는 국가, 기업 및 소비자를 올바른 길로 인도하는 일련의 조치와 목표가 필요합니다.

승용차 수요는 정교한 드라이브 샤프트 수요도 밀어 올릴 수 있습니다. 드라이브 샤프트 제조업체는 이러한 자동차 요구 사항을 충족할 수 있는 드라이브 샤프트를 제조하기 위해 새로운 재료 및 제조 방법을 연구하고 있습니다. 예를 들어, 강철 대신 탄소섬유를 사용하여 무게를 최소화하는 제조업체와 높은 토크 수준을 견딜 수 있는 혁신적인 복합재료를 사용하는 제조업체도 있습니다. 예를 들면

- 2023년 1월, 구동 시스템 부품 제조업체인 Kalyani Mobility Drivelines(KMD)는 EV 및 기타 특수 차량용 등속(CV) 드라이브 샤프트 라인업을 발표했습니다.

이러한 요인이나 전기자동차 및 하이브리드 자동차 시장의 확대에 의해 자동차용 드라이브 샤프트 시장은 앞으로도 성장과 진화를 계속할 것으로 예상됩니다.

아시아태평양이 시장에서 큰 점유율을 차지할 전망

중국과 인도는 아시아태평양의 자동차 제조 측면에서 유명한 국가입니다. 이 나라에는 자동차 제조업체가 많이 있으며 예측 기간 동안 시장에 유리한 기회를 만들 수 있습니다.

이 지역 정부는 자동차 판매를 강화하기 위해 많은 인센티브 플랜을 도입했습니다. 또한 이 지역의 자동차 산업 확대를 장려하기 위해 전기자동차 구매에 대한 보조금도 제공합니다. 예 :

- 승용차의 판매량과 생산량이 증가함에 따라 인도 자동차 산업은 전년 동기 대비 비약적인 성장을 이루고 있습니다. 예를 들어, 2022-2023년의 승용차 판매 대수는 전년도 대비 146만 7,039대에서 174만 7,376대로, 다목적차는 148만 9,219대에서 200만 3,718대로, 밴은 11만 3,265대에서 13만 9,020대로 증가했습니다.

인도 경제는 중간 소득층의 가처분 소득이 증가하고 확대하고 있습니다. 이것은 자동차 수요에 긍정적인 영향을 미칩니다. 자동차 생산은 인도의 저렴한 생산 비용으로 지난 5년간 급증했습니다. 자동차 제조 증가에 따라 자동차용 센서 시장도 견인력을 늘리고 있습니다.

인도 도시의 자동차 보유 대수는 평균 차령이 각각 8년, 11년인 EU 국가와 미국보다 훨씬 젊습니다.

주요 자동차 부품 제조업체는 이 지역 전체에서 제조 시설을 확대하고 신제품을 투입하고 있습니다. 예측 기간 동안 이러한 자동차 부품 제조업체는 시장에서 큰 성장을 이룰 것으로 예상됩니다. 예를 들어, KYB Corporation(KYB)은 2023년 3월까지 전기자동차(EV)의 eAxle 구동 모터 시스템용 전동 오일 펌프를 개발할 계획을 발표했습니다. 또한 이 회사는 eAxle의 윤활 및 냉각용 오일 펌프를 제조하여 전동화 시대의 신규 사업으로 개발할 계획도 발표하고 있습니다.

이처럼 아시아태평양의 자동차용 드라이브 샤프트 시장은 이러한 시장 개척과 동향을 고려하면 예측 기간 동안 큰 성장이 예상됩니다.

자동차용 드라이브 샤프트 산업 개요

자동차용 드라이브 샤프트 시장은 세계 기업 및 지역적으로 확립된 기업에 의해 통합되고 주도되고 있습니다. 이들 기업은 시장에서의 지위를 유지하기 위해 신제품 출시, 제휴, 합병 등의 전략을 채택하고 있습니다. 예를 들면

- 2023년 9월, JTEKT North America는 JTEKT Automotive Systems, Koyo Bearings, Toyoda Machine Tools 브랜드로 광범위한 제품을 제조했습니다. 7개의 새로운 기계 라인, 2개의 새로운 조립 라인, 부품을 내부에서 가공하기 위한 추가 공정을 추가함으로써 JTEKT North America는 전면 드라이브 샤프트의 생산 능력을 확대했습니다.

