|

시장보고서

상품코드

1683195

샌드위치 패널 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Sandwich Panels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

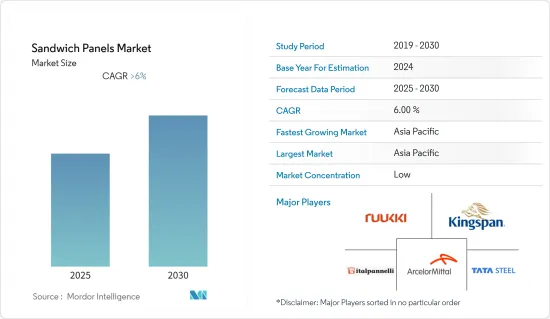

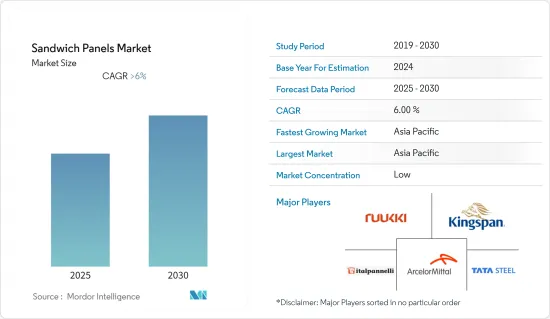

샌드위치 패널 시장은 예측 기간 동안 CAGR 6% 이상을 기록할 전망.

COVID-19 팬데믹으로 시장은 부정적인 영향을 받았습니다. 팬데믹의 시나리오로 인해 세계 여러 국가가 봉쇄되었습니다. 건설 공사는 공급망 혼란, 자금 부족, 노동력 부족, 봉쇄 규제로 인해 일시적으로 중단되었습니다. 샌드위치 패널 시장은 팬데믹에서 회복하고 크게 성장하고 있습니다.

주요 하이라이트

- 단기적으로 저온 저장 시설에서 샌드위치 패널 수요가 증가가 시장을 견인할 것으로 보입니다. 또한 PVDF 기반 알루미늄 복합 패널의 사용도 시장 수요에 기여할 것으로 보입니다.

- 그러나 일부 샌드위치 패널은 방화 성능이 낮기 때문에 시장 성장 억제요인이 될 것으로 예상됩니다.

- 산업용 건물과 상업용 건물의 건설이 증가하고 있는 것은 샌드위치 패널 시장에 대한 예측 기간 동안 큰 성장 기회입니다.

- 아시아태평양은 중국, 일본, 인도 등 국가에서 엄청난 소비로 시장을 독점할 것으로 예상됩니다.

샌드위치 패널 시장 동향

시장을 독점하는 산업 부문

- 현대 건축에서는 고성능 재료의 사용이 필수적입니다. 고성능은 강도가 높고 가볍고 내구성이 있으며 다양한 용도로 사용할 수 있는 재료입니다. 이러한 신뢰성으로 인해 샌드위치 패널은 산업용 건물에 가장 적합한 옵션 중 하나가 될 수 있습니다.

- 그 용도는 산업용 빌딩의 건설부터 단열 지붕 및 벽 패널까지, 다방면에 걸쳐 있습니다. 샌드위치 패널은 산업용도, 특히 저온 저장 시설과 창고에서 수요가 높습니다.

- 신선한 농산물, 해산물, 냉동식품, 사진필름, 화학제품, 의약품의 보존기간을 연장 및 확보하기 위한 냉장창고의 수는 급속히 증가하고 있습니다.

- 다국적 기업에 의한 식품 소매 체인의 확대는 냉장 창고 수요 증가로 이어졌습니다. 이러한 요인들로 인해 샌드위치 패널 수요는 전 세계적으로 확대될 것으로 예상됩니다.

- 세계 콜드체인 물류 시장은 2021년 2,558억 2,000만 달러 규모에 이르렀으며, 향후 8년간 4,100억 달러 이상에 달할 것으로 예상됩니다.

- 아시아태평양의 콜드체인 물류 시장 규모는 2020년 617억 5,000만 달러에 비해 2021년에는 689억 7,000만 달러에 달했습니다. 향후 6년간 이 시장은 1,340억 달러 미만에 이를 것으로 예상됩니다.

- 유럽의 콜드체인 물류 산업은 2021년에 850억 달러 이상으로 평가되었으며, 2025년에는 1,128억 달러로 성장할 것으로 예상됩니다. 신선한 농산물, 수산물, 냉동 식품, 의약품 등 제품의 품질을 보호하기 위해 냉장 포장 솔루션을 이용한 공급망을 따라 온도 제어된 물품의 이동. 콜드체인 물류로 알려져 있습니다.

- 인도 제약 협회에 의하면, 2021년까지 인도의 콜드체인 창고의 3분의 2 이상을 의약품이 차지했다고 합니다. 저렴한 제조 비용과 정부 보조금으로 인도에는 세계 3위 의약품 사업이 있습니다.