이 시장의 주요 기업으로는 GKN PLC(Melrose Industries PLC), Yamada Manufacturin, American Axle & Manufacturing Inc., JTEKT Corporation, Dana Incorporated 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- EV 판매 촉진을 위한 정부 시책 증가

- 시장 성장 억제요인

- 드라이브 샤프트에 대한 높은 유지 보수 비용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화(시장 규모 : 달러)

- 설계 유형별

- 중공 샤프트

- 솔리드 샤프트

- 포지션 유형별

- 리어 액슬

- 프론트 액슬

- 차종별

- 승용차

- 상용차

- 유통 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 기타

- 남미

- 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- GKN PLC(Melrose Industries PLC)

- JTEKT Corporation

- Dana Holding Corporation

- Hyundai Wia Corporation

- Nexteer Automotive Group Ltd

- Showa Corporation

- Yamada Manufacturing Co. Ltd

- American Axle & Manufacturing Co. Ltd

- Wanxiang Qianchao Co. Ltd

- NTN Corporation

제7장 시장 기회 및 향후 동향

AJY 25.03.31The Automotive Drive Shaft Market size is estimated at USD 79.12 billion in 2025, and is expected to reach USD 108.60 billion by 2030, at a CAGR of 6.54% during the forecast period (2025-2030).

Over the medium term, with the rising population and disposable income, the demand for automobiles, such as passenger cars and commercial vehicles, is expected to grow worldwide. The increasing production and manufacturing of automobiles are fueling the demand for drive shafts globally.

The market will likely be the focus of attention during the forecast period, driven by the growing demand for commercial vehicles and buses, both of which are expected to drive global vehicle production and sales. This trend is primarily due to the growing demand for electric vehicles. In addition, automakers are putting all their efforts into making the most energy-efficient electric vehicles as their demand grows. Driveshaft manufacturers are updating their product lines to meet the constantly shifting needs of OEMs and expand their market share.

Considering the future of electric vehicles, the major OEM companies, including Volkswagen and General Motors, are investing majorly in new technology, establishing supply chains, and increasing the production capacity of EVs and their components, such as battery packs and motors. For instance:

Key Highlights

- In June 2023, Mercedes-Benz announced an investment of billions in its European assembly plants to equip them for the shift to electric cars by the end of the decade. This move involves the production of vehicles on the new electric platforms and their components to be introduced in 2025.

The automotive drive shaft market is anticipated to grow in the coming years, driven by trends such as the rising demand for lightweight components and the increasing sales of all-wheel-drive vehicles. One notable factor that is anticipated to impact the overall growth of the automotive drive shaft market in the coming years is the sharp increase in utility vehicle sales worldwide. Asia-Pacific is distinguished by the presence of emerging economies and accounts for about half of global vehicle sales.

The Asia-Pacific automotive drive shaft market is expected to hold the largest share and register the highest growth rate in the coming years. Asia-Pacific is characterized by the presence of emerging economies and accounts for a major share of global vehicle sales, which may continue over the forecast period.

Countries such as China, the United States, and Norway are continuing to see stronger demand for electric vehicles. Automakers are planning to launch more EV models in the coming years. The majority of the present and upcoming EV models are all-wheel drives (AWD) or rear-wheel drives (RWD), which may generate the demand for lightweight drive shafts during the forecast period.

Automotive Drive Shaft Market Trends

Passenger Cars Hold the Highest Share in the Market

Passenger car sales are high in the automotive market due to features such as stylish design, size, and economic value. High demand for luxury SUVs with high performance propels this growth. Therefore, many companies are focusing on the launch of various new passenger car models. For instance:

- In May 2023, Land Rover released details about its most powerful and fastest production SUV yet. The new Range Rover Sport SV packs 635 hp with a supercharged 5-liter V8 engine.

Electric vehicles have become an integral part of the automotive industry, and they represent a pathway toward achieving energy efficiency, along with reduced emissions of pollutants and other greenhouse gases. The growing environmental concerns and favorable government initiatives are the major factors driving this growth.

According to the International Energy Agency, in Q1 2024, electric car sales grew by around 25% compared to Q1 2023, with China holding the largest share of 45%, followed by Europe with 25%.

Emission laws at the governmental and regional levels have been one of the key causes propelling the EV industry in general. Road transport is commonly acknowledged as the single-largest source of air pollution in Europe. To combat air pollution, the EU Council adopted "Directive 96/62/EC on ambient air quality assessment and management," which establishes emission targets for various harmful compounds in the atmosphere. The most important pollutants produced by cars are nitrogen oxides (NOx) and fine dust (particulate matter - PM), both of which are now capped at 40 g/ m3 per year.