- 위와 같은 요인이 산업 부문을 견인하고 예측 기간 동안 샌드위치 패널 수요를 높일 것으로 예상됩니다.

아시아태평양이 세계 시장을 독점

- 아시아태평양은 중국, 인도, 일본 등 국가에서 높은 수요로 세계 시장을 독점할 것으로 예상됩니다.

- 중국은 아시아태평양에서 건설 활동이 활발한 주요 국가 중 하나이며, 공업 및 건설 부문이 GDP의 약 50%를 차지하고 있습니다.

- 중국건설업 협회에 따르면 2021년 중국에서는 완성된 건축물 중 주택이 큰 비율을 차지했습니다. 주택용 건축물은 완성층 면적의 67% 이상을 차지하고 있습니다. 이 나라의 경제 성장에 따라 사람들은 지방에서 대도시로 이주하여 이러한 장소에서 주택 수요가 증가하고 있습니다. 또한 투자용 부동산으로 이용되는 아파트도 수요를 끌어올리고 있습니다.

- 인도에서는 향후 4-5년 사이에 신선품의 비축 문제에 대처하기 위해 냉장 창고의 설치 및 개량에 2,100억 루피(25억 3,000만 달러)의 투자가 계획되고 있습니다. 기존 냉장 창고의 기계 및 기술을 업그레이드하는 것이 시급합니다.

- 일본의 건설 부문은 공공 및 민간 인프라 투자, 신재생 에너지, 상업 프로젝트 증가로 향후 5년간은 완만하게 확대될 것으로 예상됩니다.

- 국토교통성에 따르면 2021년도 일본의 건축건설 투자는 42조 6,000억 엔(3,199억 3,000만 달러)을 넘어섰습니다. 올해 투자의 대부분은 주택건설이었습니다. 2022년도 건설투자는 43조 4,000억 엔(3,259억 3,000만 달러)으로 증가했습니다.

- 따라서 위의 모든 요소는 예측 기간 동안 샌드위치 패널 시장 수요를 증가시킬 가능성이 높습니다.

샌드위치 패널 산업 개요

샌드위치 패널 시장은 세분화되어 있으며, 수많은 진출 기업들이 시장 수요를 나누고 있습니다. 시장의 주요 기업으로는 ArcelorMittal, ITALPANNELLI SRL, Rautaruukki Corporation, Tata Steel, Kingspan Group 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 구조용 단열 패널의 냉장 창고 용도로 확대

- PVDF 기반 알루미늄 복합 패널 수요 증가

- 성장 억제요인

- 일부 샌드위치 패널의 방화 성능

- 배향 꼬임판(OSB)의 휘발성 유기 화합물(VOC) 배출량

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

- 심재별

- 폴리우레탄(PUR)

- 폴리이소시아누레이트(PIR)

- 미네랄 울

- 발포 폴리스티렌(EPS)

- 기타 심재

- 표피재별

- 상용 섬유 강화 열가소성 플라스틱(CFRT)

- 유리 섬유 강화 패널(FRP)

- 알루미늄

- 스틸

- 기타 표피재

- 용도별

- 벽 패널

- 지붕 패널

- 단열 패널

- 기타

- 최종 용도 부문별

- 주택용

- 업무용

- 산업용

- 시설 인프라

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율(%)** 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- ArcelorMittal

- Areco

- Assan Panel AS

- Building Components Solutions LLC

- Cornerstone Building Brands

- DANA Group of Companies

- ITALPANNELLI SRL

- Kingspan Group

- Multicolor Steels(India) Pvt Ltd

- Rautaruukki Corporation

- Safal group

- Sintex

- Tata Steel

제7장 시장 기회 및 향후 동향

- 산업 및 상업 빌딩의 건설 증가

- 기타 기회

The Sandwich Panels Market is expected to register a CAGR of greater than 6% during the forecast period.

The market was negatively impacted due to the COVID-19 pandemic. Owing to the pandemic scenario, several countries around the world went into lockdown. Construction works were halted temporarily due to supply chain disruptions, lack of funds, labor shortages, and lockdown restrictions. The sandwich panels market recovered from the pandemic and is growing significantly.

Key Highlights

- Over the short term, the rising demand for these panels from cold storage facilities is expected to drive the market. Moreover, the usage of PVDF-based aluminum composite panels is also expected to contribute to the market demand.

- However, the low fire performance of some sandwich panels is expected to restrain the market.

- Nevertheless, increasing the construction of industrial and commercial buildings is a significant growth opportunity for the sandwich panels market over the forecast period.

- Asia-Pacific region is expected to dominate the market with enormous consumption from countries such as China, Japan, and India.

Sandwich Panel Market Trends

Industrial Segment to Dominate the Market

- In modern-day construction, the use of high-performance materials is essential. High performance entails that the material is strong, lightweight, and durable and can be used in various applications. For this reliability, sandwich panels can be one of the best options for industrial buildings.