Europe has set a lofty target of being climate-neutral by 2050. The European Commission plans to publish several new legislative proposals over the next few years to meet this goal, many of which are aimed at improving mobility. By the end of this decade, the European Commission aims to have at least 30 million electric vehicles on the road, a tremendous increase from the current 1.4 million EVs on European roads. To achieve this aim, a set of policies and targets must be in place to guide states, businesses, and consumers on the correct path.

The demand for passenger cars may also boost the demand for sophisticated drive shafts. Manufacturers of drive shafts are researching novel materials and manufacturing procedures to build drive shafts that can handle the requirements of these vehicles. Some producers, for example, use carbon fiber instead of steel to minimize weight, while others use innovative composite materials that can withstand high torque levels. For instance:

- In January 2023, Kalyani Mobility Drivelines (KMD), a manufacturer of driveline components, introduced a lineup of constant-velocity (CV) driveshafts for EVs and other specialty vehicles.

Owing to such factors and the expansion of the electric and hybrid vehicle market, the automotive drive shaft market will likely continue to grow and evolve.

Asia-Pacific is Expected to Hold a Significant Share in the Market

China and India are the prominent countries in terms of vehicle manufacturing in Asia-Pacific. The countries have a major presence of automotive manufacturers, which may create lucrative opportunities for the market during the forecast period.

The governments in the region have introduced many incentive plans to bolster auto sales. They are also offering subsidies on the purchase of electric vehicles to encourage the expansion of the region's automotive industry. For instance:

- With the growing sales and production of passenger cars, the Indian automotive industry has been witnessing exponential growth Y-o-Y. For instance, sales of passenger cars increased from 14,67,039 to 17,47,376 units, utility vehicles from 14,89,219 to 20,03,718 units, and vans from 1,13,265 to 1,39,020 units in FY 2022-23 compared to the previous financial year.

The Indian economy is expanding as there is a rise in the disposable income of middle-income consumers. This factor, in turn, has a favorable impact on the demand for automobiles. Vehicle manufacturing has increased rapidly over the last five years due to the country's cheap production costs. The automotive sensor market is gaining traction as vehicle manufacturing increases.

The vehicular fleet in Indian cities is much younger than in EU nations and the United States, where the average age of cars is eight years and 11 years, respectively.

Major automotive component manufacturers are expanding their manufacturing facilities and introducing new products across the region. They are expected to witness major growth in the market during the forecast period. For example, KYB Corporation (KYB) announced plans to develop electric oil pumps for eAxle drive motor systems in electric vehicles (EVs) by March 2023. The company also announced plans to build oil pumps for lubricating and cooling eAxles and develop them as a new business for the era of electrification.

Thus, considering such developments and trends in the market, the Asia-Pacific automotive drive shaft market is expected to have significant growth during the forecast period.

Automotive Drive Shaft Industry Overview

The automotive drive shaft market is consolidated and led by global and regionally established players. These companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions. For instance:

- In September 2023, JTEKT North America manufactured a broad range of products under the JTEKT Automotive Systems, Koyo Bearings, and Toyoda Machine Tools brands. By adding seven new machine lines, two new assembly lines, and additional processes to machine components internally, JTEKT North America expanded its capability to produce front drive shafts.

Some of the major players in the market include GKN PLC (Melrose Industries PLC), Yamada Manufacturing Co. Ltd, American Axle & Manufacturing Inc., JTEKT Corporation, and Dana Incorporated.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Government Policies to Promote EV Sales

- 4.2 Market Restraints

- 4.2.1 High Cost of Maintenance Related to Drive Shafts

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Design Type

- 5.1.1 Hollow Shaft

- 5.1.2 Solid Shaft

- 5.2 By Position Type

- 5.2.1 Rear Axle

- 5.2.2 Front Axle

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 GKN PLC (Melrose Industries PLC)

- 6.2.2 JTEKT Corporation

- 6.2.3 Dana Holding Corporation

- 6.2.4 Hyundai Wia Corporation

- 6.2.5 Nexteer Automotive Group Ltd

- 6.2.6 Showa Corporation

- 6.2.7 Yamada Manufacturing Co. Ltd

- 6.2.8 American Axle & Manufacturing Co. Ltd

- 6.2.9 Wanxiang Qianchao Co. Ltd

- 6.2.10 NTN Corporation