- The vast spectrum of applications includes everything from industrial building construction to insulated roof and wall panels. Sandwich panels are in high demand in industrial applications, particularly in cold storage facilities and warehouses.

- The number of cold storage operations meant to extend and ensure the shelf life of fresh agricultural produce, seafood, frozen food, photographic film, chemicals, and pharmaceutical drugs is rapidly increasing.

- Multinational companies' expansion of retail food chains led to increased demand for cold storage. These factors, in turn, are expected to augment the demand for sandwich panels across the globe.

- The global cold chain logistics market was worth USD 255.82 billion in 2021 and is expected to exceed USD 410 billion over the next eight years.

- The Asia-Pacific cold chain logistics market was valued at USD 68.97 billion in 2021, compared to USD 61.75 billion in 2020. Over the next six years, this market is expected to reach just under USD 134 billion.

- The European cold chain logistics industry was valued at more than USD 85 billion in 2021 and is predicted to grow to USD 112.8 billion by 2025. The temperature-controlled items movement along a supply chain utilizing chilled packaging solutions to protect the quality of products such as fresh agricultural commodities, seafood, frozen food, or pharmaceutical products. It is known as cold chain logistics.

- According to the Indian Pharmaceutical Association, pharmaceutical items accounted for over two-thirds of India's cold chain storage by 2021. Due to cheap manufacturing costs and government subsidies, India includes the world's third-biggest pharmaceutical business.

- All the above factors are expected to drive the industrial segment, enhancing the demand for sandwich panels during the forecast period.

Asia-Pacific Region to Dominate the Global Market

- Asia-Pacific region is expected to dominate the global market due to the high demand from countries such as China, India, and Japan.

- China is one of the major countries in Asia-Pacific with ample construction activities, with the industrial and construction sectors accounting for approximately 50% of the GDP.

- According to China Construction Industry Association, in 2021, residential buildings accounted for a significant share of finished construction in China. Buildings intended for housing accounted for over 67% of finished floor space. As the country's economy grows, people migrate from rural regions to major cities, increasing demand for residential accommodation in these locations. Furthermore, flats utilized as investment properties also drive up demand.

- In India, in the next 4-5 years, INR 21,000 crore (USD 2.53 billion) is planned to be invested in setting up or upgrading cold storage to address the stockpiling perishable commodities problem. There is an urgent need to upgrade the existing cold storage plant machinery and technology.

- Japan's construction sector is expected to expand moderately over the next five years, owing to increasing public and private infrastructure investments, renewable energy, and commercial projects.

- According to The Ministry of Land, Infrastructure, Transport, and Tourism (Japan), building construction investments in Japan were over JPY 42.6 trillion (USD 319.93 billion) in the fiscal year 2021. Most of the investments were made that year to construct residential houses. Building construction investment raised to JPY 43.4 trillion (USD 325.93 billion) in the fiscal year 2022.

- Thus, all the above factors will likely increase demand for the sandwich panels market during the forecast period.

Sandwich Panel Industry Overview

The sandwich panels market is fragmented, with numerous players sharing the market demand. Key players in the market include ArcelorMittal, ITALPANNELLI SRL, Rautaruukki Corporation, Tata Steel, and Kingspan Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Cold Storage Applications of Structural Insulated Panels

- 4.1.2 Increasing Demand for PVDF-based Aluminum Composite Panels

- 4.2 Restraints

- 4.2.1 Fire Performance of Some Sandwich Panels

- 4.2.2 Oriented Stranded Board (OSB) Emissions of Volatile Organic Compounds (VOCs)

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 Core Material

- 5.1.1 Polyurethane (PUR)

- 5.1.2 Polyisocyanurate (PIR)

- 5.1.3 Mineral Wool

- 5.1.4 Expanded Polystyrene (EPS)

- 5.1.5 Other Core Materials

- 5.2 Skin Material

- 5.2.1 Continuous Fiber Reinforced Thermoplastics (CFRT)

- 5.2.2 Fiberglass Reinforced Panel (FRP)

- 5.2.3 Aluminum

- 5.2.4 Steel

- 5.2.5 Other Skin Materials

- 5.3 Application

- 5.3.1 Wall Panels

- 5.3.2 Roof Panels

- 5.3.3 Insulated Panels

- 5.3.4 Other Applications

- 5.4 End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Institutional and Infrastructure

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 Areco

- 6.4.3 Assan Panel A.S.

- 6.4.4 Building Components Solutions LLC

- 6.4.5 Cornerstone Building Brands

- 6.4.6 DANA Group of Companies

- 6.4.7 ITALPANNELLI SRL

- 6.4.8 Kingspan Group

- 6.4.9 Multicolor Steels (India) Pvt Ltd

- 6.4.10 Rautaruukki Corporation

- 6.4.11 Safal group

- 6.4.12 Sintex

- 6.4.13 Tata Steel

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Construction of Industrial and Commercial Buildings

- 7.2 Other Opportunities